Firm Size and Profitability in Indian Automobile Industry: An Analysis

|

Neeraj Kumar

Research Scholar

Punjab School of Economics

Guru Nanak Dev University, Amritsar, Punjab, India

|

Dr. Kuldip Kaur

Professor

Punjab School of Economics

Guru Nanak Dev University, Amritsar, Punjab, India

|

Abstract

Present study is an attempt to test the size and profitability relationship in the Indian automobile industry. The empirical evidence on size and profitability is vast and showed variations in results; few reported positive and few negative relationships between size and profitability. To analyze the relationship, the linear regression model has been employed over the years 1998 to 2014 as well as cross-sectionally. For profitability, ratio of net profit to total sales turnover and ratio of net profit to net assets plus working capital has been used whereas firm size is represented by total sales turnover and net assets. The study found mix results; time-series analysis showed the positive relationship and cross-section analysis showed that there exists no relationship between firm size and profitability.

Keywords: Automobile, Size, Profitability, Assets, Turnover

Introduction

The size of a firm is the important determinant of its profitability. Many researchers tried to examine the sources of variations in firm level profitability (e.g. Hall and Weiss, 1967; Singh and Whittington, 1968; Kamerschen, 1968; Amato and Wilder, 1985; Majumdar, 1997; John and Adebayo, 2013; Dogan, 2013). It is general opinion in the field of industrial economics that big firms have more competitive power as compared to small firms. The large size may bring economies or diseconomies. The size in economic terminology, defined as ‘scale’- which may be scale of production, output or operation, constitutes, one of the important elements determining efficiency of a firm. Large firms may erect barriers to entry into the market which gives them a measure of monopoly power and degree of independence in their pricing and output decisions. Thus, it is an important cause of profitability. The size of firm may be affected by marketing, financial, technological and entrepreneurial factors. A firm well equipped with these factors, is successful in increasing its firm size. In the words of John and Adebayo (2013):

“Firm size has been recognized as an essential variable in explaining organizational profitability. The size of a firm is very essential in today’s world due to the phenomenon of economies of scale. Bigger firms can manufacture items on much lower costs in contrast to smaller firms. Firms of the modern era look to increase their size so as to get a competitive edge on their competitors by lowering production costs and increasing their market share” (p.1171).

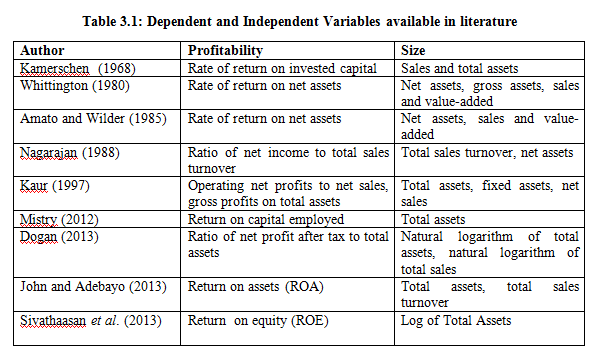

Now, it is imperative to find out the different measures of firm size which are frequently used in the industrial study. Basically, there are three measures found on the basis of different literature: first, inputs into the productive process, secondly output; thirdly ‘values’ of firm. In the first category, the number of employees of a firm, the labour input, some measures of assets representing the capital input, quantity of raw material used or amount of power consumed can be included. In the second category, physical output is rarely used as a measure of firm size; instead a monetary value such as sales turnover is widely used. Third category includes the indicators of firm size as the stock holder’s equity or value added by the firm (Kaur, 1997).

Size and Profitability: Evidence from Survey of Literature

In majority of the literature, size has been taken as a fundamental variable in explaining profitability where these studies attempted to identify the effect of firm size on profitability. The empirical evidence on size and profitability is vast and showed variations in results. Some studies reported positive and others negative relationship between size and profitability variables. The studies which showed positive relationships are Hall and Weiss (1967), Kamerschen (1968), Majumdar (1997), Jonsson (2007), Zubairi (2009), Lee (2009), Dogan (2013), Babalola and Abiodun (2013), and Sivathaasan et al. (2013).

