A Refereed Monthly International Journal of Management

A Study of Customer Innovativeness for the Mobile Wallet Acceptance in Rajasthan

Author

|

David Campbell

Research Scholar, Department of Banking, Economics & Finance, Bundelkhand University, Jhansi, India.

|

Dr. C. B. Singh

Professor, Department of Banking, Economics & Finance, Bundelkhand University, Jhansi, India.

|

Abstract:

This study tries to investigate the impact of customer innovativeness on the acceptance of mobile wallet in India using Perceived Usefulness and Perceived Ease of Use from Technology Acceptance Model (TAM). The purpose of this paper is to find whether Customer Innovativeness (CI), Perceived Usefulness (PU) and Perceived Ease of Use (PEU) for Mobile Wallet, influence Indian Behavioural Intention (BI) to use digital payment platforms (Mobile Wallets) with the emergence of Digital and Cashless India. The findings revealed that only the ‘Perceived Ease of Use has direct influence on Behavioural Intention to use mobile wallet but ‘Perceived Usefulness’ and ‘Innovativeness of Customers’ do not have significant effect on ‘behavioural Intention’ which is indeed a matter of concern for establishing Mobile Wallet industry in India.

Keywords: Customer Innovativeness, Perceived Usefulness, Perceived Ease of Use, Mobile Wallet.

Introduction

As per Himanshu (2016), Mobile telephony has changed the entire scene of India where at one time landline was considered a luxury enjoyed only by the affluent. Presently, ninety percent of India is connected with telecom networks and almost all Indian families especially those residing in cities have mobile phones giving base to the epithet Digital India. The mobile banking transaction grew by 4,000 per cent in value terms and over 500 per cent in volume terms from 2012 to 2015 (Himanshu, 2016). It gave rise to many start-ups as well as lured major players of mobile wallet to enter the domain of financial transactions. As part of Digital and Cashless India not only all government transaction were made online, but non government transactions were also encouraged to follow the same. The Indian Government is putting a lot of effort to generalise the use of cashless transactions. The main tool for this can only be Mobile Wallets. Some like ‘BHEEM’ are run through government initiatives and many are operated by private companies and banks. Many mobile wallets or Digital Wallets or e-Wallet apps are available in Indian market. Some are PayTM, Mobikwik, FreeCharge, State Bank Buddy, HDFC PayZapp, ICICI Pockets, LIME of Axis Bank, PhonePe from Flipkart Group Company, Ola Money and Airtel Money (List of best Mobile Wallets in India to Make Online Payments). Though in future, through government compulsion and fines, use of mobile wallet may increase but the question is how fast innovative customers will accept mobile wallet and by word of mouth popularise its usage amid customers who are either followers or laggards. In such a situation it becomes imperative to study the factors which could play an influential role in accepting mobile wallet by Indians.

This study is one of the preliminary endeavours to relate Customer Innovativeness (CI) with consumer behaviour for mobile wallets in India. This would aid companies as well as government agencies to take pre-emptive measures for successful implementation of their marketing strategies by developing methods to involve more and more people of India. `

Customers who are high in innovativeness are important when implementing new technology in any society. They are the first one to try new technology and spread their reviews and feedback. It is necessary that innovators show positive behaviour towards new technology like digital mobile, otherwise, implementing new technology could fail or take more time than required. Therefore, it become imperative to answer few questions like

- Does an innovative customer have any future intention to use Mobile Wallet?

- Does ‘innovative customer’ recognise Mobile wallet as useful?

- Whether innovative customer identifies Mobile Wallet as easy to use?

- Do customers who perceive mobile wallet easy to use have any intention to use mobile wallet in future?

- Can we say that those customers who perceive using mobile wallet useful will be using mobile wallet in future too?

To cater the above questions, it becomes relevant to unveil the effect of operational factors like PU, PEU and CI on Behavioural Intention (BI) and to explore new extended model like TAM for Mobile Wallet which includes personality parameter like innovativeness.

