Management Practices in Working Capital -A Comparative Study in NALCO Vs HINDALCO

|

Dr. Suman Kalyan Chaudhury

Faculty Member

P.G. Department of Business Administration

Berhmapur University

Odisha

|

Mr. Pramath Nath Acharya

Research Scholar

P.G. Department of Commerce

Berhampur, Odisha

|

Abstract

Working capital

management is important in financial management due to the fact that it plays

an essential role in keeping the wheels of a business enterprises running. The

business will not be able to carry on day to day activities without the

availability of adequate working capital. In a common way, managing of current

assets and current liability is called the Working Capital management. In any

business firm, whether it is trading or manufacturing business, the relevance

of working capital can never be overemphasised. Shortage of funds for working

capital has caused many businesses to fail and in many cases has retarded their

growth. Lack of efficient and effective utilisation of working capital leads to

earn low rate of return on capital employed or even compel sustain losses. In

other words, the efficiency of a business enterprise depends largely on its ability

to manage its working capital. However the requirement of working capital

varies from firm to firm. It is depending upon the nature of the business like

production policies, market conditions, seasonality of operations, conditions

of supplies etc. For manufacturing companies, working capital creates

challenges because supplier and production expenses frequently require payment

several months before goods are sold to customers. Aluminium companies, as a

part of manufacturing sector, are required to give emphasis in this regard. In

this context, it is an effort to accesses the practice of working capital

management in Nalco and Hindalco through some

hypothesis testing. In this paper, the authors’ try to analyse the working

capital management practices of NALCO and HINDALCO which would facilitate in

maximizing the firm’s value and the wealth of the shareholders.

Keywords: Working Capital Management,

Capital Insolvency, Liquidity, Ratios

Introduction

Working

capital is considered as a significant issue in financial decision-making. It

calls for appropriate financing investment. However, according to Sanger,

working capital has always been ignored in financial decision-making because it

involves investment and financing in short-term period. It also acts as a

restrain in financial performance, since it does not contribute directly to

Return on Stakeholders’ Equity (ROSE). The essential part in management of

working capital lies in maintaining its liquidity in day-to-day operation to

ensure smooth running of the business and meets its obligations or else it

would lead to operational insolvency. Managers must ensure that the firm

functioning is efficient and profitable. Further, there are high possibilities

of mismatch between current asset and current liability during this process. If

this happens and firm’s manager fails to manage it properly then it will affect

firm’s growth and profitability which will further escort to financial distress

and finally firms can go capital insolvency.

Aluminium Industry in India

Aluminum industry is one of the highly concentrated industry

in India and the top five companies in this sector offers a great share towards

the production of the country. With the increasing demand for aluminum in

India, the top players in this sector are also growing at a faster

pace. The fact is that production of Aluminum in India has presently outpaced

the demand for aluminum in the country. India holds the third place in the

aluminum production in the world and the country has a competence of producing

2.7 million tones (MTPA), which is nearly 5% of the total aluminum production

all over the world.

Table-1 Major Aluminium

Producing Countries

|

Countries

|

Production

in ‘000 t

|

|

2008

|

% of total

|

2014

|

% of total

|

|

China

|

13,695

|

34

|

21,481

|

43

|

|

Russia

|

4,191

|

10

|

3,712

|

7

|

|

Canada

|

3,124

|

8

|

756

|

2

|

|

USA

|

2,658

|

7

|

1,754

|

3

|

|

Australia

|

1,978

|

5

|

1,727

|

3

|

|

Brazil

|

1,661

|

4

|

1,684

|

3

|

|

Norway

|

1,383

|

3

|

1,195

|

2

|

|

India

|

1,348

|

3

|

3,958

|

8

|

|

Dubai

|

899

|

2

|

1026

|

2

|

|

Others

|

9,194

|

23

|

13,042

|

26

|

|

Total

|

40,131

|

100

|

50,335

|

100

|

Source:

