A Refereed Monthly International Journal of Management

Author

|

Name of Corresponding Author (s) Babita Kundu

Designation: Senior Research Fellow

Affiliation Babita Kundu, Senior Research Fellow, Department of Accountancy & Law, Faculty of Commerce, Dayalbagh Educational Institute, Agra.

Residential address with Pin Code Babita Kundu, H.No. 36, JeevanJyoti Enclave, Dayalbagh, Agra – 282005

Mobile Number(s) 8755590361

E-mail Address: babita81k@gmail.com

View Corporate Social Responsibility through Companies Act 2013-A Study of Selected Maharatna companies

|

Abstract

With the introduction of Companies act 2013, it is a new era for corporations to fulfil its social obligation. There are several new provisions introduced in Companies act and one of such new provision is about corporate social responsibility (CSR). CSR has been applicable from 1 April 2014 as mandatory contribution for such company which has net worth of Rs.500 cr. or more OR net turnover of Rs. 1000 cr. or more OR net profit of Rs. 5 cr. or more during any financial year. This study presents a view on CSR as per Companies Act 2013. In India, Public sector has played a major role in industrial and economic development and having significant share in gross domestic product. Role of some public sector companies especially Maharatna, Navratna and Miniratna is well acknowledged in the economic development. They are having strong financial results which guide the Indian economy’s health. This study is an attempt to check that are these companies performed well in terms of social responsibility also. It is an exploratory study based on Content analysis of annual reports of selected 5 Maharatna companies for financial year 2014-2015 about corporate social responsibility. In this study, CSR performance of sample companies are evaluated with key aspects of section 135 of Companies Act 2013 and concluded that performance of selected companies is act as a benchmark for fulfilling the corporate social responsibility. On the basis of CSR activities and number of CSR projects, BHEL is 1st while on the basis of CSR budget and CSR expenditure, NTPC is 1st among all selected Maharatna companies. All companies have given preference to invest in CSR1, CSR2 and CSR4 as these activities have maximum score as per disclosure index.

Key words: Companies Act 2013, Corporate Social Responsibility, Maharatna, Public Sector undertakings.

Introduction

Corporate social responsibility (CSR) is not a new phenomenon for Indian society. Companies performed this responsibility as a voluntary initiative before the introduction of section135 of Companies Act 2013. Many companies are having great sense for social welfare & development and they have voluntary performed their responsibility towards society. There are companies which are proactive while others are performed only when they have pushed and pressurise to do so. So it was a need to make social responsibility as a legal provision to create a legal pressure on such companies. Government as well as regulators have felt this need and Business Responsibility Reporting guidelines given by SEBI and Section 135 of Companies Act 2013 are the initiatives taken by them. Companies Act 2013 came into force from 30 August, 2013 having various new provisions for Indian corporates for improving the way of doing business. These sections have been evolved after various discussions with stakeholders such as government, corporate houses, NGOs and general public. Section 135 is one of the revolutionary provisions among these new provisions which clearly prescribe guidelines about CSR such as its applicability criteria, expenditure, CSR policy, various social initiatives & projects and it’s reporting in annual reports. On the basis of CSR provision, social spending and its reporting have become mandatory for those companies who are fulfilling the applicability criteria and this has been implemented from 1 April 2014.

In India, Public sector has played a major role in industrial and economic development and having significant share in gross domestic product. Role of some public sector companies especially Maharatna, Navratna and Miniratna is well acknowledged in the economic development. They are having strong financial results which guide the Indian economy’s health. This study is an attempt to check that are these companies performed well in terms of social responsibility also.

