Efficiency

and Volatility of Foreign Exchange Market: Evidence from select exchange Rates

|

Gnyana Ranjan Bal

Assistant Professor

Department of Commerce

Guru Ghasidas Vishwavidyalaya

Bilaspur, Chhattisgarh-495009

Contact No.- +91-8109875791

Email: gnyana.friend@gmail.com

|

Dr. Budheshwar Prasad Singhraul

Assistant Professor

Department of Commerce

Guru Ghasidas Vishwavidyalaya, Bilaspur, C.G.

|

Abstract

The study attempts to test the random

walk behaviour and weak form efficiency of foreign exchange market. For this

purpose two exchange rates namely USD and YEN has been selected from April 2007

to Mar 2015. We have applied the Unit root and Variance ratio test to study the

random walk hypothesis. The findings shows the both the exchange rates do not exhibit

the random walk. Thus implies weak form of market inefficient. Further to analyze

the volatility clustering and persistence we have employed GARCH (1, 1). The results

show there is evidence of volatility clustering and persistence in case of both

the exchange rates. This type of study is highly relevant, as the healthy

functioning of foreign exchange market can lead to high economic growth.

Keywords:

Efficient Market Hypothesis, Volatility, Foreign Exchange Market, GARCH (1,1)

Introduction

In the past few decades the area of

market efficiency has received a significant attention of the both researchers

and academicians all over the world. Generally as per efficient market hypothesis,

the past informationcannot be utilized to predict the future returns in an

efficient market. In other words the past information are already been

reflected in present prices. The efficient market hypothesis can be three

typessuch as weak form of efficiency, Semi-strong and strong form of market

efficiency (Fama, 1970). Weak form of efficiency means the past prices related

information is useless i.e. the current price reflectsthe entire past price

information. In semi-strong form of efficiency the present price reflects all

past price related information as well as publically available information. The

strong form of market efficiency means the current prices reflect all the

public as well as non public information. In other word all the information are

useless even if the insider trading information. So nobody can make excess or

speculative profit in long run.

However,

the past studies have given mixed evidence in the context of market efficiency

in both stock and foreign exchange market. Like Barnes (1986) has shown

evidence of weak form of market efficiency in case of Kuala Lumpur stock

exchange. In another study Sharma and Seth (2011) haveanalyzed the impact of

global financial crisis on market efficiency. The study has taken both NSE and

BSE in two sub-periods (Pre and Post crisis). They did not find evidence of

weak form efficiency of Indian stock market. Also the study concluded that the results

are similar in both the period,so there is no impact of financial crisis on

market efficiency. Arora(2013) has tested the weak form of market efficiency

and random walk of Indian stock market. By taking the Nifty returns the study

conclude that Indian market rejects the weak form of market efficient

hypothesis.Chen (2008) has applied variance ratio test to study the random walk

hypothesis of Euro exchange rate. By taking the sample from January 1998 to

July 2008 the study conclude that Random walk cannot be rejected, thus the euro

exchange rate shows weak form of efficiency. Li and Liu (2012) have studied the

random walk in case of 34 MSCI country index. The study concluded that majority

of country are in weak form of efficient.

Charles and Darne(2009) studied the random walk behavior of major Euro

exchange rate. By applying Variance ratio test the study conclude that exchange

rates for major trading countries (such as Australia, Canada,Korea, Japan,New

Zealand, UK,USA, and Switzerland) follow a random walk hypothesis in case both

daily and weekly frequency data. But their findings are different for non major

trading currencies especially for Swedish Kroner. In overall among similar

studies in Indian market Rao and Shankaraiah (2003), Samanta (2004) and Sharma

andMahendru (2009) have supported weak form of efficiency. While the studies

like Guptaand Basu (2007),Choudhari (1991), Sharma and Seth (2011) and Arora

(2013) have rejected the random walk of market.

The

past literature shows that many of the studies have focused on the efficiency

of stock market, while very few studies have been made on foreign exchange

market. The present study attempts to test the random walk hypothesis and weak

form efficiency of foreign exchange market. We have selected two exchange rates

such as USD a nd YEN to study the random walk behavior of

foreign exchange market. In addition to this the study also analyses the

volatility clustering and persistence of the foreign exchange market.

