A Refereed Monthly International Journal of Management

Public-Private Project Finance in Kazakhstan’s Business

Author

|

Dana A. Eshimova, PhD in Law, Associate Professor ,

Azamat R. Oinarov, PhD in Sciences

Deputy Chairperson of the Board

Kazakhstan Center for Public-Private Partnership

65 Temirqazyk St., Astana 010017, Kazakhstan, T: + 7 7172701445 dana.eshimova@kzppp.kz

Chairman of the Board

Kazakhstan Center for Public-Private Partnership

65 Temirqazyk St., Astana 010017, Kazakhstan, T: + 7 7172701445

azamat.oinarov@kzppp.kz

|

Abstract

The paper examines the key mechanisms of the public-private project financing. On the example of Kazakhstan, a Central Asian country, the paper reflected the empirical evidences of how project finance could adapt to the conditions of a developing country. The study developed the model of public-private project financing. The paper recommended that each such public-private project financing model should adapt to specific multiple stakeholder interests. The outcomes of the study may be useful for potential investors in developing countries as well as broad end users.

Key words: public-private sector project finance, corporate finance, investor confidence, risk allocation, management.

Introduction

The evidences of the lead role of public-private partnerships (PPPs) indicate at the rising demand for PPPs. According to the 2014 Ernst & Young survey of world’s 440 top public officials, 75% respondents confirmed that PPPs will be critical in funding new investments on infrastructure in nearest future. Amongst the projects good governance principles(UNECE, 2008), investments are open to the diverse PPP models. To name just a few: the Norway model, Yale, the Canadian and the collaborative model stem from the strategies of private & public institutions, geared to deliver on the economic and social benefits for local citizenry (Sharma, 2015). Kazakhstan has yet to define its long-term path in using PPPs for business. How that goal may be attained under the condition that investor interests should be duely accounted for. In Kazakhstan’s overall economy, the share of the public-private sector attributes to a modest 15 percent share of GDP, as in most of the developing world. How can Kazakhstan draw in business capital to the PPPs development? Which financing model for PPP projects will it deploy? Those are the prime issues that this paper explores.

Conceptual Framework

In project implementation, financial losses of businesses are most conspicuous challenges. Today’s world faces the 12% increase in project financial losses compared to 2015. In overall, nearly US$ 122 million is annually wasted from every billion invested in projects, according to the PMI’s 8th Project Management Survey of 2016 (Sinha, 2011). The need for a choice of an appropriate project finance framework is acute. This is most pertinent for developing countries. One of the attractive features in such a model is that government may secure investments in the public sector without raising taxes or borrowing. The specific element in the PPP project finance that scares off potential investors is the fiscal risks. The conceptual framework of this paper builds on the development of the PPP project’s financing model. Hence, the development of such model derives from project implementation efficiency, interlinkages between different financing modes, and risk sharing. The model attributes to specific features of Kazakhstan’s PPP projects − for the model to meet the needs of a developing country such as Kazakhstan. The latter’s no-recourse based project finance framework needs to be explored for the possibility of involving special purpose project companies.

Review of Literature

The review of literature relating to project finance revealed the varying views on the research matter. Some specified time value of cash flows in PPP projects at the back of the lengthy life cycle (Yescombe, 2007). Others claimed that in situations when government can borrow funding at lower costs, taxpayers’ money should not be used for increasing private sector’s income (Tvarno, 2013). Practitioners mainly focused on the effective risk allocation between project parties. Risk allocation was believed to be the driver of project successes (Jing-Feng Yuan, 2010). Few among practitioners argued that risk allocation should be the key determinant of whether a given PPP project will be bankable or not (GIH, 2016). Most hybrid-type PPP projects favor capital improvements in an existing facility. The private sector entity was activated, to finance and operate the facilityrather than investing from scratch (US Dep. Trans., 2012). Amidst many suggestions on an institutional set-up for the PPP project finance, ones that offer a regulated PPP framework promises to be workable (Peterson, 2010). In essence, O. Hart pointed that incomplete contracting enables seeing the differences between government funding and PPP project financing (Hart O. , 2003). He discovered strong incentives that PPPs may offer for a private contractor “to plan beyond the bounds of the main phase of a project and, to incorporate features that will facilitate project operations” (Grimsey, 2004), p.92. As with all the above varied views, it becomes obvious that the research relating to how project finance in PPP projects may adapt to a developing country’s needs is insufficient. In the absence of empirical evidences on this matter, this paper argues that the readymade models on project finance are, in reality, not always applicable to every country. Therefore, the paper seeks answers to the question of what are the specificities of adapting PPP project finance in a developing country. It seeks for what should be done in order to make it workable.

