Porter’s Five Forces Industry Analysis of Indian Passenger Car Industry

|

Dr. Jeannie Bhatia

Assistant Professor (International Business and Marketing)

Department of Business Studies

D.A.V. Institute of Management

NH-3, NIT, Faridabad

Haryana - 121001

Email: jeanniebhatia@gmail.com

Contact No.- +91 9891739262

|

Abstract

Passenger car industry is one of the key industries in India as well as the world. Since the compulsive and ambitious structural adjustment programme of Indian government aimed at economic liberalization in 1991, the Indian car industry has sailed along. With the reforms in economy and the sector, the car market with significantly low penetration level immense market size, coupled with rise in the per capita and disposable income of the working population, has made it an attractive destination for global automobile players. Considering the significance of the sector at the global level, the present analytical study was undertaken to analyze the recent trends and provide a situational inventory based onPorter’s five forcesmodel. The analysis findings suggest that the overall attractiveness of the Indian car industry in the present scenario may be rated as moderate. Though, with the projections pertaining to the expected growth rate in the coming years and potential in the niche Indian rural market along with the favorable government initiatives the axis of the attractiveness would fall on the higher side.

Keywords: Industry Analysis, Porter’s five Forces Analysis, Indian Passenger Car Industry

Introduction

The key industries of a national economy largely determines the growth prospects.Peter F. Drucker, the founding father of the study of management coined the automobile industry as "theindustry of industries" in 1946(Peter and Yannis, 1994), and it has been a major constituent ofsurface transport and plays a vital role ineconomic growth of a country. Morespecifically, the passenger car industries in manycountries have proven to be one of the strongestdrivers of technology, growth, and employmentand its advancement has characterized globalcompetitiveness of leading industrializedeconomies in the last few years (Gottschalk and Kalmbach, 2007).The various tax reliefs by the Government ofIndia including de-licensing, an provision of 100 per cent FDI under the automatic route in the auto sector, abolition of phased manufacturingprogramme, reduction of excise duty and importduties of 'Completely Knocked Down Units(CKD)' and 'Completely Built Up Units (CBU)' (Mukherjee, 1997),inclusion of automobile sector under Make in India Campaign with a commitment to indigenization schedules;complemented by the country's large middleclass population with a growing earning power, strongtechnological capability and availability oftrained manpower at competitive prices attracteda large number of multinational auto companies,especially from Japan, South Korea, U.S.A. andEurope to enter the Indian markets (Delloite, 2011; KPMG, 2015). Furthermore,the intensely low penetration level of 19 cars perthousand people, and an untapped niche marketin terms of rural Indian markets, offers theglobal passenger car industry with anopportunity for colossal growth and acompetitive environment.

A number of studies have been undertaken in thepast, but still there exists a gap to exhibit thepotential untapped passenger car market in theIndian scenario touse acumen of the industry to the existing andpotential car manufacturers. This paper is anattempt to make an inclusive situational analysisof such a scenario by carrying out Industryanalysis of the Indian passenger car industry using the Porter’s five forces analysis model. Itis expected that findings of the study shall be ofsuccor to the car manufacturers in determiningtheir future course pertaining to the grand andcorporate level strategies in regard to the Indianmarket.

Indian automobile and Passenger Car Industry

1.An Insight into the Journey of PostLiberalization Era

Since the 1980s, the Indian car industry has seena major resurgence with the opening up ofIndian shores to foreign manufacturers andcollaborators. Post the BOP crisis of 1990 and the bail out from the InternationalMonetary Fund, the Indian government had totake a course of expedient actions towardliberalization and deregulation (Jenkins, 1999; Joshi and Little, 1996). Thisperiod became the melting point for the industry in India when large number of foreign playerscame into the country through collaborationsand partnerships. (Yeong-Hyun, 2003) described it as a shift fromCLP (controls, licenses and protectionism) toLPG (liberalization, privatization andglobalization).The face of the Indian industry has beenchanging in the post-economic liberalization era;remarkable changes have been seen in thepassenger car industry. According to (Mukherjee and Sastry, 1996), most ofthe major global automobile companies wereeither operative in India or were in the processof launching in the country by the year 1996. Asa result, while initially there were only aboutthree vehicles to choose from, consumers nowhave a wide variety of options (Mukherjee and Sastry, 1996).Further in 1997, some more reforms were madewhere new foreign entrants required establishingactual production facilities, followed by further alterations in 2002, the government’s policyallowing 100 per cent foreign direct investmentin Indian automobile industry. With the reason,the Indian auto industry became a level playingfield, with government’s role reduced toproviding direction to the industry. Given themerits of market potential and the newautomobile policy, it attracted a large number ofautomobile companies and almost all the globalauto companies established facilities in India (Mukherjee, 1997).

India witnessed a rushed entry of global carmanufacturers in the auto industry, includingGM and Ford from US, Toyota and Honda from Japan, Fiat, BMW, Mercedes-Benz, Audi,Volkswagen, Volvo, and Porsche from Europeand Hyundai and Daewoo from South Koreahaving set up new production facilities aroundthe country resulting in tremendous increase inthe production levels, from 2 million in 1992 to9.7 million in 2006. India’s passenger carindustry has experienced a wave of new models,and unprecedented marketing wars amongautomobile companies in the past decade.

