Awareness and Adoption of Technology in Banking Especially by Rural Areas Customers:

A Study of Udaipur Rural Belt

|

Dr. Harshita Bhatnagar

Assistant Professor

Vidya Bhawan Rural Institute

Udaipur, Rajasthan, India

36 Gayatri Marg, Kanji Ka Hatta, Udaipur-313001, Rajasthan, India

Email: hbhatnagar.mba@gmail.com

|

Abstract

ICT has been the cornerstone of recent financial sector reforms aimed at increasing

the speed and reliability of financial operations and initiatives to strengthen

the banking sector. The intense competitive environment is continuously forcing

the banks to become customer-centric. Today technology has emerged as a strategic

resource for achieving higher efficiency, control of operations, productivity and

profitability for Banks as well as it is the realization of their ‘anywhere, anytime,

anyway’ banking dream for customers. But instead of all these benefits, the awareness

and adoption rate of banking services among the rural customers is still

found very low. Hence this paper presents the preliminary findings on investigation

of the level of the customer’s awareness as well as adoption of banking services

by the rural customers based on demographics, bank type, familiarity with computer/internet.

Keywords: Banking; Information and Communication Technology (ICT); Awareness,

Adoption, Internet

Introduction

Banking is the blood of the economy whose vitality signifies the health and prosperity

of any nation. India had a system of indigenous banking from very early times, though

it was not similar to banking in modern times. Since independence commercial banks

have a wide network to operate in the country under RBI. Straight from the nationalisation

of banks in 1969 to the recent application of BASEL III, from a small number of

PSB to a huge figure of private and foreign banks, from its humdrum and laid back

system to the modern hi-tech systems with e-banking, m-banking, t-banking, etc.

banks has come up to a long way. Banking Industry in India has travelled a protracted

path to assume its present status and is continuously undergoing nonstop transformation.

Modern banks execute multiplicity of function by providing numerous products and

services to the customer with the ultimate objective to increase profits along with

customer satisfaction. Innovation is a dynamic phenomenon which involves adoption

of new technology, products, services and methods. The technological innovation

in banking actually began in 1950 well before it began in most of the industries,

when the first automated machine was installed at a few US Banks, which then became

common in subsequent decades.

E-Banking in rural areas of udaipur district

Banking technology also assumes the activity of using advanced computer algorithms

in raveling the patterns of customer behaviors by sifting through customer details

such as demographic, psychographic and transactional data. This activity is also

known as Data Mining which helps bank to achieve their business objectives by solving

various marketing problems such as customer segmentation, customer scoring, target

marketing, market based analysis, cross sell, customer retention by modeling churn

and so forth.

Electronic banking refers to the use of technology which allows customer to access

banking services electronically whether it is to pay bills, transfer funds, view

account or to obtain information and technology and advices. Internet or web based

banking is network of banks and financial institutes as well other sealers. It provides

electronic payments and settlement services to customers. It implies the most pragmatic

use of information technology as medium of universal communication. It has brought

unprecedented changes in banking industry.

Today technology has emerged as a strategic resource for achieving higher efficiency,

control of operations, productivity and profitability for Banks as well as it is

the realization of their ‘anywhere, anytime, anyway’ banking dream for customers.

But instead of all these benefits, the awareness and adoption rate of banking services

among the rural customers is still found very low. Hence this study will

basically focuses on investigation of the level of the customers awareness as well

as adoption of banking services by the rural customers. There are many factors like

security & privacy, trust, innovativeness, familiarity, awareness level increase

the acceptance of technology based banking services among rural Indian customers.

REVIEW OF LITERATURE

Malik, S. (2014) said that financial innovation is key to survival of banks

in contemporary banking environment. The importance of financial innovation is widely

recognized. Innovation in product development is one of the forms of innovation

that has been used by banks. Srivastav, P.K. (2013) conventional banking

is an art but e-banking is more of science than art as it is more knowledge based

and scientific in using electronic devices. Suresh (2008) highlighted recently

developed e-banking technology had created unpredicted opportunities for the banks

to organize their financial products, profits, service delivery and marketing. The

author analyzed that e-banking will be an innovation if it preserved both business

model and technology knowledge, and disruptive if it destroys both the model and

knowledge. Manoharan (2007) highlighted the e-payment system in India and

its performance impact on Indian banking sector. The author described that competition

in banking industry had forced the banks to rethink the way they operate their business.

