Measuring the Effects of Monetary Shocks on Superior

Industries Index in Capital Market of Iran

|

Zarifeh Jalili

Phd Student of Economics

Tarbiat Modares University

Tehran, Iran

|

Abbas Assari Arani

Assistant Professor of Economics

Tarbiat Modares University

Tehran, Iran

Email: Assari_a@modares.ac.ir

|

Kazem Yavari

Associate Professor of Economics

Tarbiat Modares University

Tehran, Iran

|

Hassan Heydari

Associate Professor of Economics

Tarbiat Modares University

Tehran, Iran

|

Abstract

The main purpose

of this study is analyzing the effect of monetary policies on stock exchange on

selected Top 10 Industries in Iran by using Structural Vector Auto Regressive

(SVAR) method and monthly data of 2005-2012. Obtained results using SVAR method

show that monetary policy has significant effect on

indices of Top 10 industries in the stock market. Moreover, monetary shocks

impulse respond function and the impact on index of top industries in stock

market are investigated. Obtained results show that monetary shocks have

different impacts on different industries. In general, obtained results show

that stock market can be considered as one asset market as a channel to

transfer effects of monetary policy.

Key

words: stock market, monetary policy, liquidity, interest

rate, loans, structural vector auto regressive (SVAR)

Introduction

Development of

capital market and banking system through increase in productive investment

opportunities, reduce transaction costs, reduce risks, mobilize savings,

increase transparency and facilitate the optimal allocation of resources can

lead to boom in production and economic growth. The interdependency between

asset price and monetary policy is one of the main issues of financial

economics, which has been especially considered after 2008, last financial

crisis of the world. Wide range studies are being conducted in field of

relationship between behavior of advanced stock market elements and monetary

policies, while this issue is remained almost unknown for the emerging markets

(Surial, 2002, p.3). Among different aspects of the interdependence,

effectiveness of monetary policy shocks on stock efficiency has been almost

considered more than other issues in theoretical literature. In Iran, according

to emergent of the capital market and on the other hand, because of bank-based

nature of financing system of majority of industrial groups, it is necessary to

conduct further studies in field of capital market indices, active groups and

especially top industries in this market and effects of monetary variables on

them in capital market of the country. It should be mentioned that

effectiveness of monetary policies and especially liquidity impulses on real

part of economics including investment, consumption and production are the most

important issues in field of implementing monetary policies and the active and

top industries in stock exchange can be the key and important axes in this

field. This effect could be created through a process that is called as the

transmission mechanism of monetary policy. In general, transmission mechanism

of monetary policy could be classified to 4 main classes including interest

rate channel, exchange rate channel, asset price channel and the credit

channel. Among the monetary policy transmission channels, asset price channel

plays key role. Effects of monetary policy on asset price could be transferred

through asset price channel and change in these prices to the economics

(Meshkin, 1996, p.7).

Theoretical framework

Over the years

and after emergence of financial crisis, effects of monetary policies on

financial markets have gained many attentions and its role has become brilliant

as a precondition for efficient markets. During recent financial crisis across

the world, Central banks have used wide range interferences of monetary

policies to create facilities in financial markets (Amador et al, 2013, p.50).

Monetary policy refers to a series of policies that follow macroeconomic goals

through changing interest rate and volume of money. One of the important

discussions in field of implementing monetary policies is its effectiveness.

Monetary officials should have exact evaluation of scheduling and effect of

monetary policies on the economics to be successful in this important field.

Therefore, it is necessary for them to identify mechanism, based on which

monetary policy affects economics and macroeconomic variables (Meshkin, 1996,

p.1). In this field, the most important affecting channels of monetary policy

and transferring its impacts are investigated. The channels are as follows:

1. Interest rate channel

Interest rate channel is the standard

direction of transferring monetary policy in view of Keynesians, so that

reduction of real interest rate can reduce capital cost and can increase also

investment expenses. As a result, total demand and input (product) is also

increased. Expansionary monetary policy that reduces short-term nominal

interest rate and increases liquidity in the society can also reduce short-tern

real interest rate and this is true under condition of dominance of rational

expectations. Lower real interest rates can increase capital of firms,

investments of domestic households, consumer durable expenses and capital

stock. All mentioned issues can also increase total output (Poddar, Tushar et al,

2006, pp.4-5).

2. Banks' loan channel

According to bank's loan channel,

restrictive monetary policy (such as increase in legal deposits or purchasing

commercial banks' reserve asset by central bank) can reduce usable deposits of

commercial banks. Moreover, tighter monetary policy can reduce attracting

deposits in commercial banks through affecting economic activities. These

factors can decrease supply of existing loans, especially allocated credit to

small firms. As a result, it can also affect investment activities in opposite

direction (Mukherjee et al, 2011, p.5).

3. Asset price channel

This channel includes 2 channels of

exchange rate and equity price channel:

- Exchange rate channel

Exchange rate channel has weak

cooperation and relationship with other channels. However, placing the exchange

rate besides loaning channel can result in expansion of effect of exchange rate

on the output. Moreover, exchange rate shows response to changes of short-term

rates of government bonds (Ghazanchyan, M, 2014, p.23). However, in countries

with flexible exchange rate, exchange rate channel can be a strong mechanism

for effects of monetary policy. Moreover, exchange rate can show more

transparent sign of monetary conditions in countries that time series

statistics of economics are not available easily (Mohanty, M.S, 2014, p.3).

- Equity price channel

There are two channels that are related

to equity price and are important in the discussion of transmission mechanism

of monetary policy. The two channels include Tobin's q theory in field of

investment and wealth effect on consumption. Tobin's q theory provides such

mechanism to affect monetary policy of economics through affecting corporate

asset value. Tobin defines q as market value of corporates that is distributed

by replacement cost of capital. If q is in high level, market value of

corporates is high compared to replacement cost of capital and the investment

equipment and machineries are also cheaper compared to market value of

commercial firms. As a result, companies can publish stocks and the price

received for it will be higher than machinery and equipment purchased by them.

Therefore, capital expenses would be increased, since companies can purchase

high volume of investment products through publishing small amount of stock.

Literature review

In this section, the relevant studies in

field of effects of monetary policies on stock market are investigated.

Ghosh (2009) has conducted a study in

India on investigating the effects of monetary policy on industries of this country

using VAR method and has found that different industries show different

responses to monetary shocks. Moreover, obtained results from the study showed

that response of industries is mainly related to difference in size of industry

and its intensity in using the capitals.