Zubairi (2009) investigatd the size-profitabilty hypothesis in Pakistan automobile sector during 2000-2008. He found that firm size had direct effect on profitability of automobile firms in Pakistan. On the contrary Becker-Blease et al. (2010), Banchuenvijit (2012), Kouser et al. (2012) have found a negative relation between firm size and profitability. Other than above studies, Simon (1962), Whittington (1980) have found that firm size does not have any affect on profitability. They argued that firm profitability is independent from firm size. Niresh and Velnampy (2014) explored the effects of firm size on profitability of manufacturing firms in Sri Lanka during 2008-2012 and concluded that there is no indicative relationship between firm size and profitability in manufacturing firms.

The Indian Scenario

In international studies most of them support the positive relationship hypothesis between size and profitability variables. In India too, many researchers tested this relationship mostly for two and three digit manufacturing data and obtained mixed results like Nagarajan (1988), Kaur (1997) and Mistry (2012). Nagarajan (1988) tested the size-profitability relationship in pharmaceutical industry of India, using firm level data from 1970 to 1985. By using ratio of operating profits to total assets as profitability and total assets as measure of firm size the study observed some indication of a negative relationship between profitability and size. On the other hand Kaur (1997) obtained mixed results by utilizing 235 firms data of eight major industries groups over the period 1971 to 1991. She found that the degree of relationship is not uniform in all the eight industries. The coefficient of correlation varied from -0.002 to -0.48 and average profitability is largely independent of firm size. The inter-firm dispersion of profitability tends to decline with size, although the relationship was not very strong. With regard to incentives to greater industrial concentration, she concluded that profitability did not, on average, provide an incentive for large firms to grow at a relatively high rate. Majumdar (1997) tried to investigate size-profitability relationship in 1020 Indian firms. He found that big firms have a higher profitability compared to small firms. Mistry (2012) ascertained the determinant of profitability in Indian automobile industry and found that Debt-Equity Ratio, Inventory Turnover Ratio and Size (total assets) are the main determinants of profitability. He observed that regression coefficient of size had positive values during most of the years under the study, which suggests that there was a positive relationship between profitability and size. It means that the companies that are big in size have more profitability as compared to the companies which are small in size.

Variable Selection and Model Specification

On the basis of different studies national and international and availability of data as per the requirement of the study, below listed dependent and independent variables have been selected. Most of the studies used the same measures for profitability as well as firm size with little variation. The variables taken by different researchers have been presented below in tabular form.

On the basis of review of above available literature, the variables selected for profitability and size for the present study are given below:

For Profitability: Two different measures have been used, (i) ratio of net profit to total sales turnover and (ii) ratio of net income to net assets plus working capital

For Firm Size: Two different indicators of firm size have been used, (i) total sales turnover and (ii) net assets

Hypotheses: The hypotheses usually used to test relationship among the variables employed in the study. The basic hypotheses on the basis of earlier literature designed are

H1: Pr1 is significantly determined by SIZ1

H1: Pr1 is significantly determined by SIZ2

H1: Pr2 is significantly determined by SIZ1

The basic objective of this study is to check the effect of size on profitability by taking other factors remain constant like diversification, advertising, research and development and merger and acquisition, etc. For this we follow the format of Singh and Whittington (1968), Nagarajan (1988), Kaur (1997) and Dogan (2013). By following earlier studies linear regression model has been employed for the analysis.

Pr1 = α+ SIZ1β+ U……….(1.1)

Pr1 = α + SIZ2β + U………(1.2)

Pr2 = α + SIZ1β + U………(1.3)

Where, Pr1 is the ratio of net profit to total sales turnover

Pr2 is the ratio of net profit to net assets plus working capital

SIZ1 is a measure of firm size represented by total sales turnover

SIZ2 is a measure of firm size represented by net assets

Results and Empirical Analysis

The results obtained are presented in table 4.1, 4.2 and 4.3. Then they are compared on the basis of the p-value and adjusted R2; the model showing the lowest p-value and highest adjusted R2 is taken as the best fit. Generally, p-value is used to test the significance of hypothesis that is made about a population.

