Impact of Capital structure on Firm’s Profitability: A Study of Selected listed Cement Companies in India

|

Mr. Bhushan Singh & Dr. Mohinder Singh

Research Scholar

Department of Accounting and Finance

School of Business and Management Studies

Central University of Himachal Pradesh, Dharamshala, Himachal Pradesh, India- 176206

Email: singhatlas1973@gmail.com

Contact No.- +91 9418459015

|

Abstract

The objective of this study is to investigate the impact of capital structure on firm’s profitability through the selected cement companies in India. The study is based on secondary data i.e. five years financial statements collected from PROWESS data base of CMIE. Based on correlation coefficient, study found a significant negative relationship between debt and profitability meaning that companies with higher proportion of debt tend to have low profitability.

Keywords: Capital Structure, Return on Capital Employed, Gross Profit.

JEL- G32, L61, and, O53

Introduction

Cement industry is among the one of largest industries of the world and occupies the predominant place as one of the basic industry for development and it has capacity to provide employment opportunities for large no of people. Cement rank next to steel in construction material and so is the basis of all modern construction.

India’s cement industry is world second largest industry with the share of around 7 percent of total world cement production being china on the top with share of around 35 percent of total world cement production. In year 2014 Indian cement industry has completed its 100 years of existence. In its journey of a century, there had been several period in which cement industry is hit hard due to Government policies while some spell provided relief too. Through all this, the constant has been a continuous shortfall in the infrastructure support – power, coal and railway wagons (Source: Ministry of Commerce).

The exponential growth posted by the cement industry can be seen from the fact that the cement industry took 83 long years to touch the first 100 Mt. capacity, while for adding the second and third 100 Mt. mark, the period was substantially compressed to 11 years and 3 years respectively. The cement industry reached over 300 Mt. cement capacity and 168 Mt. productions in 2007-08. During year 2009-10 to 2013-14 industry has recorded about 65 percent growth in production. As we all know cement plays an important role in developing and shaping the nation, so one should study and try to give some suggestion to improvement of the industry. (Source: - ministry of commerce, government of India, cement manufacturer association o, Department of industrial policy and promotion (DIPP) and Cement Corporation of India).

An optimum Capital structure plays an important role in the growth and progress of any company. An optimum capital structure refers to is one which gives maximum return to the shareholders. So it needs proper care and attention in determining an optimum capital structure. Solomon and Fred Weston (1973), “The proper and right combination of debt and equity will always lead to market value enhancement.” The term capital structure refers to the kinds of securities and the proportionate amount that makes up capitalization. It is the mix of different long term sources of finance like shares equity or preference, bond or debentures, funded debt long term or short term and retained earnings. The importance of capital structure is validated by the different academician like Modigliani & Miller (1950), David Durand (1952) and Ezta Solomon & Fred Weston (1973) have documented the significance of financing decisions on firm’s profitability. Capital structure has diverged combinations and company needs to identify the one which gives the maximum return to its shareholders.

Review of Literature

Capital structure always remains the topic of interest among Researcher, academician, students and business firms. Numerous studies have been carried out in this field on national and international level. For the clear understanding of the topic the relationship between capital structure and profitability some of the major studies have been reviewed as follow;