To maintain this high rate of growth and toretain the attractiveness of Indian market and forfurther enhancing the competitiveness of Indiancompanies, the Government through theDevelopment Council on Automobile and AlliedIndustries constituted a Task Force to draw up aten year Mission Plan for the Indian AutomotiveIndustry (Govt. of India, 2007). The plan was to focus on giving ashape to a futuristic plan of action with fullparticipation of the stakeholders towards thegrowth of industry. Besides making concertedefforts for removal of obstacles for acceleratedgrowth, the prime need was to put in placerequired infrastructure well in time to facilitategrowth. Through this, Government wanted to provide a level playing field to all players in thesector and to lay a predictable direction ofgrowth to enable the manufacturers to take moreinformed investment decision (Govt. of India, 2007; Nag, 2008).Released in 2007, the plan visualized India as anemerging destination of choice in the world fordesign and manufacture of automobiles and autocomponents with output accounting for morethan 10 per cent of the GDP and providingadditional employment to 25 million people by 2016 (Govt. of India 2007). Every major shift in policies made bythe Indian government, the automotive industryhas come out stronger and better.

It is paradoxical that the Indianmiddle class, the most attractive feature forforeign investment in the liberalization phase,was an outcome of the statist ideologies in theregulatory phase. The product innovations ofdomestic firms like Tata Motors and Bajaj Autoare the fruits of indigenization and protectionpolicies of the regulatory phases (Ranawat and Tiwari, 2009).Presently this industry is fully capable ofproducing and targeting all the segments in thepassenger car industry with some of the leadingnames echoing in the Indian automobile industry includes Maruti Suzuki, Tata Motors, Mahindraand Mahindra, Hyundai Motors, Honda andFord in addition to a number of others. The Indian automobile industry currently accounts for 22 per cent of the nation’s manufacturing GDP and constitute 7 per cent of country’s total GDP providing employment to nearly 19 Million people directly or indirectly. India is currently the seventh-largest producer in the world with an average annual production of 17.5 Million vehicles, of which 2.3 Million are exported. The Indian automobile market is estimated to become the 3rd largest in the world by 2016 and will account for more than 5% of global vehicle sales (Govt. of India, 2015). The passenger car industry constitute nearly 14 percent of the overall automobile industry.

2. Recent Trends in Indian Passenger Car Market

The passenger car Industry in India has shown a tremendous market potential after economicliberalization in 1990s like never before. Amongst the Asian countries,India was the fourth largest exporter ofpassenger cars with Chennai accounting forapproximately 60 per cent of the exports (Delloite, 2011).The report further explains that China is theleader with 23.51 per cent of the totalproduction, followed by Japan with 12.39 percent, USA with 9.9 per cent, Germany with 7.6per cent, South Korea with 5.5 per cent andIndia with 4.58 per cent of the total globalvehicle production in 2009-10.

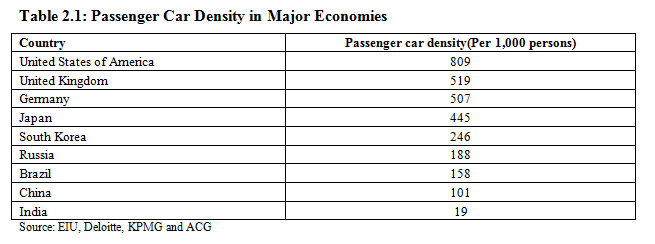

The passenger car density per thousand people in major markets of the world is highest for USA followed by Germany, UK, Japan, South Korea, Russia, Brazil, Turkey, China and India continues to have one the lowest car density. The domestic passenger car industry has been on a relatively steady growth phase over most of the last decade and has registered a 10 years CAGR of 10.3 per cent during the period. It has been one of the few markets worldwide which saw growing passenger car sales during the liquidity crisis and recessionary phase witnessed during financial year 2009 (ICRA, 2011a). Buoyant economic growth, rising disposable income levels, favorable demographics, strong growth from tier II/III cities and rural India, together with improving availability of vehicle financing at competitive interest rates have been the key factors fueling growth in the Indian passenger vehicle market.

However, since the beginning of 2011-12, the industry witnessed a slowdown in volume growth marred by rising inflation, hardening interest rates and increasing fuel prices that have combined to dent consumer sentiment. Even the festive season failed to stoke domestic demand despite new model launches, aggressive discounts and promotional schemes offered by car manufacturers during financial years of 2012, 2013 and part of 2014. Apart from macro-economic headwinds dampening demand, events such as production disruption at India’s largest car manufacturer, Maruti Suzuki, the natural calamities in Japan and Thailand also created supply chain stresses, further aggravating the weak performance of the passenger car industry (Moneycontrol, 2013; ICRA 2014; SIAM 2015).The large incumbents in the domestic carindustry derive strength from their low costmanufacturing capabilities, established vendorbase and widespread sales and service network;however, their dominance is being challenged bymultinational car manufacturers that haveentered the domestic market in the recent past(ICRA, 2011b; ICRA, 2015). Overall, it is believed that carmanufacturers may continue to face challengingtimes at least over the short term as sluggishdemand on one hand and increasing competitionon the other may restrict earnings growth.