Note: ***significant at p= 0.001level; **significant at p= 0.01 level; *significant at p=0.05 level; and .Significant at p=0.10 level; Parenthesis indicates t-values; NS- Not Significant

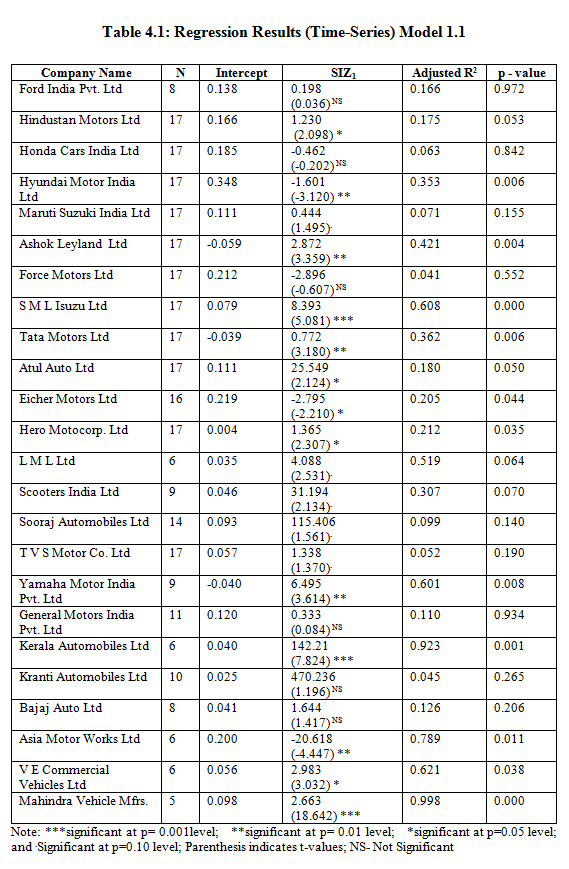

The table 4.1 presents the result of model 1.1, where out of twenty four firms; seven firms are showing non-significant results. It means that these seven firms are not able to reject the null hypothesis i.e. profitability is not determined by firm size. Thus, these firms support the results of Simon (1962) and Whittington (1980). This results cause a vague understanding of the affect of firm size on profitability. Besides these results, five firms namely Hyundai Motor India Ltd, Force Motors Ltd, Eicher Motors Ltd, Honda Cars India Ltd and Asia Motor Works Ltd represented negative relationship between size and profitability and out of five, two firms are statistically significant. On the other hand, three firms (Mahindra Vehicle Mfrs, Kerala Automobiles Ltd and S M L Isuzu Ltd) registered highly significant result and support the earlier studies of Punnose (2008) and Lee (2009). In these three firms more than 90 per cent variations in profitability explained by size.

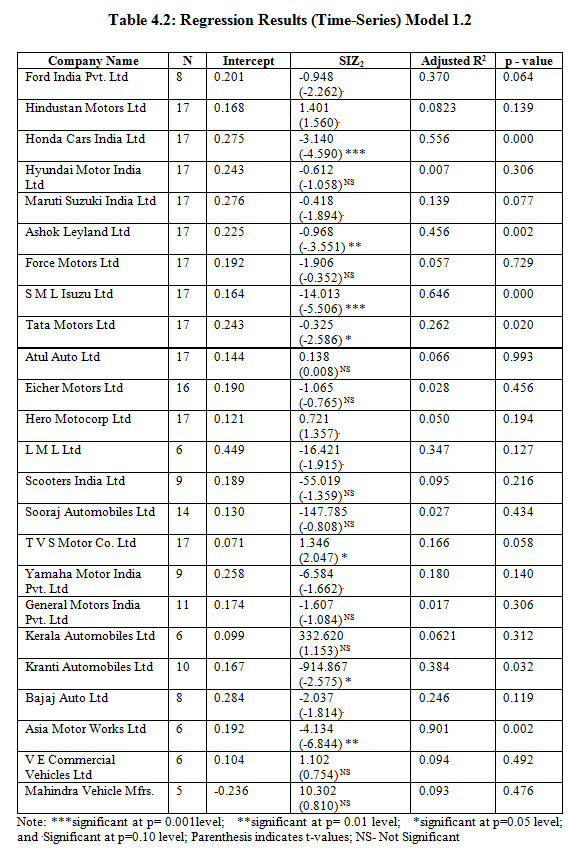

In table 4.2, where total assets have been taken as size variable and ratio of net profit to sales turnover as profitability variable, ten firms showed insignificant relationship between size and profitability variables.