Literature Review

(Gupta, 2015) has studied the concept of CSR in relation to its evolution, CSR provisions in India related to CSR committee, CSR policy, CSR activities, its benefits and shortcomings. This study suggested that 50% of CSR amount should be spent on the development of the locality in which company doing their business and 50% should be spent on remote areas for balanced social development. (Mathur, 2014)has explored various dimensions and challenges of section 135 of Companies Act 2013 and concluded that mandatory spending for CSR will prove a game changer as it will increase innovative and effective CSR activities. With this, there are challenges also which a company has to face for implementing CSR and initial implementation of law is itself a challenge. Except all doubts and challenges section 135 of this act will play a vital role in social welfare of the Indian Economy. (Pooja& Khan, 2014) have viewed CSR as legislation and have studied rules & regulation given in Companies Act 2013 related to CSR. CSR which was voluntary earlier has become mandatory as per Companies Act 2013 and its reporting has to be given in the form of CSR policy and its reporting in the form of web link. Now companies cannot ignore it.(T.N.Panday, 2013)has discussed CSR under the Companies Act 2013and has tried to find out that this concept is well conceived or not. In this study, he has discussed legal provision for CSR in nutshell, analytically appraised the scheme & its impact as a new law for CSR, explained about the conflict between section 135, section 181, and section 182 about spending on CSR and has given his views and criticism on this scheme.

Above studies have discussed the CSR as per section 135 of Companies Act 2013 in general and not studied for some specific sample. The present study is viewed CSR as per Companies Act 2013 in selected Public Sector Undertakings with the following objectives.

Research Objectives:

- To explore key aspectsof Section 135 of Companies Act 2013.

- To comparatively evaluate the CSR reporting of selected Public sector undertakings as per Companies Act 2013.

Research Methodology:

Research approach: Exploratory study with content analysis of CSR parameters given in annual reports of selected companies and hypothesis testing with the help of Anova single factor.

Sample size & data: 5 Maharatana public sector undertakings. These are

|

Bharat Heavy Electricals Ltd. (BHEL)

|

|

Coal India Ltd. (CIL)

|

|

Indian Oil Corporation Ltd. (Indian oil)

|

|

National Thermal Power Corporation (NTPC)

|

|

Steel Authority of India Ltd. (SAIL)

|

Time period: Financial year 2014-15.

Source of data: Secondary data from Annual reports of F.Y. 2014-15 of selected companies.

Hypothesis:

H01: There is no significant difference among selected companies on the basis of CSR activities.

Research tools: Content analysis, disclosure index, hypothesis testing by Anova.

Disclosure index score= Number of disclosed items/ Total number of items*100. This formula has been applied for calculating disclosure score for CSR reporting.

Limitation & further scope of the study: This study has been conducted on a small sample (5) and for the period of 1 year. Time period and sample size can be increased for further study.

Findings and conclusions:

Key aspects of Section135 of Companies Act 2013 with evaluation in selected companies:

- Definition of Corporate Social Responsibility (CSR):

According to CSR Rules, the term CSR is defined in terms of projects or programs relating to those activities which are given in Schedule (vii) of Companies Act 2013; activities undertaken by the board which are recommended by the CSR committee and declared in CSR policy of the company as per Schedule (vii) of Companies Act 2013.There is a flexibility permitted to the companies to invest in any such activities according to their preference.

- Applicability :

Section 135 (1) of Co. act 2013 deals with the criteria for CSR which requires that every company which fulfils at least one of the following criteria will constitute CSR committee and spends 2% of average profit of preceding 3 financial years on CSR initiatives.

Criteria: Companies

- having net worth of 500 crore or more or

- having total annual turnover 1000 crore or more or

- having net profit of 5 crore or more

Table1. Financial details of selected companies

|

Companies

|

Total Turnover (cr.)

|

Net worth(cr.)

|

Profit after tax (cr.)

|

Paid up capital (cr.)

|

|

BHEL

|

30,947

|

34,085

|

1,419

|

490

|

|

CIL

|

95,435

|

40,343

|

13,727

|

516

|

|

Indian oil

|

4,50,756

|

67,970

|

5,273

|

2,428

|

|

NTPC

|

75,363

|

81,658

|

10,291

|

8,246

|

|

SAIL

|

50,627

|

43,505

|

2,093

|

4,131

|

Source: author’s compilation (annual reports of selected companies)

Table-1shows that on the basis of financial details, all selected companies are fulfilling the above criteria. Among all selected companies

- NTPC is the largest on the basis of net worth & paid up capital.

- Indian oil is having highest total turnover.

- CIL is having highest profit after tax.