Amador et al (2013) have used SVAR model

for Euro zone and have conducted a study under the title of can monetary policy

determine liquidity of stocks? Obtained results from the study showed that

Expansionary monetary policy of European Central Bank could increase total

liquidity of stock market in Germany, France and Italy. Moreover, effect of

monetary policy on smaller stock markets has been significantly higher than

others and this refers to nonlinear effect of monetary policy on liquidity of

stock market (Amador, O et al, 2013).

Krainer (2014) has studied monetary

policy and bank credits in Euro Zone and has presented this question that is

there any stock market channel or interest rate channel in this field or not?

This study used non-nested hypothesis test, Test of omitted variables and

Granger causality tests and showed that central bank should try to make

monetary policies to achieve the target of economic stability and crediting by

banks and consider also changed in stock prices (Krainer, Robert E., 2014,

p.284).

Tsai (2014) has investigated effects of

monetary policy on stock returns under limited conditions of financing. The

research period has been 1999-2007. Obtained results showed that under

conditions that comments of Federal Reserve Monetary Committee are announced,

stock returns would significantly show response to sudden shocks of monetary

policy. The response would be in low level, when no announcement is taken

(Tsai, 2014, p.273).

Devtyan, Karen

(2016) has conducted a study under the title of distributive effects of

conventional and unconventional monetary policies using SVAR test and showed

that after financial crisis of 2008, many central banks reduces their policy

rates considerably and used Unconventional instruments of monetary policy.

Particularly, one of the executive samples of unconventional monetary policies

has been purchasing assets by Reserve Federal. The operations changed relative

supply of bonds and other assets and as a result, it could affect their prices

and the cash flow in economic system.

Gueriny, Pierre

and Danilo Leiva-Leonz (2016) have conducted a study under the title of effect

of monetary policy on stock returns in industries in the changing world and

used Factor-Augmented VAR (FAVAR) method to evaluate effects of unexpected

monetary policies on stock returns and showed that there is significant

difference among response of different industries on monetary shocks. Moreover,

the results of this study showed that to help understanding heterogeneity in

response to monetary shocks, industrial interdependence (measured by network

criteria) is important.

Keshavarz Haddad

and Mahdavi (2005) have also conducted a study under the title of "can

stock market in Iran economics be a channel to pass over monetary policy or

not". According to this study, through considering use of direct tools of

monetary policy, there is no indicator variable in economics of Iran to show

changes of monetary policy. Considering the mentioned limitations, the relationship

of conditional volatility, the conditional variance of stock returns and

conditional vitality of monetary variables is emphasized in this study. The

relationship between conditional vitality of variables is also measured using

bivariate vector autoregressive (VAR) method. Obtained results from the study

showed that stock market in Iran's economics is not a channel for monetary

transmission mechanism.

Shahbazi, Rezaei

and Abbasi (2012) have also used empirical evidence of Iran and have

investigated efficiency of stock market based on monetary policies. The desired

data of this study has been related to time period of 1999-2008. Analysis

method used in this study has been Autoregressive Distributed Lags (ARDL)

method. Obtained results from the study showed that current values of money

supply has significant and negative effect on current stock returns and hence,

the hypothesis of efficiency of stock market to monetary policies is confirmed.

Methodology

The general and

common method to explain the relationship between monetary policy (liquidity

impulses) and stock return behavior is to estimate Vector Autoregressive (VAR)

model for different monetary indices and stock return. In VAR models, Cholesky

decomposition is used to achieve impulse response functions. Cholesky

decomposition refers to a causal arrangement. Hence, if the purpose is to

investigate effects of more than one shock, it may be unacceptable. In this

study, to analyze effects of monetary shocks on stock market, SVAR model is

used. The main advantage of SVAR models compared to VAR models, in which

identification of structural impulses are implicitly and based on taste, is

existence of an economic logic based on economic theories to apply limitations.

In this study, to specify the model, SVAR model introduced by Lutkepohl (2005)

is used. Accordingly, effect of variables such as real interest rate (r),

Facilities granted to the private sector (l), real exchange rate (ex) and

liquidity (M2) are investigated using SVAR on efficiency of top 10 industries.

In terms of expansion of the subject and in line with facility of comparative

issues, this study is focused on effects of liquidity and its impulses.

Limitations can be applied in two forms of short-term and long-term. Applying

these limitations can be a basis to identify structural shocks.

In the above matrix, refers to shocks of

real interest rate of deposits in banking system; refers to shocks of granted facilities to the private sector; refers to exchange

rate shocks and refers to monetary

shocks. In this study, effects of these shocks on indices of top industries of

stock exchange are analyzed.

According to the4se shocks, the impulse respond

functions could be obtained and dynamic analysis of economic variables could be

done. In other words, for better analysis of impulses of monetary policy

through liquidity and analysis of short-term shocks and its relationship with

long-term shocks, impulse respond function (IRF) analysis is used.

1. Model estimations and data analysis

Granger causality test

In line with determining endogeneity of variables,

the method selected in this study is Granger Causality Test considered for

variables of indices of top 10 industries, liquidity, nominal exchange rate,

granted facilities to private sector and real interest rate (table 1). The

arrangement of endogeneity of variables based on results of the mentioned test

is as follows:

P… M2 ex

l r

Table

1: results of Granger Causality Test to determine arrangement of variable

endogeniety

|

Pairwise

Granger Causality Tests

|

|

Date:

06/21/15 Time: 15:43

|

|

Sample:

1384M01 1392M12

|

|

Lags:

2

|

|

|

|

Null

Hypothesis:

|

Obs

|

F-Statistic

|

Prob.

|

|

r

does not Granger Cause M2

|

106

|

0.03546

|

0.9652

|

|

M2

does not Granger Cause r

|

0.10554

|

0.8999

|

|

|

|

|

|

|

L

does not Granger Cause M2

|

106

|

22.8857

|

6.E-09

|

|

M2

does not Granger Cause L

|

1.45849

|

0.2374

|

|

|

|

|

|

|

P

does not Granger Cause M2

|

106

|

5.13452

|

0.0075

|

|

M2

does not Granger Cause P

|

2.23036

|

0.1128

|

|

|

|

|

|

|

Ex

does not Granger Cause M2

|

106

|

3.31110

|

0.0405

|

|

M2

does not Granger Cause Ex

|

0.79548

|

0.4542

|

|

|

|

|

|

|

L

does not Granger Cause r

|

106

|

0.30970

|

0.7344

|

|

r

does not Granger Cause L

|

1.20615

|

0.3036

|

|

|

|

|

|

|

P

does not Granger Cause r

|

106

|

0.51454

|

0.5993

|

|

r

does not Granger Cause P

|

1.44762

|

0.2400

|

|

|

|

|

|

|

EX

does not Granger Cause R

|

106

|

8.65182

|

0.0003

|

|

R

does not Granger Cause EX

|

3.05201

|

0.0516

|

|

|

|

|

|

|

P

does not Granger Cause L

|

106

|

3.99420

|

0.0214

|

|

L

does not Granger Cause P

|

8.11249

|

0.0005

|

|

|

|

|

|

|

EX

does not Granger Cause L

|

106

|

0.79470

|

0.4545

|

|

L

does not Granger Cause EX

|

1.79528

|

0.1713

|

|

|

|

|

|

|

EX

does not Granger Cause P

|

106

|

3.76076

|

0.0266

|

|

P

does not Granger Cause EX

|

0.70701

|

0.4955

|

In other words,

index of top 10 industries has had highest endogeniety and after that,

liquidity, nominal exchange rate, facilities granted to private sector and real

interest rate have possessed next places. Accordingly, in different analyses,

the criterion of placement of variables is based on result of Granger causality

test.