The Conceptual Framework of the Study

One of the famous models for adopting technology is Technology Acceptance Model given by Davis (1989). Many studies have been done with TAM to analyse intention and actual behaviour for new and innovative technologies like Hong, Teh, & Soh (2014) on young customers for accepting Smartphone, Venkatesh & Davis (2000) for generating new model UTAUT, Saadé, Nebebe, & Tan (2007) for Multimedia Learning Environments, etc.. In these studies, customer personality is not included which could be important in anticipating future intention of customers. To quote Rosen (2005), the Unified Theory of Acceptance and Use of Technology (UTAUT) model, does not include the personality aspect. To fill this lacuna the paper will include customer innovativeness for better understanding of ‘Intention’ to use new technology. In TAM also, customer innovativeness is not included. By incorporating customer innovativeness with TAM, the paper attempts to offer a more pragmatic model for customer behavioural intention.

- Literature Review.

- Perceived Ease of Use and Perceived Usefulness:

Davis, (1989) in his paper, studied two factors: Perceived Usefulness and Perceived Ease of Use . The purpose of Davis was to pursue better measure for the two factors. Perceived Usefulness is an extent to which an individual thinks that his job performance will enhance if he uses a particular new technology (Davis, 1989). Perceived Ease of Use is the vicinity to which one thinks that using a particular new technology or system will be easy or free of any effort (Davis, 1989). As per Davis (1989), these two variables are especially important among other factors, which influence Information Technology usage. These two factors are important for people to accept or reject Information Technology.

Venkatesh, Morris, Davis, & Davis (2003)did take the study on new technology acceptance to a new level where they analysed eight different models of technology acceptance and gave a unified model based on them. The Eight models studied were: Theory of Reasoned Action, The Technology Acceptance Model, The Theory of Planned Behaviour, The Model of PC Utilization, The Motivational Model, Model combining Technology Acceptance Model and the Theory of Planned Behaviour, The Innovation Diffusion Model and The Social Cognitive Theory. The four factors which were finalised for study were effort expectance, performance expectancy, facilitating conditions and social influence. Out of them performance expectancy was similar to and represented perceived usefulness. Performance expectancy means degree to which one thinks technology could improvise one’s job performance. Another churned construct was effort expectancy which was similar to and represented perceived ease. Effort expectancy means degree of ease affiliated with usage of new technology system. Both, performance expectancy and effort expectancy are significant in the study and important factors in determining behavioural intention to use new technology (Venkatesh et al., 2003).

Chao, Reid, & Mavondo (2009) discussed three type of consumer innovativeness which influences adoption of new electronic products. First is Consumer Innate Innovativeness (CII). CII is defined as the degree to which one is ready to accept innovative concept without involving others or their past experience. Second is Domain Specific Innovativeness (DSI). DSI is defined as tendency to learn new things and try new things related to a particular domain of interest. Third is Vicarious Innovativeness (VI), which is, acquiring knowledge about new product but not necessarily purchasing it. In the result the DSI is directly influence adoption of product innovation (Chao et al., 2009).

Rogers (1995) in his book “DIFFUSION OF INNOVATIONS” mentioned that many innovations require long period to be part of society. This may take years from implementation to full acceptance by population in their day to day work. Diffusion is the process by which innovation is communicated through some channel among the members of social system. Innovativeness is the degree to which an individual or other unit of adoption is relatively earlier in adopting new ideas than the other members of a system (Rogers, 1995). Innovators do regularly check out for new ideas and are first in the community to accept.

Rosen (2005) in his thesis studied personal innovativeness and its influence on technology acceptance and use. He used The Unified Theory of Acceptance and Use of Technology (UTAUT) model given by Venkatesh et al., (2003). As per Rosen (2005), though UTAUT is a latest and upgraded model and is a synthesis of many of the previous models, it still lacked the personality factor. The study included customer innovativeness in the UTAUT Model to prove Personal Innovativeness as a significant predictor for behavioural intention while using technology.

Jawed & Khan, (n.d.) in their paper examined customer innovativeness with TAM by using structural equation modelling with sampling size of 252 derived through purposive sampling method. Apart from ease of use and attitude, innovativeness has significant effect on future intention.

