Grievance Redressal Mechanism in Indian Life Insurance Industry: An Exploratory Study on Quantifying Relationships

|

Prof. R. C. S. Rajpurohit

Professor and Former Dean

Faculty of Commerce and Management Studies

Jai Narain Vyas University, Jodhpur (Rajasthan), India.

|

Ranu Nawal

Research Scholar

Department of Business Administration

FCMS, Jai Narain Vyas University, Jodhpur (Rajasthan), India

|

ABSTRACT

Excellent customer service is the vital key for survival and growth of business in today’s competitive era. Customer Relationship Management becomes more important in case of market driven and people- centric service sector like insurance. In insurance sector, CRM cannot be achieved without having an effective procedure for redressing the complaints of dissatisfied customers. The study is based on the secondary data collected from IRDA annual reports and research papers from various journals. The study evaluates the performance of the Life Insurance sector regarding redressal of grievances escalated to IRDA. The study also presents a comprehensive view of grievance redressal procedure followed by LIC of India, the only public sector life insurance company working in India. An effort also has been made to find out relationship between number of policies sold and grievance received to find out the ith year in which grievance is likely to come.

Keywords: Grievance, Grievance redressal, Life Insurance, Customer Relationship Management, Insurance Regulatory and Assessment Authority (IRDA)

INTRODUCTION

Insurance sector has been liberalised in 2000. After liberalisation, insurance industry has seen tremendous growth. As, number of players is increasing in the market and competition is becoming fierce, Customer Relationship Management is gaining more attention (Amarpreet Singh Ghura and Siddharth M. Bhome, 2004).Customer Relationship Management is a suitable strategy for better taking care of the customers (Biswamohan Das and Sabyasachi Das, 2013). ‘Grievance’ is the last word any businessman wants to hear. A grievance without resolution leads to dissatisfaction beyond control. The redressal of customer grievances is a pre – requisite for ensuing long term relationship with customers and customer loyalty in service industry like insurance (Deepa Sharma, 2010). Life insurance contract is a long term contract between the life assured and insurance company. Both the parties are bound to fulfil obligations lies with them. Life assured i.e. the policyholder is required to pay premiums as and when becomes due and in contravention to it, insurance company is required to pay the consideration by way of claims as and when becomes due as per the policy conditions. Grievances occur when any of the services are not provided by insurance company not in proper manner or in time. Causes of grievances may be non-receipt of policy bond, mistake in policy bond, change in address, change in nomination, assignment, reassignment, payment of periodical amount during policy term, raising of loan, surrender of policy, maturity claim or death claim, etc. Poor work quality, non – accountability in every day performance and failure to review the process are other important causes of grievance.

An efficient insurer is one who has an effective mechanism not only for providing excellent service but for redressing the complaints of customers. Implementing Customer Relationship Management is one of the important tools that will help managers and companies to increase the satisfaction and loyalty of customers (Raman S. and Uma K, 2015).

GRIEVANCE/COMPLAINT

A “Grievance/complaint” is defined as any communication that expresses dissatisfaction about an action or lack of action, about the standard of service/deficiency of service of an insurance company and/or any intermediary or asks for remedial action. (Source: IRDA Guidelines for Grievance Redressal by Insurance Companies). In other words, Grievance may be the dissatisfaction arisen due to deficiency of service provided to the customer by the insurance company or its representative. Grievances are clearly distinguished from inquiries and requests. In today’s scenario of insurance market, with the large volume of insurance transactions and huge customer size, it is an accepted fact that there will be growing number of policyholder grievances for every insurance providing company (R. K. Yadav, S. Mohania).

There are three types of grievances in each segment—1. General Grievances, 2. Claim Related Grievances and 3. Acknowledgement Grievances.

General grievances include grievances related to initial proposal submissions, rendering the documents to policyholders and doing corrections etc. General grievances erupt in the start of the policy issuance process and just after the issuance of policy.