Materials, Methods, Research Tools

The study used economic analyses tools, including regression analysis and economic simulation. The variables, as the result of the analyses, have been stored in the internal files of the Kazakhstan Public-Private Partnership Center (KPPPC), to ensure that property rights on information of private parties to the PPP projects be safeguarded. The bulk of 800 past and currently ongoing public and private projects have been processed by the study. The samplings of projects consisted of small, medium-sized, and large projects that have been implemented in such diverse sectors of the national economy as power, oil & gas, transport, industry, water & sewerage, waste & recycling. The study applied the historic approach and the principles of coherence, reliability, transparency and quality of the input data in carrying out the analyses of the paper. Interviews of the involved project managers, bank employees and other project staff have been conducted as relevant for project documents analysis. All data have been verified with last point sources of information. In analyzing the input data, the study used statistical analyses tools, including SPSS. The officially verified data has been derived from the Committee on Statistics under Kazakhstan’s Ministry of National Economy. Also, the open source databases of such international organizations as World Bank (WB), the United Nations (UN), International Monetary fund (IMF), and Organization of Economic Cooperation and Development (OECD) have been used.

In fulfilling the objective of the paper, the study first examined Kazakhstan’s new long-term PPP development program and outlined six core strategic goals in PPP development for 2016-2020:

- Establishment of the comprehensive PPP development system

- Removal of legal barriers

- Sophisticated risk allocation

- Diversifying funding sources

- Ensuring solid infrastructure investment market

- Replicating PPP experiences by well-trained civil service.

Strategically, the study employed the findings relating to the cabinet meeting’s outcomes on September 9, 2016, where the 5% GDP growth rate has been set for the country, starting from year 2017 onwards. The study primarily stemmed from the country’s needs to rapidly absorb the US$7 billion investments in subsequent five years. The study aligned with the country’s lead strategy of abstaining from direct budget funding of projects. Rather private sector businesses involvement was favored through PPP project financing and various off-budget subsidies. The use of project finance mechanisms has been publicly admitted as urgency (Nazarbayev, 2013). Therefore objective of this paper – to build the project finance model − stemmed from the fact that the new state budget, which was designed for 2017-2019, primarily targeted the new project financing mechanisms.

The study pursued to task of researching the project finance from the implementation stance. To that effect, Kazakhstan’s Prime Minister announced on September 15, 2016 that the deployment of PPP finance mechanisms should be extensive (Government, 2016). In this context, the study has set to explore project finance from the point of view of the five objectives on the implementation of PPP projects in 2016-2021:

- Implementing the project finance

- Improving the PPP framework for project financing

- Expanding on the contract types of PPP projects

- Forming the sustainable PPP project pipeline

- Introducing transparency and accountability in PPP project implementation

The PPP projects have been so designed to bridge in the missing links in funding the public-private sector development. According to the forecasts of the International Finance Corporation (IFC), an estimated amount of US$ 2 trillion a year would be required for private infrastructure investments and US$ 100 billion for handling global challenges. Likewise, the survey of the American Society of Civil Engineers in 2013 reported that business needs in the U.S. have been estimated at US$3.6 trillion in investments, by 2020 (Maher, 2016). In that sense, Kazakhstan is within world’s 90% of resources investments(Dobbs, 2013). The country’s needs for infrastructure project financing are modest. It is because of the limited access to private capital.

For the purposes of this paper, the study used the samplings of the PPPs, designed as a window of opportunities through which investors can offer their support. In this regard, small and medium sized public investment projects have been considered. That was due to their greater degree of flexibility. In this, the specific attention has been paid to those that are open to involving the PPP project finance. The study used the term of the project finance as being in use in Kazakhstan’s business circles, in particular, the ‘limited recourse financing’. Under the local legislation, public-private projects fall under category of the public (state) investment projects. In sampling the PPP projects for the purposes of the study of implementation and interlinkages within it, both, the project and corporate accounting practices have been sampled. Both have been recognized to be in equal need for decisionmaking on the PPP projects.

The hypothesis of the paper reflects the design of the study, which targeted to primarily serve the objectives of financing the country projects through PPPs. In this, the national holding companies envisage in their structures special purpose vehicles, SPVs. Those are to assume the right to build and operate the PPP projects. In this context, the project finance is being used for refurbishment. To that effect, SPVs have no existing businesses. These rather depend on revenue collections in each contract. In view of these realities, the study has admitted the following hypotheses:

Hypothesis 1-project finance is dependable on the project implementation performance

Hypothesis 2-project finance and corporate finance should be implemented parallel in time

Hypothesis 3-SPV is unnecessary for prospective project finance

Hypothesis 4-project finance is dependable on the effective risk allocation

- Limitation & Scope of the Study

The study had limitations stemming from the lack of locally available analyses tools, specific for PPP project finance. For that reason, the World Bank Group derived tools have been used for formulae and internationally standardized accounting techniques. The constraints associated with the locally existing safeguarding policies relating to the right of ownership of information on the PPP projects have also posed serious limitations as regards the disclosure of the project details. The scope of the study covered the public and private projects on the territory of Kazakhstan.

