A Refereed Monthly International Journal of Management

An Empirical Study on Effect of Experience on Consumer Adoption Intention towards Internet Banking

Author

|

Monica Bhardwaj1

Fortune Institute of International Business,

Plot no 5, Rao Tula Ram Marg,, Vasant Vihar, Delhi, Delhi, India- 110057

monica29rose@hotmail.com

|

Dr. Renu Aggarwal2

YMCA University, Faridabad

renu_aggarwal77@yahoo.co.in

|

Abstract

Internet banking has emerged as the most lucrative and cost effective service in electronic commerce. While the movement of the major banks and financial service providers towards the digital channels, the future scope of online presence appears highly optimistic. Besides offering major banking services through this mode, the banks and financial service providers get platform to maintain direct connect with their customers that enable them to offer superior services and strengthen customer relations. The present study investigates the moderation effect of user experience with varied lengths of use on the adoption intention and continued use towards internet banking. The study extends technology acceptance model to examine the user perceptions towards internet banking over a period of time. The findings highlight the differences in behavior based on the frequency use. The study provides useful implications for the academicians and the managers.

Keywords -Internet banking, experience, adoption intention, Technology Acceptance Model

Introduction

Value creation through customized experiences intensifies the customer longevity. Engagement of customer in the co-creation of the service enables personalization to enable continued service use. The key to ecommerce success is embedded in the acquiring and retaining of the customer (Jarvenpaa and Todd, 1997; Reichheld and Schefter, 2000). The replacement of acquired customers is deeply costly affair owing to high costs involved in initial stages of customer acquisition (Ouma et al., 2013). The retained customers generate higher revenues through repeat purchases and yield strong branding through positive word-of-mouth. In addition they tend to be less sensitive to price changes (Cvent, 2013). The customer retention strongly influence the costs and profitability of a business over time (Kottler, 2000).

Majority of the internet service providers fail to differentiate the users based on diverse expectations and preferences. The returning customer must receive a different more personalized experience as compared to the others. The internet explosion and growing user dependence makes it an interesting area for exploration by academicians and practicing managers to understand the consumer behavior of diverse lengths of user ( Mäenpää et al, 2008). So the current study investigates the impact of experience on adoption intention of internet banking.

The rest of the paper is organised as follows. In the next section, literature has been reviewed. Section 3 presents the hypothesised research model. Research methods are discussed in section 4 that describes the data collection method and the survey instrument along with scale development. Following section presents the analysis and results are reported. This is followed by the discussion and managerial implications.

Review of Literature

Experiences shape users attitudes towards expectation from the providers for future use. Different levels of experiences influence the different directions of reinforcement on clues. The clues maybe a positive brand or service recall or vice versa. Hence inefficiency in recognition and management of clues appropriately may lead to building negative perception (Fatma, S. (2014). Customers hold diverse concerns based on varied levels of experience. The customer retention is high in the cases where the customer possess high positive experiences (Liang and Huang, 1998). According to cognitive dissonance theory (Festinger,1957) the initial transaction experience causes change in initial beliefs, affect and values (cognition) on basis of real experience which keeps being revised with every transaction experience until a balance is achieved between the real and observed behaviour (Gupta & Kim, 2007). Experiences consists of direct (online purchase, search etc) and indirect (advertisements) experiences on basis of which the online information is understood and presented by the customer. Experience is regarded as strong determinant of customer expertise and familiarity. Expertise and familiarity are identified as the two dimensions of customer knowledge. Hence experience is linked with the knowledge accumulated in memory and decision making ability of the user (Rodgers et al, 2005; Alba and Hutchinson, 1987).