Note: ***significant at p= 0.001level; **significant at p= 0.01 level; *significant at p=0.05 level; and .Significant at p=0.10 level; Parenthesis indicates t-values; NS- Not Significant

The remaining firms also did not indicate highly significant relationship, about seven firms showed significant relationship at 0.10 per cent level. Honda Cars India Ltd and S M L Isuzu Ltd indicated negative but highly significant relationship between size and profitability, where p-value is highly significant at 0.001 per cent level. Most of the firms show negative relationship between size-profitability, which further supports the study of Nagarajan (1988), who employed the total assets and ratio of income to sales turnover in Indian pharmaceutical industry over the period of 1970 to 1983 as measures of size and profitability respectively.

Note: ***significant at p= 0.001level; **significant at p= 0.01 level; *significant at p=0.05 level; and .Significant at p=0.10 level; Parenthesis indicates t-values; NS- Not Significant

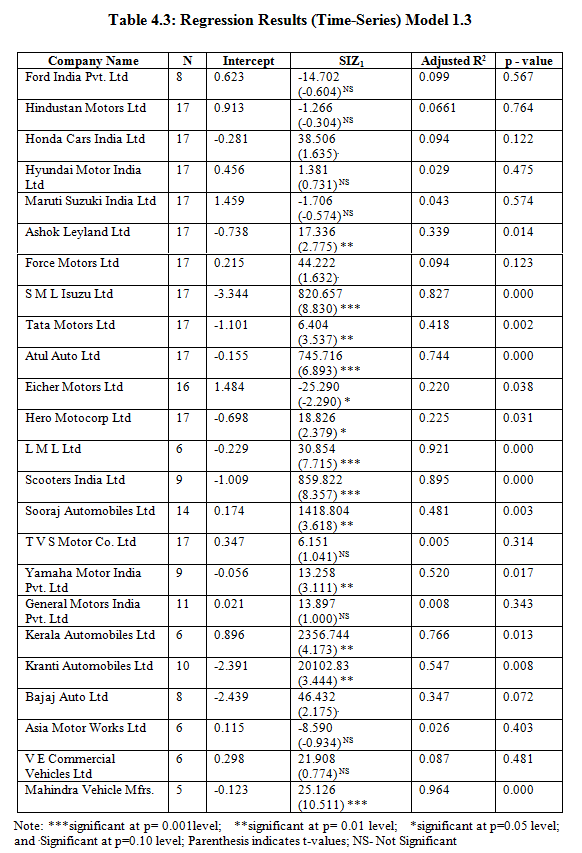

The table 4.3 tests the hypothesis whether firm size (total sales turnover) affected the profitability indicator (ratio of net income to net assets plus working capital). Most of the firms show significant relationship except eight firms (Ford India Pvt. Ltd, Hindustan Motors Ltd, Hyundai Motor India Ltd, Maruti Suzuki India Ltd, T V S Motor Co. Ltd, General Motors India Pvt. Ltd, Asia Motor Works Ltd and V E Commercial Vehicles Ltd) out of twenty four firms and five firms (S M L Isuzu Ltd, Atul Auto Ltd, L M L Ltd, Scooters India Ltd, and Mahindra Vehicle Mfrs) exhibit highly significant Size-Profitability relationship.