So, e- banking has made it possible to find alternate banking practices. In the

paper, the author divided the payment system in India into three parts, i.e., large

value payment system, retail payment system, and retail electronic system. Sakkthivel

A M (2006) conducted an extensive primary research in India in order to

identify the willingness of Internet users to buy different services over Internet

and provides a specific focus to identify the impact of demographics in influencing

Indian Internet users in consuming different services online. The outcomes would

help the corporate world to understand the importance of demographics on online

purchase which could be adopted and deployed for better use.

RATIONALE OF RESEARCH PROBLEM

Providing financial services to poor people is costly, because they have small amount

of money but after liberalisation, technology banking is spreading their wings continuously

in small and rural areas. During last two decades, we have observed that technology

is reaching and capturing various day to day activities of life like use of mobiles,

laptop, tablets, plastic cards etc. Urban population is very well versed with technology

but if we talk about rural areas, customers are untouched with various technological

services provided by their banks. Hence in order to increase the rural customer

base for greater use of technology related services, it is imperative to understand

the customer awareness and usage level of rural customers towards technology based

banking services. Information on the above aspects would be useful to formulate

program to motivate more and more customers to use technology based banking services.

Therefore in lieu of the above mentioned issue, this project study is relevant to

be done.

OBJECTIVES OF THE STUDY

The tremendous advances in technology in the banking industry worldwide have turned

out to be the nucleus issue of various studies all over the world. The research

was guided by the following research objectives;

- To study awareness of technology based banking services among rural customers.

- To analyse adoption and usage pattern technology based banking services among rural

customers.

- To study the impact of familiarity of internet use on awareness and usage of technology

base banking services among rural area customers.

HYPOTHESIS

H1a: The awareness of customers regarding about the technology based banking

services and Age, Gender, Education, Profession and Income of customers are related.

H2a: The usage status of customers regarding technology based banking

services differs from Age Wise, Gender Wise, Education Wise, Profession Wise, and

Income Wise.

H3a: Familiarity with computer and Internet influences the regular usage of technology

based banking services

H4a: The status of usage for different technology based banking services differ significantly.

H5a: There is no significant difference between the awareness levels among the Public

and Private bank Customers.

H6a: There is no significant difference between the usage levels among the Public

and Private Bank customers

DESCRIPTIVE RESEARCH DESIGN

In order to understand the role of technology in banking, the awareness level of

customers especially of rural areas, the usage pattern and various factors affecting

the promotion of technology based banking services along with various problems faced

by them while using them, to study all these problems, a descriptive research design

was framed. In this research one survey was conducted in three major rural area

of Udaipur district. For the same one schedule was framed, which was then filled

by the investigator and the data collected were then undergo empirical testing.

The data is collected through a descriptive survey done with the sample of 150 rural

customers.

SAMPLE DESIGN

A sample design is a definite plan for obtaining a sample from a given population.

It refers to the technique or the procedure the researcher would adopt in selecting

item for the sample. Sample design may be well lay down the number of items to be

included in the sample i.e. size of the sample. Respondents include customers of

reputed public sector bank and private sector bank existing in the three different

cluster of rural belt of Udaipur district. Respondents are those who already have

their account in that particular bank and are of different age, sex, religion, profession

and family background.

1. SAMPLE SIZE

In this study simple random sampling method has been used. Total 150 schedules were

filled by the interviewer from three different sample units. The division of respondents

is shown below in table 1

2. SAMPLE UNITS

The customers are selected randomly from three different major rural areas of Udaipur

district Kherwada, Mavli and Salumber were selected and proportionally schedules

were filled from each area. 50 schedules were filled by the interviewer from the

each division selected on random basis.

TABLE 1: DISTRIBUTION OF SAMPLE UNITS

|

S.No.

|

Mavli

|

Salumber

|

Kherwada

|

|

1

|

Mavli

|

Salumber

|

Kherwada

|

|

2

|

Fatehnagar

|

Sarada

|

Rishabdeo

|

|

3

|

Vallabhnagar

|

Lasadia

|

Kalyanpur

|

|

4

|

Kheroda

|

Kun

|

Parsad

|

|

5

|

Bhinder

|

Semari

|

Chawand

|

3. SAMPLING SELECTION TECHNIQUES

Simple Random sampling method is used in the survey .Three division Kherwada, Mavli

and Salumber were selected and proportionally 50 customers are selected from each.

DATA COLLECTION

There are two methods of generating information or collecting data required for

research, one through observation and other through experimentation. Observation

is the process of measuring variables just as they occur in nature, without directly

or deliberately influencing their values. Experimentation method has the foundation

of science. Its essence is the manipulating an independent variables and then measuring

the resulting change in the dependent variable. The data is collected through both

primary and secondary sources.