Park, Park, Park, & Chung, (2016) did a research in which they studied innate innovativeness and domain specific innovativeness related to cooking intention by watching cookery shows on television. In their model they inculcate Technology Acceptance Model to study effect of CI on perceived ease of use and perceived usefulness.

Chung & Park, (2016) studied cooking classes TV shows in which effect of consumer innovativeness on perceived usefulness, perceived ease of use and cooking intention was studied. The study concluded the significant effect of Consumer Innovativeness on intention to cook, ease of use and usefulness.

Figure 1: Research Framework

- Research Methodology

- To identify the impact of customer innovativeness on ‘behavioural intention’, ‘perceived usefulness’ and ‘perceived ease of use’ to use mobile wallet in future.

- To find the influence of ‘Perceived Usefulness of Digital Wallet’ and ‘Perceived Ease of Use of Digital Wallet’ on Behavioural Intention to use ‘Mobile Wallet’ in India.

First the model under study was defined and required data was collected. Pilot study was done to understand the relevance of items in questionnaire. After testing the reliability and validly partial least square structural equation modelling was done to study the significance of hypothesis under study. The entire study was done with 10 percent of significance level with confidence level of 90 percent.

The study was conducted in Jaipur and Ajmer cities of Rajasthan state in India.

The period of study was four months.

- Method of Data Collection

This study was oriented on primary data collected through hardcopy of questionnaire and also through Google Forms Questionnaire. Non-Probability Sampling like Snowball and Convenience Sampling methods were used by the researcher.

The size of the sample is 100. Maximum number of pointers pointing on any endogenous construct multiplied by 10 is the thumb rule for sample size by Barclay, D., Thompson, R., Dan Higgins (1995), (as cited in Garson, 2016). Hence in our case it is 3 multiplied by 10 which give 30. Hence our sample is sufficient for the PLS SEM analysis.

Partial least Square Structural Equation Modelling has been used. Software used is SmartPLS (v.3.2.6) student’s version. Partial Least Square SEM surpasses traditional Covariance Based SEM when study is primarily exploratory in nature and objective is not only to define model but to understand the predictive nature of factors under study.

Questionnaire was used as an instrument of data collection. All questions are with 5 point Likert scale with ‘Strongly Disagree’ to ‘Strongly Agree’ as extreme ends. The questionnaire was developed using previous scales (table 1).

H1 customer innovativeness does not significantly affect behavioural intention to use mobile wallet in India.

H2 customer innovativeness does not significantly affect the perceived usefulness of mobile wallet

H3 customer innovativeness does not significantly affect the perceived ease of use of mobile wallet

H4 perceived usefulness does not significantly affect the intention to use of mobile wallet

H5 perceived ease of use does not significantly affect the intention to use of mobile wallet

H6 perceived ease of use does not significantly affect the perceived usefulness for mobile wallet

Analysis and Interpretation

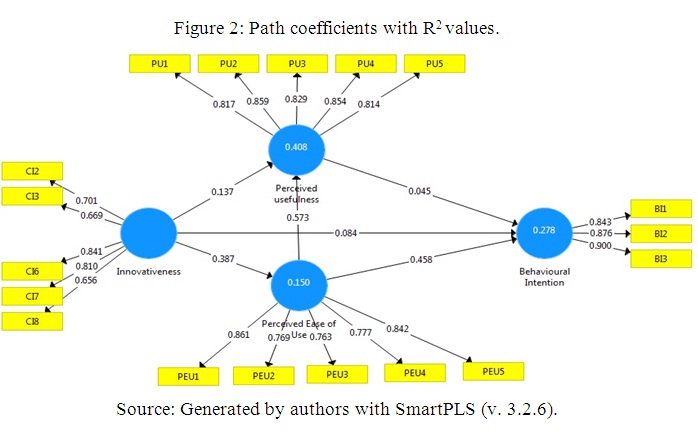

Following figure depicts t statistics from PLS-SEM of the model under study.