- Analysis

Hypothesis 1-project finance depends on project implementation

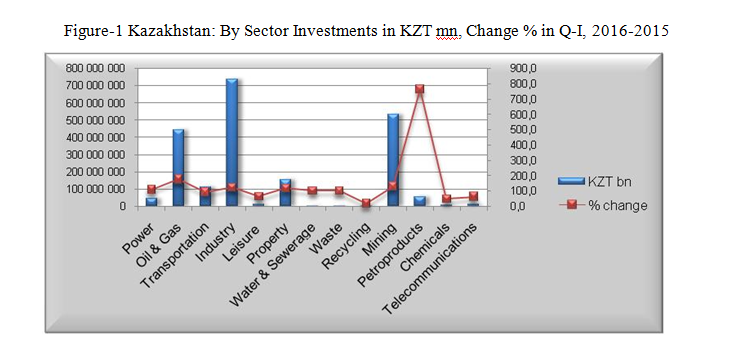

The analysis of the implementation performance of the PPP projects indicated that local fiscal institutions are in essence capable of providing the most needed capital. For that, however, the lengthy time frame was required. In theory, they are also capable of sharing project risks by putting up a proportion of their investments as equity. On one hand, Kazakhstan’s private businesses can handle such risks. On the other hand, consulting services help manage such risks. In practice, the bulk of project proceeds turned out to be tied up to the project performance. On the implementation side, Kazakhstan completed 800 infrastructure projects, until now. Specifically, the overall growth of the country’s GDP in the first 8 months of 2016 registered 0.3 percent rate (Bishimbayev, 2016). It was done at the back of investments growth at the 40% rate vs. the 2015 growth. Driven by government subsidizes, project investments grew to 12.7 billion KZT in 2016 from 6.1 billion Kazakhstan’s Tenges (KZT) in 2015. The breakdown of the incremental growth in investments has been shown in Figure-2.

Figure-1 Kazakhstan: By Sector Investments in KZT mn, Change % in Q-I, 2016-2015

Higher project proceeds have been in metals production at 8.3%, construction 6.7%, agriculture 4.9%, gas 3.5%, transport 4.2%. Yet, low project performance has been in manufacturing industry 0.7% and services 0.4%. Strong PPPs tend to rejuvenate an economy and their capacity to generate new assets(Yehoue, 2013). The analysis stemmed from the theoretical assertion that project finance may be effective for the implementation of PPP projects (Geraldi, 2008). In this context, the study offered the following five key advantages of the PPP project finance, to reinvigorate the weakening economy:

- Ability to start PPP projects from the zero level

- PPP-attracted investments are manifold excessive of PPP-owned capital

- Effective risks allocation amongst PPP project participants

- Systemic risks neutralization by introducing organizational PMOs

- Temporary deferral of servicing investors interests until projects’ operational capacity is fully unraveled

Hypothesis 2-project finance and corporate finance should be implemented parallel in time

To see how implementation of the PPP projects is financed, the study investigated the following key types of interlinkages between the project finance and corporate finance modes. Those are reflected in Table-1. The factors indicated at how a PPP project manager’s actions may impact the corporate financial statements.

Table – 1 Interlinkages within Kazakhstan’s Finance Practices

|

No.

|

Actions of a PPP Project Manager

|

Impacts of Corporate Financial Statements

|

|

1.

|

Improves planning and project scheduling with the aim of narrowing down the time interval b/w money spent and money collected

|

Positively affects the cash flow statement

|

|

2.

|

Makes payment transactions on the project bills on the accrual basis only when actual payments are due, not earlier

|

Positively affects the cash flow statement allowing a corporate business using its cash available longer. This action positively affects the balance sheet

|

|

3.

|

Negotiates with creditors the extended terms of debt payment over the longer period

|

Positively affects the status of the current liabilities as they decrease and the long-term liabilities increase and tend depreciating with the passage of time. This action impacts financial ratios on both, the cash flow statement and the balance sheet

|

|

4.

|

Makes the targeted purchases only at times when these are needed by project works

|

Positively impacts the cash outflows as those are delayed in time for as long as possible. This action strengthens the JIT inventory system. The end impact is on both, the cash flow statement and the balance sheet

|

|

5.

|

Obtains the competitive contractor bids

|

Positively impacts the income statement in view of significant reductions in project expenses

|

|

6.

|

Obtains the timely trade discounts and seasonal easy terms of trade

|

Positively affects the cash flow statement by limiting the cash outflows whilst at the same time builds asset inventory. Since the asset inventory is reflected in the corporate balance sheet, this action equally affects the balance sheet

|

|

7.

|

Complies with high quality standards of the PPP project delivery

|

Positively affects the income statement and the cash flow statement since less money is spent on re-work and compensation of clients’ claims

|

|

8.

|

Provides activity-based calculations of the cost of inventory to reveal the hidden costs

|

Positively affects all three financial statements since this action provides a realistic estimate of cash outflows and allows the company to bill the PPP project clients against the relevant costs incurred by the project.

|

Based on the analysis and the survey of project managers and bank employees revealing how closely interrelated were the interlinkages between project finance and corporate finance practices, the following six findings have been found:

- The study found corporate finance practices, firmly footed in Kazakhstan. Moreover, those practices served as a jump-start for ambitious prospects for Astana, Kazakhstan’s capital city, to function as a regional financial hub in Central Asia. Global influential financial organizations support Kazakhstan’s regional good governance financial management efforts. In spite of a high stature of Kazakhstan’s corporate finance, the study found that project finance yet remains immature. It had no sufficient presence in the corporate accounting systems. Many fail to visualize the differences between corporate finance and project finance. In that regard, the study strongly recommended that potential PPP project managers produce the three generally accepted financial statements for each PPP project, along with the project finance statements. The study believed that handling PPP projects by using the earned value management (EVM) method, which is specific for PPPs, may be irrational. It would rather be proper to gradually integrate EVM within the financial information system. And also, to incorporate it in a company’s financial statements for decisionmaking on PPP projects.