2. Variable viability test

To determine

variable viability, generalized Dickey-Fuller test is used. Results of the

tests are presented in table 2. All variables are unviable in their level,

since their probability value is always higher than 0.05 and hence, H0 based on

existence of unit root can't be rejected and as a result, all variables have

unit root. Secondly, first difference of all variables is viable, since their

probability is entirely lower than 0.05 and hence, H0 based on existence of

unit root (unviability) is rejected and as a result, all variables are viable

in first level. Considering obtained results, it could be demonstrated that the

studied variables I (l) are accumulated and they can be estimated and tested in

form of VAR model.

Table 2: results of

generalized Dickey-Fuller test

|

Variable name

|

Critical values in level:

|

t-stat

|

Prob

|

|

10%

|

5%

|

1%

|

|

M2

|

Level

|

-2.58

|

-2.89

|

-3.49

|

-1.32

|

0.62

|

|

First order difference

|

-2.58

|

-2.89

|

-3.49

|

-9.88

|

0.00

|

|

p

…

|

Level

|

-2.58

|

-2.89

|

-3.49

|

1.02

|

0.99

|

|

First order difference

|

-2.58

|

-2.89

|

-3.49

|

-5.92

|

0.00

|

|

ex

|

Level

|

-2.58

|

-2.89

|

-3.49

|

0.32

|

0.98

|

|

First order difference

|

-2.58

|

-2.89

|

-3.49

|

-7.67

|

0.00

|

|

r

|

Level

|

-2.58

|

-2.89

|

-3.49

|

1.27

|

0.99

|

|

First order difference

|

-2.58

|

-2.89

|

-3.49

|

-7.12

|

0.00

|

|

l

|

Level

|

-2.58

|

-2.89

|

-3.49

|

-2.81

|

0.06

|

|

First order difference

|

-2.58

|

-2.89

|

-3.49

|

-10.73

|

0.00

|

Source: research findings using Eviews software

2.1.

Short-term SVAR model

and effects of monetary shocks on top industries index

Determining VAR lag order

To determine lag order in VAR model, different

criteria such as likelihood ratio (LR), final prediction error (FPE), Akaike

information criterion (AIC), Schwartz information criterion (SC) and

Hannan-Quinn information criterion (HQ) are used. In all cases of using the

criteria in this study, Akaike criterion is considered as practical criterion.

Accordingly, existence of a lag in VAR order is proved based on Akaike

criterion, since the highest value of Akaike is equal to 9.62 in terms of

absolute value, which can determine VAR order in level of 1 lag (table 3). This

test is true for top 10 industries.

Table 3: assessing and

determining VAR order

|

Endogenous variables

|

p…M2 ex l r

|

|

Lag

|

LR

|

FPE

|

AIC

|

CS

|

HQ

|

|

0

|

-

|

0.00

|

5.22

|

5.36

|

5.28

|

|

1

|

1448.72

|

-4.81

|

-9.62*

|

-8.45*

|

-8.91*

|

|

2

|

67.18*

|

-5.35*

|

-9.47

|

-8.06

|

-8.89

|

|

3

|

26.34

|

-0.47

|

-9.28

|

-7.24

|

-8.46

|

|

4

|

26.24

|

0.76

|

-9.11

|

-6.43

|

-8.03

|

|

5

|

30.52

|

0.72

|

-9.03

|

-5.70

|

-5.70

|

Source:

research findings using Eviews software

2.2.

SVAR results and

effects of monetary shocks on top industry index

The results related to SVAR model for top 10

industries are presented in table 5 and the summary of the results of presented

in table 4.

Table 4: structural

effects of monetary shocks for top 10 exchange industries

|

Index

|

Coefficient of effects of liquidity shocks

|

Coefficients of effects of exchange rate shocks

|

Coefficients of effects of shocks in granted facilities

to private sector

|

Coefficient of effects of real interest rate shocks in

banking system

|

|

Pbank

|

0.03

|

0.001

|

-0.004

|

0.05

|

|

Pcmn

|

0.51

|

0.21

|

0.02

|

-2.61

|

|

Pcar

|

4.09

|

2.05

|

1.01

|

0.61

|

|

Pmd

|

0.85

|

0.18

|

0.24

|

0.23

|

|

Pchem

|

0.36

|

0.11

|

0.12

|

-0.54

|

|

Pmx

|

0.59

|

1.85

|

0.11

|

-0.29

|

|

Pmetl

|

0.13

|

0.11

|

0.61

|

-2.19

|

|

Pent

|

0.82

|

0.23

|

0.12

|

-5.32

|

|

Poil

|

1.29

|

0.17

|

0.8

|

-3.85

|

|

Pest

|

2.57

|

0.35

|

0.9

|

-6.39

|

Source:

research findings using Eviews software

In table 4, the indices are as follows: Pbank: index

of banks and credit institutes; Pcmn: cement industry index; Pcar: car and

assembly industry index; Pmd: multidisciplinary industry index; Pchem: chemicals

industry index; Pmx: metal excavation industry; Pmetl: fundamental metals

industry index; Pent: enterprise index; Poil: oil product and nuclear fuel

industry index; Pest: real estate and mass building industry index.

