A Refereed Monthly International Journal of Management

Z-Score Analysis on Efficiency of Working Capital Management: An Evidence of Select Indian Food Processing Companies Listed In NSE

Author

ABSTRACT

Working capital management is a very important component of corporate finance as well as essential for manufacturing sector because it directly affects the liquidity and profitability of the company. It deals with current assets and current liabilities. There are two concepts of working capital viz. quantitative and qualitative. Some people also define the two concepts as gross concept and net concept. This preliminary study was made with an attempt to analyze the Altman’s Z-Score on efficiency of working capital management i.e. Discriminant Analysis for a time horizon of 5 years with respect to the select Indian Food Processing companies which are listed in National Stock Exchange (NSE). The secondary data have been used for analysis which is driven from some Database as well as Annual Report of the companies. A sample of 14 select Indian Food Processing Companies listed in NSE have been taken for testing the efficiency. After the study the result found majority of select companies are fail to maintain their liquidity ratios and for the reason companies are in risk zone as per z-score analysis. This paper has been divided into four major segments namely Introduction, Methodology, Main Findings and discussion and finally Suggestions and Conclusion.

KEYWORDS: Working Capital Management, Z-Score Analysis, Food Processing Companies, NSE.

Research Scholar, Dept. of Commerce, AMU Aligarh, E-mail Id: mahendvi.rs@amu.ac.in, Cont. No. 91+9756111122.

Introduction

Working Capital is a capital who work like an active guard for a business enterprises to meet the day by day business expenses at any circumstances but the capital must be adequate. The maintenance of Working capital in a business enterprises is mandatory because it plays an important role like a role of blood in a body. It is very necessary to maintain adequate capital because if insufficient capital can harm or fail to meet the obligation of the business enterprise. The same way extra capital can also unable to achieve the objectives of the business. So it is mandatory to arrange the adequate capital. Although it is important for every sector of the business somewhere less or somewhere more but in one of the sector called manufacturing sector of business where the capital is required for purchasing raw material from different places or different suppliers who want to receive cash or chequeetc or unable to trade in credit is most significant to arrange the working capital and manage them in an adequate manner. This study will try to examine or test the management of working capital of Indian food Processing companies of manufacturing sector. The Indian food and grocery market is the sixth largest market of the world, with 70% approx. contribution of retail of the sales.The Indian food and grocery market is the world’s sixth largest, with retail contributing 70 per cent of the sales. As per the information of “India Brand Equity Foundation” The Indian food processing industry accounts for 32 per cent of the country’s total food market, one of the largest industries in India and is ranked fifth in terms of production, consumption, export and expected growth. It contributes around 14 per cent of manufacturing Gross Domestic Product (GDP), 13 per cent of India’s exports and six per cent of total industrial investment. Indian food service industry is expected to reach US$ 78 billion by 2018. The food Processing Industry is working hard to achieve the target of highest rank in the world but it is necessary to work collectively in a right path for the achievement and for the achieving the objectives, the business must have maintain their performance where working capital is also an element for success. The author in this study has opted 14 companies of Indian food Processing Industry with five years of financial data and will try to check the efficiency of working capital and its financial constraints.

Working Capital and its Management

It is a measure of both a company's efficiency and its short-term financial health. Working Capitals are used for carrying out the routine or regular business operations consisting of purchase of raw materials, payment of direct and indirect expenses, carrying out of production, investment in stocks and stores. It can also be regarded as that proportion of the company’s total capital, which is employed in short term operations. It is not necessary that the amount is always available in the form of cash. It can take the form of near cash assets or even assets a little further from cash, but yet in the process of moving towards the cash form in a short period. The study of working capital management occupies an important place in financial management. It has never received so much attention as in recent years. Working capital management is an integral part of overall financial management. The sphere of working capital throws a welcome challenge and opportunity to a financial manager. “Working capital management has been looked upon as the driving seat of financial manager.” The management of working capital is synonymous with the management of short term financial liquidity. The importance of short term liquidity can best be gauged by examining the repercussions which stem from a lack of ability to meet short term obligations. A lack of liquidity implies a lack of freedom of choice as well as constraints on management’s freedom of movement. If lack of liquidity continues to be a problem, it may ultimately lead to insolvency and bankruptcy. Thus working capital management is linked with the continuous existence of an enterprise. Regardless of excellent products, effective marketing, efficient production, and wise fixed assets management. Many management has lost the control of its firm because liquidity crisis resulted in takeover by creditors, forced merger or bankruptcy. An excellent long run outlook for a business becomes immaterial if control is lost in the short run. Working capital policies affect marketing, personnel, production and what happens in the business related to working capital decisions. Working capital management as an area is concerned with carrying out working capital functions. In any enterprise, the working capital function must exist in some form or other.