- The study revealed that complexities associated with implementing project finance in Kazakhstan are linked to diverse tools in banking, each system having its own distinctively visible characteristics. Examples are Islamic Financing and Chinese financing modes the EU financial and accounting standards. Such background served the evidence that suggested using both the financing modes for PPP projects, project finance and corporate finance. The study confirmed that, in the long run, those two modes would eventually be merged, to intake the best of features of each. For the time being, the study affirmed that, in managing the PPP projects, the project finance is capable of creating a useful bridging link between the two financing modes.

- The survey, carried out by under this study, discovered views of Kazakhstan’s banking employees on the project finance. According to them, the EVM is a purely project management accounting method and, as such, it measures project performance by integrating project’s scope, schedule, and resources. The bank employees see it as the technique capable of functioning only when certain project accounting tools are in use and certain project-specific information softwares are applied. Specific features of the project finance, such as work breakdown structure, schedule, and budget allow tracking actual costs and accounting changes in projects. Without using those tools the EVM-derived calculations prove to be incomplete. According to the views of the local project managers, questioned in the course of Kazakhstan’s fora and conferences during 2016, the key deficiency of the project finance has turned out to be the ignoring of managerial preferences that are, in fact, the advantages of the corporate finance.

- Although EVM is widely spread at global scale, it is hardly known amongst Kazakhstan’s corporate businesses. The latters primarily rely on the corporate finance tools in their project estimates and assessments. To that effect, the study recommended that project management offices (PMOs) should be built within the organizational management systems of corporate businesses as well as of public sector entities. By definition, the PMOs, as high level decision-making authorities(Pulse of the Profession, 2013), would help integrate accounting data on project performance in the corporate finance information. Also, the study revealed that the role of PMOs will be indispensable in aligning the accounting data, generated by corporate finance, with that of project finance. The PMO will be critical in consolidating multiple project performance indicators in aligning them with the overall corporate income, cash flows statements, and balance sheet. Thus, the study suggested that PMOs may become critical in combining managerial preferences and strategic lookouts into the project-specific decisions. Because of the fact that each PPP project directly impacts a company’s financial health, the study recommended using the PMOs to create a bridging link between the project finance accounting procedures and a company’s corporate accounting systems, in line with global trends (Haas, 2009). The paper noted that the project finance-relevant expertise was unavailable in Kazakhstan. Against that background, the PMOs are indispensable especially in bringing the needed expertise and knowhow on the project finance to end users.

- The study found that financial tools, built in the projects feasibility studies, remain the viable levers for monitoring the PPP projects’ actual implementation over their life time.

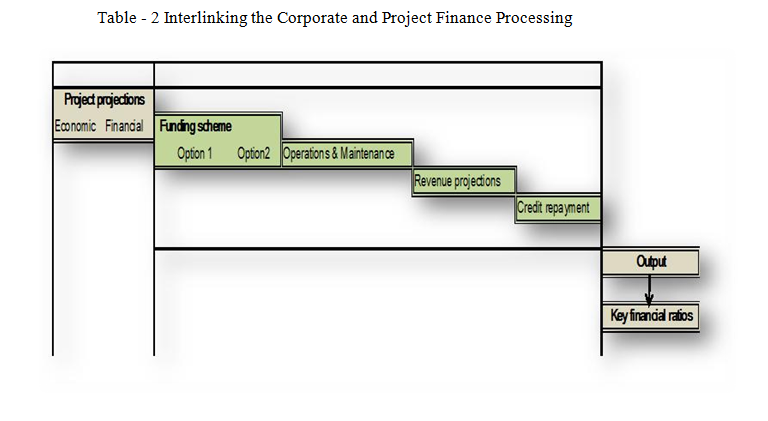

- The study observed that considering the project’s initial targets through the prism of the corporate and the project finance (taken together) would yield a different managerial decision on any given PPP project. That, compared to a decision adopted solely on the basis of the EVM-derived figures, had more rationale and a broader strategically corporate lookout on the projects performance. It is one additional argument in favor of using both the financing approaches, as shown in Table- 2.