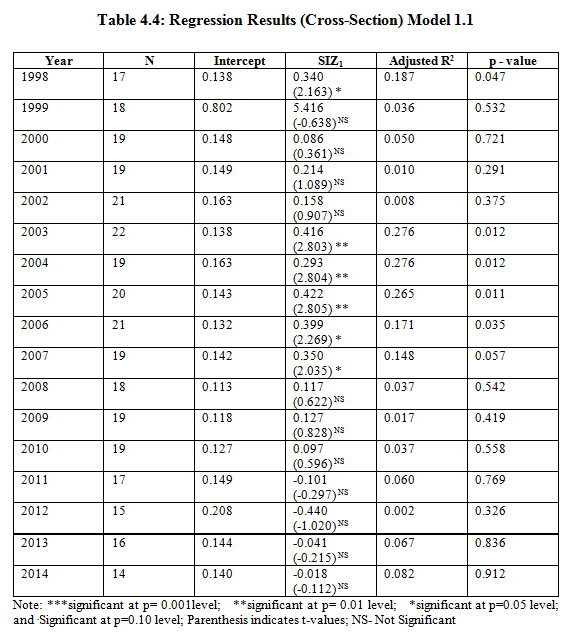

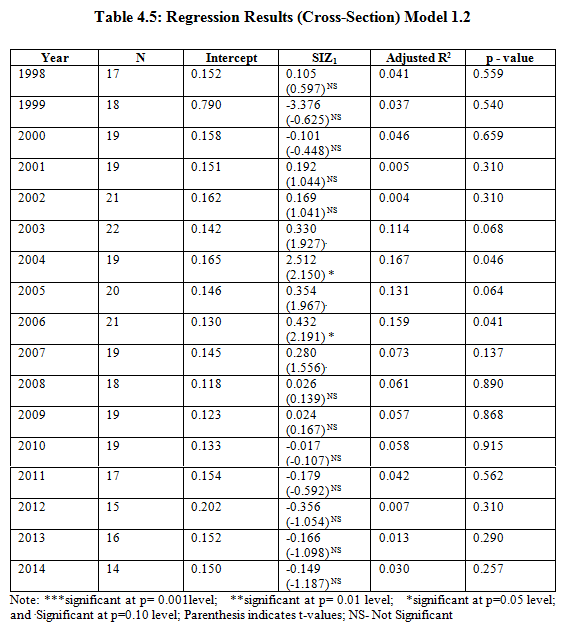

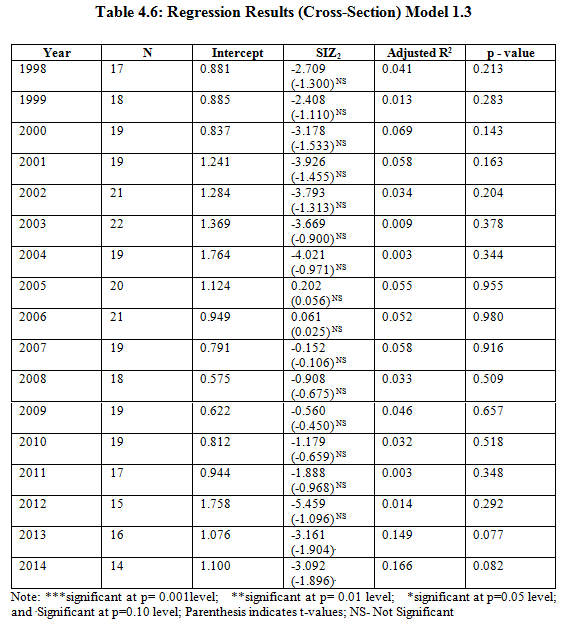

We also further investigated the size-profitability relationship at cross-sectional level over the years 1998 to 2014, using above said regression model. The results of these are given below in table 4.4, 4.5 and 4.6.

Note: ***significant at p= 0.001level; **significant at p= 0.01 level; *significant at p=0.05 level; and .Significant at p=0.10 level; Parenthesis indicates t-values; NS- Not Significant

Note: ***significant at p= 0.001level; **significant at p= 0.01 level; *significant at p=0.05 level; and .Significant at p=0.10 level; Parenthesis indicates t-values; NS- Not Significant

Note: ***significant at p= 0.001level; **significant at p= 0.01 level; *significant at p=0.05 level; and .Significant at p=0.10 level; Parenthesis indicates t-values; NS- Not Significant

It is observed that when size-profitability hypothesis is tested cross-sectionally, the results from 2003 to 2007 turned out to be statistically non-significant in model 1.1(table 4.4) and model 1.2 (table 4.5) and in model 1.3 (table 4.6). So the results indicate no relationship between size- profitability, which support Nagarajan (1988), Simon (1962) and Whittington (1980) studies. Thus cross-sectional regression exhibits low relationship between size-profitability variables.

Conclusion

The Indian automobile industry occupies a prominent place in Indian economy. It passed from different phases, the emergence of indigenous automobile manufactures and self reliance before 1983 to Freedom to Grow after 1991 economic reforms. For considering Structure-Conduct-Performance Paradigm, this study obtained mix results, time-series analysis showed the positive relationship between firm size and their profitability. On the other hand when analyzed cross-sectionally, the results indicate no relationship between firm size (SIZ1 is a measure of firm size presented by total sales turnover and SIZ2 is a measure of firm size presented by net assets) and profitability indicators (Pr1 ratio of net income to total sales turnover and Pr2 is the ratio of net income to net assets plus working capital), which means profitability of any firm is independent of firm size.