All four constructs are related to Smartphone. Outer loadings, path coefficients and R2 values are depicted in figure taken from SmartPLS (v. 3.2.6). For reliability and validity, kindly refer table no. 1.

Table 1. For Reliability and Convergent Validity.

|

Latent Variables

|

Indicators

|

Loadings

|

Loadings Square

|

Composite Reliability

|

AVE

|

|

Customer Innovativeness

|

CI1

|

0.701

|

0.491

|

0.857

|

0.547

|

|

CI2

|

0.669

|

0.448

|

|

CI3

|

0.841

|

0.707

|

|

CI4

|

0.810

|

0.656

|

|

CI5

|

0.656

|

0.430

|

|

Perceived Usefulness

|

PU1

|

0.817

|

0.667

|

0.920

|

0.697

|

|

PU2

|

0.859

|

0.738

|

|

PU3

|

0.829

|

0.687

|

|

PU4

|

0.854

|

0.729

|

|

PU5

|

0.814

|

0.663

|

|

Perceived Ease of Use

|

PEU1

|

0.861

|

0.741

|

0.901

|

0.645

|

|

PEU2

|

0.769

|

0.591

|

|

PEU3

|

0.763

|

0.582

|

|

PEU4

|

0.777

|

0.604

|

|

PEU5

|

0.842

|

0.709

|

|

Behavioural Intention

|

BI1

|

0.843

|

0.711

|

0.906

|

0.763

|

|

BI2

|

0.876

|

0.767

|

|

BI3

|

0.900

|

0.810

|

Source: Generated by authors with SmartPLS (v. 3.2.6).

All indicators’ loadings in our study is greater than 0.4. 0.7 and higher are preferred and 0.4 and higher are acceptable especially in case of exploratory as per by Hulland (1999) (cited in Wong 2013). In our case all are well above 0.4. Hence our indictor reliability exists. Hair, Hult, Ringle, & Sarstedt (2013) stated that composite reliability should be greater than 0.6 as below it, composite reliability is lacking. Composite reliability is all greater than 0.6 internal consistency reliability is reflected by all four constructs (Table 1); hence internal consistency reliability is established. Average Variance Extracted (AVE) should be greater than 0.5 (Hair et al., 2013). All Average Variance Extracted (AVE) are greater than 0.5, hence convergent validity is confirmed (Table 1). For discriminant validity, we Fornell and Laker Criterion approach is used as suggested by Hair et al. (2013). If AVE square root of a construct is greater than correlation values among constructs then that construct is discriminant or distinct in meaning from other. Kindly refer table 2 for Fornell and Laker method. Over here all square root values of AVE are greater than correlation values, hence discriminant validity is established (Table 2). Value of the standardised root mean square residual (SRMR) is 0.08 which is less than 0.9; hence our model is fit for research. As per Hu and Bentler, 1999, value of SRMR should be 0.09 or lower (cited in Iacobucci, 2010).

Table 2. Fornell and Laker Criterion for Discriminant Validity.

| |

Behavioural Intention

|

Customer Innovativeness

|

Perceived Ease of Use

|

Perceived Usefulness

|

|

Behavioural Intention

|

0.874

|

|

|

|

|

Customer Innovativeness

|

0.278

|

0.739

|

|

|

|

Perceived Ease of Use

|

0.519

|

0.387

|

0.803

|

|

|

Perceived Usefulness

|

0.363

|

0.359

|

0.626

|

0.835

|

Source: Generated by authors with SmartPLS (v. 3.2.6).

For the given paths and also for our hypothesis, the value ‘T’ when greater than 1.65 is significant with 90 percent confidence level and if greater than 1.96 then relation is significant with 95 percent confidence level. In our study 10000 subsamples are taken for Bootstrapping from which ‘T’ value and ‘P’ values are generated. In our study, we can observe that H3, H5 and H6 are accepted and the rest of the hypotheses are not significant.