http://aluminium-india.org/Worldscenario.php

Table-2 Major Aluminium Consuming Countries

|

Countries

|

Consumption in ‘000 t

|

|

2008

|

% of total

|

2014

|

% of total

|

|

China

|

12,604

|

34

|

22,088

|

44

|

|

USA

|

5,147

|

14

|

5,505

|

11

|

|

Japan

|

2,319

|

6

|

2,259

|

4

|

|

Germany

|

1,929

|

5

|

2,054

|

4

|

|

Middle East

|

1,459

|

4

|

2,030

|

4

|

|

India

|

1,089

|

3

|

3,800

|

8

|

|

Italy

|

951

|

3

|

869

|

2

|

|

South Korea

|

937

|

3

|

1297

|

3

|

|

Brazil

|

933

|

3

|

1,198

|

2

|

|

Others

|

10,051

|

24

|

9,551

|

19

|

|

Total

|

37,419

|

100

|

50,651

|

100

|

Source:

http://aluminium-india.org/Worldscenario.php

Aluminium plays a key role in the industrial development of India as it

serves as a basic input for most of the industries. Progressing in long way

since early fifties, India’s aluminium industry is well placed to explore

untapped demand potential. With a meagre production capacity of 5000 tonnes

(TPA) in fifties, the production of Indian aluminium industry has reached 3958000

tonnes as on 2014. Aluminium industry

in India, comparatively a recent origin, has progressed very fast and has been ranked

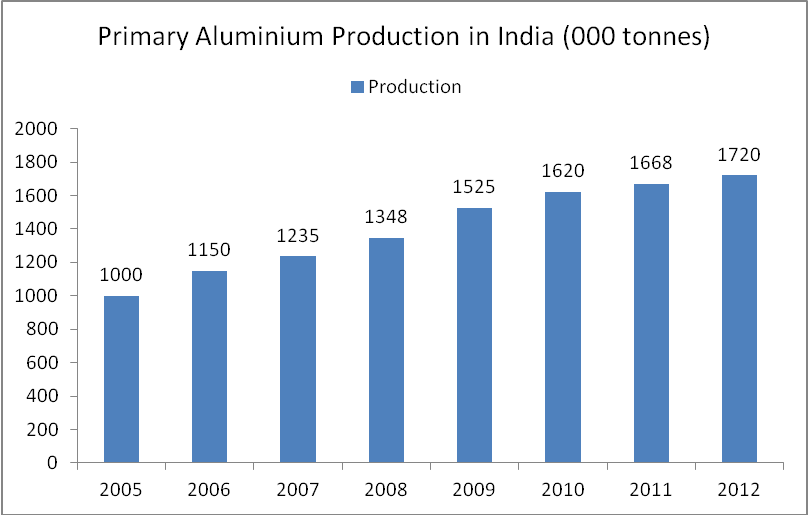

as 2nd largest producer of aluminium in the world after China. However, in India, the production of primary aluminium

was stagnated around the 1.6 to 1.7 million tonne mark for the last three years

as surge in the global demand.

Simililarly the table -2 signifes the global consumption of alumninium,whereas

Indian consumption satands at 3rd position with a consuption 3800000

tonnes next to China and USA. The aluminium consuption of China and USA is

22088000 tonnes and 5505000 tonnes respectively. The major users in the segment of aluminium consumption continues

to be automotive & transportation sector followed by building &

construction, packaging, consumer durables, electrical & electronics, industrial

and other applications including defence in indian domestic market.

Fig No-1 Primary Aluminium Production

in India

Source: Company Report/ MCG Research

Table-3

Production of Major Aluminium Players

|

Name of the Company

|

Production in Thousand Tonns

|

|

Year

|

2011-12

|

2012-13

|

2013-14

|

2014-15

|

|

HINDALCO

|

574

|

542

|

512

|

593

|

|

NALCO

|

413

|

403

|

316

|

244

|

|

VEDANTA

|

429

|

527

|

542

|

406

|

|

Total

|

1416

|

1472

|

1370

|

1243

|

Source: Press Information Bureau (PIB), Ministry of Mines,

Government of India.

Table-3

Sales of Major Aluminium Players

|

Sl. No

|

Name of the Company

|

2011-12

Sales in Cr’s

|

2012-13

Sales in Cr’s

|

2013-14 Sales in Cr’s

|

2014-15

Sales in Cr’s

|

|

01

|

HINDALCO

|

26596.78

|

26056.93

|

27850.93

|

34525.03

|

|

02

|

NALCO

|

6611.48

|

6916.48

|

6780.85

|

7382.81

|

|

03

|

VENDANTA

|

6513.45

|

2187.92

|

28536.53

|

32502.41

|

Source: Annual Reports

In India the

aluminium production is carried out by public sector as well as private sector

companies. A list of companies producing aluminium in India is given in table

no. 3. It can be observed from the table that Hindalco and Nalco have became

the largest players in this market. The three primary aluminum

producers, viz. Hindalco, Vedanta and Nalco have

expansion plans as well as greenfield projects that

should take the production to 2.5 to 3.0 million tonnes in the foreseeable

future.