Internet banking being the newer platform for transactions, with every experience the probability of its adoption and continued usage increases. Individuals utilize the knowledge acquired from their previous experiences to shape their present intentions (Fishbein and Ajzen, 1975; Sun & Zhang, 2006). Technology acceptance model identifies perceived usefulness and perceived ease of use as the significant determinants for acceptance of new system. So the user recognizing the usefulness of the internet banking benefits and having expertise on using would have positive perceptions towards its use and perceive it less complex to use(Black et al., 2001;Polasik & Wisniewski ,2009). The impact of experience have been validated in digital transactions in previous studies on probability of using online shopping (Lee and Lee, 2000; Polasik & Wisniewski, 2009 ;Lee et al.,2005). Moreover technology acceptance is based on perceptions of user beliefs ( viz PU and PEOU in TAM). Such beliefs may vary over the period of time as individuals develop experience. Experience was thus believed to be one of the major factors in online context that explains user behaviour and contributes to differences in goal-directed and exploratory online browsing behaviours (Castañeda et al, 2007). Researchers have argued that users with more experience displayed intended behaviour in normal way compared to less experienced ones who seek basic exploration. Yoon (2010) demonstrated distinctiveness among users having high and low level of experiences on basis of knowledge structure (Mitchell & Dacin, 1996; Söderlund, 2002; Yoon, 2010). The difference in the structures of knowledge is visible through various activities associated with information processing, like problem solving, reasoning, induction and opinion formation, information recalling and reconditioning (Maestro et al, 2007). It suggests that individuals evaluate their satisfaction regarding online transactions in different ways based on their experiences (Yoon, 2010).

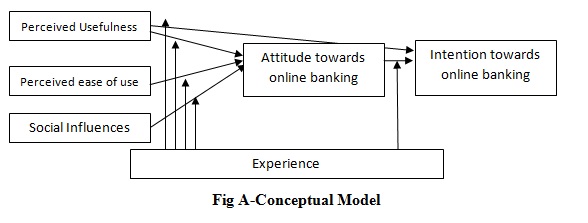

Model and hypotheses- Figure A shows the conceptual model

The previous studies have highlighted the moderating effect of diverse levels of experience on perceived usefulness (Casta˜neda et al., 2007; Gefen et al., 2003). But there is no consensus on impact of PU with different levels of experience. Few researchers advocate the influence of PU increases with increased familiarity with information technology (Karahanna et al., 1999) and PU is higher for experienced e-customers (Hernández et al, 2010). The users with higher levels of experience will give emphasis on PU prior to system use (San José, 2007). On the contrary , some researchers argue that impact of PU becomes stronger for individuals with low levels of experience (Taylor and Todd, 1995; Yu et al., 2005).The relationship between PU and attitude would be strong where level of experience is less in similar technology regarding a new system(Liébana-Cabanillas et al, 2014). Some authors suggested that PU has no significant impact on either of the experience levels (Bhattacherjee and Prekumar, 2004).

This study proposes that PU has high influence to users with high experience.

H1. PU has high influence on adoption intention of users with high experience

Taylor and Todd (1995) advocated that individuals having no experience emphasize on ease of use first and further to addressing their issues the focus is shifted towards usefulness. Castaneda et al. (2007) investigated that the association between ease of use and behaviour and found that it is significant for users with low levels of experience. Davis (1989) found that the influence of PEOU disappeared when users worked on IT for 14 weeks.

Hence the study proposes that:

H2. PEOU has high influence on adoption intention of users with low experience levels

As the online banking is new technology and individuals might have feelings of uncertainties about the possible consequences of its use. In such cases the user intends to minimize this fear and uncertainty by taking opinions of friends, family and significant others (Liébana-Cabanillas et al, 2014). Davis et al (1989) created the TAM model that has been extended in various ways in many research pertaining to the online and technology adoption owing to its strong predictive power and parsimonious nature. TAM has been extended in multiple ways to identify the system acceptance across various scenarios.

With growing technologies, the social network groups have become sound platforms for information sharing and interacting. Interactions among online buyers create a distinct community that influences business value. Such influences could also lead to building loyalty among customers. Increasing frequency of online transactions by the committed buyers may influence more users to follow it. The role of opinion leaders or community heads, impact of word-of-mouth communication could go act as catalyst in enhancing the image of online sellers. In case of online banking services, as the user gains experience with the system intrinsic fears tends to disappear. The higher levels of experience minimize the user’s tendency to depend on his reference groups for opinions and consultations and are therefore capable of handling issues himself.