Table - 2 Interlinking the Corporate and Project Finance Processing

Hypothesis 3-SPV is unnecessary for prospective project finance

In developing Kazakhstan’s finance model, the study noted the existence of governance inefficiencies on the project finance. In the view of project managers of the local PPPs, the establishment of SPVs may ensure easy terms for replacement of a project operator. Such substitution becomes possible because a credit agreement is finalized with the SPV, not the project operator. In reality, project finance, as supplemented by the SPV, turns out to be complimentary to a direct contracting. The notion of an SPV is often constrained by the incomplete financial and legal structures(Chowdhury, 2010). The latter is being widely used outside Kazakhstan but has not been duely accounted for in the country’s existing legislation. In July 2014, the concept of a direct agreement was initiated. That was a written agreement between a concessionaire and a creditor for a concession project. The need for creating the SPVs for the sole purpose of finalizing a project finance deal was thus admitted obsolete. To that end, a variety of new types of the concession agreements significantly expanded in the aftermath of newly modified legal instruments regulating implementations of concessions. Thus, the concession agreements have been streamlined along the following four major types:

- The concession agreement, stipulating the establishment of the concession facility by a concessionaire with subsequent transfer of concession facilities to state property;

- The concession agreement, stipulating joint activities of a concessionaire and a concession provider to build (rehabilitate) and operate a concession facility;

- The concession agreement, ensuring a transfer of state-owned concession facilities to a trust management or property lease (rent) of a concession provider or an authorized agent and the right of redemption of concession facility by a concession provider.

The investigation of the above new types of concession agreements discovered that they have been made legitimate. Moreover, the study revealed a series of faults in practicing the legal norms governing the concessions where the listings of investment projects, under the project finance mode, were, in fact, defined by government. The existing laws however do prescribe that such listings should be defined by the central executive authority that are in charge of state planning, under the condition that project facilities are registered as national property. That norm has also been true in the situations where ownership was vested with the regional legislative bodies, and cities of the republican scale, and also, municipal authorities. The above findings resonated with the thinking that the types of contract ownership can predict the future course of a project (Holmstrom, 1991), even if contractual provisions envision all possible variations in ownership and court enforcement as doable.

Based on the above findings, the study suggested that the act of defining the listings of state-funded investment projects should be carried out under the project finance mode (MOJ, 2013). Such practice should be assigned to the government in exclusive cases when a project is defined as one possessing a special value. In other instances, the act of defining the listings of projects, to be carried out under the project finance mode, should be assigned to the central executive authority in charge of state planning, provided that the releases of publicly-funded projects will have transferred to state property. Likewise, the regional legislative entities should define the listings of public investment projects, to be implemented under the project finance mode, in cases where such project releases are then transferred to the power of authority of the municipal utility services.

The study also found that Kazakhstan’s grantor may exit from project implementation any time, at a short notice received by a creditor 15 days prior to actually undertaking the exit. In this regard, a greater flexibility was granted to all parties of PPP projects. Thus, a concessions agreement was allowed to finalize a deal between all interested parties, to equally reflect their direct interests. The study identified major terms of such agreements. Those are as follows:

- a concessionaire has a right for substitution of a project operator

- a creditor has a right to appoint a temporary project operator

In view of above findings, the study recommended introducing a new norm within concessions-related laws. That norm shall have rectified the two major terms, as noted above. A new measure has entailed from a specific nature of Kazakhstan’s doing business practices, under the PPP projects framework, where the level of confidence amongst various partners remains low. The study wished to follow the global trends on investor confidence. According to the results of the 2012 World Bank survey of banks, Kazakhstan staged record NPL accumulations at 31% of the country’s total lending. In Ireland, Lithuania, and Greece the share of NPLs stood at 18.7%, 18%, and 17.2% of total lending (Vorotilov, 2013). According to Kazakhstan’s Forbes Magazine, foreign investors, in overall, lost nearly US $ 15 billion of which US$ 10 billion were lost due to inefficiencies of the BTA Bank, US$ 3 billion were lost to Alliance Bank, and US$ 1 billion to Astana Finance Bank (Amangeldy, 2014).

One of the key reasons behind such massive money loss was fraud. According to Kazakhstan’s independent expert view, an estimated 85% of frauds implied corruption at the senior level bank officials who had intentionally steered fraudulent banking operations while they were cognizant of implications. Amongst other causes, ineffective bank management on risks assessment attributed to the 15% share in the increase in NPLs. To remedy this, the National Bank of Kazakhstan (NBK) tightened its finance policies. The study found that on November 12, 2012 the NBK imposed limits on the size of owner capital of the second-tier banks where the underwritten debt threshold level was set at KZT5 billion from January 1, 2016. From January 1, 2017, the NBK announced the KZT 50 billion limit against owner capital of 30-50 billion KZT. In future, namely, in 2018, such requirements will reach the proportion of 75 vs. 50-75, and in 2018, 100 billion vs. 75-100 billion KZT. Fraud prevention measures will have resulted by year 2019 in the 10 times increases in the requirements to owner’s capitalization of the second tier banks. The NBK forecasts its near future credit policy to remain unchanged. That may signal of the low confidence between banks and businesses. From banking perspective, the project finance is currently not a rescue solution for supporting PPPs as creditors face the danger of higher risks. One of the prerequisites of project finance is the upfront pledge of the 25-30% of the total cost of project by a project initiator. Under Kazakhstan’s realities, a concessionaire has to put up at least 10% of the cost of the project. However, to obtain the trusted quality of project products, a concessionaire needs more capital, prior to project initiation.

