“Evaluating the Impact of Advertisement on Buying Behavior: A study of Financial

Service Sector”

|

Pallavi

Research Scholar

Guru Nanak Dev University,

Amritsar

|

Dr. Rishi Raj Sharma

Astt. Prof.,

RC- Gurdaspur

Guru Nanak Dev University, Amritsar

|

Abstract

The wide spread of media provides a lot of awareness among the public regarding

all the changes and innovations that are taking place all around the globe. The

technology when combined with the media makes it more easily to reach to the maximum

number of customers. Therefore, the present paper intended to find the influence

of the advertisement on the buying behavior towards banking and financial sector.

The paper tries to explore the various factors which will affect the customers when

they select the specific banking and financial services. Further, the paper will

find the single factor which has the highest impact on the customers purchase decisions.

The research objectives of the paper will be obtained by applying the Factor Analysis

on the collected data and afterwards the regression analysis in order to find the

relationship between the various factors and to identify the single prominent factor

which has highest impact.

Keywords: Advertisement, Banking and Financial Services, Buying Behavior,

Customer purchase decisions

Introduction

Advertisement plays an important role in the society, and now financial sector is

no exception to this. It generates the awareness between the consumers about the

recent products which are being offered to them. It also creates a relationship

between the company and the consumer. Advertisement helps Financial Institutions

to makes an attempt to change or reinforce the attitude of the customer, reader

and viewer towards the advertised products. Most of the advertisements creator intended

to increase the sales of goods and further to establish a brand image in the mind

of the customers. Therefore they had embedded message with factual information and

various hidden intentions. Advertising can be used to change the views of the reader/viewer

toward the product or service, to gain public opinion and political support by having

some effect as desired by advertisers.

The next major consideration is how the advertisement plays an important role in

the introduction of new products and services. This can be answered that advertisement

helps to change the buyer’s attitude by introducing to some of the features, the

process of manufacturing, how the design and packaging look like, what are the benefits

that it will give to the customers when they will buy. (Sidhu, 2003 ).In order to

deliver the desired message to the general public all the available media is used

like print media, electronic media, internet resources etc. ( http://www.managementparadise.com).

The main objective of the present study is to analyze the major determinants which

will have impact on the customers buying intention and play an important role in

their decision. The paper is divided into critically examination of the literature

available, data interpretation of the collected data with the help of questionnaire,

application of the data analysis technique so as to withdraw the important factors

from the collected data, analyzing of the results and the conclusion.

Literature Review

The competition in the financial services has increased a lot in the last decade.

One of the probable reasons is the globalization. Carter et al (2001) explored the

effect of the increasing globalization and its effect on the financial industry.

In order to understand these effect the customer panel’s reports, sales technology

tools and other important information parameters of the three financial firms GE

Capital, Fidelity Investments in London and Morgan Stanley Dean Witter were examined.

In the time of high competition, the various firms try to attract the customers

by adopting the various innovative and different features. Ryals (2001) explored

the implementation of the advanced IT services in the financial services in UK.

By adopting the more advanced IT services more and more customers will buy your

products and it will help to maintain a strong customer relationship with the customers.

By analysing the collected data with the means of the depth interviews, the study

concluded that adopting the essential technology enabled services will result in

the strong customer relationship as customer are benefited by the more advanced

services.

The financial service provider should adopt the better distribution channels in

order to reach maximum consumers. Gupta and Westal (1994 ) explored the relationships

between pricing policy and distribution channels. The study determined the relationship

between the tree parties manufacturer, distributor and the customer. Targeting to

maximum customers is the foremost objective of the financial service provider but

due to the constraint of the price dimensions, firms need to understand all these

relationships and determine their strategies according to that.

Apart from the distribution channels, marketing is important. Ekerete (2005) analyzed

the depth of the marketing strategies that are adopted by the banks present in the

Nigeria. In order to fulfill the objective the data had been collected from depth

interviews and the questionnaire. After analyzing the collected data, the results

showed that there is a positive impact of the marketing activities on the profitability

and image of the banks.