- Composition of CSR committee:

According to Section 135(1), company which fulfils the applicability criteria will constitute the CSR committee having minimum three members/directors in which at least one is independent director in case of public company. A private company without having any independent director can constitute CSR committee. It means that private companies will form CSR committee with 2 members/ directors. A foreign company will also form CSR committee with 2 members in which one member should be resident in India and other can be nominated by the foreign company.

Section 135(2) has made disclosure of composition of CSR committee mandatory in the Board’s report.

Section 135(3) has mentioned the responsibility of CSR committee. This committee will formulate CSR policy, monitor and update this policy, recommend the CSR expenditure, identify key CSR issues, take decisions on CSR related investment on the basis of needs and preferences of the community etc. This committee will hold CSR meeting to review the CSR practices and recommend the necessary measures for implementing CSR policy.

Table2. Composition of CSR committee of selected companies

|

Composition of CSR committee

|

BHEL

|

CIL

|

Indian oil

|

NTPC

|

SAIL

|

|

Number of dependent directors

|

3

|

2

|

4

|

3

|

2

|

|

Number of independent directors

|

1

|

2

|

2

|

1

|

1

|

|

Total number of members including chairperson and govt. nominee

|

4

|

4

|

6

|

5

|

3

|

|

Number of CSR committee meetings during financial year 2014-15

|

6

|

3

|

----

|

1

|

3

|

Source: author’s compilation (annual reports of selected companies)

Table-2 shows that

- In all selected companies, chairman is the independent director. Indian oil is having maximum number of members while SAIL is having minimum number of members among all selected companies.

- BHEL is conducting maximum number of CSR committee meeting during 2014-15 while there is no CSR committee meeting held in Indian oil during this year.

- Reporting on CSR as per Company Act 2013

Reporting about Corporate Social Responsibility includes a brief outline of CSR policy of company which includes proposed projects/ programmes for CSR and web link for CSR policy for reference; policy on CSR; mechanisms for CSR implementation; CSR practices; Composition of CSR committee; average net profit of a company of last three financial year; prescribed CSR expenditure; details of CSR spent during financial year; reasons for not spending the prescribed amount for CSR etc.

Section 135(4) (a) states that CSR policy will be approved after the recommendations made by CSR committee and company will disclose the content of CSR policy on the company’s website in the prescribed format.

Table3. CSR reporting of selected companies

|

CSR reporting parameters

|

BHEL

|

CIL

|

Indian Oil

|

NTPC

|

SAIL

|

|

1. Brief outline of CSR policy

|

1

|

1

|

1

|

1

|

1

|

|

2. Overview of proposed projects & programs for CSR

|

1

|

1

|

1

|

1

|

1

|

|

3. Composition of CSR committee

|

1

|

1

|

1

|

1

|

1

|

|

4. Average net profit of the company for last three years

|

1

|

1

|

1

|

1

|

1

|

|

5. Prescribed CSR expenditure

|

1

|

1

|

1

|

1

|

1

|

|

6. Details of CSR spent during financial year

|

1

|

1

|

1

|

1

|

1

|

|

7. Manner in which the amount spent during financial year

|

1

|

1

|

1

|

1

|

1

|

|

8. Reasons for not spending the prescribed amount for CSR

|

1

|

1

|

1

|

1

|

1

|

|

9.Implementation, monitoring and reporting of CSR mechanism

|

1

|

1

|

1

|

1

|

1

|

|

10. Responsibility statement of CSR

|

1

|

1

|

1

|

1

|

1

|

|

Disclosure %

|

100%

|

100%

|

100%

|

100%

|

100%

|

Source: author’s compilation (annual report of selected companies)

CSR reporting parameters in table-3 are compiled from the format for CSR activities which is to be included in the Board’s report. Disclosure percentage on the basis of above CSR parameters is 100% for all selected companies. This happens because CSR reporting is mandatory in annual reports as part of Board’s report for these companies in the prescribed format from 1 April 2014.

- Details of CSR activities: Section 135(4) (b) states that company will ensure that CSR activities which are included in CSR policy of the company are undertaken by the company. Schedule VII of Companies Act 2013 has given broad categories of activities on which a company can spend under its CSR initiatives. These activities are shown in annexure 1 and for this study; codes are assigned to these activities such as for activity 1 code- CSR1, activity 2- CSR2, activity 3-CSR3 and so on.