The claim related grievances are more complex and sensitive grievances which may occur at the start of policy issuance and may occur after some years. Such grievances are mostly related to claims. Claims can be of maturity, survival benefit payment, surrender value payment, policy loan, death claim, policy loan interest etc. Except death claim, other types of claim generally arise after 3 to 5 years of start of the policy because all other types of claims are payable only when policyholder has paid three years full premiums. Without paying three years premium, policy does not bear cash value or paid up value as per the actuarial and prudential norms.

Acknowledgement grievances occurred when acknowledgement by concerned officer of reporting the grievance is denied.

REVIEW OF LITERATURE

The review of given studies provides a broad spectrum of work done in the area of grievance redressal in insurance sector and provided basis for the formulation of appropriate objective and methodology for the present study.

G.Johary (2007) attempts to give a comprehensive view of Grievance Redressal System currently in vogue in General Insurance Industry and also suggest an alternative dispute resolution mechanism. He also proposes that there is a need to have an independent redressal system, exclusively for the insurance industry.

According to analysis conducted by Shilpy Sinha and Preeti Kulkarni , Published in ‘The Economic Times’ , Nov 9,2011, “The Protection of Policyholder’s interest, it seems, is on the top of the agenda of IRDA. Yet, one cannot deny the need for a campaign to create awareness about the intricacies of the existing grievance redressal mechanism.

Dr A. Lenin Jothi and Ms. V. Gupta (2012) attempted to give a brief introduction of in house and external grievance redressal mechanism in Indian Life Insurance Industry. The authors also insist that a well-defined and strengthened mechanism will definitely pave the way to customer satisfaction.

Dr. M. Syed Ibrahim and Shakeel- ul- Rehman (2012) provided insights into consumer protection and the awareness with reference to the grievance settlement operations of the life insurance industry in India. According to the authors, IRDA is playing an important role in the areas of consumer protection and education and consumer grievance redressal.

S.Kaur Bawa and N.Kaur (2014) evaluates the performance of the general insurer regarding the solution of the grievances and compares the performance of general public insurer and general private insurer in terms of effective handling of complaints.

S. Raman and K. Uma (2015) emphasizes that grievance redressal mechanism affects customer relationship management. The author also reveals that speed, sensitivity and accuracy is required on the part of the insurers towards grievances in the fastest time possible.

SIGNIFICANCE OF GRIEVANCE REDRESSAL

Grievances/Complaints lead to dissatisfaction which hampers loyalty of customers. It is a confirmed fact that one dissatisfied customer will spread the message more earnestly than a satisfied customer. Therefore, customer grievance redressal has to be laid at the top most concern from the perspective of the insurance company. An effective and speedy grievance redressal not only helps winning back a losing customer but also gaining more loyal customers. An effective grievance redressal mechanism helps understand customer from his point of view which always provides scope for improving service quality. If grievances are redressed on time, it creates goodwill of insurance company in the marketplace.

As per the regulation 5 of IRDA, Regulation for Protection of Policy holder’s Interest, 2002, all insurers should have speedy and effective Grievance Redressal System and has issued instructions that every insurer shall have a Board approved Grievance Redressal Policy and it has to be filed with IRDA.

GRIEVANCE REDRESSAL PROCEDURE OF LIC OF INDIA

Purpose:

The main purpose of Grievance Redressal Policy is to place an appropriate mechanism where the customer believes that he/she has been wronged by any act of the company is given a fair opportunity to redress his/her grievances. In compliance of IRDA provisions and with an objective of providing dedicated service, LIC of India has framed a Grievance Redressal Policy to strengthen the redressal mechanism and to reinforce the commitment of serving the customers with sensitivity, accountability, transparency and fairness.