Brief of Food Processing industry in India

The Indian food industry is poised for huge growth, increasing its contribution to world food trade every year. In India, the food sector has emerged as a high-growth and high-profit sector due to its immense potential for value addition, particularly within the food processing industry.

According to the data provided by the Department of Industrial Policies and Promotion (DIPP), the food processing sector in India has received around US$ 6.82 billion worth of Foreign Direct Investment (FDI) during the period April 2000-March 2016. The Confederation of Indian Industry (CII) estimates that the food processing sectors have the potential to attract as much as US$ 33 billion of investment over the next 10 years and also generate employment of nine million person-days.

India is known as agricultural land and more than 60% Approx is full of cultivated land and so many organization are set here to manage this business like The Agricultural and Processed Food Products Export Development Authority (APEDA) was established by the Government of India under the Agricultural and Processed Food Products Export Development Authority Act passed by the Parliament in December, 1985. The work have assigned to manage by this organization is development of industries relating to the scheduled products for export by way of providing financial assistance or otherwise for undertaking surveys and feasibility studies, participation in enquiry capital through joint ventures and other reliefs and subsidy schemes. APEDA is mandated with the responsibility of export promotion and development of the scheduled products like Fruits Vegetables and their Products, Meat and Meat Products,Poultry and Poultry Products,Dairy Products. Confectionery, Biscuits and Bakery Products, Honey, Sugar Products,Cocoa and its products, chocolates of all kinds,Alcoholic and Non-Alcoholic Beverages, Cereal and Cereal Products. Groundnuts, Peanuts and Walnuts,Pickles, Floriculture and Floriculture Products,Herbal and Medicinal Plants.

Review of literature

There are too many research on working capital management in different sector by different authors. In some of the Research has been reviewed and demonstrated below:

Baños-Caballero, S.,et.al(2014) in their paper titled “Working Capital Management, Corporate Performance and Financial Constraints” propounded from the sample of non-financial UK companies with help of panel data that an inverted U-shaped relation between Working Capital and Corporate Finance, which implies that there existed an optimal level of investment in working capital that balances costs and benefits and maximizes a firm's performance. They have also tested financial constraint of the companies and found that theoptimum was lower for firms more likely to be financially constrained.

Reddy, D. et.alin their research paper entitled “ financial status of select Sugar manufacturing units –Z-score model” tested the financial distress of the some select companies and found constrained and the reason showed the liquidity, working capital efficiency and the solvency position was not good.

Dr. seemahuda analyzed Altman’s Z-score analysis in the paper “Z-Score Analysis of Co-operative Sugar Mills in Haryana” and suggested to the co-operatives to manage their quality and liquidity. Although the period had been taken 10 years and it had been also suggested to the state government to take care of the co-operatives because they all were found financially distressed.

Sharma, A. K., et.al (2011). Their aim of this article was to examine the effect of working capital on profitability of Indian firms. They collected data about a sample of 263 non-financial BSE 500 firms listed at the Bombay Stock (BSE) from 2000 to 2008 and evaluated the data using OLS multiple regression. The findings of their study significantly departed from the various international studies conducted in different markets. The results reveal that working capital management and profitability was positively correlated in Indian companies. The study further reveals that inventory of number of days and number of days accounts payable were negatively correlated with a firm’s profitability, whereas number of days accounts receivables and cash conversion period exhibit a positive relationship with corporate profitability.