Table4. Calculation of CSR activities of selected companies

|

COMPANY

|

CSR1

|

CSR2

|

CSR3

|

CSR4

|

CSR5

|

CSR6

|

CSR7

|

CSR8

|

CSR9

|

CSR 10

|

Disclosure score

|

|

BHEL

|

1

|

1

|

1

|

1

|

1

|

0

|

1

|

0

|

0

|

1

|

0.7

|

|

CIL

|

1

|

1

|

1

|

1

|

0

|

0

|

0

|

0

|

0

|

0

|

0.4

|

|

IOCL

|

1

|

1

|

0

|

1

|

0

|

0

|

1

|

0

|

0

|

0

|

0.4

|

|

NTPC

|

1

|

1

|

1

|

1

|

1

|

0

|

1

|

0

|

0

|

0

|

0.6

|

|

SAIL

|

1

|

1

|

1

|

1

|

1

|

0

|

1

|

0

|

0

|

1

|

0.7

|

|

Disclosure score of activities

|

1

|

1

|

0.8

|

1

|

0.6

|

0

|

0.8

|

0

|

0

|

0.4

|

|

Source: author’s compilation

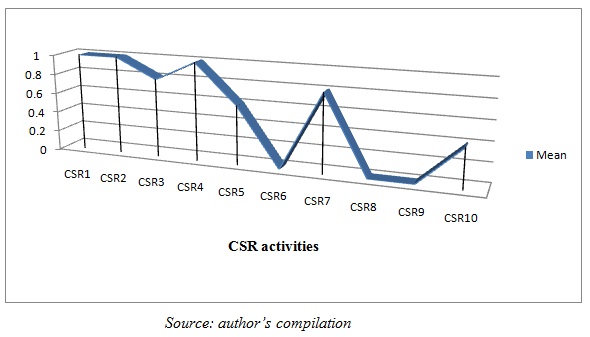

In table-4, disclosure scores are calculated of all CSR activities of selected companies for the year 2014-15. BHEL and SAIL are having maximum score (0.7) among all selected companies. It means that these companies are contributing in more activities and no matter what the CSR expenditure budget they have. NTPC is having maximum CSR budget but on the basis of activities it stands after BHEL and SAIL.

On the basis of mean value of CSR activities of selected companies, all companies have given preference to invest in CSR1, CSR2 and CSR4 as these activities have maximum disclosure score. After that CSR3, CSR7, CSR5 and CSR10 are in their priority list. There is no investment in CSR6, CSR8 and CSR9 by the selected companies during 2014-15. By this, it may be concluded that healthcare; sanitation; education; employment generation; environment sustainability are the premier areas for CSR investment while measures for the benefits of armed forces dependents, contribution to PM relief fund and contribution to technology incubators are not considered at all by these companies in the year 2014-15 to fulfil their social obligations. All companies are contributing for Swachh Bharat SwachhVidyalaya Campaign. Detail of this campaign is as follows:

Table 5.Swachh Bharat SwachhVidyalaya Campaign

|

Contribution

|

BHEL

|

CIL

|

Indian Oil

|

NTPC

|

SAIL

|

|

No. of toilets

|

-

|

48735

|

2700

|

24000

|

690

|

|

No. of schools

|

-

|

30340

|

-

|

-

|

-

|

|

No. of states

|

-

|

-

|

16

|

17

|

-

|

|

No. of districts

|

-

|

-

|

-

|

82

|

-

|

|

No. of locations

|

15 villages

|

-

|

-

|

41

|

-

|

Source: author’s compilation

In table-5, CIL has made maximum number of toilets and contributed maximum in this Campaign.

Chart1. Disclosure of CSR activities

Chart 1 shows the CSR activities in which companies are contributing. Maximum contribution is in CSR1, CSR2 and CSR4 and minimum contribution is in CSR6, CSR8, CSR 9. All selected companies are focusing more on education, healthcare and environmental issues.