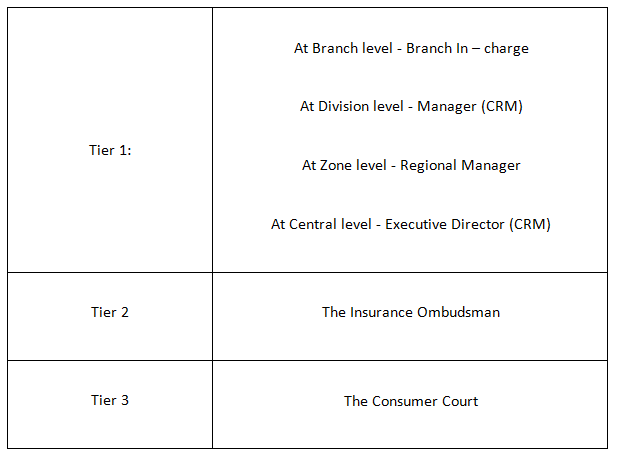

Procedure:

At every level from lowest to highest office at tier 1, there shall be a grievance redressal officer as under-

The respective grievance redressal officers will be available on all Mondays between 2:30 PM to 4:30 PM at their offices for personal interviews with the customers. This is a physical interface to lodge the complaint. Another interface can be electronic interface which includes voice based (Interactive voice response system, Telephonic conversation or both, Text message, Missed call interface, etc.) and web based (Through website, Mobile app, E-mail, Live chat, Social media, etc.). Tier 2 and Tier 3 include external grievance redressal bodies in case customer is not satisfied with Tier 1 grievance redressal mechanism.

A centralised system known as “Integrated Complaint Management System (ICMS)” is made available on website of Life Insurance Corporation of India (www.licindia.in) for online registration of grievances by policy holders. The idea behind ICMS is to monitor the complaints and analyse the patterns. After registration of grievances, a complaint registration number is allotted immediately which can be used for future references as well as for viewing the status of the complaint. In select cities, Special servicing centres called “CUSTOMER ZONES” are also functioning for grievance registration.

Repudiation of death claims:

With an objective of redressing the grievances related to repudiated death claims, Claim Review Committees are formed which function at zonal level and central level. Claim Review Committee consists of senior officers and Hon’ble retired judge of High Court.

Policy Holder Councils and Zonal Advisory Boards:

At all divisional centres, policy holder councils are formed. These councils represent the interest of the policy holders and interact on consumer concerns. Similarly, at all zonal centres, Zonal Advisory Boards are functioning.

Turnaround Time (TAT) and Process of resolution of Grievance:

1. Written acknowledgement will be sent to the customer within three working days of receipt of grievance.

2. The acknowledgement will contain name and designation of the officer who will deal with the grievance.

3. It will specify the approximate time required for redressing the grievance.

4. The final letter of resolution/rejection will be sent to customer not letter than two weeks.

5. The final letter of resolution/rejection should also contain how to pursue the complaint if dissatisfied with the decision.

External Grievance Redressal:

If the policy holder is not satisfied with the solution provided by the insurance company, he has the opportunity to lodge the complaint to the external bodies. These bodies could be the IRDA, Grievance Redressal Cell, Ombudsman, Consumer Court, Civil Court and Supreme Court.

“Alternative Dispute Resolution (ADR)”, as an alternative to litigation is also available to save time and money of both the parties. The most commonly used methods of ADR are negotiation, mediation, conciliation, and arbitration.

THE MODEL

The grievances received by LIC and private insurer in ith year should be function of number of policies issued in jth year. The grievance may rise any time of the policy term. The type of grievance may be estimated on the basis of year in which it erupts. For example, the grievance may arise just after the issuance of policies than ith Year = jth Year and such grievances can be of different nature than the grievances arising after certain gap.