1. PRIMARY DATA COLLECTION

The most appropriate method for this research work is Survey Method. It consists

of Personal Interview, Telephone Interview and Mail Interview. It is the technique

of gathering data by asking questions to people who are thought to have desired

information. Schedules were prepared and 150 respondents were contacted.

2. CONSTRUCTION OF A QUESTIONNAIRE

Primary data was collected from respondents using a self administered questionnaire,

this created anonymity leading to more valid responses as well as allowing respondents

to fill them at their convenience. The questionnaire was designed according to the

objectives and study variables. The questionnaire is divided into 5 parts.

Part I consists has seven items which aims at collecting information about

the demographic details of the rural customers.

Part II dealt with questions framed specifically for understanding the awareness

level of customers for technology in banking.

Part III dealt with questions framed specifically for understanding the usage

pattern and familiarity of technology in banking.

3. SECONDARY DATA

The sources of secondary data that is referred are Libraries, trade publications,

companies’ brochures, websites, various books and journals are some important sources

of data are the sources for gathering information

STATISTICAL TOOLS AND TECHNIQUES

The key literature on banking and role of technology in banking is reviewed. Primary

data was collected using questionnaire survey. Descriptive and inferential analysis

was done and Statistical tools such as ANOVA and Correlation test etc employed using

SPSS version 16 to analyze the data.

LIMITATION OF STUDY

Each and every human being is unique in itself. We cannot apply the same approach

to different people. As each individual has his/her unique set of mind, opinions,

beliefs, aspiration etc therefore we need a specific approach for specific person.

Every research work is subjected to certain limitations; and this study is also

not an exception. The present study has the following limitations:

1. The responses for the study have been solicited from the rural belt of Udaipur

Division, Rajasthan state only. The expectations of the customers in Udaipur may

vary from those of the rest of India.

2. Any primary data based study carried through a pre-designed questionnaire/ Schedule

suffers from the basic limitation of possibility of difference between what is recorded

and what is truth, no matter how carefully the interview has been conducted. The

present study may also suffer from this limitation because the people might not

have deliberately reported their true opinion due to some biasness. Objectives of

the study are based upon primary data which is collected from the customers’ perspective.

So, the study may suffer from the elements of biasness; and it is difficult to reach

at the real situation.

DATA NALYSIS AND INTERPRETATION

The data collected through schedules were coded, and analyzed through spss.16.0

version. The analysis and interpretation is describe in five broad categories

Part A: It describes the respondent’s distribution based on area, demographic factors

and bank wise.

Part B: It deals with the extent of awareness, usage and familiarity of respondents

with technology based banking services and impact of demographic on awareness and

usage

Part C: It deals with comparative analysis of awareness and usage level among respondents

of public and private sector bank

PART A – DISTRIBUTION OF RESPONDENTS

A1: AREA WISE DISTRIBUTION:

TABLE 2: AREA WISE CLASSIFICATION

|

Division

|

Number of Respondents

|

|

Kherwara

|

50

|

|

Mavli

|

50

|

|

Salumber

|

50

|

Interpretation: Table 5.1 shows that Schedules were filled from three divisions

of Udaipur city. There are five subdivisions in each division. Total 150 schedules

were filled and from each three division 50 schedules taken for the study.

A2: DISTRIBUTION ON THE BASIS OF AWARENESS OF TECHNOLOGY: Schedules from

150 respondents were filled to know that so many aspects. Beginning of the schedule

is with to know how many respondents who are having their account in banks are really

aware about technology based banking services.

TABLE 3: AWARE OF TECHNOLOGY BASED BANKING SERVICES

|

Aware

|

Number of Respondents

|

|

Traditional Banking

|

150

|

|

Technology Banking

|

120

|

Interpretation- Table 3 shows that out of total 150 schedules it is found

that only out of 150 respondents only 120 respondents are aware about technology

based banking services.

A3: DEMOGRAPHIC DISTRIBUTON: The following Tables/Graphs show the various

demographic conditions of the only those respondents who are using technology while

performing banking transactions.

1. GENDER WISE DISTRIBUTION

TABLE 4: GENDER CLASSIFICATION

|

Gender

|

Percentage

|

Number

|

|

Male

|

89.17

|

107

|

|

Female

|

10.83

|

13

|

Interpretation: Most of the respondents belong to male category (89.17%).

Hence we can say that in rural areas most of the bank transactions are still handled

by males in comparison to females- “Male dominant”.