The root cause of the low investor confidence was found to be weak institutional capacity in protecting the interests of PPP projects’ private parties. Here, the disputes on PPP projects are resolved in locally based civil courts while those of foreign partners fall under the jurisdiction of the international law. Kazakhstan’s residents are entitled to apply to tertiary courts to resolve private businesses’ disputes, however, those courts are in fact not authorized to handle cases where one of parties to PPP projects is state. Wherever state interests in court, the tertiary courts have no right to step in. The above noted evidences of institutional inefficiencies caused delays in PPP project implementation and financial losses. It is therefore that this paper suggested that the laws on tertiary courts should be substantially amended (Varnavskii, 2010) as well as on the law on international arbitrage, to enable sound project finance.

The study revealed that the role of the local special purpose project companies is such that project finance obligations are reflected on the balance sheets of neither concession arranger nor concessionaires thereby leaving their creditworthiness undisturbed. Project finance provided higher margins vs. corporate crediting. It ensured much higher average weighted cost of capital compared to net financing out of owner capital. The study observed that in spite that Kazakhstan’s medium-term PPP development program admitted the project finance as one of its major goals, this mechanism was not sufficiently practiced. No formal agreement on the project finance has pushed through to is fruition since 2012 although the legal framework for PPPs had been in place since long. In this regard, the paper noted urgency for new law enforcement measures on the project finance governance (MOJ, 2014). To that effect, the study found that application of the project finance, in practice, had the following four constraints:

- Lack of a creditor step-in- right to rescue the project. It lessens PPP projects’ bankability;

- Incompliances between the prescribed norms on establishing the SPV and those governing the LTDs or JSCs;

- Inability of second tier banks to join in the PPP agreements as a third party due to the constraints and barriers in the existing legislation;

- Uncertainties associated with transfer of rights in PPPs to government supported measures and state-granted compensation of project costs.

In view of the above constraints and complexities, the study suggested that the mandatory establishment of SPV in the PPP projects is unnecessary.

Hypothesis 4-project finance depends on the effective risk allocation

The study found that Kazakhstan’s private sector, although prepared to share its knowhow on identifying the public sector risks, had little or no past experiences on risk mitigation. To that effect, local businesses developed risk matrices for using them as instruments in gaining recognition as advisory on project management. The major constraint was admitted to be complexity of the project finance. The bulk of organizational structures, initially designed to handle project finance, were dissolved. Currently, the local banks continue loaning businesses under conventional financing schemes, not the project finance. The lack of project finance-specific skill amongst bank personnel was admitted a serious constraint. In this regard, the study recommended that the comprehensive system of risks allocation should be legitimized in Kazakhstan. Having conducted the survey of bank employees, the study attached preference to the application of the following five approaches in managing risks:

- Avoiding the risks that are undesirable for project participants;

- Allocating the risks by assigning the responsibility for its mitigation to the project party that is most capable of fulfilling the task at minimal costs;

- Neutralizing the risks by means of risk insurance, risk transfer, sponsor-backed up risk guarantees

- Acceptance of those risks that were missed being managed by a private party;

- Ensuring the contingencies for high-scored risks by budget funding required for repairs and debt servicing.

The extent of fiscal risks in the project finance depended on the fiscal institutions that configure the government’s decisions on PPPs. Example, the fiscal targets in PPP projects, including project budgeting procedures, the choice of accounting and auditing standards, assigning responsibilities for adopting fiscal decisions amongst diverse government agencies were the subject areas where the influence exerted by institutions could be strongly felt. Incentives of policymaking may be through rewards for minimizing short-term cash expenditures. Alternatively, decision-makers may be well rewarded for neutralizing fiscal vulnerabilities. Because the fiscal institutions essentially influence the diverse aspects relating to the PPP risks mitigation, the study suggested that strengthening of Kazakhstan’s fiscal institutions should be proceeded. It may help implement the project finance schemes efficiently and effectively. Based on the evidences, as described in this section, the structure of the financial model for Kazakhstan’s PPP projects may emerge, as reflected in Figure -2.

Figure-2 Kazakhstan’s PPP Project Finance Model

5.1 Discussion of Findings

The study’s initial question was to develop the project finance model for PPP projects. Based on the findings of the study as well as the data and information, financial worksheets, and projects’ banking transactions, the study found that processing of projects financial data and performance indicators should be based on input indicators and shall consist of processing of key indicators of costs assessment, risks allocation, to be supported by market analyses. All the above types of processing, under this paper-suggested project finance mode, should be strictly aligned with the project requirements that were initially set by stakeholders. The latters should be able to produce the pre-agreed variations in the output indicators at different stages of project implementation over the project’s life time. Continual flows-in and flows-out of the projects’ financial data and performance indicators should fill in the contents of the financial model as relevant to each of the individual PPP projects, of which the exact configurations should be clearly prescribed by relevant concessions agreement, specific for each individual PPP project.