2.1. Indian Passenger Car Market Share

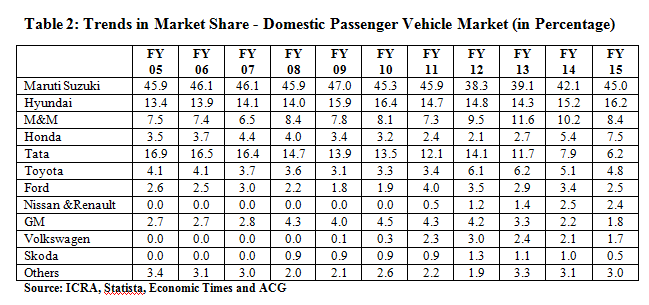

The top four players namely Suzuki, Hyundai,Mahindra and Mahindra and Hondaconstitute nearly 80 per cent of the passengercar sales thereby making it a highly concentratedmarket. However, increasing competition acrossvehicle segments is expected to lower theconcentration levels, with new players quickly gainingmarket share, though small in percentage but itis expected that the passenger car market willhave 5 or more players making up for 80 percent of the market in the near future (Table 2).Maruti Suzuki India Limited has been the all-time market leader in India since economic reforms. Though it lost the market in thefinancial year 2012 and 2013, where the industry volumeswere impacted by production disruptions. But in last couple of years it has gained back the share with launch of new products and riding on the response from the rural market. Thevolumes of all the players were also observed onthe path of slow growth due to the overall slumpand slowdown in the automobile industry in theyear 2012-13(Gupta, 2013; Economic Times, 2015; ACG, 2015; Statista, 2015). Moreover during the down phase at Maruti Suzuki (India) Limited, a part of the demand shifted to other OEMs like Toyota and Honda which gained market share that was also facilitated by their new product launches. Also, market participants having diesel models and newly launched compact SUV’s in their portfolio specifically M&M and Renault and general diesel variants offered by Tata Motors and Ford consolidated their market position.

2.2. Sales, Production and Export Trends in Indian Passenger Car Market

In India, car production has been greater thansales over the decade. The CAGR of sales andproduction were 15.8 per cent and 17.6 per centrespectively during the last decade. Thedomestic sales witnessed and reported a verystrong volume growth over the last few fiscalyears, with as much as more than 20 per centgrowth in 2010 and even higher than 25 per centin the year 2011 (Table 3). However, thedomestic passenger vehicle industry startedobserving a drastic slowdown in financial year 2012 with theyear ending at only 4 per cent year on year growth (SIAM, 2013c). After witnessing a slowdown in 2013 and a negative growth in year 2014, the industry sales has recovered with a YoY growth of 4 percent (SIAM, 2015c).

In the last few years, a number of new models andrefreshed versions of ongoing brands havebeen launched in the Indian market. This hasbeen amongst the strongest pace of new productintroductions in India so far. However, this increased supply pushhas coincided with a period of slow industryvolume expansion making it difficult for themarket to assimilate all new models. Aroundhalf of the new product introductions havereceived a lukewarm market response, exertingpressure on the profitability of OEMs as well asassociated suppliers and dealers. While growthmomentum slowed down in the passenger carssegment, the Utility Vehicle (UV) segmentcontinued to witness strong volume growthaided by increasing demand for recentlyintroduced models.

Riding majorly on the domestic demand the production trends were very similar to the sales trends (SIAM, 2013b). After seeing an exceptional growth of production at more than 25 per cent for two consecutive years in 2010 and 2011, the economic slowdown paralyzed the manufacturers specifically the major players to a point that the units had to be either shut-down or work at half the capacity for several days with piling inventory in the year 2012 and 2013 with the year-on-year growth in production posted at just 4 per cent and 3 per cent respectively (Table 4). Before observing a positive turn in last year the production like the sales also witnessed a negative turn in 2014 with 4 percent reduction and finally restoring the levels similar to 2013 in the financial year 2015 (SIAM, 2015c).

Counter-balancing the declining domestic sales due to the subdued sentiments in the domestic auto market, a concerted export push and has kept the country's biggest car makers in good stead. Growing exports also offers a partial hedge on foreign exchange exposures at a time when the rupee has been vacillating sharply.

Maruti Suzuki and the other major players in thecountry took a conscious call in lieu of theslowing European markets, which accounted formore than 70 per cent of their exports and took anote of the need to develop alternate markets.Consequently new market in Latin America,Africa and the ASEAN countries were targetedand as a result now the dependence on Europeanmarkets has come down to just 25 per cent andcurrently 75 per cent of vehicle exports aregoing to Non-European markets.Although the economy is adversely affected dueto a falling rupee but it is proving beneficial asfar as the exports are concerned. This is beingattributed as one of the reasons for growingexports in the sector (SIAM, 2013c; SIAM, 2015c). The exports in thesector has seen a continuous growth every yearover the decade, except for the 0.4 per centdecline in 2011, which was majorly attributed tothe dependence over the European marketswhich entered an economic turmoil during theperiod (Table 5). With the manufacturersrealizing and developing the new markets, theexport has again seen respectable growth in 2012 and 2013despite an overall slowdown even in the Asianand non-European markets (SIAM, 2013c). Even when the domestic sales was down in 2014 the exports steadily grew at 6 percent and by another 4 per cent in 2015.

Research Methodology

The presented research is descriptive cum analytical in nature and is purely based on secondary data collected from various authentic and reliable sources like the reports and statistics provided by Society of Indian Automobile Manufacturers (SIAM), Automotive Component Manufacturer’s Association ACMA), ICRA and Moody’s, Economist Intelligence Unit (EIU) and Deloitte, Autobei Consulting Group (ACG), International Organization of Motor Vehicle Manufacturers (OICA), Govt. of India, trade journals and white papers, industry portals, monitoring industry news and developments, and research articles published by authors.