2. AGE WISE DISTRIBUTION

TABLE 5: AGE GROUP CLASSIFICATION

|

Age

|

Percentage

|

Number

|

|

10 - 20 Yrs

|

4.17

|

5

|

|

21 - 30 Yrs

|

34.17

|

41

|

|

31 - 40 Yrs

|

49.17

|

59

|

|

41 - 50 Yrs

|

9.17

|

11

|

|

Above 50 Yrs

|

3.33

|

4

|

Interpretation: Most of the respondents belong to age category of 31-40 years

(49.17%) and then 21-30 years (34.17 %). Hence we can say that in rural areas most

of the bank transactions are handled by youth - “Youth are ahead”

3. EDUCATIONAL QUALIFICATION

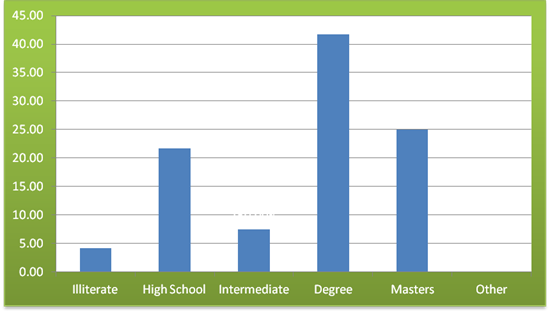

GRAPH 1: EDUCATIONAL QUALIFICATIONS.

Interpretation: Graph 1 shows that most of the respondents are either graduates

( 41.67 %) or have passes high schools (21.67%). “Graduates are mostly users”.

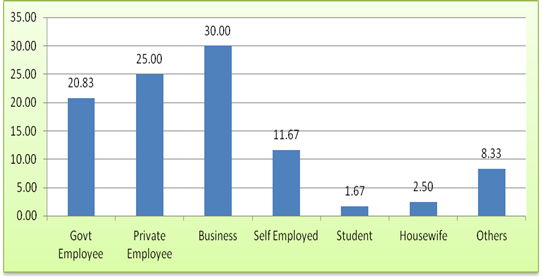

4. PROFESSION WISE DISTRIBUTION

GRAPH 2: PROFESSIONAL DISTRIBUTION (IN %)

Interpretation: Graph 2 shows that most of the respondents are entrepreneurs

who self initiated their business or are continuing their family business. Hence

we can conclude that most of the people dealing with the Banks are Businessman in

the rural areas other people are least interested in technology based banking services.

“Businessman is technology users.”

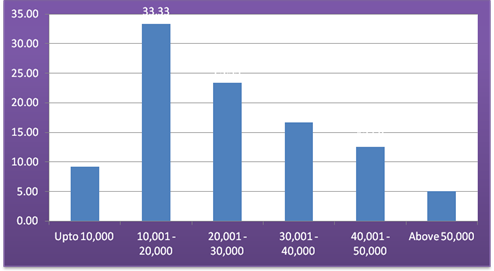

5. MONTHLY INCOME: The following graph shows the monthly income of the respondents.

GRAPH 3: MONTHLY INCOME (%)

Interpretation: Graph 3 shows that most of the respondents run their

own business and 33.33% of them have a monthly income lying between 10001-20000rs.

A4: BANK WISE DISTRIBUTION OF CUSTOMERS

TABLE 6: BANK WISE CLASSIFICATION

|

Bank type

|

Number of respondents

|

|

Public Sector Bank

|

74

|

|

Private Sector Bank

|

46

|

Interpretation: Table 5.5 shows that out of total schedule filled, 74 were

the customers of public sector bank and 46 were customers of private sector banks

who are using technology while dealing with banking services. Hence we can say that

most of the respondents in our study are having their accounts in public sector

bank.

PART B: DEALS WITH AWARENESS LEVEL, USAGE STATUS AND WITH FAMILIARITY WITH TECHNOLOGY

AND IMPACT OF DEMOGRAPHIC FACTORS ON AWARENESS, USAGE AND FAMILIARITY.

B1: AWARENESS LEVEL AND IMPACT OF DEMOGRAPHICS

The following chart & table shows the awareness with technology service among

respondents.