Vahid,T. K., Elham, G.,et.al. This research studied the effect of working capital management over the performance of firms Listed in Tehran Stock Exchange (TSE). Average Collection Period (ACP), Inventory Turnover (ITR) in days, Average Payment Period (APP), Cash Conversion Cycle (CCC), and Net Trading Cycle (NTC) were used to assess working capital management, and Net Operating Profitability was used to assess firms' performance. The study’s findings of the 50 different companies during the time period between 2006 and 2009 by using a multi-regression model showed that there was a negative and significant relationship between the variables of ACP, ITR in days, APP, NTC and the performance of firms Listed in Tehran Stock Exchange (TSE). There were no evidences to prove the existence of a significant relationship between Cash Conversion Cycle and the company's performances (NOP). The results also showed that the increase in Collection Period, Payment Period, and Net Trading will lead towards the reduction of profitability in the company.

Dhaliwal, N. K., & Kaur, J. examined in the paper entitled “Financial analysis of co-operative marketing federations--a comparative study of MARKFED and HAFED” .The co-operative marketing societies occupied a pivotal place in the agricultural marketing system of India. In the states of Punjab and Haryana, The Punjab State Cooperative Supply and Marketing Federation (MARKFED) and The Haryana State Cooperative Supply and Marketing Federation (HAFED) were playing an important role in building a unified structure for remunerative agricultural marketing. The paper attempted to undertake a comparative financial analysis of the MARKFED and the HAFED and examined their financial health. This study was based on secondary data covering period from 2000-01 to 2010-11. The analysis had been done on the basis of various indicators using tools like averages, standard deviation, co-efficient of variation, T-test and Z-score analysis. The study found significant differences in the financial position of MARKFED and HAFED. The MARKFED was more concerned towards day to day working of the federation whereas the HAFED concentrated more on maintaining assets for the future. The study concluded that the financial condition of MARKFED was better than that of HAFED. But both the federations needed to pay attention towards their financial condition and take effective measures.

There are many other literatures for testing the linkage of working capital and corporate finance, working capital and profitability and many more. The literature also showed the financial constraints of the listed or non-listed, financial or non- financial and many more companies and somewhere found positive linkage and somewhere found negative. Many of the author showed the liquidity performance, solvency and activity performance was not in a good condition.

In this research the author will try to find the linkage of working capital effectiveness on liquidity and activity and also try to examine the financial constraint of the select 14 companies through Altman’s Z-score Analysis.

Need of the study

Although the above reviews have showed the significance of the measurement of financial distress as well as linkage of working capital management with corporate performance. This study will also work for evaluation of linkage between Efficiency of Working Capital Management through liquidity and activity performance of the select Indian Food Processing Companies Listed in NSE and its financial constraint with the help of Altman’s Z-score analysis.

Objectives of the study

- To study the Liquidity performance of the select Companies.

- To study the working capital efficiency of the select Companies.

- To carry out Z-Score i.e. Discriminant Analysis for a time horizon of 5 years (i.e. 2011-2015) with respect to the selected Indian Food Processing companies which are listed in NSE

- To suggest the measures to improve Working Capital Management of the firm under the study.

Sources of Data

The present study is descriptive and analytical in nature based on secondary data collected from financial reports of the select Food Processing Companies available on their official websites. The period selected from the study is ranging from 2011 to 2015. The companies have been select which is listed in National Stock Exchange (NSE). The top 100 companies have been drawn for the study but only 14 companies have been select for the study on the basis of availability of data, on the basis of food processing products, although most of the companies who have been select, manufacture other products too but their major trade is to product of processed food. The Hind Industries Limited (HIL) has been taken on basis of meat processing companies listed in NSE because of the other 13 companies are not in a business of processing meat. The companies select for study are Nestle India Limited, Britannia Industries Limited, Kwality Ltd. , GlaxoSmithKline PLC, KRBL limited, Heritage Foods Limited, REI Agro Limited, LT Foods Limited, Usher Agro Limited, Kohinoor Foods limited,Prabhat Dairy Limited, SKM Egg Product export (India) Limited, ADF Foods Limited and Hind industries Limited.