As more and more banks and financial service provider are there, it has resulted

in the increased competition in the banking industry. Therefore, nowadays customer

demands more portfolios of the banking services. Sadeghi and Bemani (2011) analyzed

the banking service quality of the financial service providers in the strong competition.

The data had been collected from the customers of the Eghtesad-e-Novin bank. The

results of the study concluded that there bank understand their banking needs as

per there expectation.

Ekankumo and Henry (2011) examined the relevance of sales Promotion strategies of

the banking industry in Nigeria generally, and Bayelsa State specifically. It also

attempted to evaluate the extent and relative impact of sales promotion on the development,

growth, and survival of banks.

Hooman (2008) examined the hidden

drivers for the price and quality factors behind the financial services. These factors

were measured using the multi item scales for the six financial services. The results

concluded that price seems to be the important parameter in the financial services.

Also, consumer knowledge about the price and more and more advertisements exposure

increased the knowledge of the customers about their financial service provider.

Lindholm (2008) examined whether customer behavior is influenced by the promotion

activities in the case of the financial services. The post behavior of the respondents

was analyzed by observing the credit card purchases in three segments pre purchase

behavior, during and post purchase after the promotional periods.

As the markets are very dynamic therefore the manufacturers are interested in finding

factors influencing attitude towards advertising. Past studies suggested that advertisement

used by the individuals three basis purposes viz. information seeking, entertainment,

social expression and may influence attitude towards advertising. Bamoriya and Singh

(2011) investigated the role of the demographic variables with the information seeking

behavior of the respondent. Also, the various sources of information that were used

by the respondents.

We can define the term advertising as a form of communication intended to encourage

buy or react on upon products, information, or services etc. Saleen

S. (2011) investigated the relationship between variables which will affect the

attitude and the emotion in the consumer buying behavior in the financial and banking

products.

Imam A. (2011) analyzed the customers buying behavior in financial industry with

special focus on Life insurance products. The study found that the customer satisfaction

and behavior is important for any business to grow and achieve their objectives.

Nowadays more and more financial industry is depending upon the mobile phone for

promotion and advertisement, for most of the operations. Dass and Pal (2011) analyzed

the adoption of the mobile banking nowadays. The study analyzed the strength of

the factors which play an important role through a scoring model.

Dogra (2012) analyzed the role of advertising on the investor’s behavior.

The study specially focuses on the financial product mutual fund. The study concluded

that consumer’s investment decisions are not based on the advertisement as high

parameter of risk is associated in the mutual funds.

Some of the studies reveal that during the past few years the competition in banking

industry have been growing in Iran, which resulted that banks find difficult to

attain a big market share. Danaei (2013) analyzed the effect of advertisements

on the willingness of the customers in case of the banking and financial services.

The results of the study showed that customer awareness towards brand name affect

the customer to willingly accept the banking services of that particular bank.

Mohammed (2012) explored the factors that play an important role in effectiveness

of the online advertisements. The results of the study revealed that internet skills,

advertisement content, advertisement location, income play an important role in

the impact of the advertisement.

Financial advertizing includes advertizing performed by banks, financial institutions,

insurance companies and investment companies. Mylonakis (2008) examined the role

and objectives of financial advertizing and its impact on bank customers regarding

specific banking products, like banking accounts, credit cards, consumer loans,

housing loans, interviews and analyzed by content analysis techniques.

Beckett et al. (2000) purposed a model in order to describe the consumer behavior

while the purchasing of financial services and products. The research finding showed

that consumer purchasing behavior is to a great extent affected by the type of financial

product being purchased. Further, the findings were examined to recognize suitable

strategies which are helpful to increased customer maintenance and profitability.

Krishnan (1999) opined a model for evaluating the customer’s feedback into the final

actions so that there will be improvement in overall customer satisfaction with

financial services. The results of the study demonstrated that product offerings

were the main parameter in satisfaction of the customer. Also the quality of telephone

and branch services also influences the satisfaction.