Based on 35 companies listed at Hong Cong Stock Exchange, Chiang et al., (2002) found that capital structure and profitability are related with each other. Baral (2004) in his study on determinants of capital structure found that size, growth rate and earning are statistically significant determinant’s of capital structure. Abor (2005) studied the relationship among capital structure and profitability in Ghana and found the significant positive relationship between short term debt to ROE and negative relationship between long term debt to ROE. Hall et al. (2004) in their study found that age is positively related to long-term debt but negatively related to short-term debt. Booth et al, (2001) in ten developing countries, and Huang and Song (2002) in their study in China, found that tangibility is significantly negatively associated to leverage. It is contend, however, that this relation depends on the type of debt. .Dimitris, M. & Maria, P. (2008) studied the relationship between capital structure, ownership structure and firm performance across different industries using a sample of French manufacturing firms. They found that there is a negative relationship profitability and leverage. Chisti et al. (2013) in their study on capital structure and profitability found that debt and equity ratio is negatively correlated with profitability. On other hand debt to assets ratio and interest coverage ratio is significantly associated with the profitability of companies. Tailab M (2014) made a study on analyzing factor effecting profitability of non-financial US firms and found that leverage, inventory, growth and age a negative significant impact on ROA, while liquidity and size in term of sale has significant positive effect on profitability of US firm. However an insignificant relation has found between size in term of asset and return on asset. Mohamed and Tailab (2014) in their study on the effect of capital structure on profitability of energy American Firms found that total debt have singnificant negative impact on ROE and ROA. Gill et al., (2011) try to extend the findings of Abor (2005) on relationship among capital structure and profitability. They have taken sample from American service and manufacturing firms. The Empirical results of the study show a positive relationship between short-term debt to total assets and profitability and between total debt to total assets and profitability in the service industry. The results of the paper also show a positive relationship between short-term debt to total assets and profitability, long-term debt to total assets and profitability, and between total debt to total assets and profitability in the manufacturing industry. Velnampy and Niresh(2012) in their study on banking sector found that there is a significant negative relationship between debt equity ratio (D/E) and return on equity (ROE).The other studies in this area by Haldlock and James (2002), Mesquitaand Lara (2003), Pandey (2004), Philips and sipahioglu (2004) , Huang and Song (2006) , Arbabiyan and Safari (2009) , Chakraborty (2010) also validates the results some of them confirm the positive relationship between capital structure and profitability and other found negative relationship among variables.

Research Gap

Numerous studies have been carried out in this field but most of them belong to other parts of the world, only few studies have been taken place in India. But none of those studies has been given special importance to cement industry; most of studies have used variables like long term fund and short term funds to find relationship. In present study an attempt has been made to find the association among capital structure and profitability by adding some new variables like Debt to total fund and gross profit ratios compare to previous studies. Because debt to total fund ratio give us the wide view on debt and equity mix as it compare debt with the total funds available in business. Sometime due to the large amount of indirect expenses net profit of firm become very low, so when we compare it with capital structure it shows low profitability so to eliminate this problem gross profit ratio has been taken into the study.

Rationale of Study

The growth of a firm depends upon several factors like the efficiency of management, nature of business, size of business and type of financing etc. So by word type of financing we mean debt and equity or capital structure number of academicians like Modigliani & Miller, David Durand, Ezta Solomon & Fred Weston has proved that good capital structure of a firm can enhance its value. So in this study an attempt was made to find the association among capital structure and profitability. The study will be useful to those who are associated with cement industries like owners, shareholders, supplier, management, investors etc. It will help the owner to design an optimum capital structure, supplier to assess that credibility of firm, shareholder to assess the financial risk, management in taking financial decision and investors in investing in leveraged firm.

Conceptualization

After doing review of literature the following model has been developed. This modal of capital structure in cement industry introduce new constructs and uniquely combines them in specifying that the profitability is a function of debt to equity and debt to total funds in the capital structure.

Figure 1: Conceptualization model

Objectives

The general objective of this study is to find the relationship between financing decisions (capital structure) and the profitability of cement companies in India. Other specific objectives are as follow:

- Explore the relationship of Debt/Equity ratio with Gross Profit Ratio, Return on Capital Employed and Return on Equity.

- Explore the relationship of Debt/ Total Fund Ratio with Gross Profit Ratio, Return on Capital Employed and Return on Equity.

Database and Research Methodology

To achieve the objective, data has been collected from secondary source by going through various web sites and annual reports of the selected companies. The reference period of the study is five years i.e. which is from the financial year 2009-10 to 2013-14 during this period of time recorded 65 percent growth in production. Out of 42 cement companies listed on Bombay stock exchange (BSE) top 10 companies have been selected. These companies capture almost ninety percent of the total market share of cement Industry.

Debt to equity ratio and debt to total fund ratio have been taken as proxy variables for Capital structure and profitability has been measured by return on capital, return on equity and gross profit ratio. Mean and Standard deviation of all these ratios and Pearson product correlation analysis has been computed with the help of SPSS to find the relationship between capital structure and profitability.

Results and Discussion

The first section of result and discussion discuss about the individual companies performance during the period of study.

The table 1 depicts that among all the cement companies JP cement, Ramco cement and Prism cement are highly leveraged companies having highest debt to equity ratio i.e. 1.57, 1.21 and 1.06 respectively. On the other side companies like ACC cement, Ambuja cement and Ultratech cement are low leveraged with lowest debt to equity ratio with the mean score of 0.05, 0.01 and 0.43 respectively.