Porter’s Five Forces Industry Analysis

Backed by robust volumes as well as realizations, car manufacturers have registered a phenomenal growth across the world over the past few years. The situation in the domestic industry is no exception. In fact, it enjoyed a double digit growth rate backed by a robust growing economy over the last decade. Car manufacturers are always subject to industry forces which they would have to keep dealing with constantly. And irrespective of the size or stature of the business or its dominance of the market in terms of brand value or market share, there is no escaping the fact that these competitive forces could dislodge the car manufacturing company from its position of dominance in the market at a quick turn of events.

Porter (1979) and Porter (2008) listed down five major forces of competition that applies to every industry including to that of the car manufacturers that needs to be kept track of, if they have to succeed in the complex world of industry dynamics and competitive strategy. The five competitive forces that shape strategy includes:

· Threat of New entrants

· Bargaining power of Suppliers

· Bargaining Power of Buyers

· Threat of Substitute products or services

· Intensity of Rivalry among existing competitors.

This study analyzes the economic and market forces that will ultimately influence the car manufacturing industry in India through Michael Porter's five force model so as to understand the competitiveness of the sector.

Automobile industry in India is an emerging sector and has a huge potential to improve. The increasing GDP and economical resources have boost up during the last decade which has increased purchasing power of the Indian consumer. The car segment in India has emerged as one of the promising sector and has shown growth trends in tremendous production, sales and exports (The Equicom Research, 2013). Despite economic slowdown, the Indian automobile sector has shown high growth. The passenger vehicle market, which constitutes around 80 per cent of automobile sales, has immense growth potential as passenger car stock which stood at around 13 per 1,000 people in 2011 (Delloite, 2011) increased to around 19 to 20 per 1,000 people in 2012-15 (Trefis, 2013, KPMG, 2015). The other reasons attracting global auto manufacturers to India are the country’s large middle class population, growing earning power, strong technological capability, availability of trained manpower at competitive prices and the recently launched ‘Make in India’ campaign of the government.

1. Threat of New Entrants

According to Porter (2008), the new entrants bring new capacity and a desire to gain market share that puts pressure on prices, costs, and the rate of investment necessary to compete in an industry. Thus, the threat of new entrants puts a cap on the profit potential of an industry. The threat of entry in an industry is determined by the level of entry barriers that are present and on the reaction entrants can expect from incumbents. The barriers to entry includes the factors like Economies of Scale and Capital requirement; Brand identity, Product Differentiation and Customer Switching Costs; Access to technology, raw material and Channels of distribution; and Government policies and protection.

· Economies of Scale and Capital requirement as a barrier for new entrants in the automobile industry, an enormous amount of capital is required. Besides capital, a new firm that is interested in entering the market needs to conduct in-depth research beforehand. An entering firm would need a tremendous amount of implicit and explicit knowledge in order to design and manufacture a product that has never been presented or offered before. An automobile manufacturing facility is very specific and specialized; therefore in the event of a failure or malfunction, the cost of repair is extensive. In recent years the international majors like Renault, Nissan, Volkswagen, Fiat etc. have overcome this factor by inculcating strategies like alliances initially with domestic players, or alliances based on Badge engineering for their manufacturing and marketing in case of Fiat with Tata and Renault with Mahindra and Mahindra or setting up the facilities in alliances like Renault - Nissan and Volkswagen for its offered brands including Skoda, Volkswagen and Audi (Business Line, 2012; and Ramanathan and Raj, 2013). Though on this factor it may be stated that large amount of capital for entering the industry is required and that economy of scale prevails and make it a significantly difficult for new entrants to enter the industry.

· Brand identity, Product Differentiation and Customer Switching Costs: Brand identity is a crucial barrier to entry. Exclusive high quality car brands have established extremely high brand equity-value over time. This is one of the main reasons why the public is willing to pay premium price for it. Although the barriers to this exclusive market are substantial, there are various ways around this obstacle. Companies who are well established in the automobile sector may enter the new market (luxury cars) through strategic partnerships or through buying out or merging with other companies. Maruti Suzuki India Limited, a subsidiary of Suzuki Motor Corporation of Japan is India's largest and leading passenger car companies which presently hold a share of over 45 per cent of the domestic car market, despite the entry of many multinationals over the years, post liberalization. Although, in recent years Tata Motors which was leader in commercial vehicle segment has emerged as key player in Indian Passenger Vehicles as well with a market share of 16.45 per cent. Tata motors recently entered the luxury and premium segment with the acquisition of Jaguar and Land Rover Brands on one hand and launched the world’s cheapest car “Nano” on the other, which changed and shifted the automobile sector paradigm as many other companies have started focusing on the cheapest segment of the industry (The Equicom Research, 2013). Other key players in automobile segment of India have also performed well and have contributed significantly and the scenario in market is attracting other international brands to the market. With the increasing per capita income and purchasing power of the Indian population, the sale of luxury cars has grown and market share has gained over the years and India is projected to be amongst top three luxury car market by 2020 (Malhi, 2013).

· Many foreign automobile manufacturers are aggressively entering high growth emerging markets such as India amidst slowing demand in the developed economies. Volkswagen has succeeded in establishing its brand in the Indian market since its entry in 2008. After its entry into India, Volkswagen’s Polo, along with Ford India’s Figo and General Motors India’s Beat have managed to capture the market share from the companies such as Maruti, Hyundai and Tata Motors Ltd. The threat of new entrants is high for the car industry in general but specifically for the small car segment it is very high. The growing economy and the increasing buying power of the customers have made every automobile player to grab the opportunity in small car segment. There are around five new players coming in to the small car market; H800 from Hyundai priced around 1.6 lack, Maruti Cervo 600 priced 1.6 lacks, Bajaj-Nissan’s new electric car etc. Non automobile players also have their focus in this segment like Ajanta Manufacturing limited has launched electric car ‘Orevo’. Barriers for entering would include economies of scale, competition from existing players, customer switching costs and the investment decisions.