Research Methodology

Ratio Analysis has been conducted using Current Ratio (CR) and Quick Ratio (QR) as a measure of Liquidity,Inventory Turnover Ratio (ITR)and Debtor Turnover Ratio (DTR) as a measure of Working Capital Efficiency Test. And Z-Score Analysis model for testing the bankruptcy of the Companies have been used as measure of solvency Test.

Liquidity test and its interpretation

Liquidity values of the Select Companies

|

S.NO.

|

COMPANIES

|

2011

|

2012

|

2013

|

2014

|

2015

|

|

CR

|

QR

|

CR

|

QR

|

CR

|

QR

|

CR

|

QR

|

CR

|

QR

|

|

01.

|

Nestle India Limited

|

0.88

|

0.38

|

1.31

|

0.65

|

1.71

|

1.16

|

1.45

|

0.83

|

1.68

|

1.12

|

|

02.

|

Britannia Industries Limited

|

1.54

|

0.86

|

0.88

|

0.49

|

0.82

|

0.44

|

0.90

|

0.51

|

1.19

|

0.90

|

|

03.

|

Kwality Ltd.

|

1.34

|

1.18

|

1.33

|

1.16

|

1.31

|

1.19

|

1.30

|

1.15

|

1.42

|

1.18

|

|

04.

|

GlaxoSmithKline PLC

|

1.42

|

1.19

|

1.85

|

1.41

|

1.81

|

1.45

|

1.90

|

1.59

|

1.83

|

1.53

|

|

05.

|

KRBL limited

|

1.26

|

0.55

|

1.30

|

0.70

|

1.38

|

0.74

|

1.43

|

1.18

|

1.49

|

0.83

|

|

06.

|

Heritage Foods Limited

|

0.66

|

0.32

|

0.68

|

0.25

|

0.73

|

0.32

|

0.78

|

0.33

|

0.87

|

0.30

|

|

07.

|

REI Agro Limited

|

1.59

|

0.59

|

1.48

|

0.59

|

1.31

|

0.43

|

1.02

|

0.50

|

0.18

|

0.14

|

|

08.

|

LT Foods Limited

|

1.07

|

0.34

|

1.05

|

0.44

|

1.06

|

0.40

|

1.09

|

0.36

|

1.07

|

0.46

|

|

09.

|

Usher Agro Limited

|

1.44

|

0.66

|

1.42

|

0.67

|

1.39

|

0.61

|

1.27

|

0.46

|

1.22

|

0.49

|

|

10.

|

Kohinoor Foods limited

|

1.10

|

0.27

|

1.21

|

0.30

|

1.17

|

0.25

|

1.24

|

0.29

|

1.15

|

0.21

|

|

11.

|

Prabhat Dairy Limited

|

0.88

|

0.73

|

0.81

|

0.67

|

0.81

|

0.58

|

0.61

|

0.45

|

1.25

|

1.09

|

|

12.

|

SKM Egg Pro.Ex.(India) Ltd.

|

0.57

|

0.19

|

0.33

|

0.11

|

0.11

|

0.02

|

0.09

|

0.02

|

0.05

|

0.02

|

|

13.

|

ADF Foods Limited

|

5.19

|

4.04

|

2.95

|

2.35

|

3.01

|

2.48

|

3.45

|

2.76

|

4.70

|

3.69

|

|

14.

|

Hind industries Limited.