- Implementation:

As per provision in Section 135(5) company will spend on CSR activities in the local and nearby areas where it operates. A company may carry out CSR activities directly and through any implementing agency. A registered trust or society, any company established under section 8 of the Act having an established track record of at least 3 financial years for implementing CSR can be taken as an implementing agency. A company may also collaborate with other companies for carry out CSR programs. But each company will spend 2% and shows its CSR report separately.

Table6. Implementation & Assessment of CSR

|

Basis

|

BHEL

|

CIL

|

Indian Oil

|

NTPC

|

SAIL

|

|

Amount spent through

|

Directly as well as

through implementing agency

|

Directly as well as

through implementing agency

|

Directly as well as

through implementing agency

|

through implementing /contracting agency

|

Directly as well as

through implementing agency

|

|

Areas to spent for CSR Initiatives

|

75% of reserved amount for CSR in Local & nearby areas/ district of operating units and remaining for other areas

|

Local area of companies operating units

|

Local area of companies operating units

|

Local area of companies operating units

|

Local area of companies operating units

|

|

Impact assessment

|

Impact assessment of Mega project (having value 2 cr. or more) mandatory by external agency

|

Impact assessment of environmental projects

|

Impact assessment for large projects

|

-----

|

-----

|

|

Need assessment

|

yes

|

yes

|

yes

|

yes

|

yes

|

|

Monitoring and reporting mechanism

|

yes

|

yes

|

yes

|

yes

|

yes

|

Source: author’s compilation

---- meant for unavailable information

Table-6 gives the information about assessment and implementation of CSR of selected companies for the year 2014-15. These companies are taking CSR initiatives in local and neighbourhood areas of operating units with the help of trust and NGOs. Need assessment and monitoring of CSR policy is also performed by them. BHEL, CIL and Indian Oil has assessed the need of CSR project before its implementation while there is no such information available in NTPC and SAIL for 2014-15.

- Penalties for non-compliance of CSR provision: Currently, CSR provision is enacted on the principle of ‘comply or explain’ and having no specific provision of penalties for not spending the requisite amount on CSR in a year. Company which has not been able to spend this amount can only mention the reasons for this in the Board of Directors’ report. SaiVenkateshwaran, Partner and Head -Accounting Advisory Services, KPMG in India reported that if the compliance levels are seen low then ministry of corporate affairs would consider introduction of penalties.

- Details of CSR expenditure:

Section135 (5) is related to the CSR expenditure in which prescribed CSR expenditure limit is 2% of average net profit. This average net profit is the average of immediate past 3 years’ profit and calculation of net profit is as per section 198 of Companies Act 2013.

Table7. Details of CSR expenditure during 2014-15

|

Particulars

|

BHEL

|

CIL

|

Indian Oil

|

NTPC

|

SAIL

|

|

Average net profit (cr.)

|

8222.33

|

1202.12

|

5647.50

|

14173.78

|

3872

|

|

Prescribed CSR Expenditure (cr.)

|

164.45

|

24.04

|

112.95

|

283.48

|

78

|

|

Approved CSR Budget (cr.)

|

165

|

24.04

|

133.40 (112.95+20.45)

|

283.48

|

78

|

|

Expenditure incurred (cr.)

|

102.06

|

24.72

|

113.79

|

205.18

|

35.04

|

|

Amount unspent (cr.)

|

62.94

|

0

|

19.61

|

78.30

|

42.96

|

|

No. of CSR projects

|

314

|

16

|

19

|

203

|

58

|

Source: author’s compilation (annual report of selected companies)

Average net profit shown in table-7 is related to financial year 2014-15 which is calculated from the last 3 financial years i.e. 2011-12, 2012-13, and 2013-14 as per section 198 of Companies Act 2013. Prescribed CSR expenditure is 2% of this average net profit. This amount has been spent directly by selected companies and with the help of trust and NGOs. All selected companies except CIL has unspent expenditure. In approved CSR budget, Indian oil has unspent CSR expenditure of Rs. 20.45 for previous year. NTPC has maximum CSR expenditure as well as maximum unspent CSR expenditure incurred while CIL has minimum CSR expenditure incurred.