Howcroft et.al (2010) examined the consumer purchase intentions, attitudes and motivation

during the purchase of the financial products. The results revealed that the financial

service provider should have better understanding of their customer behavior which

influence their attitude while selection and then final purchase of financial products

including the banking , insurance and investment products.

Izquierdo et al (2008) investigated the ways so that the customers can be converted

into valued customers which remain loyal to financial service provider and bring

new customers. The study found a strong relationship between consumer loyalty and

the value which a client can obtain.

Need of the study

Advertising has become a part of our everyday life. Advertisement serves the purpose

of a guide for ‘buying’ in which the intended message is delivered to masses through

various media. A number of studies had been done which described the attitudes of

the customers towards the financial service providers and their financial products.

Some researchers have even discussed the role of advertising in persuading the consumers

to choose a particular set of service. Even some studies could be cited out which

have dwelled upon different marketing models in the developed nations as far as

the marketing of financial services is concerned. But, there is dearth of literature

in the studies related to the advertising in Banking and financial Sector and their

impact upon the perceptual framing of the respondents and also upon the impact of

these advertisements upon the purchase behavior of the respondents.

Objectives of the Study

The main objective of the research paper is to explore the respondent’s perception

towards the financial service advertisements and to measure the impact of these

advertisements on the purchase behavior of the respondents towards different financial

products/ services advertised.

Research Methodology

Convenience sampling technique was adopted. Surveyed customers consist of all those

customers who had purchased financial products. The data had been collected from

the Non Metro region- Mathura and metro region- New Delhi and Noida. 110 questionnaires

were distributed out of which 92 were found completely filled by the respondents.

Thus a total percentage of response rates were 83.6%.

The questionnaire was designed in such a way to collect information about the financial

and banking products consumers had purchased and the role of various factors they

considered while selecting banking and financial service provider. In order to achieve

the above said objectives, likert type scaling was used; multiple choice questions

were given to the respondent. The likert scale was divided into five dimensions

[Strongly Agree (5) and Strongly Disagree (1)]. Twenty different statements were

included in this category and most of these were derived from available literature

from current banking and financial.

Reliability test was conducted for these statements. The cronbach alpha value was

0.838 as above .06 is acceptable (see Appendix I). The questionnaire also included

the demographic information about respondents such as his/her Gender, Marital Status,

Age group, Monthly income and qualifications.

Analysis and Discussion

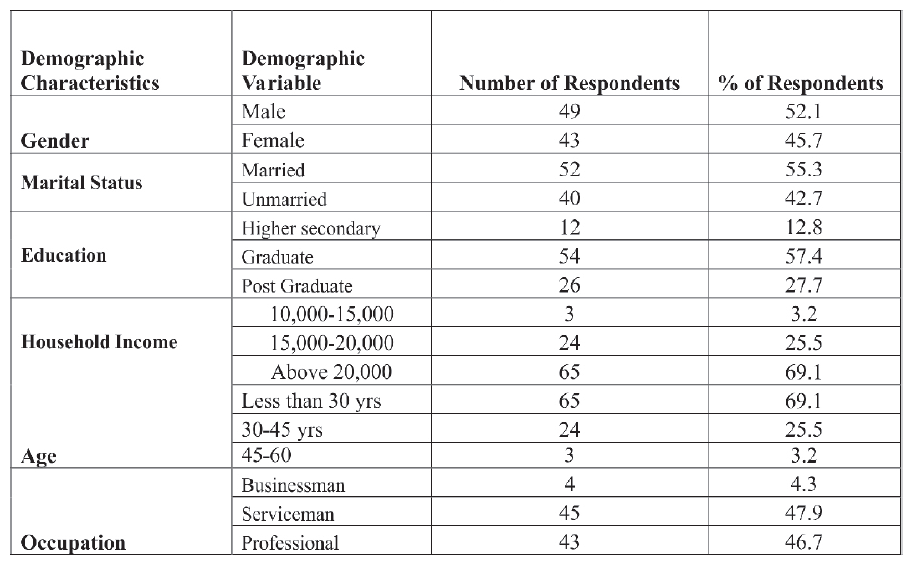

The demographic characteristics of the respondents are shown in below Table no.