It is also clear from the table that JP cement have highest standard deviation of 0.73 which indicates that this company made number of changes in its debt and equity mix over the period of time on the other hand Birla cement and India cement have lowest standard deviation of 0.05 and 0.06 which indicates that these companies have made very few changes in their capital structure.

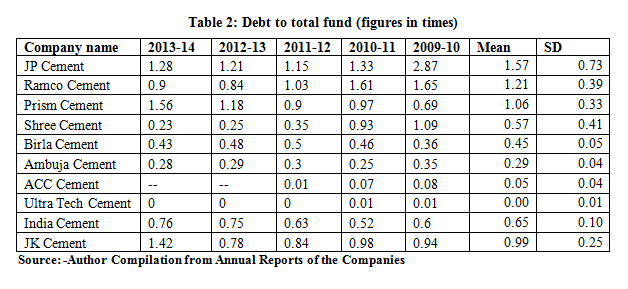

Table 2 reveals that debt to total fund ratio is also higher in case of JP cement, JK cement and Prism cement with the mean score of 1.57, 1.27, and 1.06 times respectively. On other hand Ultra Tech cement have minimum debt to total fund ratio with score 0.004 which shows that company have very less burden of debt. In addition to this company is having very low level of standard deviation with the mean score of 0.05 as compared to other companies in study. It is also clear from table that JP cement have relatively higher standard deviation as compared to other companies in study.

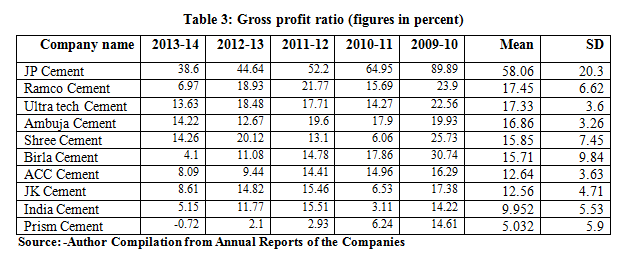

The above table 3 depicts that JP cement have highest gross profit ratio with the mean score of 58.05 and implies that this company is very efficient in producing products and have efficient resources to pay for cost required to run and grow their business. On other hand companies like Prism cement, India cement are having low gross profit ratio with mean score 5.03 and 9.9 respectively as compare to other companies in the study. This shows that companies are inefficient in producing products.

The standard deviation of gross profit ratio of JP cement, Birla cement and Shree cement is maximum (20.3, 9.8 and 7.4 respectively). It means that these companies are not consistent in generating profits. On other hand companies like Ambuja cement, Ultra tech cement and ACC cement have minimum standard deviation (i.e.3.2, 3.60 and 3.63 respectively) which implies that companies are enjoying gross profit at constant rate.

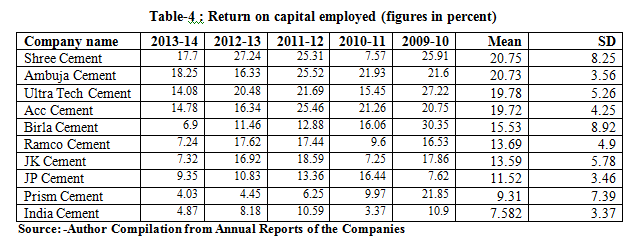

It can be observed from table 4 that return on capital employed ratio is maximum in case of Shree Cement, Ambuja Cement, and Ultra Tech Cement having the mean value of 20.7, 20.78 and 19.7 times respectively as compare to other companies in the study. It implies that these companies are using their funds efficiently and are also among the preferred choice among investors. On other side the companies like India Cement, Prism Cement and JP Cement have lowest return on capital with mean score of 7.5, 9.3 and 11.5 respectively.

Birla cement and Shree cement have shown inconsistency in their earning as reflected by high standard deviation. On the other companies like JP Cement, Ambuja Cement and ACC Cement have minimum standard deviation which implies that there is a minor fluctuation in their return.