Table 5: results of

SVAR test

1) Pbank =0.03 M2(-1) +0.001EX

(-1)–0.004L (-1)+0.05 R (-1)

2) Pcmn =0.51M2(-1)+0.21EX

(-1)+0.02L(-1)-2.61 R (-1)

3) Pcar =4.09M2(-1)+2.05EX (-1)+1.01L(-1)-0.61 R (-1)

4) Pmd =0.85M2(-1)+0.18EX (-1)+0.24L(-1)-0.23 R (-1)

5) Pchem =0.36M2(-1)+0.11EX (-1)+0.12L(-1)-0.54R (-1)

6) Pmx =0.59M2(-1)+1.85EX(-1)+0.11L(-1)-0.29R(-1)

7) Pmetl =0.13M2(-1)+0.11EX(-1)+0.61L(-1)-2.19R(-1)

8) Pent =0.82M2(-1)+0.23EX (-1)+0.12L(-1)-5.32R (-1)

9) Poil =1.29M2(-1)+0.17EX

(-1)+0.80L(-1)-3.85R (-1)

10) Pest =2.57M2(-1)+0.35EX(-1)+0.91L(-1)-6.39R (-1)

|

According to

table 4:

-

In short-term,

expansionary policy can affect index of top 10 industries positively through

increasing liquidity (Reduction of legal reserves, injection of high-powered

money, reduce the penalty rate of the Central Bank and reduced the documents

discount rate by the Central Bank). Hence, Expansionary monetary policy

(restrictive) can have positive (negative) effect on index of top 10 industries

in terms of liquidity directly and in short-term.

-

Expansionary monetary

policy (restrictive) in field of facilities granted by banks can empower

(weaken) liquidity volume and can have positive (negative) effect in short-term

and indirectly on indices of cement, Lime & Plaster, car, multidisciplinary

industries, chemical industries, metal extraction, fundamental metals,

enterprises, oil products and nuclear fuel and mass building and can also

empower direct effect. However, in regard with exchange index of banks and

credit institutes, this effect is negative and neutralizes direct effect and

the overall effect of outcome of the two effects is not clear and is depended

on volume and amount of monetary shocks and granted facilities to private

sector (according to results of table 5).

-

In short-term,

liquidity, exchange nominal rate and facilities granted to private sector can

have positive effect on mass building and real estate and real interest rate

can have negative effect on the said index. Hence, as coefficient of real

interest rate is higher than total coefficient of other variables, it seems

that expansionary monetary policy (restrictive) can have positive (negative)

effect on mass building and real estate index in short-term.

-

In short-term, exchange

rates shocks can have negative effects on monetary policy; it means that shocks

resulted from exchange rate impulses can lead to turbulence of monetary policy

in short-term and such turbulence of monetary policy can lead to higher

turbulence in most studied exchange indices through restriction of liquidity.

-

In general, liquidity

and facilities granted to private sector can have positive effect on total

exchange index and also, exchange rate and real interest rate can have negative

effect on the said index.

-

In short-term,

liquidity, exchange rate and real interest rate and facilities granted by banks

can have positive effect on index of banks and credit institute group in

exchange.

-

Liquidity, nominal

exchange rate and facilities granted to private sector can have positive effect

on car industry and assembly index, cement, lime and plaster industry,

multidisciplinary industries, chemicals, enterprises, metal extraction, oil

products and nuclear fuel and real estate in short term. Also, real interest

rate of deposits has negative effect on the mentioned indices.

-

In field of facilities

granted by banks, expansionary monetary policy (restrictive) can empower

(weaken) volume of money and through this, it can have positive (negative)

effect on all exchange indices in short-term.

-

In short-term, monetary

policy shocks in regard with interest rate in case of expansionary policy

(increase in interest rate), it can enhance liquidity status (increase in bank

deposits) and as a result, it can improve all studied indices in stock

exchange.

As a result, expansionary monetary

policy resulted from increase in facilities granted to private sector can

empower exchange rate in short-term and through this, it can have positive but

small effect on bank and credit institute group index in stock exchange.

Restrictive monetary policy can worsen

status of granted facilities to private sector through increasing real interest

rate and through this; it can result in a little improvement in index of bank

and credit institute group in stock exchange. This shows that banks are not

significantly dependent on Revenues from credit facilities.

Testing normality of distribution of

residuals of SVAR model

Relevant results of normality of

distribution of residuals of SVAR model for top 10 industries in stock market

could be interpreted as follows:

a) As

probability of chi-square distribution in level of model residuals is more than

0.05, H0 based on no skew in distribution of residuals is related to SVAR model

of top 10 industries and distribution of the mentioned residuals has no

skewness.

b) As

probability of chi-square distribution among 5 variables is higher than 0.05,

H0 based on lack of skewness among residuals of vectors studied variables is

confirmed and hence, the relevant patterns of top 10 indices have not abnormal

skewness.

c) Total

distribution of the test based on Jarque-Bera criterion shows that probability

related to this distribution among 5 variables is higher than 0.05 and hence,

the H0 based on multivariate normal distribution of SVAR model for top 10 industries is confirmed. Hence,

the entire model is distributed normally.

2.3. Testing

lack of inequality of variances among residuals of variables

Obtained results from the Wite Test in

regard with inequality of variables of SVAR model for top 10 industries show

that (table 6):

a) Probability

of distribution of chi-square test with df of 300 is over 0.05 and hence, H0

based on no inequality among residuals of studied patterns is confirmed.

b) Although

there is inequality of variances among some residuals of variables, their

vector combination has no inequality of variance based on the results in

paragraph (a).

Table 6: results of total

correlation of inequality of variances

|

H0: lack of

cross terms

|

|

Df

|

Chi-square

(X2)

|

Prob

|

|

300

|

434.68

|

0.1125

|

Source: research findings using Eviews

software

2.4.

Variance decomposition

(VD) of SVAR model for indices of top 10 industries

Obtained results from the test in

variance decomposition section show that facilities granted to private sector

can have highest effect respectively in field of metal extraction, fundamental

metals, entire stock exchange, enterprises and cement. Real interest rate has

also showed highest effect during the study respectively in field of bank

indices, multidisciplinary industries and chemicals. Liquidity has had the

highest effect just in field of oil products index and exchange rate has had

the highest effect in field of car industry. Hence, the changes in facilities

granted to private sector and real interest rate have been the most important

factors affecting top exchange indices (table 7).

Table 7: summary of the results of

variance decomposition of monetary variables in top 10 industries

|

Monetary

variables of stock exchange indices

|

M2

|

L

|

R

|

Ex

|

|

Pbank

|

0.57

|

0.57

|

4.70

|

0.64

|

|

Pcmn

|

0.13

|

1.77

|

0.59

|

1.17

|

|

Pcar

|

0.10

|

1.45

|

0.11

|

3.93

|

|

Pmd

|

0.04

|

1.02

|

2.45

|

2.18

|

|

Pchem

|

0.04

|

1.02

|

2.44

|

2.18

|

|

Pmx

|

0.73

|

5.19

|

0.96

|

2.03

|

|

Pmetl

|

0.01

|

3.64

|

3.25

|

2.89

|

|

Pent

|

0.096

|

3.09

|

0.89

|

0.91

|

|

Poil

|

1.77

|

0.21

|

1.39

|

2.91

|

|

Pest

|

0.495

|

3.46

|

1.65

|

0.46

|

Source: calculations of the suthor

derived from Eviews

2.5.