· Other factors like access to raw material, technology and distribution channel in the automobile industry are concerned, are not easily accessible or easy to establish. With the new regulation policies pertaining to fuel emission, efficiency and a projected efficiency rating; rising fuel prices; downturn in the economic scenario and new segments like compact sedans, compact SUVs, luxury hatchbacks etc. (Bhanushali, 2013; Baggonkar, 2013). Having created and established by the existing competitors, it would be really challenging for the potential new entrants in the industry to bring out such technologically advanced products that can compete in the existing market. Another barriers for the new entrant and even the recently entered players in the industry would be to compete with the major players like Maruti Suzuki, Hyundai and Tata’s which has established and provides the dealership and service networks for their vehicle even in the remote countryside areas of the country (Gupta, 2013). With the saturating urban demands and huge countryside market potentials, the distribution channels are going to play a significant role in the future course and direction of the car market.

· Government policies and protection for the sector: since the automobile sector in India is a crucial aspect of its growing economy and the GDP, the government has liberalized the policies pertaining to the sector. Currently, the Government of India allows 100 per cent foreign direct investment (FDI) in the automotive industry through automatic route and is also planning to introduce fuel-efficiency ratings for automobiles to encourage sale of cars that consume less petrol or diesel along with the plans to accelerate the supply of electric vehicles over the next eight years (IBEF, 2006 and 2013). Another major step taken by government to promote the industry is the Make in India Campaign launched in 2014 and Automobile industry is a major component of it.

From the present scenario pertaining to the Threat of New Entrants in the car manufacturing industry in India, it may be concluded on the basis of the above discussions on the factors including Economies of Scale and Capital requirement; Brand identity, Product Differentiation and Customer Switching Costs; Access to technology, raw material and Channels of distribution; and Government policies and protection, that the threat is moderately on the higher side, and hence Industry attractiveness from this aspect is moderately low.

2. Bargaining Power of Suppliers

The automobile industry is considered to be highly Capital and Labor intensive as the major part of the cost of production include wage bills of labor; material costs including that of steel, aluminum, dashboards, seats, tires etc.; and intensive advertising and market research activities. Though, the automotive market majorly comprise of the vehicles, but the auto parts make up the other half of the industry which includes the parts manufactured by the original equipment manufacturers themselves and the replacement parts or accessories and other rubber fabrications that are procured from the suppliers in the industry (Investopedia, 2013).

The suppliers play a vital role in the value chain of the automobile industry and affect the crucial aspects including the lead times and even the overall quality of the products, and thus, analyzing the bargaining power of the suppliers in the Indian automobile industry is significant. According to Porter (2008), the parameters on which the bargaining power of suppliers can be assessed includes the number of suppliers present, availability of substitutes for suppliers available to the manufacturers, contribution of suppliers in cost and quality and the importance of the industry for the suppliers.

· As far asnumber of suppliers in Indian automotive industry is concerned, there are more than 500 auto component manufacturers in the organized sector which are largely represented by the Automotive Components Manufacturer’s Association of India - ACMA apart from other 5000 manufacturers in the unorganized sector which caters to the domestic market demand and also export a significant share of its output (Automotive Mission Plan, 2006-16). Apart from the available large number of suppliers in almost all the categories of required components the manufacturers also have an alternative to source the auto components from the nations which have the free trade agreements with India and from the countries for which India has lowered the duties and taxes including the auto technology majors like Japan, South Korea and even Thailand and other low cost labor oriented nations including China, Malaysia and South Africa (ICRA, 2011b).

· As far as the contribution of suppliers in cost and quality of the product is concerned, it is significant in the automobile sector, but with the alternatives available to the manufacturers ranging from the large number of domestic suppliers to globally available sources which have excelled in the technology over the years it does not extends the bargaining power to the suppliers in the industry (ICRA, 2011b).

Thus, on the aspect of the bargaining power of suppliers in the Indian automobile industry, based on the noteworthy dependence of the component suppliers on the domestically growing industry and a downturn in the economies globally on one hand and the alternatives available with the manufacturers for the sourcing component ranging from domestic to global suppliers on the other, it may be concluded that the overall bargaining power with the suppliers in the present Indian automobile scenario is either moderate or low.

3. Bargaining Power of Buyers

In today’s competitive environment and customer driven markets, the bargaining power of the buyers or customers is significant and influence every decision that the manufacturers make and the automobile industry is no different in this case. According to Porter (2008), the bargaining power of buyers can be assessed on the basis of number of buyers in the industry, the availability of substitutes, switching costs involved and the contribution of buyers in the cost and quality.

· The Indian automobile industry has been enjoying the CAGR of around 10 per cent over the last decade and with the potential in unexplored and rural markets, it is expected to continue the run over the coming many years (Deloitte, 2011). With an increased purchasing power, a developing state of the economy and large untapped rural markets, the number of potential customers in India is huge and all the existing manufacturers as well as the proposed new entrants can expect to grow enormously in those areas.