Table 3: Path Significance.

|

PATHS

|

ORIGINAL SAMPLE

|

SAMPLE MEAN

|

STANDARD ERROR

|

T STATISTICS

|

P VALUE

|

|

H1 Customer Innovativeness -> Behavioural Intention

|

0.084

|

0.093

|

0.085

|

0.991

|

0.322

|

|

H3 Customer Innovativeness -> Perceived Ease of Use

|

0.387

|

0.402

|

0.090

|

4.305

|

0.000**

|

|

H2 Customer Innovativeness -> Perceived Usefulness

|

0.137

|

0.137

|

0.092

|

1.494

|

0.135

|

|

H5 Perceived Ease of Use -> Behavioural Intention

|

0.458

|

0.464

|

0.125

|

3.660

|

0.000**

|

|

H6 Perceived Ease of use -> Perceived Usefulness

|

0.573

|

0.579

|

0.068

|

8.412

|

0.000**

|

|

H4 Perceived Usefulness -> Behavioural Intention

|

0.045

|

0.040

|

0.015

|

0.303

|

0.762

|

|

‘*’ statistically significant with 90 percent confidence.

‘**’ statistically significant with 95 percent confidence.

|

Source: Generated by authors with SmartPLS (v. 3.2.6).

All ‘R2’ values are significant at 95 percent confidence level for endogenous constructs (table 4).

Table 4. R2 Significance

| |

original sample

|

sample mean

|

standard deviation

|

T statistics

|

P values

|

|

Behavioural Intention

|

0.278

|

0.311

|

0.076

|

3.646

|

0.000**

|

|

Perceived ease of use

|

0.150

|

0.17

|

0.071

|

2.111

|

0.035**

|

|

Perceived usefulness

|

0.408

|

0.426

|

0.074

|

5.487

|

0.000**

|

|

** Statistically significant with 95 percent confidence.

|

Source: Generated by authors with SmartPLS (v. 3.2.6).

As per f square values (Table 5), perceived ease of use is the main contributing factor in ‘Behavioural Intention’ to use mobile wallet. ‘Perceived ease of use’ is also the main construct in explaining variance in ‘Perceived usefulness’.

Table 5. ‘f square’

|

f square

|

Behavioural Intention

|

Customer Innovativeness

|

Perceived ease of use

|

Perceived usefulness

|

|

Behavioural Intention

|

|

|

|

|

|

Customer Innovativeness

|

0.008

|

|

0.176*

|

0.027

|

|

Perceived ease of use

|

0.168*

|

|

|

0.471*

|

|

Perceived usefulness

|

0.002

|

|

|

|

|

‘*’ statistically significance

|

Source: Generated by authors with SmartPLS (v. 3.2.6).

From our study, the findings are as follows.

- The main setback is customer innovativeness, which is not directly affecting behavioural intention. From this we can say that those customers who are having innovative personality and are the crux in the society to accept technology and advocate it, are still not ready to use mobile wallet. The main reason for this is innovative customers are not finding mobile wallet useful as there is no direct relation between innovativeness of customers and perceived usefulness.

- Also, people who perceive mobile wallet as useful, have no intention to use mobile wallet regularly in future. The reason may be other options for transactions, which are either more easy to use or have become a regular habit for the people.

- Another sighting is that innovative customers find mobile wallet easy to use (relationship is significant). This is the only reason which is establishing indirect relationship between innovativeness and behavioural intention. Definitely, innovative customers find new technologies easy to use and this prompts them to at least experience a novel mode of financial transaction.

- In our study, perceived ease of use is a part of total perceived usefulness and is significant but not enough to make mobile wallet useful.

Discussion

Innovative customers are simply using mobile wallet for the sake of experiencing it. They are not finding mobile wallet useful enough to make it their preferred choice of transaction. If innovative customers are not finding mobile wallet useful then they will neither propagate it through positive word of mouth nor advice it to followers or laggards. If this happens it may take government a lot more time to successfully institute the culture of cashless transactions in Indian society.

Government should promote and popularise its merits and usability in the society. The government should also create hurdles in using other options like bank ATM cash withdrawals to increase usefulness of mobile wallet. By introducing mobile wallet through innovative customers, government could endorse mobile wallet usage without losing positive vibes for itself because other methods like penalties and fines could make society dubious towards the government.