TABLE 7: AWARENESS WITH TECHNOLOGY SERVICE

|

Awareness with Service

|

Percentage

|

Number

|

|

High

|

83.33

|

100

|

|

Partially / Low

|

16.66

|

20

|

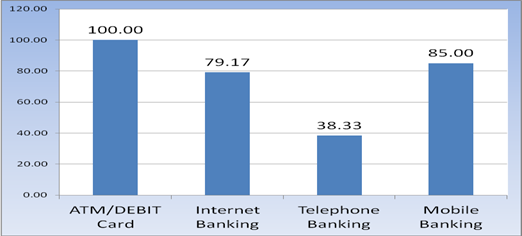

TABLE 8: AWARENESS WITH DIFFERENT SERVICE

|

Awareness with Service

|

Percentage

|

Number

|

|

ATM/DEBIT Card

|

100

|

120

|

|

Internet Banking

|

79.17

|

95

|

|

Telephone Banking

|

38.33

|

46

|

|

Mobile Banking

|

85.00

|

102

|

GRAPH 4: AWARENESS WITH DIFFERENT SERVICE

Interpretation: Table 8 shows that most of the respondents are highly aware

of the technology 83.33% and few are partially aware. If we talk about different

innovative services like ATM, Internet Banking, Telephone Banking and Mobile Banking.

It is clear from the table 5.7 that out of these four innovative technology based

banking services provided by banks, ATM/Debit card has the majority of 100% awareness

followed by mobile banking with 85 %.

2. Impact of Demographic Characteristics on the Awareness level of Rural People

. In order to understand whether the different demographic characteristics influences

and causes any impact on the awareness level of respondents about technology based

banking services. Chi Square Test was applied to determine whether there is a significant

impact of demographic on awareness level of the respondents. The hypothesis were

framed as:

H1a: The awareness of customers regarding about the technology based

banking services and Age, Gender, Education, Profession and Income of customers

are related.

TABLE 9: AWARENESS LEVEL AND DEMOGRAPHIC

|

Demographic Characteristic

|

Pearson Chi Square

|

Df

|

Sig Value

|

|

Gender

|

0.017

|

1

|

0.895

|

|

Age Group

|

10.051

|

4

|

0.04

|

|

Education

|

42.047

|

4

|

0

|

|

Profession

|

15.154

|

6

|

0.019

|

|

Income

|

26.767

|

5

|

0

|

Interpretation: Chi-square test shows that the p value is lesser than .05

in case of age, education, profession and income except in the case of gender, this

signifies that the null hypothesis is rejected in all the cases except Gender.

Hence we can conclude that demographic factors like Age, Education Level, Profession

and Income influences the awareness level. The significant value shows that these

four demographic characteristics of the respondents do influence their awareness

level regarding technology based banking services.

B2: USAGE OF TECHNOLOGY AND IMPACT OF DEMOGRAPHICS

1. The following chart & table shows the usage of technology by the customers

on the regular basis or not.

TABLE 10: REGULAR USAGE OF TECHNOLOGY

|

Using Tech. Services

|

Percentage

|

Number

|

|

Yes

|

79.17

|

95

|

|

No

|

20.83

|

25

|

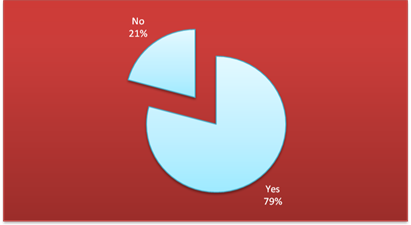

GRAPH 5: USAGE OF TECHNOLOGY

Interpretation: Table 10 shows that out of total 120 respondents who are

aware of technology banking services, only 95 (79.17%) respondents are using technology

services regularly for banking operations in one or other mode. Remaining 21% respondents

are using technology but not the regular basis.

2. The table 11 shows that which service is more commonly used by the customers.

TABLE 11: SERVICES TRIED

|

Tried which banking service

|

Percentage

|

Number

|

|

ATM/DEBIT Card

|

100

|

120

|

|

Internet Banking

|

66.66

|

80

|

|

Telephone Banking

|

13.33

|

16

|

|

Mobile Banking

|

65.83

|

79

|

Interpretation: As per the above table 11, the customers are using technology

in banking either regularly or rarely but out of all four categories, majority of

them are using ATM/ Debit card with 100% followed by internet banking with 66.66%.

Telephone Banking is least preferred by the respondents, reason can be greater availability

of mobile and internet facilities.

3. Impact of demographic characteristics on the regularity of use of technology

based banking services by the rural customer:

In order to understand whether the different demographic characteristics influences

and causes any impact on usage of technology based banking services, Chi Square

Test was applied. The hypothesis framed is:

H2a: The usage status of customers regarding technology

based banking services differs from Age Wise, Gender Wise, Education Wise, Profession

Wise, and Income Wise.