· Though with the changing preferences, income graphs and saturating urban markets on one hand and increasing number of alternatives, be it mode of transportation, types of vehicles or the number of brands and their products ranging from hatchbacks and sedans to SUVs and luxury segments, the power of choosing from the available alternatives lies with the customers. At present there are 9 Indian and 15 foreign manufacturers producing or assembling nearly 120 models and their variants locally apart from another 100 models that are imported by the car manufacturers as complete built units. Further, most of the car manufacturers are either proposed to launch new models or are developing newer ones to be launched in Indian market over the next few years (Surfindia, 2013).

· In the automobile industry with low switching costs involved and since most of the brands are new in the market except from the few established ones, the brand loyalty aspect does not impact much, and thus the manufacturers are continuously challenged to bring out more efficient and quality vehicles at the lowest possible costs. Apart from that the manufacturers have to incur a significant amount on the market research at the time of development and on advertising and promotion at the time of launch and sale of the product, which constitutes a large part of the overall cost of the product(Bradley, Bruns, Fleming, Ling, Margolin, Roman and Flury, 2005).

Thus, it may be concluded that the relationship between the car industry and its buyers or purchasers of finished vehicles, the power axis is tipped towards the consumers. The Consumers enjoys the greatest power in this relationship due to the fairly standardized nature of the commodity and the low switching costs associated with selecting from among competing brands. However, the automotive industry remains marginally powerful due to the large customer to producer ratio.

4. Threats from Substitutes

The threat to a car manufacturer is not just that a customer would buy a different brand of car but they also need to consider the likelihood of a potential customer taking the alternative modes of transport including bus, train or airplane to their destination. The higher the cost of operating a vehicle, the more likely people will seek alternative transportation options (Investopedia, 2013). The factor of fuel prices has a large effect on consumer’s decisions to buy vehicles. Apart from the cost while determining the availability of substitutes the factors including time, money, personal preference and convenience are also considered in the travel industry. According to Porter (2008), while analyzing the threat from substitutes, one need to consider the parameters including availability of close substitutes, switching cost and substitute’s price and value.

· As far as the scenario of travel industry in India is concerned, rail and air travel comprise of 10 per cent of the total passenger travel and rest 90 per cent of passenger travel is undertaken by roads (World Bank, 2013). And this share of road travel encompass 72 per cent of two-wheelers, 14 per cent of passenger vehicles including cars, jeeps and taxis and rest 14 of other public transport busses and non-passenger vehicles (Govt. of India, 2011). The biggest and ever emerging available substitute for passenger cars is the two-wheeler segment, which has grown from 8 per cent at the time of independence to the whopping 72 per cent in the present scenario. And this one segment has very low switching cost and price. There have been efforts from the respective state governments to promote the public transportation modes, but the positive shift in the incomes and purchasing power graphs has increased the usage of private vehicles. Although in metro cities like Delhi, there has been a marginal increase in usage of the economical public transport, with the start of the dedicated metro rail projects, and considering the response of commuters a number of other such projects have been proposed and approved for other metro cities (The Indian Express, 2012).

Based on the evidences and reports on the factors pertaining to the threat from substitutes to the Indian car industry, it may be concluded that threat is significantly high and thus the industry attractiveness on this aspect is low.

5. Intensity of Industry Rivalry

The auto industry is considered to be an oligopoly around the globe, which helps to minimize the effects of price-based competition (Investopedia, 2013). Though, while taking a note of Indian automobile industry, the industry rivalry has been divided into two major phases: the phase before the economic reforms in 1991 and the other post the reforms. In the first phase there were only three major players including the Maruti Udyog, Hindustan Motors and Premier Automobiles which were competing in the passenger car segment which were not even able to meet the market demand during that time. Such factors and other economic circumstances led to the economic reforms and with the opening up of a market for foreign players that had enormous potential, the attractiveness was very high. At present the Indian customer has more than 20 domestic and foreign players offering 120 locally manufactured models and their variants apart from other foreign players offering another 100 imported models in almost all the price bands ranging from ` 1.45 Lakh to whopping amount of ` 20 Cr. to choose from (Morey, 2013; Silicon India, 2013).

Porter (2008) suggests considering parameters that includes number of competitors, industry growth rate, product differentiation, switching costs involved and the strategic stakes of the manufacturers to assess the industry rivalry among existing competitors.

· The number of competitors in the Indian car market has grown significantly in last decade and many others are expected to arrive over the next few years with 100 per cent FDI allowed in Indian automobile sector (Philip, 2013) and the sector being included in the Make in India Campaign. The industry has grown with a CAGR of 10 per cent over the last decade and though it might have slowed down over the current economic crunch across the globe, but is expected to continue the growth over the next few years (Delloite, 2011; and IBEF, 2013).

· The intense product war in the Indian car market with minimal differentiation, almost every player offers one or more products in the defined segments. The extreme competition exists in the small car or the hatchback segment which constitutes nearly 80 per cent of the total car sales (ICRA, 2011a). Though, in last few years the SUV and luxury segment with a CAGR of nearly 30 per cent has also witnessed a close competition (Thakker, 2012). The companies have focused on new product launches, be it the newer enhanced versions of the existing products or launching a new product altogether in the market. The new product war is so intense that the major players are considering it as one of the major strategies to capture and increase their market share, since the market shares have picked up for auto majors like Honda, Maruti Suzuki, Renault, Ford and others after their recently launched products have been well accepted by the consumers (Bhargava, 2013).