1. The respondents profile gives detail information about financial and banking

customer’s such as age, Gender, household income level, Education qualification,

marital status and their occupation.

The analysis showed that the ratio of the male to female is 1.15:1. Whereas most

of the respondents are married compromising the percentage of 55% whereas the unmarried

% is 42.7%. The study targeted the young respondents having age less than 30 years

followed by 30-45 years and then is post graduate and higher secondary. The majority

of respondents had income above than 20,000. Majority of the respondents were professional

and serviceman.

Table no. 1: Demographic Characteristics

Results of Factor Analysis

Reliability analysis has been conducted on 20 variables and Cronbach Alpha is determined

as 0.838 which indicates reliability of the scale. Table 2 shows the reliability

statistics.

Table 2: Reliability Statistics

|

Reliability Statistics

|

|

Cronbach's Alpha

|

N of Items

|

|

.838

|

20

|

Table 3: KMO and Bartlett's Test

|

KMO and Bartlett's Test

|

|

Kaiser-Meyer-Olkin Measure of Sampling Adequacy.

|

.710

|

|

Bartlett's Test of Sphericity

|

Approx. Chi-Square

|

554.042

|

|

Df

|

190

|

|

Sig.

|

.000

|

The analysis details of the factor analysis were presented in the above Table no.

3. As we can see the value of KMO was 0.710, which should lie between 0.5 and 1.0.

Also, the statistical test for Bartlett test of sphericity was significant (p =

0.000; d.f. = 190) for all the correlations within a correlation matrix (at least

for some of the constructs).

Based on the principal components analysis and VARIMAX procedure in orthogonal rotation,

Eigen values above 1.0 are selected. Discriminant validity indicated that all items

were allocated according to the different constructs. Therefore, the items were

not overlapping and they supported the respective constructs. The factor analysis

reduced the data of 20 variables into the five factors which have the impact on

the respondents. The summarized results are shown in table no 4.

Table No 4 : Summarized Results of Factor Analysis

|

Sr.No

|

Factor-wise Dimensions

|

|

Eigen Value

|

% of variance explained

|

Cumulative % of variance explained

|

|

1.

|

Celebrity Endorsement

|

|

2.800

|

14.000

|

14.000

|

|

|

I feel excited when I saw my favorite celebrity endorsing the Bank advertisements.

|

.768

|

|

|

|

|

|

Due to coming of my favorite celebrity in advertisement my trust on my Bank has

increased.

|

.815

|

|

|

|

|

|

I believe the celebrities also use the same Bank for which they endorse

|

.687

|

|

|

|

|

|

I feel celebrity endorsement help in brand promotion of banks as well.

|

.552

|

|

|

|

|

2.

|

Decision making

|

|

2.481

|

12.403

|

26.404

|

|

|

Advertisement helps to be associated with the specific Bank.

|

.720

|

|

|

|

|

|

Quality Bank promote their products with the help of advertisement

|

.644

|

|

|

|

|

|

Publicity about my Bank influenced my decision for selecting this bank.

|

.529

|

|

|

|

|

3

|

Knowledgeable

|

|

2.087

|

10.435

|

36.838

|

|

|

The advertisement and promotions of my Bank are knowledgeable.

|

.577

|

|

|

|

|

|

The content shown in the advertisement is easy to understand.

|

.787

|

|

|

|

|

|

Advertisement provides the information about the infrastructure, Customer services

and other facilities of bank.

|

.681

|

|

|

|

|

4

|

Publicity effects

|

|

2.028

|

10.142

|

46.981

|

|

|

The publicity about the Bank revealed some things I had not considered about this

bank.

|

.539

|

|

|

|

|

|

I noted the message as shown in the advertisement act as guiding tool for my future

decision.