Before releasing the output project performance indicators, the consolidated financial and project pro-forma report templates have to be sensitivity tested. The key financial ratios and formulae to be used by all project parties would need to be mutually agreed by all parties involved − to fully satisfy their project interests.

The study found that project projections would need to incorporate economic and financial forecasting. The funding schemes shall offer no less than two alternative options. Operations & maintenance & revenue projections shall be processed using both the corporate finance and the project finance. In all processing of calculations, the use of both the financing modes, the project finance and corporate finance shall be equally valid. For the output worksheets, prevalence will be after the corporate finance accounting procedures.

The paper discovered the root causes to failures in initiating the project finance. The lack of the long-term funding and complexities in practically applying the PPP financing modes have been identified as the key constraints. The most appalling constraint in implementing the project finance has been working environment in the financial sector where fraud and low managerial skill have been registered.

The study confirmed that the pattern of setting up the SPVs has not been followed for long. The reasons behind this have been the lack of clear rules of the game for diverse economic agents, private businesses, and investors as regards the SPVs. Conspicuous mismatches in the existing legislation as per the project finance and the PPPs schemes have been identified by the study. The study termed those as serious barriers in implementing the project finance. The improvements relating to the law on tertiary courts and on international arbitrage have been suggested to be taken into account when laying down the firm foundation for the PPP project finance development.

- Conclusion

The paper pursued the task of developing the PPP project finance model as relevant for a developing country, on the example of Kazakhstan. In its analyses, the paper looked at country’s PPP development program, various project financing modes, as practiced by the country’s public and private sector. Aspects relating to public projects implementation, interlinkages of financing modes in projects, financial policies, banking practices and specific aspects of the PPP projects, as relevant for this study, have been explored to develop the PPP project finance model.

The paper confirmed that project finance is dependable on the sound project performance at the background of Kazakhstan’s economic situation, which is sound, to accommodate the PPP project finance.

The study also confirmed that the local financial environment in Kazakhstan (driven by capacity of the National Bank of Kazakhstan) is mature for implementing the PPP project finance model.

The study admitted that the law enforcement measures relating to the PPP project finance have been immature, despite that the appropriate legal framework was long in place. Law enforcement practices relating to the project finance implementation however differed significantly, at spots.

The paper confirmed that financing of the PPP projects is a serious challenge faced by the country’s public and private sectors. The reputational risks entailing from inefficiencies in implementing the PPP project finance due to its novice nature are huge. The key factors that negatively influenced the ongoing PPP development were found to be: the diverse forms of ownership in PPPs and the lack of confidence amongst project parties.

The paper recommended that in the immediate future the country should sustain practicing the corporate finance mode whilst, parallel in time, it will have to implement the project finance mode.

Based on the finding of the study, the paper developed the project finance model as applicable to Kazakhstan and it may be used by developing countries.

Based on the conclusions of the study that confirmed by the hypotheses initially posted by the research, the paper recommended the following:

- The SPV may not be mandatory for the PPP project finance, wherever the concessions agreement is in place because the latter serves as an alternative tool.

- A specifically-tailored PPP finance model should be developed for each PPP project individually, to reflect all stakeholders’ interests and expectations of project outputs.

- Both of the financing modes, the corporate finance and the project finance should be applied in financing the PPP projects, for greater reliability.

The outcomes of this paper may be useful for diverse end-users, including project managers, banking employees, government agencies, policy makers, investors, regulators, academia, and students. They are also for the users of the KPPC network, in its capacity of the central project operator in Kazakhstan as well as of the lead regional think tank in Central Asia.

References

Amangeldy, S. (2014). National Bank of Kazakhstan to Increase the Minimum Capital Requirements. Halyk Finance, Issue of Sep. 4, 2014.

Bishimbayev, K. (2016, September 15). K.Bishimbayev presented the 2017-2021 socio-economic forecasts. Electronic Government RK: Astana. Retrieved from URL: http://government.kz/ru/novosti/1003872-k-bishimbaev-prezentoval-prognoz-sotsialno-ekonomicheskogo-razvitiya-strany-na-2017-2021-gody.html.

Bishimbayev, K. (2016, September 9). Positive Economic Growth Emerged. Kazinform: Astana. Retrieved from URL: http://government.kz/ru/novosti/1003739-nametilsya-polozhitelnyj-rost-ekonomiki-rk-kuandyk-bishimbaev.html/.

Chowdhury, A. &. Chen, P-H. (2010). Special Purpose Vehicle (SPV) of Public Private Partnership Projects in Asia and Mediterranean Middle East: Trends and Techniques. Int. J. of Institutions and Economics 2 (4), 64-88.

Crawford, L. M. et al. (2006). Practitioner development: from trained technicians to reflective practitioners. International Journal of Project Management, 2196), 443-448.

Dao, N. & Marisetty, V. (2017). Public Private Partnerships and Corporate Finance: Evidence from China and India. Brisbane, Australia: RMIT University, Financial Research Network (FIRN).