Impulse respond

function analysis of SVAR model for top 10 industries

Impulse respond function (IRF) could be

presented structurally for bank and credit institute group index in stock

exchange according to the results in table 8 (diagrams 1-24):

Table 8: results of IRF test for

top 10 industries to one standard deviation monetary shock

|

Variable

period

|

Banks

|

Car

|

Multidisciplinary

|

Chemicals

|

Metal

extraction

|

Fundamental

metals

|

enterprises

|

Oil

|

Real estate

|

Cement

|

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

|

1

|

Positive and

Explosive

|

Positive

|

Positive

|

Negative and

Explosive

|

Negative and

Explosive

|

Negative and

explosive

|

Negative

|

Negative and

explosive

|

Positive

|

0

|

|

2

|

Negative and

explosive

|

Positive and

reductive

|

Positive and

reductive

|

Negative and

reductive

|

Negative and

reductive

|

Negative and

reductive

|

Negative and

reductive

|

Negative and

reductive

|

Negative and

explosive

|

Negative

|

|

3

|

Positive and

reductive

|

Constant

|

0

|

Positive and

reductive

|

Positive and

reductive

|

Negative and

reductive

|

Positive and

explosive

|

Positive and

explosive

|

Negative and

reductive

|

Negative and

reductive

|

|

4

|

Positive and

reductive

|

Positive and

reductive

|

0

|

Negative

|

Positive and

reductive

|

Negative and

reductive

|

0

|

Positive and

reductive

|

positive

|

Negative and

reductive

|

|

5

|

0

|

0

|

0

|

Negative and

reductive

|

Negative and

reductive

|

Negative and

reductive

|

0

|

Negative and

reductive

|

Positive and

reductive

|

0

|

|

6

|

0

|

0

|

0

|

Positive and

reductive

|

Positive and

reductive

|

0

|

0

|

Positive and

reductive

|

Negative and

reductive

|

0

|

|

7

|

0

|

0

|

0

|

00

|

0

|

0

|

0

|

Constant

|

0

|

0

|

|

8

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

Constant

|

0

|

0

|

|

9

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

Positive and

reductive

|

0

|

0

|

|

10

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

0

|

Source: research findings using Eviews

software

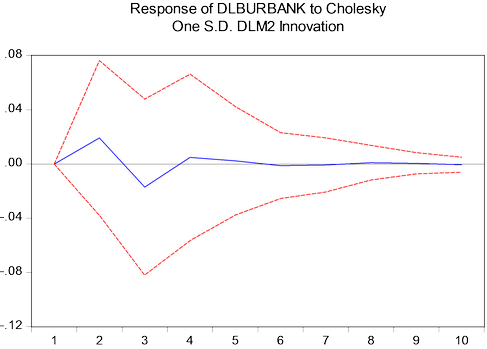

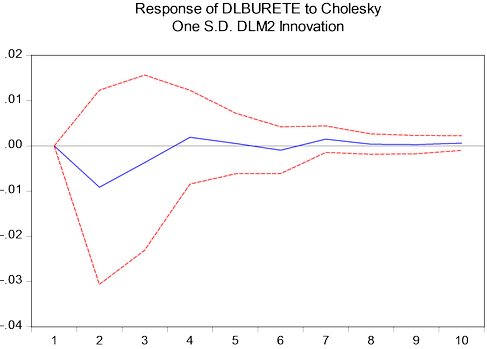

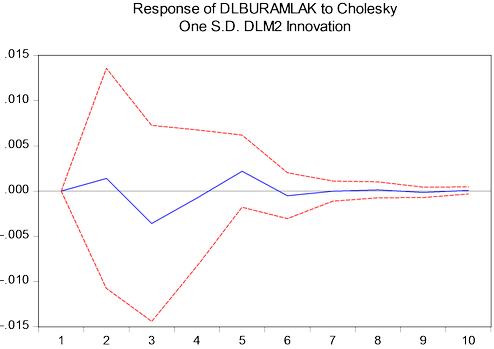

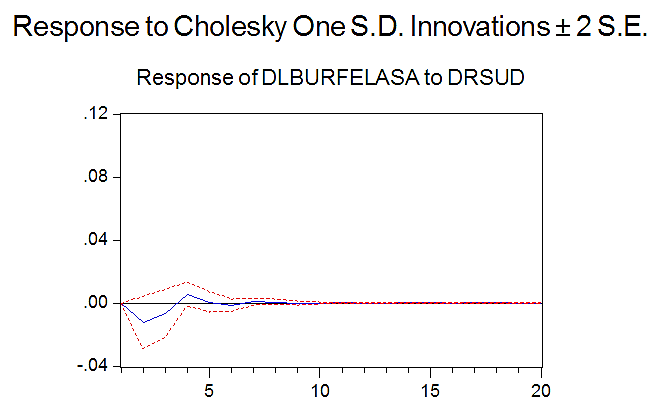

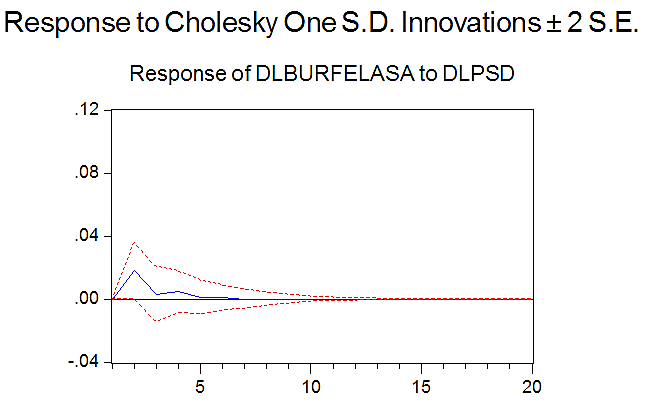

Figure 1: diagram of results of the

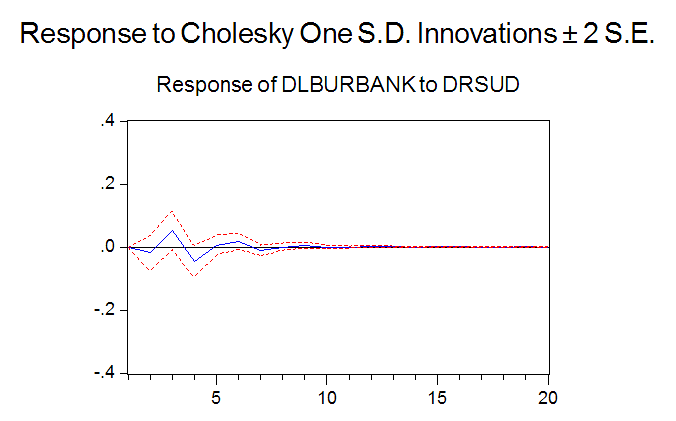

IFR of banks and credit institute index to monetary shocks

Figure 2: diagram of results of the

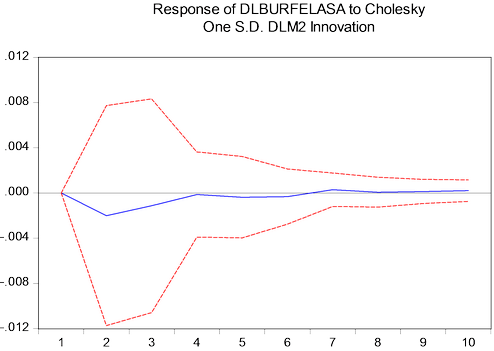

IFR of cement stock exchange index to monetary shocks

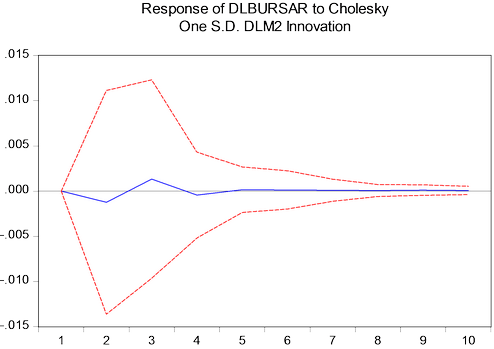

Figure 3: diagram of

results of the IFR of car industry stock exchange index to monetary shocks

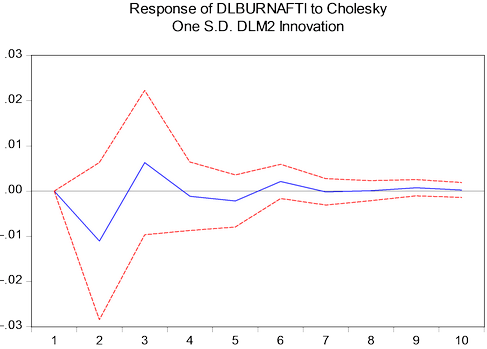

Figure 4: diagram of the IFR

results of multidisciplinary industry stock exchange index to monetary shocks