|

.569

|

|

|

|

|

|

I purchase banking and investments products whenever new promotional offers are

offered.

|

.740

|

|

|

|

|

5

|

Promotion About new schemes

|

|

1.841

|

9.207

|

56.187

|

|

|

My bank advertises whenever new schemes are available.

|

.755

|

|

|

|

|

|

I feel positive toward the advertizing and promotions of my Bank.

|

.686

|

|

|

|

Results for Regression Analysis

In order to determine the factor which is most important among the factors which

has been extracted by the factor analysis we had applied the multiple regression

analysis. The multiple regression analysis has been used to identify the impact

of the advertisement on the buying behavior of the respondents.

In the table 5, R value represents the simple correlation and is .649 (the

"R" Column), which indicates a high degree of correlation. The

R2 value (the "R Square" column) indicates how

much of the total variation in the dependent variable. In this case, 62.8 % can

be explained, which is very large.

Table 5: Regression results between the Bank Selection parameters and the Advertisement

|

Model Summary

|

|

Model

|

R

|

R Square

|

Adjusted R Square

|

Std. Error of the Estimate

|

|

1

|

.805a

|

.649

|

.628

|

.47064

|

|

Table 6 : ANOVA table for the Bank Selection parameters and the Advertisement

|

|

ANOVAb

|

|

Model

|

Sum of Squares

|

Df

|

Mean Square

|

F

|

Sig.

|

|

1

|

Regression

|

35.158

|

5

|

7.032

|

31.745

|

.000a

|

|

Residual

|

19.049

|

86

|

.222

|

|

|

|

Total

|

54.207

|

91

|

|

|

|

|

|

|

|

Table 6 indicates the statistical significance of the regression model that was

run. Here, p < 0.0005, which is less than 0.05, and indicates that, overall,

the regression model statistically significantly predicts the outcome variable (i.e.,

it is a good fit for the data).

Table 7: T-value and p-value for the regression result between the Advertisement

and the buying behavior

|

Coefficientsa

|

|

Model

|

Unstandardized Coefficients

|

Standardized Coefficients

|

t

|

Sig.

|

|

B

|

Std. Error

|

Beta

|

|

1

|

(Constant)

|

3.772

|

.049

|

|

76.869

|

.000

|

|

REGR factor score 1 for analysis 1

|

.172

|

.049

|

.223

|

3.487

|

.001

|

|

REGR factor score 2 for analysis 1

|

.556

|

.049

|

.720

|

11.268

|

.000

|

|

REGR factor score 3 for analysis 1

|

-.129

|

.049

|

-.168

|

-2.625

|

.010

|

|

REGR factor score 4 for analysis 1

|

.077

|

.049

|

.100

|

1.564

|

.122

|

|

REGR factor score 5 for analysis 1

|

.158

|

.049

|

.205

|

3.202

|

.002

|

|

|

The Coefficients table 7 provides us with the necessary information to predict

Impact of advertisement on bank selection or buying behavior of financial products,

as well as determine which independent variable of bank selection parameter have

major impact or is more important.

The table shows that factor 2 which is Decision making have the major

impact on the people while they are watching advertisement since the sig value is

less than .05 also the value of B is highest among all. Whereas the above table

also predicts that factor 3 which is knowledgeable have the negative impact on the

people while they are watching advertisements.

The regression equation for the above is:

Y= 3.772(constant) + .172( Celebrity Endorsement)X1 + .556(Decision making) X2 +

(-.129) (Knowledgeable) X3 + .077 ( Publicity effects ) X4 + .158( Promotion About

new products) X5

Summary and Conclusion

The present study we have performed an empirical investigation to find the major

factors which will impact the customer’s decision making. The data been collected

from India where the respondents were asked to tell the major factors that will

affect the decision making.