Data

and Methodology

Two exchange rates namely USD and YEN has been taken for the

purpose of analysis. The study period ranges from April, 2007 to March, 2015.

The common samples in case of all the exchange rates have been selected to make

it standardized. The returns in case of both the exchange rates i.e. USDR and

YENR have been calculated as Ln (Pt/Pt-1),

here Pt price at t period and Pt-1 price at t-1

period and Ln natural log. The methodology of the study can explained as

follows.

1. Unit

root Test

The stationarity is one of the

underlying tests to study the random walk hypothesis. Stationarity of the data

means the mean and variance are constant over the period of time; that means

they are time invariant. In case of non-stationary the series will have time

varying mean and variance. This non-stationarity can be referred as unit root

problem. The random walk of exchange rates can be written as follows:

(1)

Here is exchange rate at t period, and exchange

rates at t-1 period, is a white noise error term. We know that a

series will be said to be random walk if value at t period is equal to its

value at t-1 period plus a random shock. In the equation (1), if ρ is significantly equal to 1,

then the stochastic variable is said to be having unit root.

In other case if then series can be said as stationary and does not follow a random

walk. The Unit root has been tested in the basis of Augmented Dickey Fuller

(ADF) and Phillips-Perron (PP).The ADF test consists of the following

regression:

Here

is pure white noise error term and, in ADF we test whether. Similariliy in Phillips-Perron use non-parametric statistical methods

to take care the serial correlations in the error terms without adding lagged

difference terms.

2. Variance

Ratio Test

The

variance ratio test of Lo and MacKinlay (1988) is based on the fact that if a

series follows a random walk in a finite sample then the variance increment is

linear in its data interval. The stochastic process with drift can be as

follows:

EXt=μ+EXt-1+εt

, (3)

Here is the drift

parameter, and expected value of error is zero. The restrictions in this imply,

error will grow linearly with time. The Variance Ratio VR (q) can be defined as:

VR (q) = (4)

Where is times the variance of - and is the variance of

The null hypothesis is that a time series or its first

difference follows a martingale difference sequence.

3. Volatility clustering and Spillover

We uses the ARCH

family models ARCH (Engel, 1982) and GARCH of Bollerslev (1986) to study the

volatility clustering and persistence. In the context of volatility standard

deviation is one of traditional crude measure of variance to assess

unconditional variance. While the GARCH is estimated to measure conditional

variance. The equation of GARCH model will be as follows assuming Exchange rate

can be represented by AR(1) process.

, (5)

In above equation (5) is the intercept, exchange rate respectively in t-1 period.

Similarly is the white noise error term of exchange

rate.

Results and Discussion

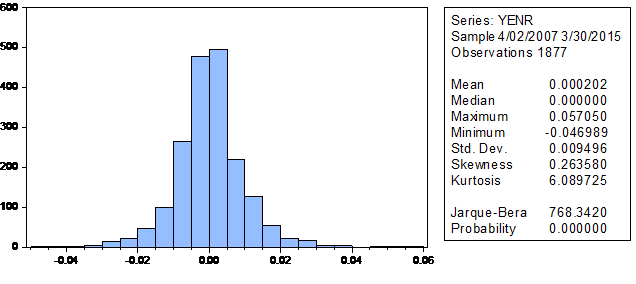

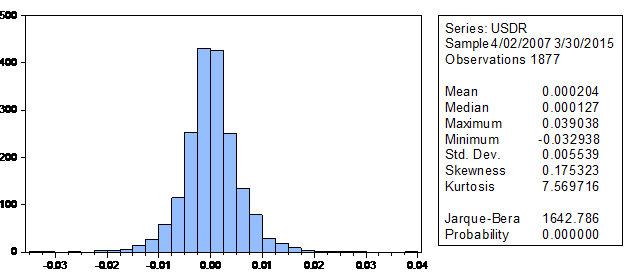

The figure-1 and figure-2 shows the

descriptive statistics of USDR and YENR respectively. We can see that the mean

of USDR is 0.000204 and Median is 0.000127. While the mean of YENR is 0.000202,

so it means the average return of USDR is more as compared to YENR. The

standard deviation of USDR is 0.005539 and YENR is 0.009496. The standard

deviation of YENR is greater than as of USDR, it indicates the YENR is more

volatile as compared to USDR. Both the USDR and YENR are positively skewed in

the sample period. Further to study the normalityJarque-bera has been tested.