Figure 5: diagram of results of the

IFR of metal extraction industry stock exchange index to monetary shocks

Figure 6: diagram of results of the

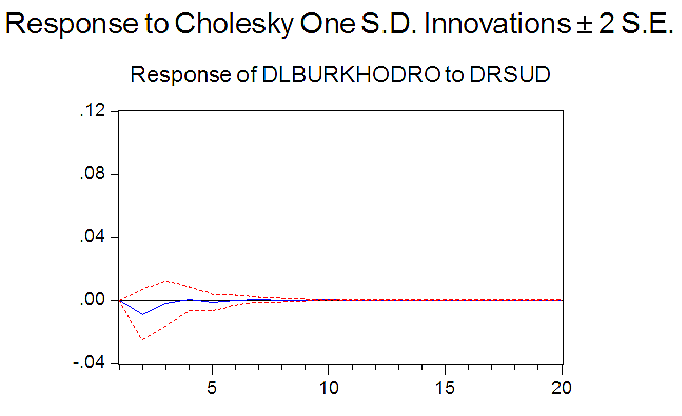

IFR of fundamental metal industry stock exchange index to monetary shocks

Figure 7: diagram of results of the

IFR of enterprises stock exchange index to monetary shocks

Figure 8: diagram of results of the

IFR of oil product stock exchange index to monetary shocks

Figure 9: diagram of results of the

IFR of real estate stock exchange index to monetary shocks

Figure 10: diagram of results of

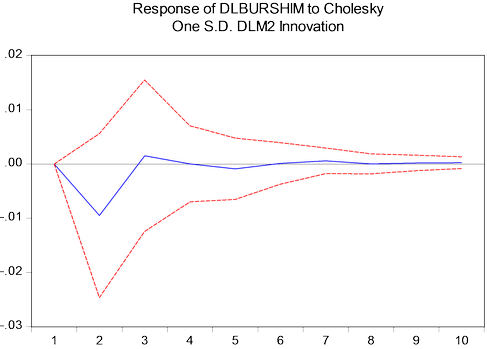

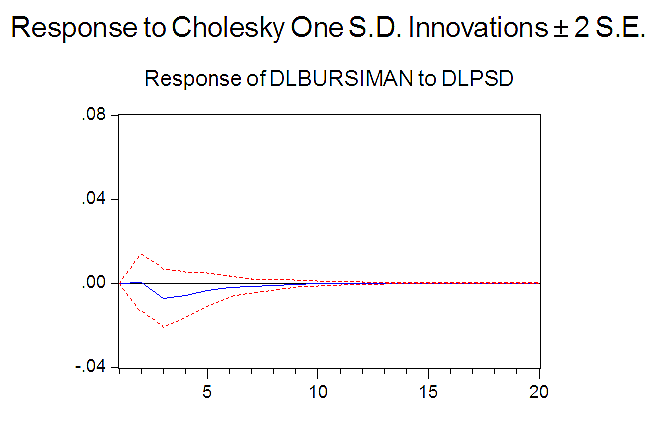

the IFR of chemicals stock exchange index to monetary shocks

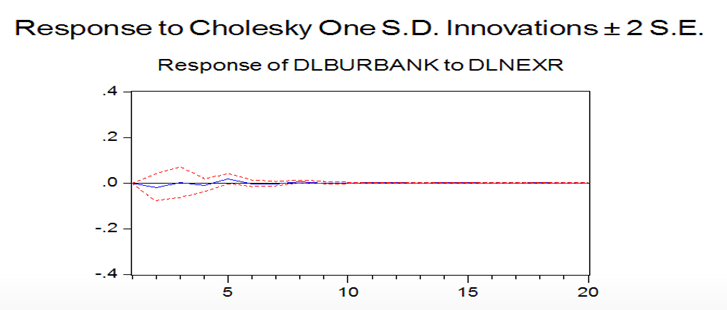

Figure 11: diagram of IFR of banks

and credit institute group index in stock exchange to monetary policy shock in

terms of exchange rate

Figure 12: diagram of IFR of banks

and credit institute group index in stock exchange to monetary policy shock in

terms of grants

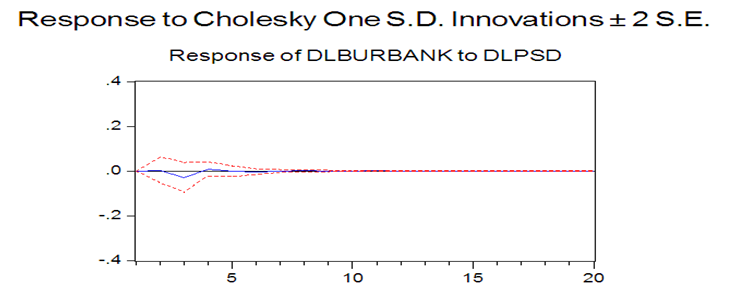

Figure 13: diagram of IFR of banks

and credit institute group index in stock exchange to monetary policy shock in

terms of real interest rate

Figure 14: diagram of IFR of cement

group index in stock exchange to monetary policy shock in terms of grants

Figure 15: diagram of IFR of cement

group index in stock exchange to monetary policy shock in terms of real

interest rate

Figure 16: diagram of IFR of cement

group index in stock exchange to monetary policy shock in terms of exchange

rate

Figure 17: diagram of IFR of car

and assembly group index in stock exchange to monetary policy shock in terms of

grants

Figure 18: diagram of IFR of car

and assembly group index in stock exchange to monetary policy shock in terms of

real interest rate

Figure 19: diagram of IFR of

multidisciplinary industries group index in stock exchange to monetary policy

shock in terms of grants

Figure 20: diagram of IFR of metal

extraction group index in stock exchange to monetary policy shock in terms of

grants

Figure 21: diagram of IFR of

fundamental metals group index in stock exchange to monetary policy shock in

terms of real interest rate

Figure 22: diagram of IFR of

fundamental metals group index in stock exchange to monetary policy shock in

terms of grants

Figure 23: diagram of IFR of mass

building and real estate group index in stock exchange to monetary policy shock

in terms of exchange rate

Figure 24: diagram of IFR of mass

building and real estate group index in stock exchange to monetary policy shock

in terms of grants

Conclusion

The interdependence of asset price and

monetary policy is the main issue of financial economics and has gained many

attentions especially after the last financial crisis of the world. Among

different aspects of the interdependence, effect of monetary policy shocks on