Objective of Study

The study was

carried out with the objectives which are presented below:

- To

understand the concept of working capital management and its importance.

- To

understand the role and significance of various ratios related to working

capital.

- To

understand the working capital practices by NALCO and HINDALCO.

- To

determine whether there is any significant difference in various ratios of

working capital management between NALCO & HINDALCO.

Hypotheses of the Study

Based on the objectives as cited,

the following hypotheses were formulated for the study:

H01:

There is no significant difference between NALCO & HINDALCO with respect to

Current Ratio.

H02:

There is no significant difference between NALCO & HINDALCO with respect to

Quick Ratio.

H03:

There is no significant difference between NALCO & HINDALCO with respect to

Inventory Turnover ratio.

H04:

There is no significant difference between NALCO & HINDALCO with respect to Debtor Turnover Ratio.

H05:

There is no significant difference between NALCO & HINDALCO with respect to

Working Capital Turnover Ratio.

Research Methodology

The

study is carried out by considering NALCO & HINDALCO as the sample unit

which are among the largest Aluminium producers in India. The data collected

for this research was basically from secondary sources which include web

sources like www.moneycontrol.com and www.rediff.com/money data base for a

period of ten years i.e. 2004-05 to

2013-14. The collected was analysed by using statistical tools in Ms-Excel such

as Mean and Standard Deviation. To test the hypotheses, the researchers have

used t-test

to get the level of significance and draw inference for the study. The study

was carried out by developing and testing some hypotheses with respect to both

the companies.

Limitations of Study

In the course of

research certain problems were encountered which might had adverse effect on

the work. The study is based on the data collected from the secondary sources.

Time constraint is one of the most important limitations for the study. Limited

sample size is another problem where the result could not be generalised.

Data Analysis and Interpretation:

The analysis and

interpretation of the study are based on the parameters mentioned in the

methodology of the study. This section is divided in to two parts. The first

one makes the analysis of Trend in working capital and second part discusses

the testing of hypothesis.

Table

4 Gross Working Capital (in Rs.)

|

Years

|

NALCO

|

HINDALCO

|

|

Mar '05

|

1,861.83

|

4,476.43

|

|

Mar '06

|

3,346.65

|

7,315.07

|

|

Mar '07

|

5,044.95

|

7,846.17

|

|

Mar '08

|

5,103.21

|

7,926.26

|

|

Mar '09

|

4,605.57

|

7,824.24

|

|

Mar '10

|

5,333.42

|

8,962.11

|

|

Mar '11

|

6,213.33

|

10,904.79

|

|

Mar '12

|

7,469.73

|

12,869.15

|

|

Mar '13

|

7,206.08

|

15,433.66

|

|

Mar '14

|

7,742.79

|

16,530.55

|

Figure 2 Gross Working Capital

The above graph

shows the trend in gross working capital of NALCO and HINDALCO during the study

period. It can be observed that HINDALCO maintains higher level of working

capital comparing to NALCO. It shows positive trend after 2009 in HINDALCO

because the firm invested more in current assets. But in case of NALCO

fluctuation is noticed during the study period.

Testing of Hypotheses

The hypotheses

of the study have been tested by applying t-test

which is normally used to determine if two sets of data are significantly

different from each other with an assumption that the test statistics would

follow normal distribution. The t-test results

are depicted in the tables given below and suitable interpretations are made

accordingly.

Hypothesis

(H01): There is no significant difference

between NALCO & HINDALCO with respect to Current ratio.