Ranks have been given to selected companies for 2014-15.

Table8. Ranks to selected companies on CSR expenditure basis for 2014-15

|

Companies

|

Average net profit (cr.) (i)

|

Approved CSR Budget (cr.) (ii)

|

Rank

|

Expenditure incurred for CSR (cr.) (iii)

|

Rank

|

Amount unspent (cr.)

(ii –iii)

|

No. of CSR projects

|

Rank

|

|

BHEL

|

8,222

|

165

|

2

|

102

|

3

|

63

|

314

|

1

|

|

CIL

|

1,202

|

24

|

5

|

25

|

5

|

0

|

16

|

5

|

|

Indian oil

|

5,648

|

134

|

3

|

114

|

2

|

20

|

19

|

4

|

|

NTPC

|

14,174

|

283

|

1

|

205

|

1

|

78

|

203

|

2

|

|

SAIL

|

3,872

|

78

|

4

|

35

|

4

|

43

|

58

|

3

|

Source: author’s compilation

In table-8, Average net profit for 2014-15 is calculated on the basis of previous 3 financial years. Approved CSR budget is 2% of average net profit. On these bases, selected companies are ranked in which NTPC has ranked 1 because of highest profit and maximum approved CSR budget. On the basis of incurred expenditure on CSR, NTPC is 1st, Indian oil is 2nd, BHEL is 3rd, SAIL is 4th and CIL is 5th. NTPC, CIL and SAIL have similar rank in terms of CSR budget and CSR expenditure while BHEL & Indian oil has got different ranks in both terms. BHEL is 2nd on the basis of CSR budget while Indian oil is 2nd on the basis of CSR expenditure. Indian oil has spent more on CSR than BHEL. On the basis of CSR projects, BHEL has maximum number of projects in different fields and areas while CIL has minimum number of CSR projects.

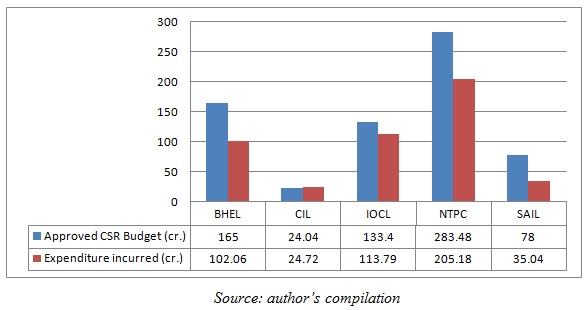

Chart2. CSR budget

Chart 2 shows that NTPC has highest and CIL has the lowest approved CSR budget. Expenditure incurred is based on this budget. Therefore, maximum expenditure incurred by NTPC while minimum expenditure incurred by CIL. All selected companies are spending less than its approved budget except CIL.

Hypothesis testing:

H01: There is no significant difference among selected companies on the basis of CSR activities.

Table9. Anova table for hypothesis testing

|

ANOVA single factor

|

|

Source of Variation

|

SS

|

df

|

MS

|

F

|

P-value

|

F criteria

|

|

Between Groups

|

0.92

|

4

|

0.23

|

0.907895

|

0.467503

|

2.578739

|

|

Within Groups

|

11.4

|

45

|

0.253333

|

|

|

|

|

Total

|

12.32

|

49

|

|

|

|

|

Source: author’s compilation (MS-Excel)

In table-9,Table value of F at 5% significant level at given degree of freedom (4, 45) is 2.58. Calculated F value is 0.91.Calculated F is less than F-criteria (0.91< 2.58) P- Value is also more than 0.05 which shows that null hypothesis is accepted. So, there is a no significant difference among selected companies on the basis of CSR activities disclosure index.