TABLE 12: USAGE STATUS AND DEMOGRAPHIC

|

Demographic

|

Pearson Chi Square

|

Df

|

sig value

|

|

Gender

|

0.262

|

1

|

0.608

|

|

Age

|

10.94

|

4

|

0.027

|

|

Education

|

35.214

|

4

|

0

|

|

Profession

|

22.311

|

6

|

0.001

|

|

Income

|

14.552

|

5

|

0.012

|

Interpretation: As the p value is lesser than .05 in all demographics except

in the case of gender, this signifies that the null hypothesis is rejected

in the case of age, education, profession and income. Hence we can conclude that

all demographic factors are Age, Education Level, Profession and Income influences

the usage status except gender doesn’t influences the usage status of the rural

customers. The Cross tables mention below gives an idea on the relationship.

B3: FAMILIARITY WITH COMPUTER/INTERNET

An Idea was taken to understand the computer knowledge of the rural customer. Kumar

S and Anjum B (2014) states that the online banking is a demand of today’s

customers because it saves the cost and time for the settlement of their financial

transactions. The major problem observed at end of the study is the lack of knowledge

among the people about the use of Internet and computer, which ultimately hamper

the growth of E-banking operation.

TABLE 13: FAMILIARITY WITH COMPUTER/INTERNET USE

|

Familiarity with computer

|

Percentage

|

Number

|

|

No Knowledge

|

15.83

|

19

|

|

Beginner

|

21.67

|

26

|

|

Average

|

50.00

|

60

|

|

Advanced

|

10.83

|

13

|

|

Expert

|

1.67

|

2

|

Interpretation: Table 13 shows that out of the total respondents 50% of the

sample size have an average familiarity with computers, 1.67% of total respondents

have an expert familiarity with computers whereas 15.83% of respondents have no

knowledge about computers.

Relationship between Computer/Internet knowledge and the usage with e-banking:

In today’s world no one is aloof from the technology. It has become the part

and parcel of each and every individual’s life. The test was applied to study whether

there is a direct relationship between familiarities with the Computer/Internet

with usage of e- banking services or not. In real world increase in familiarity

with computer/internet increases the usage of technology based banking services.

Therefore to understand, whether the familiarity with the computer/internet knowledge

influences the usage status of technology based banking services, Correlation test

was applied.

H3a: Familiarity with computer and Internet influences the regular usage of technology

based banking services.

TABLE 14.PEARSON AND SPEARMAN CORRELATION TEST

|

|

Value

|

Asymp. Std. Error (a)

|

Approx. T(b)

|

Approx. Sig.

|

|

Interval by Interval Pearson's R

|

.488

|

.075

|

-6.075

|

.000(c)

|

|

Ordinal by Ordinal Spearman Correlation

|

.469

|

.075

|

-5.773

|

.000(c)

|

|

N of Valid Cases

|

120

|

|

|

|

Interpretation: Table 23 shows that Null hypothesis is rejected and a moderate

positive, but significant relationship (with p value=0.00) is identified between

the computer knowledge and usage status of various technology based banking services.

This is a very natural phenomenon that as there is a increase in computer knowledge,

usage of technology based banking services will be more used by the customers.

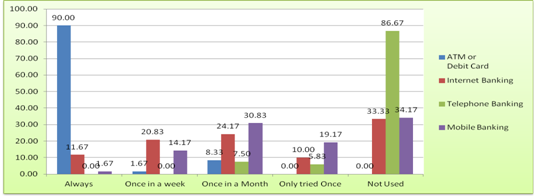

B4: USAGE STATUS FOR DIFFERENT TECNOLOGY BASED BANKING SERVICES.

The following chart & table shows the usage pattern of the respondents towards

different categories of technology based banking service.

TABLE 15: USAGE STATUS OF DIFFERENT SERVICES

|

Status of Usage

|

ATM Card

|

Internet Banking

|

Telephone Banking

|

Mobile Banking

|

|

Always

|

108

|

14

|

0

|

2

|

|

Once in a week

|

2

|

25

|

0

|

17

|

|

Once in a Month

|

10

|

29

|

9

|

37

|

|

Only tried Once

|

0

|

12

|

7

|

23

|

|

Not Used

|

0

|

40

|

104

|

41

|

GRAPH 6: USAGE STATUS OF DIFFERENT SERVICES

Interpretation: it is evident from the table 15 that the frequency of usage

of ATM/Debit card regularly is in maximum with 90%. Similarly the usage pattern

of internet banking it is observed that maximum people are using it once in a month

or mostly once in a week. It may be due to availability of internet services is

less frequent. But if we talk about telephone banking which is least preferred,

data shows that then maximum respondents had not used this service or tried only

once. Mobile banking is average used by the people once in a month.