Table 5 Current ratio

|

NALCO

|

HINDALCO

|

|

Mean

|

1.883

|

1.101

|

|

Variance

|

0.151756667

|

0.009987778

|

|

Observations

|

10

|

10

|

|

Pooled Variance

|

0.080872222

|

|

|

Hypothesized Mean Difference

|

0

|

|

|

Degree of freedom

|

18

|

|

|

t Stat

|

6.148824064*

|

|

|

P

|

0.000

|

|

|

t Critical

|

2.100922037

|

|

*1% level of significance

The above table-5

presents the current ratio of the both companies. Since the t- stat (calculated value) is greater

than t critical (tabulated value)

i.e. 6.14 > 2.11. The t stat values

are positive & significant at 1% level of significance. So the null

hypothesis will be rejected. Hence, there is a significant difference between NALCO

& HINDALCO in maintaining the current ratio. The mean value of current

ratio of NALCO is found to be better than mean value of HINDALCO during the

study period. The higher the ratio the better it will be in a position to meet

its current obligation easily. So NALCO’s position is good comparing to

HINDALCO.

Hypothesis

(H02): There is no significant difference

between NALCO & HINDALCO with respect to Quick ratio.

Table

6 Quick Ratio

|

|

NALCO

|

HINDALCO

|

|

Mean

|

1.541

|

0.628

|

|

Variance

|

0.14892111

|

0.0354178

|

|

Observations

|

10

|

10

|

|

Pooled Variance

|

0.09216944

|

|

|

Hypothesized Mean Difference

|

0

|

|

|

Degree of freedom

|

18

|

|

|

t Stat

|

6.72453556*

|

|

|

P

|

0.00

|

|

|

t Critical

|

2.10092204

|

|

*1%

level of significance

Here the calculated Table-6

presents the quick ratio of NALCO & HINDALCO. Since the t stat (calculated value) is greater

than t critical (tabulated value)

i.e. 6.72 > 2.11, the null hypothesis is rejected at 1% level of

significance. Hence there is a significant difference between NALCO and HINDALCO

in maintaining the quick ratio. Comparing the current ratio and quick ratio of

both the companies, it can be seen that HINDALCO has higher inventory position

as compared to NALCO. It is also found that the quick ratio of HINDALCO is less

than 1:1 which is considered as an ideal in a manufacturing Industry. This

means that the liquid assets of HINDALCO are not equal to its current

liabilities.

Hypothesis

(H03): There is no significant difference

between NALCO & HINDALCO with respect to Inventory turnover ratio.

Table

7 Inventory turnover ratio

|

|

NALCO

|

HINDALCO

|

|

Mean

|

8.247

|

3.809

|

|

Variance

|

14.78406778

|

0.469454444

|

|

Observations

|

10

|

10

|

|

Pooled Variance

|

7.626761111

|

|

|

Hypothesized Mean Difference

|

0

|

|

|

Degree of freedom

|

18

|

|

|

t Stat

|

3.593372405

|

|

|

p

|

0.002

|

|

|

t Critical

|

2.100922037

|

|

*1% level of significance

Inventory turnover ratio of the

firms are calculated and presented in Table-7. Since the t stat (calculated value) is greater than t critical (tabulated value) i.e. 3.59 > 2.11, the null

hypothesis is rejected at 1% level of significance. Hence there is a

significant difference between both the firms in maintaining the Inventory

turnover ratio. The higher the inventory turnover ratio, the better it is. As

compare to HINDALCO, NALCO shows higher inventory turnover ratio. This means

that NALCO is able to convert the inventory into finished stocks quickly.

Hypothesis

(H04): There is no significant

difference between NALCO and HINDALCO with respect to Debtor turnover ratio

Table

8 Debtor turnover ratio

|

NALCO

|

HINDALCO

|

|

Mean

|

77.221

|

15.539

|

|

Variance

|

2440.945

|

10.10492

|

|

Observations

|

10

|

10

|

|

Pooled Variance

|

1225.525

|

|

|

Hypothesized Mean Difference

|

0

|

|

|

Degree of freedom

|

18

|

|

|

t Stat

|

3.939874*

|

|

|

p

|

0.00096

|

|

|

t Critical

|

2.100922

|

|

*1% level of

significance

Debtor turnover ratio of the firms are calculated and presented in Table 8. Since

the t stat (calculated value) is

greater than t critical (tabulated

value) i.e. 3.93 > 2.11, the null hypothesis is rejected at 1% level of

significance. Hence there is a significant difference between both the firms in

maintaining the Debtor turnover ratio. In case of NALCO the mean debtor

turnover ratio is high whereas in case of HINDALCO it is low. This ratio

indicates the speed with which these debtors are collected that effects the

liquidity position of the firms. It is found from the above study that NALCO is

able to collect from the debtors quickly as compare to HINDALCO.