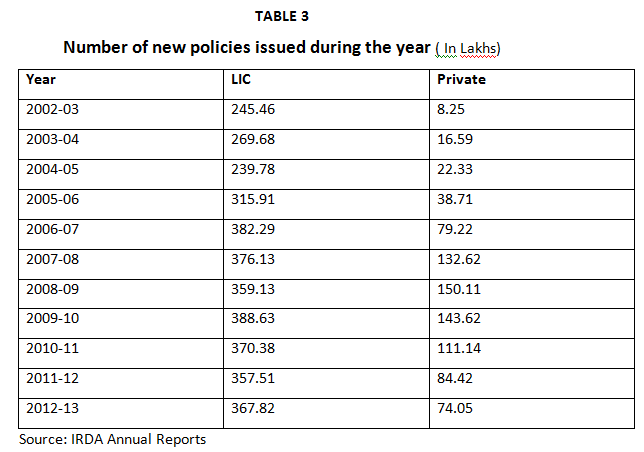

Here, researcher wants to gain insight into relationship between number of grievances received by life insurer in ith year (i = 1.2.3.4.5…..,n) and number of policies issued in jth year (j = 1,2,3,4,5………,k). As per data available, number of policies issued data ranges from 2002-03 to 2012-13 and number of grievances reported each year ranges from 2004-05 to 2012-13. Here values of i>=j.

The dependent variable is Number of Grievances (NOGi) received in ith year and independent variable is number of policies (NOPj) issued in jth year. The model can be defined as follows---

The researcher tries to explore two things from the model:

(1) Nature of relationship between dependent variable (NOGi) and independent variable (NOPj)

Nature of relationship between two variables can be linear and nonlinear. Researcher wishes to explore what is the nature of relationship among the two variables and related coefficients and constants. This will help in predicting the number of grievances expected in ith year on the basis of number of policies issued in jth year. To determine best model fit, coefficient of determination (R) and Adjusted coefficient of determination (R Squared).

(2) The year of grievance reportth year. The model can be defined as follows---

The researcher tries to explore two things from the

model---his, company can plan its CRM setup to handle the grievances efficiently. Moreover, companies can pre-emptively work upon those set of policyholders from jth year who can most likely report a grievance.

OBJECTIVES OF THE STUDY

The primary objectives of the study are:

(a) To understand and examine the process and structure of Grievance Redressal Mechanism available to customers of Life Insurance Corporation of India,

(b) To evaluate the relationship between policies sold in jth year and grievances occurred in ith year,

(c) To analyse the performance of public and private life insurance companies in terms of grievance redressal operations,

(d) To give suggestion for the improvement of the grievance redressal operations in the Life insurance Industry in India.

HYPOTHESIS OF THE STUDY

Correlation between the variables is denoted by ρ. Following hypotheses are tested for the mentioned variables---

(a) Null hypothesis: There is a significant relationship between policies sold in jth year and grievances occurred in ith year (H0: ρ = 0;)

(b) Alternative hypothesis : There is no significant relationship between policies sold in jth year and grievances occurred in ith year (HA: ρ ≠ 0 or HA: ρ< 0 or HA: ρ> 0)

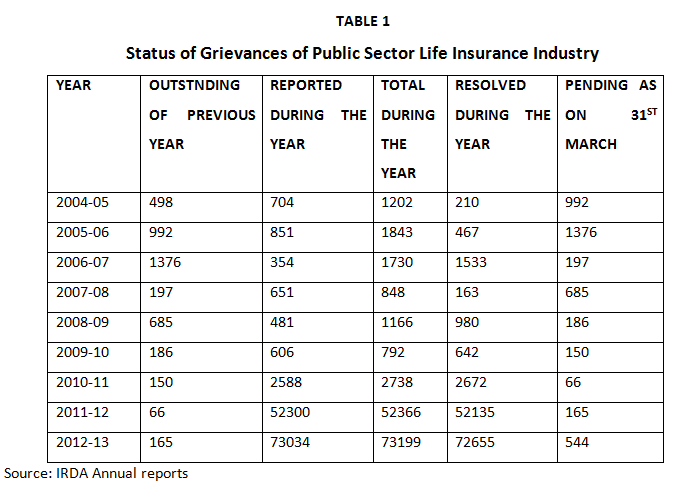

Table 1 shows that number of complaints in Public Sector Life Insurance Company is increasing every year after 2008-09 but number of complaints resolved is also increasing with a satisfactory rate. During the year 2004-05, only 17% of the total complaints recorded against Life Insurance Corporation of India were resolved while this ratio was 25% during the year 2005-06.During the year 2006-07, least numbers of complaints was recorded and approximately 90% of the total complaints were resolved. Even though number of complaints is very high during the years 2011-12 and 2012-13, more than 99% of total complaints were resolved by the insurance company.