In case both the exchange rates the Prob. is 0.0000 i.e. significant at 1%

level. So the null hypothesis of normality has been rejected, that is data are

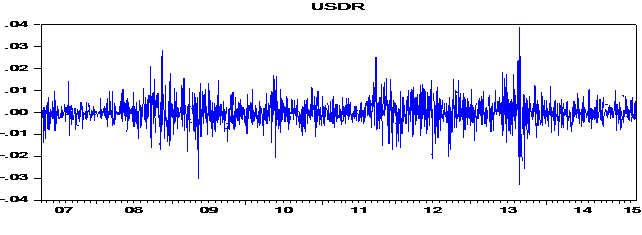

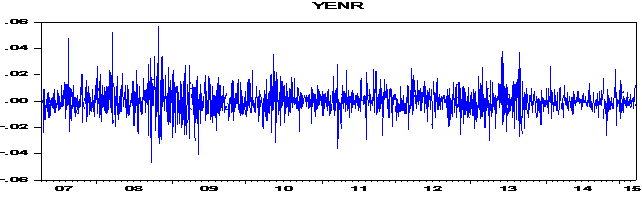

highly non-normal. Figure 3 and 4 shows the plot of return both the exchange

rates namely USDR and YENR. It can be observed that these exchange rates exhibit

some sort of volatility clustering.

Figure-1 Histogram and Descriptive

Statistics of USDR

Figure-2 Histogram and Descriptive

Statistics of YENR/b<>

Figure 3: Plot of USDR

Figure 4:

Plot of YENR

1.

ADF and PP test:

To test the stationarity of data, unit root test has been

applied in basis of ADF and PP. As already been discussed stationarity means

the series does not contain unit root. The table 1 shows the results of Unit

root test on basis of ADF. The results shows that t-statistics is more than the

critical value. It indicates statistically significant, so the null hypothesisof

non-stationarity has been rejected. The USDR does not follow a random walk. The

result is similar in case of YENR, where also the null hypothesis has been

rejected. So YENR is stationary at level. Further the stationary has been

checked on the basis of PP. The does not vary as compared to ADF (see Table 2).

Both the USDR and YENR are stationary at level as the null hypothesis of

non-stationarity has been rejected. Thus the random walk hypothesis has been

rejected in case of both the exchange rates. This implies weak form inefficient

of these exchange rates.

Table

1: Augmented Dickey Fuller test

|

Variable

|

t –Statistics

|

Prob.

|

|

USDR

|

-31.61995***

|

0.0000

|

|

YENR

|

-42.31176***

|

0.0000

|

***indicates

significant @1% level

Table

2: Phillips-Perron Test

|

Variable

|

Adj.

t-statistics

|

Prob.

|

|

USDR

|

-40.78202***

|

0.0000

|

|

YENR

|

-42.30943***

|

0.0000

|

***indicates

significant @1% level

2.

Variance

Ratio Test

Further to verify the random walk hypothesis the

conventional variance test (Lo-Mackinlay, 1988) and the sign and rank test

(Wright, 2000) have been applied. The results of USDR have shown in table 3. We

can see that the all the variance ratios at different horizon of period are

statistically significant. Thus the null hypothesis has been rejected. It shows

USDR exhibitnon-random walk. Thus USDR is weak form of inefficient, as earlier

been observed in Unit root test.

Table 3 Variance

Ratio of USDR

|

Variance Ratio of USDR

|

|

Period

|

Var. Ratio

|

Rank Var. Ratio

|

Sign Var. Ratio

|

|

2

|

0.567421***

|

0.565437 ***

|

0.688699 ***

|

|

4

|

0.248658 ***

|

0.304772 ***

|

0.517591 ***

|

|

8

|

0.135856 ***

|

0.197216 ***

|

0.448294 ***

|

|

16

|

0.068313 ***

|

0.146277 ***

|

0.411381 ***

|

***indicates

significant @1% level

The results of YENR have shown in table 4. We

can see that at different lag all the variance ratios are statistically significant.