Conclusions & suggestion:

The Public Sector Units have played an integral role in the industrial development of an economy. There are many PSUs which have performed well in terms of profit, turnover and social responsibility. This paper concluded that all selected Maharatna PSUs are fulfilling their social responsibility at the same pace according to Companies Act 2013. There is no significant difference among these companies on the basis of CSR activities. All selected companies are large Public sector undertakings and all are following CSR Policy Rules 2014 and DPE Guidelines 2014 for CSR. Most of the selected companies are focusing on healthcare, education, environmental sustainability with the help of trusts and NGOs. They should also focus on other areas which are really needed to focus. CSR practices are not new to Indian companies and what the companies act does is that it brings social change by taking more companies into the fold. By this act, a wealth pool of crore will be created and utilized for social welfare which helps to remove the poverty, hunger and inequalities and promotes healthcare, education, livelihood generation etc. in the society. This mandatory spending is surely proved to be a game changer for development and growth of Indian economy. CSR is going to rise in coming years in terms of spending, activities, scope etc. so it needs to be done purposefully, methodically and selflessly. There should be specific audit of CSR expenditure which will help to avoid the superficiality of CSR provision in relation to its compliance.

References:

- Annual reports of selected companies i.e. BHEL, CIL, SAIL, NTPC and IOCL.

- Gupta, S. (2015). Sustainable Development & CSR- An Emerging Issue. The Chartered Accountant, 63(12), 132-138.

- Mathur, C. (2014). Section 135, Companies Act 2013- A Game Changer for Corporate Social Responsibility. SSPS IJBMR.

- Pooja Rani, M. K. (2014). Corporate Social Regulation under Companies Act, 2013. International Journal of Multidisciplinary Research and Development, 1(7), 258-261.

- N.Panday. (2013). The Concept of Corporate Social Responsibility under the Companies Act 2013- Whether well conceived? Chartered Secretary, 43(9), 1053-1057.

- India: Corporate Social Responsibility - Indian Companies Act 2013 retrieved from http://www.business-standard.com/article/companies/an-overview-of-csr-rules-under-companies-act-2013 114031000385_1.html

- http://www.ey.com/IN/en/Issues/Governance-and-reporting/EY-Compass-on-Companies-Act-2013/EY-cfo-companies-act-2013-corporate-social-responsibility

- http://www.mca.gov.in/SearchableActs/Section135.html

- Comments on draft CSR Rules under Section 135 of Companies Act 2013, National Foundation for India, available at: http://www.nfi.org.in/sites/default/files/nfi_files/Comments%20on%20draft%20CSR%20rules.pdf

- Handbook on Corporate Social Responsibility in India, Confederation of Indian Industry, available at: http://www.pwc.in/en_IN/in/assets/pdfs/publications/2013/handbook-on-corporate-social-responsibility-in-india.pdf

- Implications of Companies Act, 2013 Corporate Social Responsibility, Grant Thorton, available at: http://gtw3.grantthornton.in/assets/Companies_Act-CSR.pdf

- http://attemptnwin.com/what-is-meant-by-navaratna-mahartna-companies/

Annexure 1:

|

CSR activities

|

Codes allotted

|

|

1. Eradicating hunger, poverty & malnutrition, promoting health care & sanitation, making safe drinking water available

|

CSR 1

|

|

2. Promoting education including special education, vocational education & skills for women, children, elderly and specially challenged and differently abled, skill development, capacity building, livelihood enhancement projects

|

CSR 2

|

|

3. Promoting gender equality, setting up homes and hostels for women and orphans, setting up old age homes ,social infrastructure, empowering women , measures for reducing inequalities faced by socially and economically backward groups

|

CSR 3

|

|

4. Ensuring environmental sustainability, ecological balance, protection of flora and fauna, conservation of natural resources, maintenance of quality of air, water and soil

|

CSR 4

|

|

5. Protection of national heritage, art and culture, setting up public libraries, promotion and development of traditional arts and handicrafts

|

CSR 5

|

|

6. Measures for the benefit of armed forces, veteran, war widows and their dependants

|

CSR 6

|

|

7.Training to promote rural sports nationally recognised sports and Olympic sports

|

CSR 7

|

|

8. Contribution to the Prime Minister's National Relief Fund or any fund of central govt. for welfare, relief and socio- economic development of backward classes, minorities and women

|

CSR 8

|

|

9.Contribution provided to technology incubators located within academic institutions which are approved by central govt.

|

CSR 9

|

|

10.Slum area development

|

CSR 10

|

Source: CSR activities as per Companies Act 2013