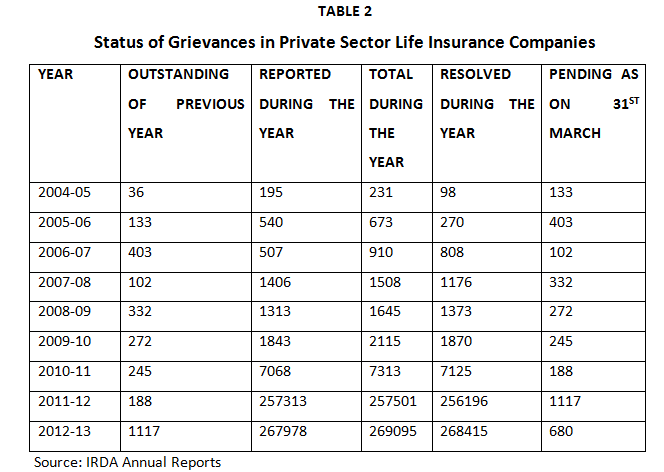

It is seen in the table 2 that the total number of complaints reported against private sector life insurance companies during the year has increased year after year but consequently there is a remarkable increase in settling of the complaints over the study period. There are various causes of increase in grievances at a fast pace but most prominent is ‘unfair business practises’.

Overall, if we look at both the sectors of life insurance industry, there has been a visible increase in the number of consumer complaints. The figure clearly reflects that attending to customer grievances is one of the biggest challenges that confront the insurance companies.

Private insurers reported complaints at a high rate than public insurers pertained to issues such as non- completion of proposal forms, non- receipts of premium receipts/ policy documents, extension of loans, surrender value not received, delay in settlements of claims, corruption against agent/ insurer, selling of wrong products, etc.

The whole analysis depicts that private insurers have proved to be more efficient in resolving the complaints as they have settled complaints at a higher rate than public insurers. The year wise analysis states that the maximum number of complaints has been handled effectively by the private insurers in almost all the years. Complaints resolving percentage has been increased in the recent years because of implementation of ‘Integrated Grievance Management System.

THE METHOD

Researcher assumes that selling style influences the eruption of grievances. If selling is a type of mis-selling than there are higher chances of grievances to be reported in coming time. In year, life insurance companies generally follow the same king of products selling because of ripple effect. If one set of companies follow selling a particular product with specific selling style, other companies tend to follow because of its visible success with set of companies and practice of selling same kind of product and same kind of selling styles through same kind of flyers. If this is true, than point of time of complaint eruption should be related to the year in which policy is issued with all life insurer companies. For example, if a (Pa) policy is issued by (A) company in jth year and if company receives complain for this policy in ith year , there should high chances that Policyissued by (B) company in jth year will have high chances of receiving complaint in ith year because (B) company might have followed the selling style and product type of (A) company if (A) company achieved success in selling style and product type.

To capture this phenomenon, researcher has adopted a step wise approach to compare the two data series of grievances received in ith year and number of policies issued in jth year. As data for number of policies issued is available from 2002-03 to 2012-13 and number of grievance received is available from 2004-05 to 2012-13, the minimum gap between ith year and jth year is 2 years. In stepwise approach, researcher computed correlation between number of policies data of 2002-03 to 2010-11 and number of grievances data of 2004-05 to 2012-13 with gap (i –j) of 2 years. After this step, the gap (i – j) is increased to 3 years and correlation is calculated between number of policies data of 2002-03 and number of grievances data of 2005-06 and so on. To maintain the same number of observation in each series data, the same number of observations in number of policies data is deleted from years-tail end to match with the same number of observations in number of policies data deleted at initial years.