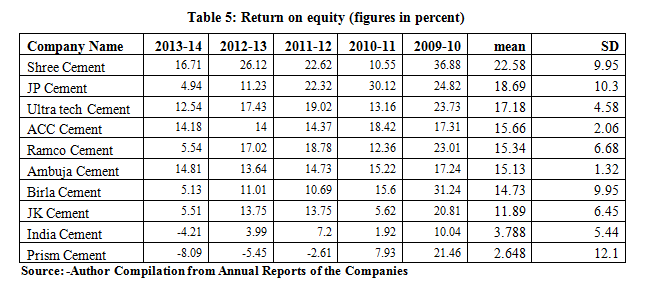

The Return on equity ratio given in table 5 is highest in case of Shree Cement, JP cement and Ultra tech cement with the mean score of 22.58, 18.69 and 17.18 respectively during study period as compare to the other companies in study. This shows that these companies are more profitable as compare to other companies in the study. So these companies may be the preferred choice among investors. On the other side Prism cement and India cement have lowest return on equity with mean score of 2.6 and 3.7 respectively.

The standard deviation of Prism cement and JP cement is maximum with the mean score of 12.1 and 10.3 respectively. It shows that there is a huge fluctuation in their returns, Ambuja cement and ACC cement shows small deviation in their returns.

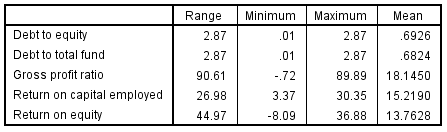

Table 6: Descriptive statistics

The overall descriptive statistics given in table 6 shows that the debt equity ratio of the sample companies is 0.692 times and debt to total fund ratio is 0.682. It means that cement companies are not using the optimum capital structure and are not in good position as far as capital gearing is concerned. Further, the minimum and maximum levels of profitability variable----GPR, ROCE and ROE depict that the returns of the companies are highly fluctuated.

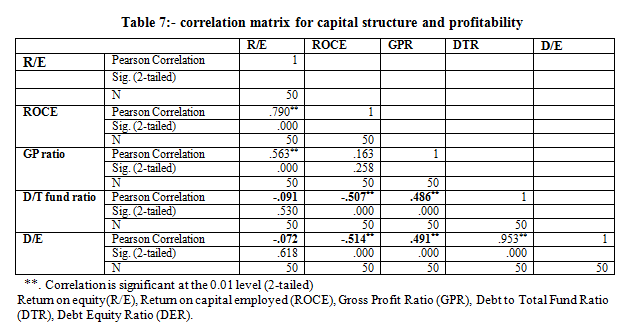

Correlation Analysis

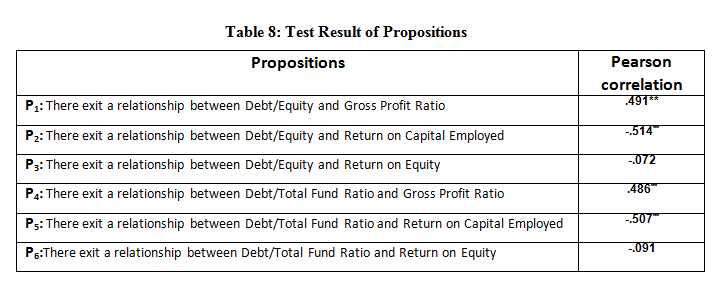

Table 7 indicates that the relationship between selected capital structure and profitability is significant negative. The negative association points toward unsuitable debt equity mix in the capital structure of the concerned companies thereby having a negative impact on the select profitability variables

Return on equity(R/E), Return on capital employed (ROCE), Gross Profit Ratio (GPR), Debt to Total Fund Ratio (DTR), Debt Equity Ratio (DER).

Now the detail of the test result of the propositions become contextual to conclude some remedial so as to overcome the existing situation and the following table show the result accordingly.

Conclusions & Discussion

Industrial firm do conduct their business in highly complex and competitive business environment today. Financial problem persisted before and will always be there, and if an industry has to move on, it should prepare itself to tackle such challenges. In this context it may be said that holding an optimum capital structure is one among pre-requisites of company for staying fit and maintaining profitability in this complex business world. In an attempt to analyze capital structure and profitability of 10 listed cement companies in India. Over a five year period from 2009 to 2014, the present study shows that firm under consideration do not have sound debt-equity composition in their capital structure and hence failed to enjoy benefits of leverage properly.

So focus should be given on the following areas to improve the existing situation in order to have positive impact on profitability of the cement industry.