The data analysis had found the five prompting factors that played a significant

part in the buying process of the respondents. The research show that factors such

as Celebrity Endorsement, Decision making, Knowledgeable, Publicity effects, Promotion

About new schemes had major impact on the attitude, mind set and approach towards

buying behavior. The customer paid a great attention to those financial players

that will advertise their products; whenever new products come they inform the present

customer about their services, and uses the latest method promotion so as to reach

the maximum number of customers. As there is time of latest technology therefore

those use latest technology such as mobile banking, e-banking, online statements,

are most preferred by the customers. Whereas the further investigation states that

the customers consider the advertisement in the decision making process as and when

they purchase the banking and financial products.

Limitations and Future Scope of Study

The present research is useful to the banking and financial service providers as

it identify the factors which play an important role in the attitude and decision

making of the consumers.

But no research is free from limitations. Due to the scarcity of time and resources

the data had not been collected from all around the country. Further the future

research should be done in order to verify the pre and post behavior of the respondents

after watching the different advertisements.

References

Carter, Tony. and Chattalas, Michael. (2001), “Marketing Financial Services in London”,

Services Marketing Quarterly, Vol. No. 22, Issue No. 4, pp. no. 63-81.

Ryals, Lynette. and Payne, Adrian. (2001), “Customer relationship management in

financial services: towards information-enabled relationship marketing”, Journal

of Strategic Marketing, Vol. No. 9, Issue No. 1, pp. no. 3-27.

Gupta, A. K. and. Westal , G.( 1992-94),” Distribution Of Financial Services”,

Transactions of the Faculty of Actuaries, Vol. 44 , pp. 24-63.

Ekerete, Pualinus P.(2005),” Marketing Of Financial Services: A Case Study Of Selected

Merchant Banks In Nigeria”, Pakistan Economic and Social Review, Vol. No.

43, Issue No. 2 , pp. 271-287.

Sadeghi, Tooraj. and Bemani, Atefeh. (2011),” Assessing the Quality of Bank Services

by Using the Gap Analysis Model”, Asian Journal of Business Management Studies,Vol

No. 2, Issue No.1, pp. 14-23.

Hooman, Estelami., (2008) "Consumer use of the price-quality cue in financial

services", Journal of Product & Brand Management, Vol. 17, Issue No. 3,

pp.197 – 208.

Lindholm Oskari. (2008), “The influence of Sales Promotion on Consumer Behavior in

financial services”, Helsinki School of management. Available at http://epub.lib.aalto.fi/en/ethesis/pdf/12006/hse_ethesis_12006.pdf

[Retrieved as on 20th July 2012].

Bamoriya, Hemant. And Singh, Rajendra .( 2011),” Attitude towards Advertising and

Information Seeking Behavior: A Structural Equation Modeling Approach”,

European Journal of Business & Management, Vol.3, Issue No. 3,pp. 1-11.

Ekankumo, Banabo. and Henry , Koroye Braye .( 2011),” Sales Promotion Strategies

of Financial Institutions in Bayelsa State” , Asian Journal of Business

Management, Vol. No. 3, Issue No.3, pp. 203-209.

Dass, Rajanish. And Pal, Sujoy .(2011),” A Meta Analysis on Adoption of Mobile Financial

Services”,Indian Institute of Management, Research and Publications, Working

Paper No.2011-01-05.

Mylonopoulos, Nikolaos A. and Doukidis, Georgios I.( 2003), “Mobile Business: Technological

Pluralism, Social Assimilation,and Growth” , International Journal of Electronic

Commerce, Vol. 8, No. 1, pp. 5-22.

Beckett, Antony.,Hewer, Paul. And Howcroft, Barry. (2001),” An exposition of consumer

behavior in the financial service industry”, International Journal of Bank

Marketing,Vol. 18, No. 1,pp.15-26.

Sidhu, Dr. Muninder.(2003),”Impact of advertisements on the purchase behavior of

urban home makers”.Journal of Management Studies, Vol. 3,pp. 105-112.

The Economic Times, August 31, (2010). Available at http://articles.economictimes.indiatimes.com

/2010-08-31/news/27628037_1_education-sector-services-sector-print-ad. [Retrieved

as on 22th July 2012].