Thus the null hypothesis has been rejected. It shows YENR exhibitnon-random

walk. Thus YENR is weak form of inefficient, as earlier been observed in Unit

root test. The similar results have been observed in case of USDR in previous

table.

Table 4 Variance

Ratio of YENR

|

Variance Ratio of YENR

|

|

Period

|

Var. Ratio

|

Rank Var. Ratio

|

Sign Var. Ratio

|

|

2

|

0.524906 ***

|

0.576886 ***

|

0.703625 ***

|

|

4

|

0.250479 ***

|

0.312084 ***

|

0.529318 ***

|

|

8

|

0.129252 ***

|

0.185763 ***

|

0.453891 ***

|

|

16

|

0.066379 ***

|

0.141602 ***

|

0.418577 ***

|

***indicates

significant @1% level

3.

Volatility Clustering and Persistence

Further our study

applies the GARCH (1, 1) model to study the volatility of two exchange rates.

The results are presented in the following table 5 and 6 for both USDR and YENR

respectively. The results in table 5 signifythe coefficients of lagged squared

residuals and conditional variances are statistically significant. And also the

aggregate of this two is near to 1, so there is presence of both volatility

clustering and persistence in USDR. The GARCH (1, 1) results of YENR are

presented in table 6. The similar results also observed in case of YENR. The

aggregate of lagged squared residuals and conditional variances are near to 1

and both are statistically significant. So there is a presence of volatility

persistence.

Table

5: GARCH(1, 1) of USDR

|

GARCH of USDR

|

|

Parameters

|

Coefficient

|

Z-stat

|

P-Value

|

|

|

7.53

|

0.685428

|

0.4931

|

|

|

6.00

|

5.491459

|

0.0000

|

|

|

0.10123

|

9.658968

|

0.0000

|

|

|

0.881305

|

79.15431

|

0.0000

|

Table

6: GARCH (1, 1) of YENR

|

GARCH of YENR

|

|

Parameters

|

Coefficient

|

Z-stat

|

P-Value

|

|

|

-0.00013

|

-0.69389

|

0.4878

|

|

|

3.40

|

5.059509

|

0.0000

|

|

|

0.109688

|

8.689931

|

0.0000

|

|

|

0.853594

|

49.16145

|

0.0000

|

Conclusion

The studies in the context of weak form

of market are highly relevant with regards to usefulness of the past

information that is typically used in technical analysis, speculation and

arbitrage phenomenon. Also from the regulatory point of view this type of study

has significant implications, as the market inefficiency ensures the efficient

and optimal allocation of capital, savings and investment of the economy. This

is highly essential for a healthy economy growth.Our study concludes that the

foreign exchange market does not exhibit a random walk, so weak form of market inefficient.

So the usefulness of past information cannot be completely rejected. As in

inefficient market the future price can be predicted, one can earn abnormal

returns. This type of inefficiency may attract the investors in short run

because of excess return but in long run disturb the pricing phenomenon. As the

current price may not reflect all the past information’s, and lead to over and

under valuation.

References

Armeanu, D. S., & CioacĂ, S.

(2014). Testing the Efficient Market Hypothesis on the Romanian Capital Market.

Proceedings of The 8th International Management Conference “Management

Challenges For Sustainable Development”, November 6th -7th , 2014, Bucharest,

Romania Testing.

Arora, H. (2013). Testing Weak Form of Efficiency of Indian Stock Market. Pacific

Business Review International, 5(12), 16–23.

Barnes, P. (1986). Thin

Trading and Stock Market Efficiency: Case Study of the Kuala Lumpur Stock

Exchange. Journal of Business Finance & Accounting, 13(4), 609-617.

Bollerslev,

T. (1986).Generalized Autoregressive Conditional Heteroskedasticity, Journal of Econometrics, 31,307--327.

Brooks,

Chris(2008). .Introductory

Econometrics for Finance. Cambridge university press.

Charles, A., & Darné, O. (2009). Testing For Random Walk Behavior In

Euro Exchange Rates. Économie Internationale, 119, 25–45.

Chen, J. (2008). Variance Ratio Tests Of Random Walk Hypothesis Of The

Euro Exchange Rate. International Business & Economic Research Journal,

7(12), 97–106.