References

Amato, L and Wilder R.P (1985), “The Effects of Firm Size on Profit Rates in U. S. Manufacturing”, Southern Economics Journal, Vol. 52(1), pp. 181 – 190

Babalola and Abiodun, Yisau (2013), “The Effect of Firm Size on Firms Profitability in Nigeria”, Journal of Economics and Sustainable Development, Vol. 4, pp. 90-94

Banchuenvijit, W. (2012), “Determinants of Firm Performance of Vietnam Listed Companies”, Academic and Business Research Institute, http://aabri.com/SA12Manuscripts/SA12078.pdf

Becker -Blease, John R., Fred R. Kaen, Ahmad Etebari and Hans Baumann (2010), “Employees, Firm Size and Profitability in U.S. Manufacturing Industries”, Investment Management and Financial Innovations, Vol. 7, pp. 7-23

Dogan, Mesut. (2013), “Does Firm Size affects the Firm Profitability? Evidence from Turkey”, Research Journal of Finance and Accounting, Vol. 4, pp.53-59

Hall, Marshall and Weiss, Leonard. (1967), “Firm Size and Profitability”, Review of Economics and Statistics, Vol. 49, pp. 319-331

John , Akinyomi Oladele and Adebayo, Olagunju. (2013), “Effect of Firm Size on Profitability: Evidence from Nigerian Manufacturing Sector”, Prime Journal of Business Administration and Management (BAM) , Vol. 3(9), pp. 1171-1175

Jonsson, B. (2007), “Does the Size matter? The relationship between Size and Profitability of Icelandic Firms”, Bifrost Journal of Social Sciences, Vol.1, pp. 43-55

Kamerschen, D.R. (1968), “The Influence of Ownership and Control on Profit Rates”, American Economic Review, vol.58, pp.432-447

Kaur, K. (1997), “Size, Growth and Profitability of Firm”, Gyan Publishing House, New Delhi, ISBN: 8121205573

Kouser, Rehana, Tahira Bano, Muhammad Azeem and Masood-ul-Hassan (2012), “Inter-Relationship between Profitability, Growth and Size: A Case of Non-Financial Companies from Pakistan”, Pakistan. Journal of Commerce and Social Science, Vol. 6, pp. 405-419

Lee, J. (2009), “Does Size Matter in Firm Performance? Evidence from US Public Firms”, International Journal of the Economics of Business, Vol.16, pp. 189-203

Majmumdar, S.K (1997), “The Impact of size and age in firm-level performance: Some Evidence from India”, Review of Industrial Organization, Vol.12, pp. 231-241

Mistry, Dharmendra S. (2012), “Determinants of Profitability in Indian Automotive Industry”, Tecnia Journal of Management Studies, Vol. 7, pp. 20-23

Nagarajan, Mohan (1988), “Some Determinants of Profitability: A Study in the Structure-Conduct-Performance Framework of the Indian pharmaceutical Industry”, Unpublished Ph.D Thesis, Indian Institute of Technology- Kanpur

Simon, L. J. (1962), “Size, Strength and Profit”, Proceedings of the Casualty Actuarial Society– Arlington, Virginia, Vol. XLIX, pp. 41-48

Singh, A and Whittington, G. (1968), “Growth, Profitability and Valuation: A Study of United Kingdom Quoted Companies”, Cambridge University Press, Cambridge.

Sivathaasan, N., R. Tharanika, M. Sinthuja and V. Hanitha (2013), “Factors determining Profitability: A Study of Selected Manufacturing Companies listed on Colombo Stock Exchange in Sri Lanka”, European Journal of Business and Management, Vol. 5, pp. 99-107

Whittington, G. (1980), “The Profitability and Size of United Kingdom Companies”, The Journal of Industrial Economics, Vol. 28, pp. 335-352

Zubairi, H. Jamal (2009), “Impact of Working Capital Management and Capital Structure on Profitability of Automobile Firms in Pakistan”, Institute of Business Management (IoBM), Karachi, Pakistan, online available at http://ssrn.com/abstract=1663354

Niresh, J. Aloy and Velnampy, T. (2014), “Firm Size and Profitability: A Stud y of Listed Manufacturing Firms in Sri Lanka”, International Journal of Business and Management, Vol. 9, pp.57-64

Punnose, E.M. (2008), “A Profitability Analysis of Business Group Firms vs Individual Firms in the Indian Electrical Machine Manufacturing Industry”, The ICFAI Journal of Management Research, Vol. 7, pp.52-76