Hence the study proposes that

H3. Social Influence has less influence on adoption intention of users with high experience levels

The PU has positive influence on the user intentions for acceptance and use of new systems.

Hence, the study proposes that:

H4. PU has positive influence on adoption intention of users

The user attitude influence their intentions for acceptance of IS systems. Positive attitude towards e-banking adoption creates higher positive intention for adoption or continued use (Püschelet al., 2010). There was no evidence in the literature pertaining to the relationship between attitude towards adoption and intention to adopt has been tested for moderation with different levels of experience groups.

Hence, the study proposes that:

H5. Attitude has positive influence on adoption intention of users

Research Methods

- Sample and Data Collection

The study was conducted by gathering data from mall intercept method where different malls in Delhi and nearby regions were surveyed and data was collected through personal administration. The users were differentiated from non-users using a question on previous use in the survey item. The final responses that were received after excluding the missing and incomplete responses were 354.

3.2. Instruments and Measures

The scale items were identified on basis of extensive literature review. The items Peou and PU were taken from Davis et al.(1989) and (Luarn and Lin(2005), social influence was from Venkatesh et al. (2003), attitude and behavioural intention Taylor and Todd (1995). A seven-point Likert-type scale was used where 1 indicated strongly disagree and 7 as strongly agree.

Results

Measurement model

The analysis began with refining of the scale items by conducting exploratory factor analysis (EFA) that resulted in reduction of scale items. The original 7 items in Peou were reduced to 4, 5 items in PU were reduced to 3. Rest all remained same. It was followed by CFA that indicated positive model fit as shown in the Table 1a below:

|

CMIN/DF

|

RMR

|

GFI

|

CFI

|

RMSEA

|

|

1.561

|

0.044

|

.956

|

0.984

|

0.04

|

Table 1a

The face validity was achieved by in depth literature review. The discriminant validity and convergent validity were analysed through the AVE values and indicated higher scores then inter-construct correlations (Fornell and Larcker, 1981). The loadings were over 0.70 and hence were significant. Also, AVE values for all the latent constructs was greater than the inter-construct correlations (Fornell and Larcker, 1981). Hence, discriminant validity and convergent validity were achieved.

Structural model

The path analysis was done through building and analysing the structural model. The model fit thus achieved was significant. The scores are shown in Table 1b below:

|

CMIN/DF

|

RMR

|

GFI

|

CFI

|

RMSEA

|

|

1.581

|

0.048

|

0.954

|

0.983

|

0.041

|

Table 1b

The analysis revealed that all hypothesis were significant at value of p less than 0.05 other than H1 and H2 as shown in the table below:

Table 2 : Hypothesis testing

|

Hypothesis

|

|

Path

|

|

Estimates

|

p-value

|

Results

|

|

H1

|

Attitude

|

<---

|

PU

|

-0.055

|

0.783

|

Not Supported

|

|

H2

|

Attitude

|

<---

|

PEOU

|

0.264

|

0.087

|

Not Supported

|

|

H4

|

BI

|

<---

|

PU

|

0.247

|

***

|

Supported

|

|

H3

|

Attitude

|

<-

|

SI

|

0.491

|

***

|

Supported

|

|

H5

|

BI

|

<---

|

Attitude

|

0.673

|

***

|

Supported

|

The significant paths were tested for moderation effect due to experience. Experience is calculated on two basis a.) based on the Frequency of use and b.) Length of time it is being used. Based on frequency, three groups emerged after merging the relatively smaller groups. These are listed in Table #3a. Based on experience, parameter which was based on time four groups emerged after merging the smaller groups. These are listed in Table #3b. There 3x4 groups were possible in total. However, one group, which comprised of only 3 responses was dropped from further analysis. This group was characterised by rare user who were using online medium since more than 3 years. Another group comprising of less than 3 month old users was merged with less than one year old users who were all frequent user so as match the group sizes with other frequent user groups. Finally 10 group emerged, which are listed in Table 3c