efficiency and stock index has been almost considered in theoretical literature

more than before. The literature could be divided to two groups:

a) Event

studies: these studies are based on descriptive method and can analyze

endogenous and unpredictable changes in monetary policy separately.

b) SVAR-based

studies, which apply some unique limitations that limit the interaction between

economic variables, so that they are not necessarily in consistence with the

data and backgrounds. The limitations are also divided to two types as follows:

1) Limitations

that introduce policy index and 2) limitations that specify method of

publishing monetary policy shocks.

Empirically, evaluation of effectiveness

of monetary policy transmission channels can result in better decision making

of Central bank through creation of a suitable insight. Monetary transmission

is a process, which can transfer monetary policy measures to economics and is

considered as an axial issue in macroeconomics. Structural features of

economics and financial markets can affect effectiveness of different channels

of monetary policy transmission. According to bank loaning channel,

expansionary monetary policy (such as increase in legal reserves or purchase of

reserve assets of commercial banks by Central Bank) can reduce usable reserves

of commercial banks. Moreover, controlled monetary policies can reduce

attraction of deposits in commercial banks through affecting economic

activities.

According to the mentioned, it could be

claimed that monetary policies can also affect stock market significantly. If

monetary policies affect real part of economics and as a result, affect prices,

monetary conditions of economics can affect behavior of return of stock

exchange. Hence, stock market as capital market plays vital role in

transferring effects of monetary policies on different economic sectors.

The common method of making relationship

between monetary policy and market behavior is estimation of SVAR model of

different monetary indices and stock returns. VAR models present flexible and

suitable framework to control the movement direction of monetary policy

mechanism. However, the relevant issue of omitted variables can lead to a

fundamental bias in VAR estimations in field of monetary policy. In this field,

a basic solution is to use SVAR method, which can solve this problem. Sims and

Bernanke (1986) have suggested a method to model deviation terms based on

economic decompositions to solve this problem. This method is based on

estimation of the relations between structural deviations based on an economic

model, which is used in this study.

Total distribution of SVAR test based on

Jarque-Bera criterion shows that probability related to this distribution among

5 variables is over 0.05 and hence, the H0 based on multivariate normal

distribution of SVAR model for top 10 industries is confirmed. As a result, the

entire model is distributed normally.