Therefore to understand that the difference in the usage status for different technology

based banking services is significant or insignificant; one way ANOVA test is applied,

taking computer knowledge as dependent variable

H4a: The status of usage for different technology based banking services differ

significantly.

TABLE 16: ONE WAY ANOVA TABLE ON USAGE PATTERN

|

Sources of variance

|

Sum of Squares

|

DOF

|

Mean Squares

|

Test Statistics

|

|

B/w Sample

|

0

|

3

|

0

|

0

|

|

Within Sample

|

17032

|

19

|

896.42

|

|

|

Total

|

17032

|

22

|

896.42

|

|

Interpretation: One way ANOVA test is applied on table 5.22 to determine

the whether the usage pattern are significantly differs for different services.

The tabulated F value is 3.5219 which is more than the critical value which implies

that the null hypothesis is accepted stating that the usage status is similar

for different e-banking services. Hence we can conclude that the differences are

insignificant and are just a matter of chance

PART C: BANK TYPES AND THE AWARENESS/USAGE STATUS

C1: BANK TYPES AND THE AWARENESS STATUS

In order to understand the difference among the awareness level among the private

and public bank the chi square test is applied. Table 5.30 gives a cross tabulation

between the type of bank and the awareness level. Hypothesis formed is as follows:

H5a: There is no significant difference between the awareness levels among

the Public and Private bank Customers.

TABLE 17: CROSS TABULATION: BANK TYPE AND AWARENESS

|

Bank Type

|

Awareness Level

|

Total

|

|

High

|

Low

|

|

Public Bank

|

56

|

18

|

74

|

|

Private Bank

|

44

|

2

|

46

|

|

Total

|

100

|

20

|

120

|

TABLE 18: CHI-SQUARE TESTS

|

|

Value

|

Df

|

Asymp. Sig. (2-sided)

|

Exact Sig. (2-sided)

|

Exact Sig. (1-sided)

|

|

Pearson Chi-Square

|

11.86

|

1

|

.263

|

|

|

|

Continuity Correction(a)

|

.475

|

1

|

.491

|

|

|

|

Likelihood Ratio

|

1.408

|

1

|

.235

|

|

|

|

Fisher's Exact Test

|

|

|

|

.405

|

.254

|

|

Linear-by-Linear Association

|

1.244

|

1

|

.265

|

|

|

|

N of Valid Cases

|

120

|

|

|

|

|

Interpretation: Respondents of public and private sector bank might be having

different outlook towards technology use in banking. Hence Chi square test is applied

to the data collected and it is found that the null hypothesis is accepted as the

p value is higher than .05, no significant difference is identified among the awareness

level of Public and Private Banks customers.

C2: TYPE OF BANK AND USAGE LEVEL

In order to understand the difference among the usage level among the private and

public bank the chi square test is applied.

H6a: There is no significant difference between the usage level

among the Public and Private Bank customers

TABLE 19: CROSS TABULATION: BANK TYPE & USAGE LEVEL

|

Bank Type

|

Usage Level

|

Total

|

|

Yes

|

No

|

|

Public

|

55

|

19

|

74

|

|

Private

|

40

|

6

|

46

|

|

Total

|

95

|

25

|

120

|

TABLE 20: CHI-SQUARE TESTS

|

|

Value

|

DF

|

Asymp. Sig (2-sided)

|

Exact Sig (2-sided)

|

Exact Sig (1-sided)

|

|

Pearson Chi-Square

|

2.745(b)

|

1

|

.098

|

|

|

|

Continuity Correction(a)

|

2.032

|

1

|

.154

|

|

|

|

Likelihood Ratio

|

2.888

|

1

|

.089

|

|

|

|

Fisher's Exact Test

|

|

|

|

.111

|

.075

|

|

Linear-by-Linear Association

|

2.722

|

1

|

.099

|

|

|

|

N of Valid Cases

|

120

|

|

|

|

|

Interpretation: Table 5.33 shows that the usage level of respondent of public

and private sector bank differs. Hence to check the significance of relationship

between the usage status and type of bank, Chi-Square test was applied. The result

shows that the null hypothesis is accepted as the p value is higher than .05, no

significant difference is identified among the usage level of Public and Private

Banks customers.

CONCLUSIONS

Indian banking industry has undergone major changes due to economic liberalisation

and globalisation which led to managerial innovations, information technology revolution,

increasing competition, changing customer requirements and financial sector reforms.