|

Group

|

Size

|

|

Weekly

|

122

|

|

Monthly

|

132

|

|

Rarely

|

98

|

Table 3a : Experience-Frequency

|

Group Name

|

Size

|

|

Less than 3 months

|

86

|

|

3 months to 1 year

|

91

|

|

1-3 years

|

111

|

|

more than 3 years

|

66

|

Table 3b : Experience-Time

|

Frequency

|

Duration

|

Group

|

Size

|

|

Weekly

|

less than 1 year

|

1

|

36

|

|

Weekly

|

1-3years

|

2

|

41

|

|

Weekly

|

>3years

|

3

|

45

|

|

Monthly

|

<3months

|

4

|

33

|

|

Monthly

|

3-12months

|

5

|

34

|

|

Monthly

|

1-3years

|

6

|

47

|

|

Monthly

|

>3years

|

7

|

18

|

|

Rarely

|

<3months

|

8

|

32

|

|

Rarely

|

3-12months

|

9

|

41

|

|

Rarely

|

1-3years

|

10

|

22

|

Table 3c : Combined Groups

These 10 groups were used to conduct the moderation analysis for the three hypothesized paths. Frequency group-wise differences were calculated. This for the groups viz., Weekly, Monthly and Rarely the groups within them were compared and no inter-frequency groups were compared.

Path from SI to attitude:

The weekly group with less than one year showed moderation effects on social influences influencing attitude higher in comparison with rest of the groups. Interestingly the 3 year and higher group exhibited comparable behavior, not much deviant from the new groups. The monthly group was studied having four sub-groups. The users between 3 months to one year old and the one having more than 3 years’ experience observed sporadic moderation effects. Amongst the rare users identified by usage on internet less than one time in a month, there was no effect of moderation observed.

Path from attitude to intention:

Impact of experience on attitude to behavioral intentions was highly significant where the new group demonstrated high beliefs towards attitude intentions path that leads to adoption of internet banking. But the group with experiences higher than 1 year exhibited dissimilarities. The monthly group showed no effect of moderation. The monthly users observed no moderations effects.

Path from PU to attitude:

This path also observed high moderation affects. The more than 3 year users demonstrated strong beliefs as compared to the rest of the groups. Rather the other two groups performed in similar manner. The rare group demonstrated high influence of moderation effect in this path. In fact the users between 1 month to 1 year showed higher positive beliefs as compared to more than 3 year experience group.

Path from PU to intention:

The effect of moderation for the monthly group was not observed in this path other than the users less than 3 months and more than 3 years’ experience. The effect of moderation was also observed in this path for the rare group. The effect was lowest for the less than 3 months. The highest effect was observed with more than 1 year experience group.

Discussion and Implications

The results show that hypothesis 3, 4 and 5 are supported indicating perceived usefulness influences behavioural intention in positive manner. Social influences have positive influence on attitude. The most significant path is influence of attitude on the user intention. Hypothesis 1 and 2 however are not supported indicating that perceived usefulness and perceived ease of use are not significant in influencing user’s attitude. Thus, customers perceived no affect on attitude toward adoption based on their perceptions of usefulness and ease of use of online banking services. This result is not consistent with the TAM findings. The inconsistency may be attributed to the fact that when the customer finds the service is increasing his work efficiency and performance it directly influences the intention to adopt so attitude has no significant role. In case of perceived ease of use, till the system is new and user is relatively less experienced ease of use is an important factor. Since the study is carried on users of online banking so it is possible that the users have already dealt with system complexity and are aware and familiar with the design and features of the application and do not find it complex or difficult to operate. Therefore significance of ease of use on attitude diminishes.