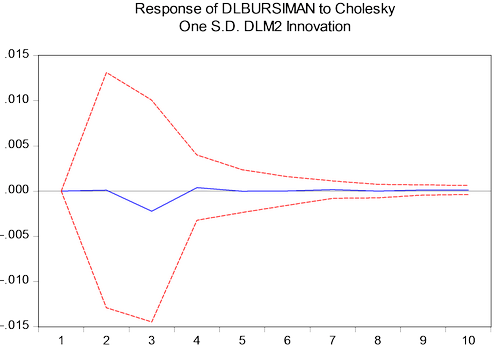

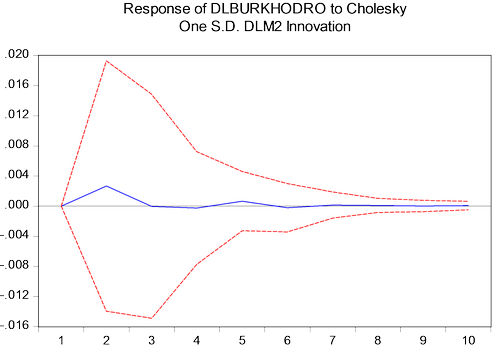

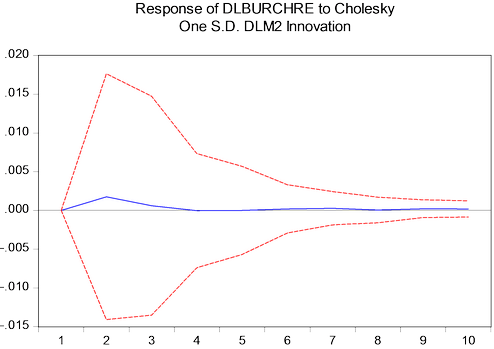

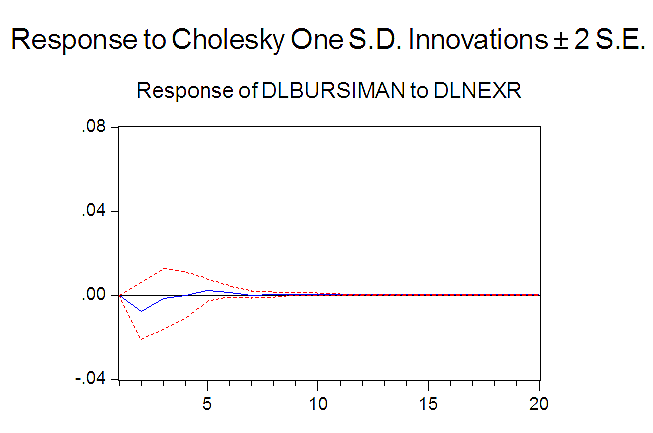

Obtained results from IRF test also show

that the shock resulted from monetary policy during first period have no effect

on indices of exchange industries; although effects of this shock would be

appeared after second period. In this field, effects of monetary shock have

been explosive on some indices (chemicals, metal and oil extraction); have been

sinus explosive on some indices (bank and credit institute exchange index) and

have been negative (enterprises and cement industry) or positive (car,

multidisciplinary industries and real-estate) on some others. However, it could

be found that among the top 10 industries, the index of banks and credit

institutes industries, oil industries, chemical industry and metal industry

have been shocked more than other ones. This can be rooted in large portion of

oil sector in economics and effect of domestic and foreign fluctuations on it

and secondly, the relationship of monetary shocks and banking network resources

and thirdly, can be rooted in high dependence of metal extraction on banking

resources.

According to obtained results in field

of SVAR model, it could be found that shocks can firstly have the most effect

on monetary policies belonged to real interest rate and on real estate and mass

building index, so that 1% increase in real interest rate has affected the said

index more than 6% negatively. Secondly, liquidity shocks have had the most

effect on car exchange index and then on real estate and mass building index.

Thirdly, exchange rate has shown most effect on car industry. Hence, with 1%

increase in exchange rate, car stock exchange index is improved to more than

2%. Fourthly, effects of monetary policies in terms of grants to private sector

have had the most effect on car industry, oil and real estate industries.

Obtained results from IRF showed that

depending on type of monetary shock, total index of stock exchange and top

indices can show different responses, so that relevant shocks of grants to

private sector have had the most and the worst effect and monetary shock has

had least and shortest effect on the mentioned indices. Relevant investigations

of SVAR model show that in short-term, expansionary policy can affect index of

top 10 industries positively through increasing liquidity (Reduction of legal

reserves, injection of high-powered money, reduce the penalty rate of the

Central Bank and reduced the documents discount rate by the Central Bank).

Hence, Expansionary monetary policy (restrictive) can have positive (negative)

effect on index of top 10 industries in terms of liquidity directly and in

short-term. On the other hand, Expansionary monetary policy (restrictive) in

field of facilities granted by banks can empower (weaken) liquidity volume and

can have positive (negative) effect in short-term and indirectly on indices of

cement, Lime & Plaster, car, multidisciplinary industries, chemical

industries, metal extraction, fundamental metals, enterprises, oil products and

nuclear fuel and mass building and can also empower direct effect. However, in

regard with exchange index of banks and credit institutes, this effect is

negative and neutralizes direct effect and the overall effect of outcome of the

two effects is not clear and is depended on volume and amount of monetary

shocks and granted facilities to private sector.

According to the objectives of this

study, the hypothesis included: 1) monetary policy can affect efficiency of top

10 industries of Tehran Stock Exchange; 2) effect of monetary policy on stock

return of different industries varies depending on type of industry. According

to obtained results, it could be mentioned that firstly, monetary policy

(monetary shocks, shocks of grants to private sector and nominal interest rate)

can affect different stock exchange indices through creating shocks in nominal

exchange rate and real interest rate (by

inflation rate). Hence, hypothesis 1 is confirmed. Secondly, monetary policies

can affect different indices of stock exchange industries and this effect

varies depending on type of industry and hence, hypothesis 2 is also

confirmed.

References

1. Central

Bank of the Islamic Republic of Iran, (2015) various indicators.

2. Securities

and Exchange Organization, (2015) monthly statistical reports.

3. Shahbazi,

K, et al, (2012). Monetary and fiscal policies and performance of the stock

market: the empirical evidence in Iran. Knowledge of financial &

securities analysis, No. 20, pp 63-77.

4. Keshavarz,

H, et al, (2005), does the stock market a channel for passing the monetary

policy in the economy? Economic Research Journal, No. 71, pp 147-170.

5.

Amador, Fernandez,

Octavio & Martin, Gachter & Martin, Larch

and Georg, peter. (2013). Does monetary policy determine stock market

Liquidity? New evidence from the euro zone. Journal of Empirical Finance.

No. 21. pp (54–68).

6.

Central Bank of Japan.

(2011), the roles of Bank of Japan and its functions in monetary policy.

7.

Devtyan, Karen. (2016),

the Distributive Effects of Conventional and Unconventional Monetary Policies.

Institut de Recerca en Economia Aplicada Regional.

8.

Ghazanchyan, Manuk.

(2014). Unraveling the Monetary Policy transmission mechanism in Sri Lanka.

IMF working paper, No. 190.

9.

Ghosh, Saibal. (2009). Industry

Effects of Monetary Policy: Evidence from India. Reserve Bank of India.

10.

Gueriny, Pierre and

Danilo Leiva-Leonz (2016), “The Effects of Monetary Policy on Industry-level

Stock Returns in a Changing World”, Bank of Canada, pp-2-4.

11.

Krainer, Robert, E.

(2014). Monetary policy and bank lending in the Euro area: Is there a stock

market channel or an interestrate channel. Journal money and finance. No.

49. P (283-298).

12. Lutkepohl,

H. (2005). New Introduction to Multiple Time Series Analysis. Berlin:

Springer Verlag.

13.

Mishkin, Fredric.

(1996), the channels of Monetary Transmission: Lessons for monetary policy.

Combridge NBER working paper series, No. 5464.

14.

Mohanty M. S. (2014). The

transmission of unconventional monetary policy to the emerging markets.

Bank for International Settlements, 78, 1-24.

15.

Mukherjee, Sanchita and

Bhattacharya, Rina. (2011). Inflation targeting and monetary Mechanism in

emerging market economies. IMF working paper, No. 229.

16.

Poddar, Tushar&

Sab, Randa and Khachatryan, Hasmik. (2006), the monetary transmission

mechanism in Jordan, IMF working paper, No. 48.

17.

Sourial, Maged Shawky.

(2002). Monetary Policy and it impact on the Stock Market: The Egyptian Case.

Ministry of Economy & Foreign Trade. Cairo, Egypt, (202), 3916-991.

18.

Tsai, chun-Li. (2014). The

effects of monetary policy on stock returns: Financing constraints and

“informative” and “uninformative” FOMC statements. International Review of

economics and finance. No. 29, pp 273-290.