Mass communication could be used for the purpose. Private firms are already doing it but the government has a much larger credibility as compared to any firm and should bear the onus responsibly. Dave (2016) in his study did mention some advantages and disadvantages for mobile wallet usage. Some of the advantages are convenience, discounts, tracking spends, budget discipline, etc, Disadvantages are identity theft, losing phone means losing money, difficult for non tech-savvy, overspending if one finds it too easy to use, etc,. Venkatachalam (2017) wrote an article on DNA India website in which security is an issue. Indian wallets do not have hardware security which makes it prone to software attacks. Wrongly typed numbers could make wrong transactions, it is not safe with public Wi-Fi, if one looses phone personal details are out, etc. There are also many places where mobile network is not proper which could also hamper mobile wallet usage. Government should intervene and provide solutions for the above stated issues. Some of the suggestive steps the government can take to increase the usefulness are introduction of biometric while using mobile wallet and improving network connectivity in upcountry. It will give more security to its usage.

Limitations and Scope for future research.

There are limitations in our study. First the sample size under study is ‘100’ which is small. If we increase the sample size, it would become easy to study demographic variables like gender, age or income of population. Second, all samples are from Ajmer and Jaipur districts where as there are around 33 districts in Rajasthan. Future research is required to study why mobile wallet is not considered useful by people of Rajasthan. A study of factors which could influence usefulness of using mobile wallet could give a more empirically proved reason.

References:

Chao, C.-W., Reid, M., & Mavondo, F. (2009). The influence of consumer innovativeness on really new product adoption. In ANZMAC 2009 (pp. 1–8). Retrieved from http://eprints.aston.ac.uk/7644/

Chung, K., & Park, S. (2016). An Empirical Study on the Innate and Domain-specific Consumer Innovativeness on Cooking Intention : Application of TAM, 9 (4), 285–294.

Davis, F. D. (1989). Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Quarterly , 13 (3), 319–340. http://doi.org/10.2307/249008

Garson, G. D. (2016). Partial Least Square: Regression & Structural Equation Models . Stastistical Associates Blue Book Series.

Hair, J. F. J., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2013). PARTIAL LEAST SQUARES STRUCTURAL EQUATION MODELING ( PLS-SEM ) (1st ed.). Thousand Oaks (California) [etc.]: SAGE Publications, Inc.

Hong, Y. H., Teh, B. H., & Soh, C. H. (2014). Acceptance of smart phone by younger consumers in Malaysia. Asian Social Science , 10 (6), 34–39. http://doi.org/10.5539/ass.v10n6p34

Iacobucci, D. (2010). Author â€TM s personal copy Structural equations modeling : Fit Indices , sample size , and advanced topics. Journal of Consumer Psychology , 20 (1), 90–98. http://doi.org/10.1016/j.jcps.2009.09.003

Jawed, T., & Khan, I. A. (n.d.). Innovativeness and Internet Shopping Adoption : An Extended Technology Acceptance Model.

Karaarslan, M. H., & M. ŞükrüAkdoğan. (2015). Consumer Innovativeness: A Market Segmentation. International Journal of Business and Social Science , 6 (8), 227–237.

Park, S., Park, G., Park, S., & Chung, K. (2016). An Empirical Study on the Innate and Domain-specific Consumer Innovativeness on Cooking Intention : Application of TAM. International Journal of U- and E- Service, Science and Technology , 9 (4), 285–294.

Rogers, E. M. (1995). Diffusion of innovations . Macmillian Publishing Co. http://doi.org/citeulike-article-id:126680

Rosen, P. A. (). (2005). The effect of personal innovativeness on technology acceptance and use . Oklahoma State University. Retrieved from http://proquest.umi.com/pqdweb?did=953999371&Fmt=7&clientId=70192&RQT=309&VName=PQD

Saadé, R. G., Nebebe, F., & Tan, W. (2007). Viability of the “Technology Acceptance Model” in Multimedia Learning Environments: A Comparative Study. Interdisciplinary Journal of Knowledge and Learning Objects , 3 , 175–184.