Looking at the moderating effect of the experience three frequency groups were analysed within their sub-groups for the moderating effect of the three aforementioned hypotheses, which were significant. For weekly users it is found that the effect of social influence is stronger for the newer or older groups however this effect diminishes after one year which. This suggests that during first year of adoption the individuals require high social support to develop a positive attitude towards adoption. Later the use of internet for banking becomes less complex. Developing the attitude is more critical during the initial year of use. Rendering high level of social influence during this phase could form the attitude for a continued use. After 3 years, this social support could be invigorated again because of enhancements in the services, changes in the features, new services offerings etc. In fact the continued users could also be rewarded for staying loyal to the company by various means such as giving freebies, bonuses etc. For the path leading from attitude to intention, the intensity reduces over the period of time. This means that the attitude needs to be reinforced else there is chance for the frequency of usage to go down. The perceived usefulness of technology adoption leading to intention to adopt has been given more weight by the users who had been long time users in comparison to the relatively new users. This means that the minimum of once in week login is must and this shall continue at least for three years. This achievement must be rewarded by the service providers in form of gifts.

The monthly users behaved a bit sporadically. This can be due to the possibility of forgetting the passwords, which might restrict the use or the users might just want to check their salaries, which is of course once in a month. The monthly user group appears critical in the time range of 3 month to 1 year as their continuity of monthly service use requires high degree of social support as compared to other groups to possess high levels attitude. Though the group between 1 and 3 years has similar behavior but the need of social support is not that critical.

The behavior of all monthly groups was alike for path between attitude and intention. But the beliefs regarding PU were critical between the groups. The impact PU was felt highest by the newest group having less than 3 months of experience as compared to the rest of the groups. Hence the usefulness of internet banking must be emphasized and communicated intensively to the new users to ensure the progressive use of services over a period of time.

The rare users who use the internet services less than once a month were analysed among the three sub-groups. For this set of users, the role of social influence in forming the attitude towards adoption is perceived invariably among the sub-groups. However, the slight difference among the sub-groups is accounted higher for the oldest group that despite being infrequent users they still exist for long time with the online services. It is likely that they may be more frequent with the competitors. The influence of attitude on intention is well moderated. The users who are less than a year old have a different perception than the users who are more than a year old. Their newer users are still more positive towards their intention to adopt than the older ones. However, it is to be well noted that the attitude towards adoption which is influencing the intention to adopt online is not differently perceived based on social influence hence this attitude formation for the users with low frequency should be further explored for its antecedents. The role of perceived usefulness in influencing the intention to adopt is also moderated for the rare users. The newer users who might have used the services once or twice in 3 months may have used it out of curiosity. The oldest users might have perceived this path in a similar way and would have remembered somehow about their enrolment with the online services and would have used it when there was no other solution available and hence the role of perceived usefulness holds the key. This solution might be positioned in the promotion for increasing the frequency of the users. The users who are 3 months to 1 year old might be little sceptical as they might be weighing other competitive options.

The study provides useful implications for academicians and the practicing managers. The theoretical implications involve contribution to the existing body of knowledge and deeper understanding of the technology adoption behavior and impact of experience on various levels. This work is among the few studies conducted where experience is used as a moderating variable to understand e-user behavior differentiated on basis of different levels of experience. Experience influences user’s attitude and intention in a big way so it is essential that online banking service provider make a distinction between users’s with high and low experience levels. Social influence had adequate impact on attitude towards online banking intention implying that the online banking users are greatly influenced by the views and opinions of friends, family and significant others in their social environment while forming their perceptions. Perceived usefulness is significant in influencing online banking adoption intention that infers that usability of the services are of prime importance and if the customer realizes that online banking is a usable service that could enhance his work and productivity then it would induce change in his perceptions and intentions in a highly positive way.