|

1.23

|

0.72

|

1.80

|

1.05

|

1.58

|

0.88

|

1.45

|

0.83

|

1.32

|

0.58

|

Interpretations

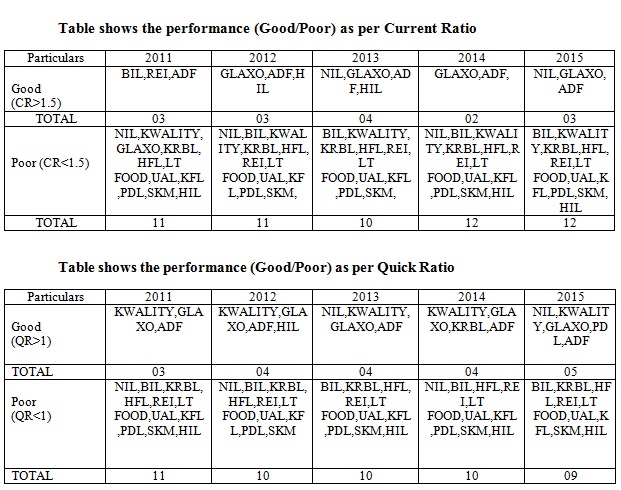

Liquidity value of select Companies have been done it showsmost of the companies except ADF Foods Limited have not enough current assets to pay-off of their current liabilities. This shows that the companies are leveraged and risky. SKM Egg Ltd. has only enough Current Assets to pay off less than 25% of his current liabilities. This shows that SKM Egg is highly leveraged and highly risky. It would be very difficult to get loan from Bank because the Banks prefer current ratio at least 1 or 2. The investors will not show their interest to invest. If we talk about Quick Ratio, so the quick ratio is an indicator of a company’s short-term liquidity. The quick ratio measures a company’s ability to meet its short-term obligations with its most liquid assets. For this reason, the ratio excludes inventories from current assets. Thus a quick ratio of 1.5 means that a company has 1.50 of liquid assets available to cover each 1 of current liabilities. The higher the quick ratio, the better the company's liquidity position. Here, most of the companies except ADF Food limited are not in a position of pay their current liabilities of quick ratio 1. In this 14 select companies only one company’s liquidity is good and rest of companies are fail to maintain their Current and Quick Ratio. Though these ratios play a significant role in a business to meet the short-term obligations.

Working Capital Efficiency test and its interpretation

W.C. Efficiency values of the Select Companies

|

S.NO.

|

COMAPANIES

|

2011

|

2012

|

2013

|

2014

|

2015

|

|

ITR

|

DTR

|

ITR

|

DTR

|

ITR

|

DTR

|

ITR

|

DTR

|

ITR

|

DTR

|

|

01.

|

Nestle India Limited

|

10.24

|

84.10

|

11.18

|

82.12

|

12.37

|

105.92

|

11.67

|

107.49

|

9.96

|

92.11

|

|

02.

|

Britannia Industries Ltd.

|

13.57

|

87.31

|

13.01

|

90.94

|

16.94

|

80.89

|

70.19

|

96.44

|

20.8

|

115.1

|

|

03.

|

Kwality Ltd.

|

25.36

|

4.78

|

24.25

|

4.48

|

37.42

|

4.65

|

27.33

|

4.30

|

19.9

|

4.48

|

|

04.

|

GlaxoSmithKline PLC

|

8.69

|

57.62

|

7.87

|

36.93

|

9.11

|

30.10

|

12.63

|

23.64

|

9.72

|

14.06

|

|

05.

|

KRBL limited

|

1.28

|

10.91

|

1.32

|

8.65

|

1.65

|

9.81

|

1.65

|

11.77

|

1.68

|

10.47

|

|

06.

|

Heritage Foods Limited

|

16.59

|

82.68

|

14.91

|

108.7

|

19.51

|

121.9

|

15.86

|

108.7

|

14.9

|

101.5

|

|

07.

|

REI Agro Limited

|

1.04

|

3.81

|

1.13

|

3.45

|

1.09

|

3.90

|

1.38

|

2.25

|

7.09

|

1.04

|

|

08.

|

LT Foods Limited

|

1.51

|

6.13

|

1.97

|

4.45

|

2.62

|

6.23

|

2.68

|

6.8

|

2.77

|

8.18

|

|

09.

|

Usher Agro Limited

|

2.47

|

5.71

|

2.56

|

4.79

|

2.32

|

4.24

|

2.16

|

4.85

|

1.85

|

4.15

|

|

10.

|

Kohinoor Foods limited

|

1.18

|

5.28

|

1.13

|

5.05

|

1.17

|

6.49

|

1.16

|

5.86

|

1.10

|

4.92

|

|

11.

|

Prabhat Dairy Limited

|

23.08

|

14.60

|

38.25

|

16.32

|

36.58

|

18.17

|

41.12

|

24.25

|

36.4

|

16.07

|

|

12.

|

SKM Egg PEx.Ltd.