The application of information and communication technology concepts, techniques,

policies and implementation strategies to banking services has become a subject

of fundamental importance and concerns to all banks and indeed a prerequisite for

local and global competitiveness.

In the present context of the market scenario the present study is very relevant

and will be very helpful to determining awareness and adoption of technology based

banking services among rural customers. It also helps in determining the basic problems

while using them and reasons behind not using these services. The present study

has been made through respondents of various reputed public and private banks of

rural areas of Udaipur division.

DEMOGRAPHIC: - Socio economic profile reveals that most of the users of banking

and technology are male (80%), belonging to the age group of 31-40 (49%) with graduation

degree (41.67%) and mostly engaged in either in their own venture or managing their

parental business. Almost 33 percent of the people have their monthly income in

the range of 10000-20000. Among all 74 were the customers of public sector bank

and 46 were customers of private sector banks.

AWARENESS LEVEL:-It is found that out of 150 respondents only 120 respondents

are aware of technology banking services. Out of 120, highly aware customers are

100 and 20 respondents are partially or less aware about banking services based

on technology. If we look at different services than it is very clear that awareness

is highest in the case of ATMs and least in case of telephone banking.

AWARENESS AND DEMOGRAPHIC: - they are studied together with the help of Chi-square

test to determine the relationship between them. Hence it is concluded that demographic

factors like Age, Education Level, Profession and Income influences the awareness

level. Only gender has no implication on the awareness level of the customers of

the banks.

USAGE LEVEL: - It is found that out of 120 respondents who are aware of technology

banking services, only 95 (79.17 %) customers are using the technology based services

regularly and 25 respondents are using technology banking services rarely. The frequency

of usage of ATM/Debit card regularly is in maximum with 90%, whereas, the usage

of internet banking varies; most of the people use once in a week and maximum people

use once in a month is high with 20.83% as being the availability of internet services

is less frequent. But if we talk about mobile banking then maximum respondents are

using this service once in a month. Telephone banking is used by few people either

once or once in a month. On applying ANOVA test it is concluded that the usage status

is similar for different e-banking services.

USAGE STATUS AND DEMOGRAPHIC: - They are studied together with the help of

Chi-square test to determine the relationship between them. Hence it is concluded

that demographic factors like Age, Education Level, Profession and Income influences

the awareness level. Only gender has no effect on the usage level of the customers

of the banks.

IMPORTANCE OF COMPUTER AND INTERNET KNOWLEDGE IN ENHANCING THE USAGE OF E-BANKING

SERVICES.

The technology has made its own world in the world of human beings. More than 50

percent of the customer has internet and computer knowledge. Correlation test was

applied to understand the relationship between familiarity with computer knowledge

and use of technology based banking services, it is found that a moderate degree

of positive correlation is identified between costumer knowledge about computers

and the use of technology in banking. Hence it clearly signifies the importance

of computer and internet knowledge in enhancing the usage of e-banking services.

BANK TYPES AND THE AWARENESS/USAGE STATUS

Respondents of public and private sector bank might be having different outlook

towards technology use in banking. To study the same data is collected and Chi-Square

test is applied and it is concluded that no significant difference is identified

among the awareness level and usage status of Public and Private Banks customers.

It indicates that even public sector banks are also taking any equal initiative

in enhancing the usage of e banking.

REFERENCES

1. Malik, S. (2014). Technological Innovations in Indian Banking Sector: Changed

face of Banking. International Journal of Advance Research in Computer Science and

Management Studies, Volume 2, Issue 6. Retrieved from http://ijarcsms.com/docs/paper/volume2/issue6/V2I6-0062.pdf

2. Kumar Sudesh and Anjum Bimal (2014). Electronic Banking: An Emerging Way of Customer

Services, Research Journal of Management Sciences, April, Vol. 3(4), 1-4, ISSN 2319–1171.

3. Srivastava, P.K. (2013). Banking Theory and Practices (12th Ed.). Mumbai: Himalya

Publishing House Limited.

4. Suresh, R. (2008), “E-banking: The Core Capabilities to Exploit”, The Management

Accountant, Vol.43, No.6, June, pp. 49-53.

5. Manoharan, B. (2007, “Indian E-payment System and its Performance”, Professional

Banker, Vol.7, No.3, pp. 61-69.

6. Sakkthivel A M : Impact Of Demographics On The Consumption Of Different Services

Online In India , Journal Of Internet Banking And Commerce, Volume . 11, Issue 3,

2006.