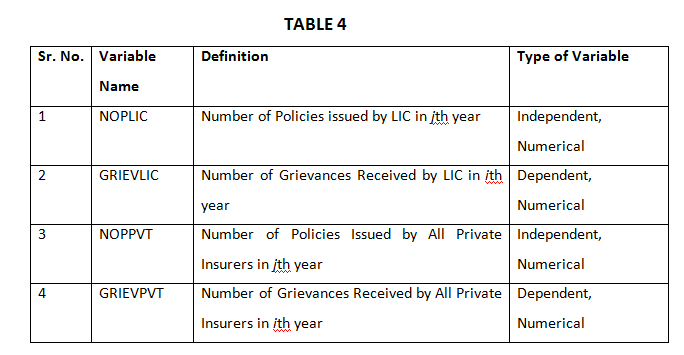

Notably, LIC of India, a public sector insurer is having more than 75 market share and other 23 private life insurers share the rest. Hence, researcher decided to have separate model fit for both types of insurers. Hence, correlation for number of policies issued by LIC (NOPLIC) in jth year and number of grievances received by LIC (GRIEVLIC) in ith year is calculated. Similarly, correlation for number of policies (NOPPVT) issued by all private insurers in jth year and number of grievances (GRIEVPVT) received by all private insurers in ith year.

After calculation of correlations with each step, the significant correlations between NOPLIC and GRIEVLIC for each step are analyzed at 5% and 1% significance levels. Correlations which have alpha value less than 0.05 and 0.01 are selected to determine the existence and nature of relationship. After ascertaining correlations for particular year step, the curve estimation is carried out observe the relationship between number of policies in jth year and number of grievances received in ith year. Curve estimation is used to determine the nature of relationship and calculating constants to predict the number of grievances to be received in ith year from number of policies issued in jth year.

DATA ANALYSIS

The data analysis is carried out in IBM SPSS Statistics Ver. 20. The correlation is calculated between the two variables. The NOPLIC and NOPPVT are regarded as dependent variables. GRIEVLIC and GRIEVPVT are regarded as independent variables. Definitions of each variable is as follows---

Data analysis is divided in two parts-- Correlation analysis and curve estimation.

CORRELATION ANALYSIS

Following correlations are found significant at 0.05 and 0.01 levels---

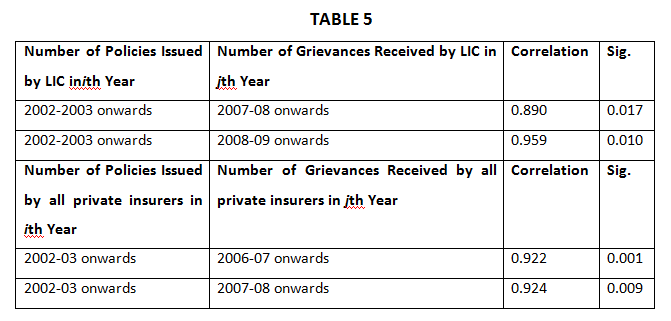

By observing TABLE 5, it is found that there is strong positive correlation between NOPLIC issued at jth year and GRIEVLIC at (i =j + 5) th year and at (i =j + 6) th year at p=0.017 and p=0.010 respectively. Similarly, there is strong correlation between NOPPVT issued in jth year and GRIEVPVT in (i =j+4) th year and (i =j + 5) th year at p=0.001 and p=0.009.

CURVE ESTIMATION

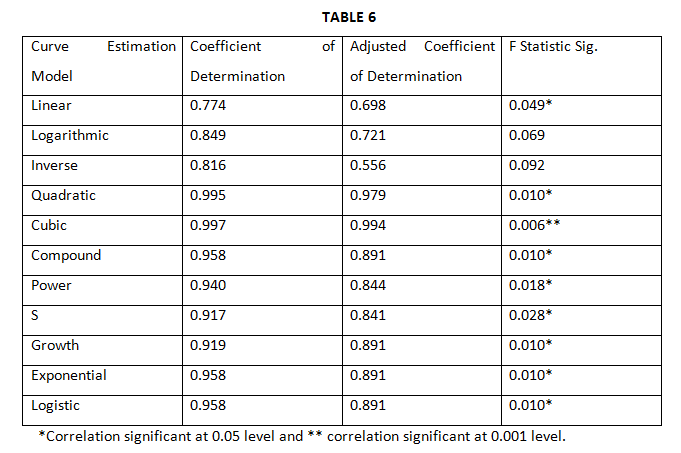

Curve estimation is used to find the best fitting model for the Equation 1. The relationship between the two variables can be linear and nonlinear. Researcher has observed the NOP and NOG for following options and calculated coefficient of determination and adjusted coefficient of determination at 0.05 levels(see table 6)---