The corporates may benefit by understanding the impact of social environment on the minds of customer and to what extent it influences their adoption and continuation of the banking services through internet. So the bank managers and the financial providers may consider redefining their image in user’s minds and their social groups to enable positive word-of-mouth promotion of their services and benefits in efficient and highly effective way. Also the companies must ensure web presence on various social networks, discussion forums and chat groups to interact with the current and potential users and handle grievances and receive suggestions. It would facilitate the sharing of information by users and also seek guidance from providers and other users. Deploying such platforms for discussions and criticisms, the service provider projects an image of sincerity, honesty and easy approachability and that would add value to their services significantly. PU places high positive influence on adoption intention of internet banking services. It signifies that with increase in user proficiency he demonstrates higher in-depth assessment of online banking benefits. Hence all sorts of useful and important information must be communicated to the user. It would rather be beneficial to the providers if they identify the key factors that create this positive impact on the users to enhance their offerings for higher satisfaction levels and continued use. Therefore the study provides insights to the practitioners and academicians on how the returning users can be categorized on basis of their experience levels to design and provide more personalized services.

References

- Ajzen, I., & Fishbein, M. (1980). Understanding attitudes and predicting social. Englewood Cliffs, NJ: Prentice-Hall .

- Alba, J.W., & Hutchinson, J.W. (1987). Dimensions of consumer expertise. Journal of Consumer Research, 13, 411–454.

- Bhattacherjee A, Prekumar G. Understanding changes in belief and attitude toward information technology use: a theoretical model and longitudinal test. MIS Quarterly 2004; 28(2):229–54.

- Black, N. J., Lockett, A., Winklhofer, H., & Ennew, C. (2001). The adoption of Internet financial services: a qualitative study. International Journal of Retail & Distribution Management , 29 (8), 390-398.

- Castañeda, J. A., Muñoz-Leiva, F., & Luque, T. (2007). Web Acceptance Model (WAM): Moderating effects of user experience. Information & Management , 44 (4), 384-396.

- Chen, S., & Chaiken, S. (1999). The heuristic-systematic model in its broader context. Dual-process theories in social psychology , 73-96.

- Cheung, W., Chang, M. K., & Lai, V. S. (2000). Prediction of Internet and World Wide Web usage at work: a test of an extended Triandis model. Decision Support Systems , 30 (1), 83-100.

- Reichheld, F. F., & Schefter, P. (2000). E-loyalty. Harvard business review , 78 (4), 105-113.

- Fazio RH, Zanna MP. Direct experience and attitude–behavior consistency. In: Berkowitz L, editor. Advances in experimental social psychology. Academic Press; 1981. p. 161–202. 6.

- Fishbein, M., & Ajzen, I. (1975). Belief, attitude, intention and behavior: An introduction to theory and research .

- Fornell, C. and Larcker, D.F. (1981). Evaluating structural equation models with unobservable variables and measure. Journal of Marketing Research 18(1), 39-50.

- Gefen D, Karahanna E, Straub DW. Inexperience and experience with online stores: the importance of TAM and trust. IEEE Trans. Eng. Manage. 2003;50(3):307.

- Gupta, S., & Kim, H. W. (2007). The moderating effect of transaction experience on the decision calculus in on-line repurchase. International Journal of Electronic Commerce , 12 (1), 127-158.

- Guriting, P., & Ndubisi, N. O. (2006). Borneo online banking: evaluating customer perceptions and behavioural intention. Management research news , 29 (1/2), 6-15.

- Hernandez Maestro, R. M., Munoz Gallego, P. A., & Santos Requejo, L. (2007). The moderating role of familiarity in rural tourism in Spain. Tourism Management, 28(4), 951–964.

- Hernández, B., Jiménez, J., & Martín, M. J. (2010). Customer behavior in electronic commerce: The moderating effect of e-purchasing experience. Journal of Business Research , 63 (9), 964-971.

- Karahanna E, Straub DW, Chervany N. Information technology adoption across time: a cross-sectional comparison of pre-adoption and post-adoption beliefs. MIS Quarterly 1999;23(2):183–213.

- Karahanna, E., & Straub, D. W. (1999). The psychological origins of perceived usefulness and ease-of-use. Information & Management , 35 (4), 237-250.

- Kim, J., Spielmann, N. and McMillan, S.J. (2012), “Experience effects on interactivity: functions, processes and perceptions”, Journal of Business Reasearch, Vol. 65 No. 11, pp. 1543-1550.