· Cement companies have scope to increase debt level in their exiting capital structure so that, companies can enjoy the benefits of leverage.

· Management should focus on internal factors like Production policy, HR policy, and marketing policy so that the fluctuation in profitability can be reduced.

Limitation and Further Scope of the Study

The present study restricted only to the one specific industry, furthermore this study is only based on secondary data other form of data primary data is not taken into consideration. So the results may not be so much reliable. The study period was only for 5 years, which is from 2009 to 2014. So keeping above points in minds there are enormous scope for the research. Based on the current study following researches are possible in this area.

A researcher can do a comparative study of different industries by adding more variables in their study like size of firm, leverage, liquidity, Net profit, Earning per share etc. Study can be done with this industry by increasing the sample size, and one can also extend the study period. In this study only secondary data has been used so in future one can also go for primary data so that results can be more reliable. Same study can also be done to check the association among profitability and capital structure in other industries.

References

1. Abor, J. (2005). The effect of capital structure on profitability: empirical analysis of listed firms in Ghana. Journal of Risk Finance, 6(5), pp. 438-445.

2. Arbabiyan, A. & Safari, M. (2009).The effects of capital structure and profitability in the listed firms in Tehran Stock Exchange, Journal of Management Perspective. 33, pp. 159-175

3. Baral, J.K. (2004). Determinants of capital structure: A case study of listed companies of Nepal. The Journal of Nepalese Business Studies. I, pp.1-13

4. Chakraborty, I. (2010). Capital Structure in an emerging Stock Market: The case of India. Research in International Business and Finance. 24(3), pp. 295-314.

5. Chiang, Y.H., Chan, P.C.A. & Hui, C.M.E. (2002). Capital structure and profitability of the property and construction sectors in Hong Kong. Journal of Property Investment and Finance, 20(6), pp. 434-454

6. Chisti, A.K. Ali, K. & Sangmi, D.M. (2013) The impact of Capital structure on Profitability of Listed Companies (evidence from India). 13, pp.183-191.

7. David, D. (1959). Cost of Debt and Equity Funds for Business: Trends and Problems of Measurement. In The Management of Corporate Capital. Edited by Ezra Solomon. New York: The Free Press.

8. Gill, A., Biger, N., & Mathur, N. (2011). The effect of capital structure on profitability: Evidence from the United States. International Journal of Management, 28(4), 3.

9. Hadlock, C.J. & James, C.M. (2002). Do banks provide financial slack?. Journal of Finance, 57, pp. 383-420.

10. Modigliani, F & Miller, H.M. (1958). The cost of capital, corporation finance and theory of investment. The American economic Review. XL8, pp.261-297.

11. Mesquita and Lara. 2003. Capital structure and profitability: The Brazilian case. Working paper, Academy of Business and Administration Sciences Conference, Vancouver. pp. 11- 13

12. Maina, L., & Ishmail, M. (2014). Capital structure and financial performance in Kenya: Evidence from firms listed at the Nairobi Securities Exchange. International Journal of Social Sciences and Entrepreneurship, 1(11), pp.209-223

13. Mohamed, M. & Tailab, K. (2014). The Effect of Capital Structure on Profitability of Energy American Firms. International Journal of Business and Management Invention. 3(2), pp.54-61.

14. Phillips, P.A. and Sipahioglu, M.A. (2004). Performance implications of capital structure as evidence from quoted UK organisations with hotel interests. The Service Industries Journal, 24(5), pp. 31-51.

15. Pandey, I. M.(2004). Capital Structure, Profitability and Market Structure: Evidence from Malaysia. Asia Pacific Journal of Economics and Business, 8(2), pp.78–91.

16. Song, M. F. & Huang, G. (2006). The Determinates of Capital Structure: Evidence from China. China Economic Review. 17(1), pp. 14-36.

17. Solomon, E. (1963). The Theory of Financial Management. New York: Columbia University Press.

18. Tailab, M.M, (2014), Analyzing Factor Affecting Profitability of non-Financial US Firms. Research Journal of Finance and Accounting 5, pp.17-26.

19. http://commerce.nic.in/MOC/index.asp. retrieved on 30-apr-2015.

20. https://prowess.cmie.com/kommon/bin/sr.php?kall=wprowstat§code=010. retrieved on 20-apr-2015.