· With decreasing brand loyalty among customers, number of available alternatives and nature of commodity with low switching costs, the manufacturers need to review, revive and enhance their customer experience on a continuous basis and with the intensity of competition it only increases the rivalry (Capgemini, 2013). Car Manufacturing/Assembling industry being capital intensive in nature involves high strategic stakes of the competitors involved in the industry. Though, most of the major players be it Maruti Suzuki (Now wholly owned by Suzuki), Tata, Mahindra and Mahindra, Toyota, Ford and others, do have their diversified businesses be it in two-wheeler or commercial vehicles; or entirely conglomerate in nature, but the stakes in this industry for all the players are very high.

Based on the reports and analysis on the factors including number of competitors, growth rate, differentiation, switching costs and the strategic stakes involved it may be concluded that the intensity of rivalry is skewed towards the higher side and thus the attractiveness in the industry may be rated as considerably low in this aspect.

Discussions and Conclusions

India assisted by its economic advancement,liberalization policy and government initiatives and massive marketing strategies by carmanufacturers and auto finance companies isexperiencing fast growth of domestic andforeign car manufacturers producing and sellingmany new car models during the recent past.Foreign car manufacturers havediscovered the Indian consumer as well as the R& D potential in the Indian technical fraternityand are setting up manufacturing plants right andleft across the country seeking cost advantages.

The Indian automobile industry is currentlyexperiencing volatility in demandfor all car segments. This scenario has beentriggered primarily by increase in disposableincomes and standards of living of middle classIndian families; and the Indian government'sliberalization measures such as relaxation of theforeign exchange and equity regulations,reduction of tariffs on imports, and bankingliberalization has fueled financing-drivenpurchases; and global economic turmoil.

Presently, among the car manufacturers in theIndian car industry, most are multinationalcompanies, who entered after the Indianeconomy opened up; Maruti Suzuki is one of thefew Indian manufacturers on the scene andoccupies approximately half of the market shareand is maintaining its share despite the stiffcompetition from manufacturers like Hyundaiand Tata Motors, who occupies over one fifth ofthe market share. The Indian car industry isdominated by Korean and Japanese automakersas compared to their western counterparts. TheIndian car industry is still in the growth andevolution stage and is depending on thedomestic regional and rural market. Though thegrowing export figures even in the time ofeconomic slowdown as the manufacturers timelyshifted to new markets, exhibits the level ofestablishment among the players. But the bleakmarket demand and decreasing figures in thedomestic sales have forced the marketers toexplore newer countryside and semi-urbanmarkets.

The overall attractiveness of the Indian car industry in the present scenario with moderate threat from new entrants; reasonably low bargaining power of suppliers; significantly high bargaining power of buyers; ominous threat from substitutes; and high intensity of rivalry; may be rated as moderate. Though, with the projections pertaining to the expected growth rate in the coming years and potential in the niche Indian rural market the axis of the attractiveness would fall on the higher side.

References

ACG (2015). Indian Passenger Vehicle Research Report FY 15. Autobei Consulting Group.

Baggonkar, S. (2013). Mercedes Benz India to launch more compact luxury cars below Rs. 30 Lakh. The Business Standard, Dated 12 July.

Bhanushali, S. (2013) Ford Ecosport and the upcoming crop of compact crossovers. Retrieved from http://www.oncars.in/Car-Article-Detail/ford-ecosport-and-the-upcoming-crop-of-compact-crossovers/230/1.

Bhargava, Y. (2013) Car Makers bet on new launches to rev up sales. The Hindu, Dated 24 July.

Bradley, D., Bruns, M., Fleming, A., Ling, J., Margolin, L., Roman, F. and Flury, A. (2005). Automotive Industry Analysis. Retrieved from http://www.srl.gatech.edu/ Members/ bbradley/me6753.industryanalysis.pdf.

Business Line (2012). Volkswagen to reposition Skoda, other brands in India. The Hindu Business Line, Dated 4 November.

Capgemini (2013). Cars online 12/13: My Car My Way. Retrieved from http:// www.in.capgemini.com/thought-leadership/capgeminicom-cars-online-1213-my-car-my-way.

Deloitte (2011) Driving Through BRIC Markets - Industry Report.

Economic Times (2015) Maruti Suzuki boosts passenger vehicle market share to 42% in FY14. Retrieved from http://articles.economictimes.indiatimes.com/2014-04-11/news/49058710_1_honda-cars-india-maruti-suzuki-india-passenger-vehicle-sales

EIU (2015) Economic Intelligence Unit Automotive Database and Views-wire. Retrieved from http://www.eiu.com/default.aspx.

Gottschalk, B. and Kalmbach, R. (2007). Mastering Automotive Challenges. Kogan Page, London.

Government of India (2007). Automotive Mission Plan - A Mission for development of Indian Automobile Industry (2006-16), Ministry of Heavy Industries and Public Enterprises.

Government of India (2015). Make In India – Automobile Sector Information. Retrieved from http://www.makeinindia.com/sector/automobiles/

Gupta, N.S. (2013). For car companies road to growth lies in countryside. The Times of India. Retrieved from http://timesofindia.indiatimes.com/business/india-business/For-car-companies-road-to-growth-lies-in-countryside/articleshow/19286376.cms.

IBEF (2013). Automobile industry in India. India Brand Equity Foundation. Retrieved from http://www.ibef.org/industry/india-automobiles.aspx.

ICRA (2011a). Indian Passenger Vehicle Industry - (March Report).

ICRA (2011b). Indian Passenger Vehicle Industry - (December Report).

ICRA (2014). Indian Passenger Vehicle Industry - (December Report).

ICRA (2015). Indian Passenger Vehicle Industry - (July Report).