Source: Self

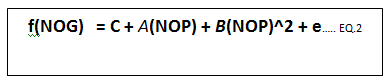

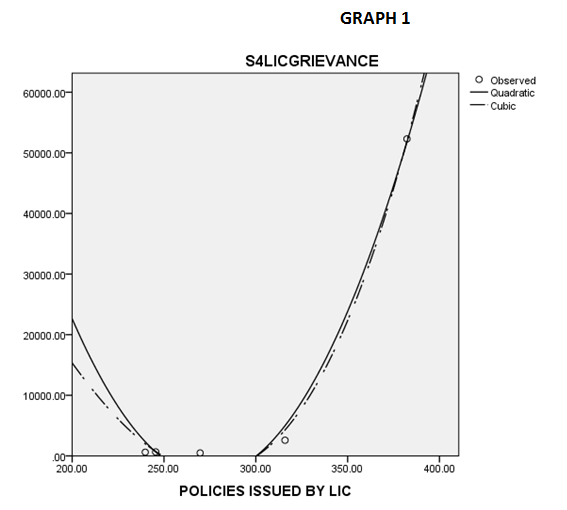

It is very apparent from TABLE 3 that Curve model in Cubic from is found significant at 0.05 and 0.01 levels. Hence, the relationship between the NOP and NOG is nonlinear and cubic. Yet, the researcher selects the quadratic function form as it is simpler than cubic form. Resultantly, the equation no. 1 can be expanded in following way to represent the model----

The graph 1 represents quadratic relationship between NOG and NOP----

GRAPH 1

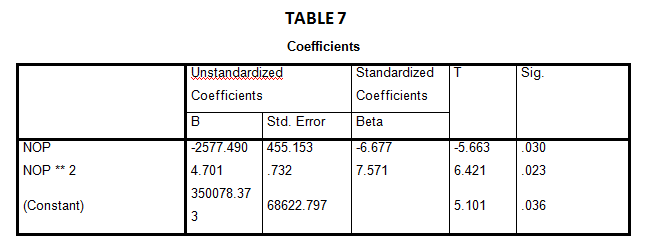

A, B and C are coefficients and D is the constant in equation 2. The term (e) in the equation 2 is error term. Table 7 shows values of each coefficient and constant for cubic function relationship between NOG and NOP—

Values of coefficients A, B and constant C are (-2577.49), (4.701) and 350078.373 respectively. Therefore, the equation 2 can be numerically reproduced as follows---

HYPOTHESIS TESTING

We hypothesized that there is a significant relationship between policies sold in jth year and grievances occurred in ith year (H0: ρ = 0;). It is concluded from above study that there is a significant relationship between policies issued by public sector life insurance company and grievance occurred in 5th and 6th years. Similarly, there is a strong relationship between policies issued by private sector life insurance companies and grievance occurred in 4th and 5th years. Therefore, alternative hypothesis was rejected.

SUGGESTIONS AND RECOMMENDATIONS

Following suggestions may be helpful to control and handle grievances:

1. After fourth year, primarily claims related and supplementrily acknowledgement grievances occur.

2. The customers mainly grumble about the delay in claim settlement. Claim settlement procedure should be simplified and less time consuming. Speedy and efficient customer service and claim settlement can lead to less grievances.

3. Many customers give complaints and their complaints are not being taken into consideration. This lead to acknowledgement grievance. Wherever, the customer lodges a complaint, it should be treated promptly and sympathetically.