Hypothesis

(H05): There is no significant

difference between NALCO and HINDALCO with respect to Working Capital turnover

ratio.

Table 9 Working Capital turnover

ratio

|

|

NALCO

|

HINDALCO

|

|

Mean

|

0.6572073

|

1.665

|

|

Variance

|

0.028035634

|

0.054761111

|

|

Observations

|

10

|

10

|

|

Pooled

Variance

|

0.041398373

|

|

|

Hypothesized

Mean Difference

|

0

|

|

|

Degree of

freedom

|

18

|

|

|

t Stat

|

-11.07553*

|

|

|

P

|

0.00

|

|

|

t Critical

|

2.100922037

|

|

*1% level of significance

Here the calculated Table-9

presents the working capital turnover ratio of the both companies. Since the t stat (calculated value) is greater

than t critical (tabulated value)

i.e. 11.07 > 2.11, the null hypothesis is rejected at 1% level of

significance. Hence there is a significant difference between NALCO and HINDALCO

in maintaining the working capital turnover ratio. Working capital turnover

ratio shows the velocity or utilization of the working capital of the firm

during a year. A high working capital turnover ratio reflects the better

utilization of the working capital of the firm.

Findings and Conclusions

In the current

study it shows that the current ratio of NALCO is higher than HINDALCO. So it

will be in a position to meet with the current obligation easily. In case of

quick ratio HINDALCO has higher inventory position as compared to NALCO because

the quick ratio of the manufacturing industry is less than the ideal ratio i.e 1:1. Inventory

turnover ratio of NALCO is higher than HINDALCO which proves that NALCO is able

to convert the inventory into finished stock quickly. It can be concluded that NALCO

can meet the current obligation comfortably. With respect to debtor turnover

ratio it is found that NALCO is able to collect from the debtors quickly as

compare to HINDALCO. It is found from the working capital turnover ratio that HINDALCO

convert the overall working capital quickly into the finished stocks.

Working capital

management is a significant issue in firm’s corporate financial decision making

process which needs careful consideration. The present study move in this

regard that from the quick ratio it is found that the NALCO is maintaining

higher quick ratio of 1.5 against 1:1 which is an ideal ratio in manufacturing

industry. Hence NALCO should take necessary steps to reduce the cash

equivalence. When we analyse the both companies in these ratios such as i.e Current

Ratio, Quick Ratio, Inventory turnover Ratio, Debtor turnover Ratio, Working

capital turnover Ratio it is found that NALCO’s performance is better than HINDALCO.

References

[1] Agrawal, A.

(2011), How to Manage Working Capital: An Empirical Study of Maruti Suzuki India Limited, Journal of Accounting and

Finance, Apr-Sept, Vol.25, pp. 85-92.

[2] Annual Reports of NALCO 2004-05 to 2013-14.

[3] Achrya,P.N and Mahpatra,R.P (2013), Working Capital

Management: A case study of NALCO, Journal of Accounting and Finance, Vol.27 ,

No.2, pp.35-44.

[4] Bhatachrya,H (2011), Working Capital Management, PHI, New Delhi.

[5] Chandara, H. and Selvaraj, H. (2012), Working Capital management in selected

Indian Steel Companies, Indian journal of Finance, Vol.6, No.11, pp.5-15.

[6] Chandra P.,(2009), “Financial management”, Tata Mc Grow-Hill

Publishing Company Limited, 7 West Patel Nagar ,New Delhi – 110008.

[7] Mukhopadhyay. D.

(2004), “Working Capital Management in heavy engineering Firms.” The

Management Accountant, Vol.10, No.23, pp.115.

[8] Pandey, I.M (2006),“Financial Management”, Ninth Edition, Vikash

Publishing House, New Delhi.

[9] Singh, J.P. and Pandey, S. (2008), Impact

of Working capital Management in the profitability of HINDALCO Industries

Limited, The ICFAI University journal of

Financial Economics, Vol.VI, No.4, pp 62-72.

[10]

www.hindalco.co.in

[11]

www.moneycontrol.com

[12]

www.nalcoindia.co.in

[13]

www.rediffmoney.com