|

1.45

|

5.02

|

2.14

|

6.05

|

0.74

|

2.42

|

0.27

|

1.83

|

0.39

|

1.36

|

|

13.

|

ADF Foods Limited

|

8.23

|

7.91

|

6.46

|

4.98

|

6.42

|

4.32

|

6.42

|

4.61

|

6.36

|

5.07

|

|

14.

|

Hind industries Limited.

|

3.76

|

5.23

|

3.60

|

4.11

|

3.54

|

3.78

|

3.28

|

3.18

|

1.14

|

1.53

|

Interpretation:

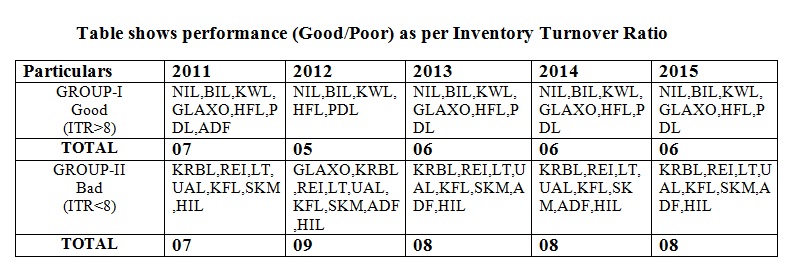

Inventory turnover is a measure of how efficiently a company can control its merchandise, so it is important to have a high turn. This shows the company does not overspend by buying too much inventory and wastes resources by storing non-salable inventory. It also shows that the company can effectively sell the inventory it buys. Following is the table shows how the enterprises are efficient to manage their inventory in one turn. Although higher turn shows the good efficiency of turnover but in this paper the authors assume 8 times and more turnover is like to good turnover.

This table shows the result of inventory turnover ratio of the select companies. More than half of the select companies are able to turnover their inventory more than 8 times in a year.

Debtor Turnover Ratio

Debtor turnover ratio is an efficiency ratio or activity ratio that measures how many times a business can turn its accounts receivable into cash during a period. In other words, Debtor turnover ratio measures how many times a business can collect its average accounts receivable during the year. This ratio shows how efficient a company is at collecting its credit sales from customers. Some companies collect their receivables from customers in 90 days while other take up to 6 months to collect from customers. In this paper almost all the company are efficiently able to manage their collection policy from the customers between these periods.

Solvency Test and its interpretation

Altman’s Z-score Analysis

The Altman Z-score is the output of a credit-strength test that gauges a publicly traded manufacturing company's likelihood of bankruptcy. The Altman Z-score is based on five financial ratios that can be calculated from data found on a company's annual report. It uses profitability, leverage, liquidity, solvency and activity to predict whether a company has a high degree of probability of being insolvent.The number produced by the model is referred to as the company's Z-score, which is a reasonably accurate predictor of future bankruptcy. The model is (For Private Firm) specified as:

0.717A + 0.847B + 3.107C + 0.420D+ 0.998E

Where:

Z = Score, measures the values of Bankruptcy of the Firms

A = Working Capital/Total Assets, Measures liquid assets in relation to the size of the company.

B = Retained Earnings/Total Assets,Measures profitability that reflects the company’s age and earning power.

C = Earnings before Interest & Tax/Total Assets, Measures operating efficiency apart from tax and leveraging factors. It recognizes operating earnings as being important to long-term viability.

D = Market Value of Equity/Total Liabilities, Adds market dimension that can show up security price fluctuation as a possible red flag.

E = Sales/Total Assets, Standard measure for total asset turnover (varies greatly from industry to industry).