Dobbs, R. O. (2013). Reverse the curse: Maximizing the potential o fresource-driven economies. MsKensey Global Institute Report, 1-164.

Geraldi, J. (2008). The balance between order and chaos in multi-project firms: A conceptual model. International Journal of Project Management, 26(4), 348-356.

GIH. (2016). Allocating Risks in Public-Private Partnership Contracts, 1-267. Sydney, Australia: Global Infrastructure Hub Ltd.

Government. (2016). Expanded Cabinet Meeting of Sep. 9, 2016 chaired by Head of State. Akorda Press: Astana. Retrieved from URL: http://www.akorda.kz/ru/events/akorda_news/meetings_and_sittings/rasshirennoe-zasedanie-pravitelstva-pod-predsedatelstvom-glavy-gosudarstva.

Grimsey, D. L. (2004). Public Private Partnerships. Cheltenham: Edward Elga.

Grout, P. A. (1997). The economics of the private finance initiative. Oxford Review of Economics, 112 (4), 1126-61.

Haas, K. (2009). Managing complex projects: A New model. Management Concepts Inc. Vienna.

Hart, O. (2003). Incomplete contracts and public ownership: remarks, and an application to public–private partnerships. Economic Journal 113, 69-76.

Hart, O. S. (1997). The proper scope of government: theory and an application to prisons. Quarterly Journal of Economics, 112(4), 1126-61.

Holland, J. (2002). Complex adaptive systems and. spontaneous emergence. In Curzio, A. Q., & Fortis, M. (edited), Complexity and industrial clusters: Dynamics and models in theory and practice. Heidelberg: NY. Physica-Verlag.

Holmstrom, B. (1991). Multi-task principal-agent analyses: incentive contracts, asset ownership and job design. Journal of Law, Economics and Organization, VII, 24-56.

Jing-Feng Yuan, et al (2010). The driving factors of China's public-private partnership projects in metropolitan transportation systems: public sector's viewpoint. Journal of Civil s Engineering and Managment, 16 (1), 5-18.

Maher, D. (2016, May 20). Public-Prvate and the Future of American Infastructure. Erlangen, Germany: Siemens USA Newsroom.

MOJ. (2013). Law on Introducing Amendments and Modifications to Some Legal Acts on Issues of Implementing New Types of Public-Private Partnerships and Expanding the Areas of Application in the Republic of Kazakhstan. (M. o. Kazakhstan, Ed. July 4, 2013. www.adilet.kz): Astana.

MOJ. (2014). Law on Introducing Amendments and Modifications to Some Legal Acts on Issues of Public Management of the Republic of Kazakhstan. (M. p. Kazakhstan, Ed. July 2, 2014. www.adilet.kz): Astana.

Nazarbayev, N. (2013). Akorda. Statement of 23 May 2013 by President of Republic of Kazakhstan at VI Astana Economic Forum, 1-3. Akorda Press: Astana.

Peterson, O. (2010). Emerging meta-govenrnance as a regulation framework for public-private partnerships: an examination of the European Union's approach. International Public Management Review, 11 (3), 1-21.

PMI (2013). The impact of PMOs on strategy implementation. (In-depth Report), The PMI's Pulse of the Profession, Nov., 1-18.

Sharma, R. (2015). The Fourth Model of Institutional Investment - The 'Collaborative' Model. Stanford GLobal Projects Center: Stanford, California, USA. SU Projects Center. Tetrieved from URL: https://gpc.stanford.edu/gpcthinks/fourth-model-institutional-investment.

Sinha, R. (2011). Financier’s Perspective: Financial Operation and Risk Mitigation for BOT/PPP Projects for Infrastructure. (IFC, Ed., & IFC, Compiler): USA. Retrieved from URL:http://www.ifc.org/wps/wcm/connect/e4675d004a1ad38b9f809f02f96b8a3d/Financier%2527s%2BPerspective%2B110801_sinha.pdf?MOD=AJPERES/.

Tvarno, C. &. Osteergard, K. (2013). PPP vs PPPP. What is wrong in Denmark? Copenhagen Business School PPP Conference Paper: Vancouver. 1-16.

UNECE. (2008). Practical Guide on PPPs. Practical Guidance on the Issues of Effective Management in the area of Public-PRivate Partnerships. UNECE Compiler Geneva, Switzerland: UN Economic Commission for Europe.

US Dep. Trans. (2012). Risk Assessment for Public-Private Partnerships: A Primer, 1-44. (F. H. Adm., Compiler).

Varnavskii, V. (2010). Public-Private Partnership: theory and practice. Gosudarstvenno-chastnoe partnerstvo:teoria i praktika: Moscow. (Москва: ГУ-ВШЭ).

Vorotilov, A. (2013). Kazakhstan - Champion on NPL. Forbes-Kazakhstan, Issue of September 17, 2013.

Yehoue, E. P. (2013). The Routeledge Companion to the Public-Private Partnerships. 1-482. Routeledge.

Yescombe, E. (2007). Public-Private Parterships. Principles of Policy and Finance, 4-369. London, UK: Yescombe Consulting Ltd.