Venkatesh, V., & Davis, F. D. (2000). A Theoretical Extension of the Technology Acceptance Model: Four Longitudinal Field Studies. Management Science , 46 (2), 186–204. http://doi.org/10.1287/mnsc.46.2.186.11926

Venkatesh, V., Morris, M. G., Davis, G. B., & Davis, F. D. (2003). U SER A CCEPTANCE OF I NFORMATION T ECHNOLOGY : TOWARD A UNIFIED V IEW. MIS Quarterly , 27 (3), 425–478.

Wong, K. K. (2013). Partial Least Squares Structural Equation Modeling (PLS-SEM) Techniques Using SmartPLS. Marketing Bulletin , 24 (1), 1–32. http://doi.org/10.1108/EBR-10-2013-0128

Websites:

About the Programme - Digital India . (n.d.). Retrieved 05 09, 2017, from http://www.digitalindia.gov.in: http://www.digitalindia.gov.in/content/about-programme

Dave, R. (2016, 12 12). Here are the advantages of cashless payments and the pitfalls you should beware of . Retrieved 05 12, 2017, from http://economictimes.indiatimes.com: http://economictimes.indiatimes.com/wealth/spend/going-cashless-is-it-good-for-you/articleshow/55908649.cms

Himanshu. ( 2016, August 20). IDC: Samsung tops Indian smartphone market in Q2, Micromax follows . Retrieved January 16, 2017, from http://www.gsmarena.com: http://www.gsmarena.com/idc_samsung_tops_indian_smartphone_market_in_q2_micromax_follows-news-20061.php

List of best Mobile Wallets in India to Make Online Payments . (n.d.). Retrieved from http://www.thewindowsclub.com: http://www.thewindowsclub.com/best-mobile-wallets-in-india

Venkatachalam, R. (2017, 01 27). Advantages and disadvantages of e-wallets . Retrieved 05 12, 2017, from http://www.dnaindia.com: http://www.dnaindia.com/money/report-advantages-and-disadvantages-of-e-wallets-2296526

Appendix

Questionnaire:

Scale from (“Strongly Disagree” = 1, to “Strongly Agree” = 5)

|

CONSTRUCTS

|

|

ITEM

|

SOURCE

|

|

Perceived Usefulness

|

PU1

|

Using Mobile Wallet would enable me to accomplish payments more quickly

|

(Davis, 1989) with modifications as per study

|

|

PU2

|

Using Mobile Wallet would improve my payment performance

|

|

PU3

|

Using Mobile Wallet would enhance my effectiveness on doing payments

|

|

PU4

|

Using Mobile Wallet would make it easier to do payments

|

|

PU5

|

I would find Mobile Wallet useful in doing payments

|

|

Perceived Ease of Use

|

PEU1

|

Learning to operate Mobile Wallet would be easy for me

|

(Davis, 1989) with modifications as per study

|

|

PEU2

|

My interaction with Mobile Wallet would be clear and understandable.

|

|

PEU3

|

I would find Mobile Wallet to be flexible to interact with

|

|

PEU4

|

I would be easy for me to become skilful at using Mobile Wallet

|

|

PEU5

|

I would find Mobile Wallet easy to use

|

|

Consumer Innovativeness

|

CI1

|

I often buy new products that make me think logically.

|

(Karaarslan & M. ŞükrüAkdoğan, 2015)

|

|

CI2

|

I find innovations that need a lot of thinking intellectually challenging and therefore I buy them instantly.

|

|

CI3

|

Innovations make my life exciting and stimulating.

|

|

CI4

|

Acquiring an innovation makes me happier.

|

|

CI5

|

The discovery of novelties makes me playful and cheerful.

|

|

Behavioural Intention to Use Mobile Wallet

|

BI1

|

I intend to use the Mobile Wallet in the next 6 months.

|

(Venkatesh et al., 2003) with modifications as per study.

|

|

BI2

|

I predict I would use the Mobile Wallet in the next 6 months.

|

|

BI3

|

I plan to use the Mobile Wallet in the next 6 months

|