4. Unfriendly attitude of employees also make customer annoying. The employees deployed for resolution of grievances should be well equipped with job knowledge, capacity to understand the grievance and very much courteous.

5. Grievances are showing increasing trend which requires more comprehensive analysis of complaints at higher level.

6. Most of the customers are not aware about mechanism available for redressing their grievances. Brief description of grievance redressal mechanism should be provided in policy bond. Print media, visual media and internet can also be used to make customers aware about these mechanisms. Life assured should also be educated regarding the importance of proper nomination and their rights, claims process, dos and don’ts etc to avoid any inconvenience.

CONCLUSION

The insurance sector plays a very important role in economic development of a nation. Customer grievance redressal plays yet another very important role for better customer relationship management. The entire insurance business rests mutual trust and harmonious relationship between insurer and insured. The study has been undertaken to assess type of grievances generally occur. By handling the grievances of policyholders effectively and efficiently, the insurance companies can create a win-win situation for both the parties.

REFERENCES

Books

1. 1.Amarpreet Singh Ghura and Shraddha M. Bhoome (2004), “Customer Relationship Management- A Theory and Practice to Manage and Retain Customers” Industrial Book House Pvt. Ltd., , P 13-15

2. Sharma, D. (2010), “Consumer Protection and Grievance Redress in India- A Study of Insurance Industry”, Lambert Academic Publication

Journals

4. A. LethinJothi, A. L., Gupta V. (2012), “Consumer Grievance Redressal System in Indian Insurance Industry” The International Journal of Economic and Business Studies, Vol. 1, Issue 7, pp 34- 38

5. Das, B., Das S. (2013), “Stretegic Customer Relationship Through CRM: A Study of Perception of Insurance officials” The International Research Journal of Commerce and Behavioural Science, Vol.2, Issue 11 (Sep.), pp 20-27

6. Bhardwaj, C. L. (2011), “A Journey Towards Proactive Customer Care- Grievance Management in Insurance”IRDA Journal, Nov., pp 14-19

7. Johary., G. (2007), “A Critical look at Grievance Redressal Mechanism in Indian Insurance Industry”Published in Insurance Times October and November issue, Accessed on 27 April 2015

8. Kumar, J.(2008), “Product does not matter, services does”, The Journal of Insurance Institute of India, Vol. 34, Issue (July- Dec), pp 32-35

9. Ibrahim, M. S.,Rehman, S. ur (2012), “Consumer’s Grievance Redressal System in the Indian Life Insurance Industry- An Analysis”South Asian Journal of Marketing and Management Research, Vol. 2, Issue 6 (June), pp 215-227

10. Yadav, R. K., Mohania, S. (2014)’ “Role of Insurance Ombudsman and Grievance Management in Life Insurance Services in Indian Perspective”, International Letters of Social and Humanistic Sciences, Vol. 31, pp 9-13

11. Raman, S., Uma, K. (2015), “Grievance Redressal Mechanism in Indian Life Insurance Industry” Indian Journal of Arts, Vol. 5, Issue 13, pp 3-6

12. Sadri, S. (2009), “Insurance Marketing”SCMS Journal of Indian Management, Vol. 6, Issue 2,

13. Bawa, S. K.,Kaur, N. (2014), “Customer Grievance Redressal in India: A Case of General Insurance Sector”Journal of The Insurance Institute of India, Vol. 1, Issue 4(Apr- Jun), pp 152-159

Press Releases

1. Sinha, S., Kulkarni, P. Published in ‘The Economic Times’ , Nov 9,2011, Accessed on 22nd April 2015 104-115

2. Customer Grievance Redressal policy, Pursuant to Board Resolution No. 371/51-01 dated 26 Nov. 2010

3. Press release by IRDA on 16.09.2013

4. Annual Reports of IRDA from 2002-03 to 2012-13

Websites

5. www.Policyholder.gov.in

6. www.irda.gov.in

7. www.licindia.in

8. www.niapune.com

9. www.shodhganga.inflibnet.ac.in

10. www.igms.irda.gov.in

11. www.dpg.gov.in

12. www.discovery.org.in