India Brand Equity Foundation (2006). Automotive Report by KPMG for IBEF Retrieved from http://www.ibef.org/download%5C Automotive_220708.pdf.

Investopedia (2013). The Industry Handbook: Automobiles. Retrieved on 24-07-2013 from http://www.investopedia.com/features/industryhandbook/automobile.asp.

Jenkins, R. (1999). Democratic Politics and Economic Reform in India. Cambridge University Press, Cambridge, UK.

Joshi, V., & Little, I. M. D. (1996). India's Economic Reforms: 1991-2001. Oxford University Press.

KPMG (2015) Global Automotive Executive Survey.

Malhi, M. (2013). HNIs will make India a top 3 luxury car market by 2020. Retrieved from http://www.automotiveworld.com/analysis/oems-and-markets/hnis-will-make-india-a-top-3-luxury-car-market-by-2020.

Moneycontrol (2013). Auto Sluggish Trends Continue post festive season, 2013. Retrieved from http://www.moneycontrol.com/news/icra-reports/auto-sluggish-rendscontinue-post-festive-season_ 809425.html.

Morey, T. (2013). 10 most expansive cars in India. Retrieved from http://www.mensxp.com/fine-living/auto/8089-10-most-expensive-cars-in-india.html.

Mukherjee, A. (1997). The Indian Automobile Industry: Speeding into The Future?. International Auto Industry Colloquium, Paris (June). Retrieved from www.univ-evry.fr/labos/gerpisa/actes/ 28/28-4.pdf.

Mukherjee, A. and Sastry, T. (1996). Entry Strategies in Emerging Economies: The Case of the Indian Automobile Industry. Indian Institute of Management, Ahmedabad, Retrieved from dspace.mit.edu/bitstream/handle/1721.1/1631/Sastry1.pdf.

Nag, B. (2008) Trade Liberalisation and International Production Networks in Asia: Experience of Indian Automotive Sector. Indian Institute for Foreign Trade, 7.

Peter, B. and Yannis, K.K. (1994), Radical Reform in the Automotive Industry. International Finance Corporation Discussion Paper No.21. The World Bank, Washington D.C.

Philip, L. (2013). Global car Makers proton Peugeot, Citron, Kia shelves India plans due to tough financial conditions. The Economic Times, Dated 18 March.

Porter, M.E. (1979). How Competitive Forces Shape Strategy. Harvard Business Review, 57(2).

Porter, M.E. (2008). The Five Competitive Forces That Shape Strategy. Harvard Business Review, 86(1).

Ramanathan, A. and Raj, A. (2013) Renault-Nissan to invest $2.5 Billion in five years in India. Live Mint, Dated 16 July.

Ranawat, M. and Tiwari, R. (2009). Influence of government policies on industry development: The case of India's automotive industry. Working Paper No. 57, Hamburg University of Technology, Germany.

SIAM (2013). Industry Statistics - Domestic Sales Trends. Society of Indian Automobile Manufacturers. Retrieved from http://www.siamindia.com/scripts /domestic-sales-trend.aspx.

SIAM (2013b). Industry Statistics - Production Trends. Society of Indian Automobile Manufacturers. Retrieved from http://www.siamindia.com /scripts/production-trend.aspx.

SIAM (2013c). Industry Statistics - Export Trends. Retrieved from http://www.siamindia.com/scripts/export-trend.aspx.

SIAM (2015). Industry Statistics - Domestic Sales Trends. Society of Indian Automobile Manufacturers. Retrieved from http://www.siamindia.com/statistics.aspx?mpgid=8&pgidtrail=14.

SIAM (2015b). Industry Statistics - Production Trends. Society of Indian Automobile Manufacturers. Retrieved from http://www.siamindia.com/statistics.aspx?mpgid=8&pgidtrail=13.

SIAM (2015c). Industry Statistics - Export Trends. Retrieved from http://www.siamindia.com/statistics.aspx?mpgid=8&pgidtrail=15.

Silicon India (2013). 8 cheapest petrol cars in India. Retrieved from http://www.siliconindia.com/news/life/8-Cheapest-Petrol-Cars-in-India-nid-144266-cid-51.html.

Statista (2015). Passenger car market share in India in FY 2014 statistics. Retrieved from http://www.statista.com/statistics/316850/indian-passenger-car-market-share/

Surfindia (2013). Car Models in India. Retrieved on 28-07-2013 from http://www.surfindia.com/automobile/ car-models.html.

Thakker, K. (2012). Luxury car market to grow slowest in 10 years: Andreas Schaaf, MD, BMW. The Economic Times, Dated 30July.

The Equicom Research (2013). Special Report on Automobile Sector - The Equicom Research. Retrieved from http://mcxcontrol.com/2013/04/27/special-report-automobile-sectore-theequicom -research.

The Indian Express (2012). Govt. to support 19 Metro rail projects: PM. The Indian Express, Dated 13 September.

Trefis (2013). Honda looks to ‘Amaze’ in India as market still offers huge growth. Retrieved from http://www.trefis.com/stock/hmc/articles /189583/honda-looks-to-amaze-in-india-as-market-still-offers-huge-growth/2013-06-04.

World Bank (2013). India Transport Sector. Retrieved from http://web.worldbank.org/website/ external/countries/southasiaext/extsarregtoptransport/content.html.

Yeong-Hyun, K.I.M. (2003). Global Auto Companies and their Supplier Relations in India. Onzieme Rencontre Internationale Du Gerpisa Eleventh Gerpisa International Colloquium.