Chinhamu,

K., & Chikobvu, D. (2014). A Garch Model Test of the Random Walk

Hypothesis: Empirical Evidence from the Platinum Market. MJSS. http://dx.doi.org/10.5901/mjss.2014.v5n14p77.

Choudhari, S.K. (1991). Short Run Price Behaviour:

New Evidence on Weak Form of Market Efficiency. Vikalpa, 16(4), 17-21.

Dickey,

D. A.; Fuller, W. A. (1979). Distribution of the Estimators for Autoregressive

Time Series with a Unit Root. Journal

of the American Statistical Association, 74 (366):

427–431.doi:10.2307/2286348. JSTOR 2286348.

Enders, W. (2008). Applied

Econometric Time Series. Wiley, New Delhi.

Engel RF (1982).

Auto regressive conditional heteroskedasticityand estimates of the variance of

UK inflation. Econometrica50(4):987–1008.

Fama, E. (1965), Random Walks in Stock Market Prices, Financial Analyst Journal, 21(5), 55-59.

Fama,

E. (1970), Efficient Capital Markets:

A Review of Theory and Empirical Work, Journal of Finance, 25(2), 383-417.

Fama, E. (1991), Efficient Market Hypothesis: II, Journal of Finance, 46(5), 1515-1617.

Gupta, R. and Basu, P.K. (2007). Weak Form

Efficiency in Indian Stock Markets. International Business &

EconomicsResearch Journal, 6(3), 57-64.

Harrison, B. (2007). Do fat tails matter in GARCH estimation: testing

market efficiency in two transition economies. Economic Issues, 12(Part-2),

15–27. Retrieved from http://www.economicissues.org.uk/Files/207Harrison.pdf

Jain, Kapil and Jain, P. (2013). Empirical Study of the Weak Form of EMH

on Indian Stock Market. International Journal of Management and Social

Science Research, 2(11), 52–59.

Li, B., & Liu, B. (2012). A Variance-Ratio Test of Random Walk in

International Stock Markets. The Empirical Economic Letters, 11(8).

Lo, A.W. and Mackinlay, A.C. (1988). Stock Market

Prices Do Not Follow Random Walks: Evidence from a Simple Specification Test. Review

of Financial Studies, 1(1), 41-66.

Nisar, S. & Hanif, M. (2012). Testing Weak Form

of Efficient Market hypothesis: Empirical Evidence from South Asia. World

Applied Science Journal, 17 (4), 414-427.

Phillips,

P. C. B.; Perron, P. (1988). Testing for a Unit Root in Time Series

Regression. Biometrika, 75 (2):

335–346. doi:10.1093/biomet/75.2.335.

Rao, D.N. and Shankaraiah, K. (2003). Stock Market

Efficiency and Strategies for Developing GCC Financial Markets: A Case Study of

the Bahrain Stock Market. The Arab Bank Review, 5(2), 16-21.

Samanta, G.P. (2004). Evolving Weak-Form

Informational Efficiency of Indian Stock Market, Journal of Quantitative

Economics, 2(1), 66-75.

Sekar, P. C., & Arasu, B. S. (2007). Indian stock market efficiency

before and after the introduction of derivatives, Journal of Contemporary Research in Management(1), 139–154.

Sharma A.K. and Seth N.

(2011), Recent Financial Crisis and Market Efficiency: An Empirical Analysis of

Indian Stock Market, Indore Management

Journal, 2 (4), 27-39.

Sharma, G.D. and Mahendru, M. (2009). Efficiency

Hypothesis of the Stock Markets: A Case of Indian Securities. International

Journal of Business and Management, 4(3), 136-144.

Singh, B.-P., & Kumar, B. (2007). Variance Ratio Tests of the Random

Walk Hypothesis for Indian Stock Index Futures : Evidence from High

Frequency Data, (2002), 3–7. Retrieved from www.nseindia.com/content/press/NS_may2009_1.pdf.

Tiwari, A. K., & Mutascu, M. (2011). Economic Growth and FDI in Asia:

A Panel-Data Approach. Economic Analysis and Policy, 41(2), 173–187.

http://doi.org/10.1016/S0313-5926(11)50018-9.

Wright, J. H., 2000.Alternative

Variance-Ratio Tests Using Ranks and Signs, Journal

of Business and Economic Statistics, 18, 1-9.