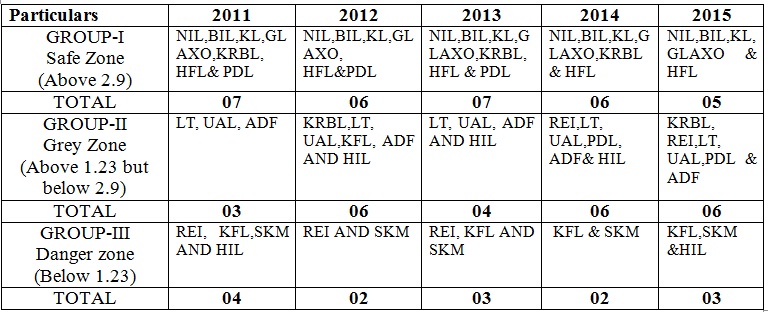

Zones of Discrimination:

IfZ-score values of a firm is more than 2.9 then the firm comes under safe zone. If Z-score values of a firm is more than 1.23 but less than 2.9 then the firm comes under Grey Zone and needs to improve. If Z-score values of a firm is below 1.23 then the firm is financially distressed and probability of shutdown is high so the firm needs to changes in their financial structures or needs to make some strong strategy for the business.

Z-Score values of the Select Companies

|

S.NO.

|

COMAPANIES

|

2011

|

2012

|

2013

|

2014

|

2015

|

|

01.

|

Nestle India Limited

|

17.66

|

14.38

|

11.94

|

14.88

|

13.18

|

|

02.

|

Britannia Industries Limited

|

21.76

|

19.70

|

20.12

|

19.10

|

15.27

|

|

03.

|

Kwality Ltd.

|

05.31

|

04.53

|

04.45

|

04.20

|

04.12

|

|

04.

|

GlaxoSmithKline PLC

|

14.43

|

13.41

|

11.99

|

10.81

|

08.89

|

|

05.

|

KRBL limited

|

03.01

|

02.80

|

03.24

|

02.90

|

02.75

|

|

06.

|

Heritage Foods Limited

|

03.59

|

04.28

|

05.47

|

05.30

|

05.43

|

|

07.

|

REI Agro Limited

|

01.15

|

01.02

|

00.97

|

02.50

|

02.09

|

|

08.

|

LT Foods Limited

|

01.27

|

01.34

|

01.82

|

01.97

|

01.79

|

|

09.

|

Usher Agro Limited

|

01.52

|

01.59

|

01.48

|

01.46

|

01.29

|

|

10.

|

Kohinoor Foods limited

|

01.11

|

01.76

|

01.14

|

01.15

|

00.86

|

|

11.

|

Prabhat Dairy Limited

|

04.03

|

03.53

|

03.57

|

02.81

|

02.73

|

|

12.

|

SKM Egg Product Ex.(India) Ltd.

|

-00.44

|

-00.18

|

-01.31

|

-01.14

|

-01.48

|

|

13.

|

ADF Foods Limited

|

02.15

|

01.78

|

01.73

|

01.72

|

01.80

|

|

14.

|

Hind industries Limited.

|

01.22

|

01.39

|

01.42

|

01.30

|

00.46

|

Table shows performance (Good/Poor) as per Z-Score Analysis

Interpretations

In this study, Z-Score analysis has been successfully done of the 14 select companies listed in NSE and the result found that the above five companies i.e. Nestle, Britannia, kwality, GlaxoSmithKline and Heritage are successfully crossed safe Zone. They are not financially distressed. KRBL and Prabhat are also not in a position of financially constraints but they are fluctuating on the border of the safe zone and fully crossed gray Zone. Though these two companies need to work maintain their liquidity or need a minor changes in their business strategy. Rest of the company i.e.REI AGRO,KOHINOOR (KFL) SKM & HIL are financially distressed. They need major changes in their business because of their illness management of liquidity, Activity ratio.

Conclusion

The study has been completed and it shows the result that some of the select companies are financially unconstraint. These result has been found after the analysis of liquidity test with help of two important variables Current ratio and Quick ratio, Working Capital Efficiency Test with variables Inventory Turnover ratio And Debtor Turnover ratio and Solvency Test with Z-Score Analysis. The study also reveals that majority of the companies are fail to manage their liquidity proportion and they are also fail to manage their inventory turnover although all are succeeded to maintain their account receivables. If we talk about the inventory of the firm, it is evident that the companies cannot afford to ignore the inventory turnover ratio. While analyzing this ratio, it is imperative that you keep a lot of factors in mind. A lower inventory turnover ratio certainly needs to be improved. However, an excessively high turnover ratio is also not a healthy sign for the company.

Suggestions

The author would like to suggest all the company in terms of liquidity to increase their current assets for pay off the liabilities. There are some suggestive measures for improving the financially constraint:

- Pay off Current Liabilities: it is not only does the current ratio depend on current assets, it is equally dependent on the current liability which is the denominator. They should be paid off as often and as early as possible. It would decrease the level of current liabilities and therefore, improve the current ratio.

- Sell-off Unproductive Assets: Cash level can be increased by selling unused fixed assets.

- Improve Current Asset by Rising Shareholder’s Funds: When the current assets are financed by equity rather than the creditors, the level of current assets would increase with current liabilities remaining the same.

- Sweep Bank Accounts: Sweeping is a facility by which excess fund are transferred from current account to another account which fetches interest on that fund. At the same time, these funds are available to use when required.

There are several ways in which the inventory turnover ratio can be improved by reducing the price of the products, improving the sales, by better forecasting, better inventory price, reduce purchase quantity etc.

References:

- Altman, E. I. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy.The journal of finance,23(4), 589-609.

- Altman, E. I. (2000). Predicting financial distress of companies: revisiting the Z-score and ZETA models.Stern School of Business, New York University, 9-12.

- Annual report of the companies from their authentic websites

- Asgharian, A., Dadashi, I., &Aghajan, A. A. P. (2015). The Investigating of the Relation between Working Capital and Performance with Considering Financial Constraints in TSE.

- Baños-Caballero, S., García-Teruel, P. J., &Martínez-Solano, P. (2014). Working capital management, corporate performance, and financial constraints.Journal of Business Research,67(3), 332-338.

- Brigham, E. F., Gapenski, L. C., &Ehrhardt, M. C. (1998).Financial Management; Theory and Practice (Book and diskette package). Harcourt College Publishers.

- Dhaliwal, N. K., & Kaur, J. (2014). Financial analysis of co-operative marketing federations--a comparative study of MARKFED and HAFED.Abhigyan,32(1), 52-64.

- Graziano, A. M., &Raulin, M. L. (1993).Research methods: A process of inquiry. HarperCollins College Publishers.

- http://apeda.gov.in/apedawebsite/index.html

- http://www.cii.in/

- http://dipp.nic.in/English/default.aspx

- http://www.defaultrisk.com/pa_score_14.htm

- http://www.ibef.org/industry/indian-food-industry.aspx

- https://galihandrianto.wordpress.com/2012/09/14/z-score-and-zeta-models/

- Huda,S.(2013). Z-Score Analysis of Co-operative Sugar Mills in Haryana. International journal Research Journal 51(5)

- Kumar, S., &Phrommathed, P. (2005).Research methodology(pp. 43-50). Springer US.

- Mehta, D. R. (1974).Working capital management. Prentice Hall.

- Padachi, K. (2006). Trends in working capital management and its impact on firms’ performance: an analysis of Mauritian small manufacturing firms.International Review of business research papers,2(2), 45-58.

- Reddy, D. N. R., & Reddy, K. H. P. (2012). Financial status of select sugar manufacturing units z-score model.International Journal of Marketing Financial Services and Management Research, (4).

- Saunders, A., & Allen, L. (2010).Credit risk management in and out of the financial crisis: new approaches to value at risk and other paradigms(Vol. 528). John Wiley & Sons.

- Scott, W. R. (1997).Financial accounting theory(Vol. 2, No. 0, p. 0). Upper Saddle River, NJ: Prentice hall.

- Sharma, A. K., & Kumar, S. (2011). Effect of working capital management on firm profitability empirical evidence from India.Global Business Review,12(1), 159-173.

- Trivedi, J. C. A Z-Score Analysis on Working Capital Management Of The Selected Listed Cement Indian Companies.

- Vahid, T. K., Elham, G., khosroshahi Mohsen, A., &Mohammadreza, E. (2012). Working capital management and corporate performance: evidence from Iranian companies.Procedia-Social and Behavioral Sciences,62, 1313-1318.

- White, G. I., Sondhi, A. C., & Fried, D. (2003).The analysis and use of financial statements(Vol. 1). John Wiley & Sons.