- Koufaris, M., Kambil, A., & LaBarbera, P. A. (2002). Consumer behavior in web-based commerce: an empirical study. International Journal of Electronic Commerce , 6 , 115-138.

- Lee, E. J., Kwon, K. N., & Schumann, D. W. (2005). Segmenting the non-adopter category in the diffusion of internet banking. International Journal of Bank Marketing , 23 (5), 414-437.

- Lee, E., & Lee, J. (2000). Haven’t adopted electronic financial services yet? The acceptance and diffusion of electronic banking technologies. Financial Counseling and Planning , 11 (1), 49-60.

- Lee, H., Choi, S.-Y. and Kang, Y.-S. (2009), “Formation of e-satisfaction and repurchase intention: moderating roles of computer self-efficacy and computer anxiety”, Expert Systems with Applications: An International Journal, Vol. 36 No. 4, pp. 7848-7859.

- Liang, T.-P. and Huang, J.-S. (1998), “An empirical study on consumer acceptance of products in electronic markets: a transaction cost model”, Decision Support Systems, Vol. 24 No. 1, pp. 29-43.

- Liébana-Cabanillas, F., Sánchez-Fernández, J., & Muñoz-Leiva, F. (2014). The moderating effect of experience in the adoption of mobile payment tools in Virtual Social Networks: The m-Payment Acceptance Model in Virtual Social Networks (MPAM-VSN). International Journal of Information Management, 34(2), 151-166.

- Mäenpää, K., Kale, S. H., Kuusela, H., & Mesiranta, N. (2008). Consumer perceptions of Internet banking in Finland: The moderating role of familiarity. Journal of retailing and consumer services, 15(4), 266-276

- Mitchell, A. A., & Dacin, P. A. (1996). The assessment of alternative measures of consumer expertise. The Journal of Consumer Research, 23(3), 219–239

- Pappas, I. O., Pateli, A. G., Giannakos, M. N., & Chrissikopoulos, V. (2014). Moderating effects of online shopping experience on customer satisfaction and repurchase intentions. International Journal of Retail & Distribution Management , 42 (3), 187-204.

- Polasik, M., & Wisniewski, T. P. (2009). Empirical analysis of internet banking adoption in Poland. International Journal of Bank Marketing , 27 (1), 32-52.

- Püschel, J., Mazzon, J. A., & Hernandez, J. M. C. (2010). Mobile banking: proposition of an integrated adoption intention framework. International Journal of Bank Marketing , 28 (5), 389-409.

- Rodgers, W., Negash, S., & Suk, K. (2005). The moderating effect of on‐line experience on the antecedents and consequences of on‐line satisfaction. Psychology & Marketing , 22 (4), 313-331.

- L. Jarvenpaa and P. A. Todd, “Consumer reactions to electronic shopping on the world wide web,” Int. J. Electron. Commerce, vol. 1, no. 2, pp. 59–88, 1997.

- San José, R. (2007). Ejecución y eficacia de la publicidad online. Los sitios web de lasagencias de viajes (doctoral thesis). Universidad de Valladolid.

- Söderlund, M. (2002). Customer familiarity and its effects on satisfaction and behavioral intentions. Psychology & Marketing, 19(10), 861–879.

- Sun, H., & Zhang, P. (2006). The role of moderating factors in user technology acceptance. International Journal of Human-Computer Studies , 64 (2), 53-78.

- Taylor S, Todd PA. Assessing it usage: the role of prior experience. MIS Quarterly 1995;19(4):561–70.

- Taylor, S., & Todd, P. A. (1995). Understanding information technology usage: a test of competing models. Information systems research , 6 (2), 144-176.

- Triandis, H. C. (1979). Values, attitudes, and interpersonal behavior. In Nebraska symposium on motivation . University of Nebraska Press.

- Yoon, C. (2010). Antecedents of customer satisfaction with online banking in China: The effects of experience. Computers in Human Behavior , 26 (6), 1296-1304.

- Yoon, C. (2010). Antecedents of customer satisfaction with online banking in China: The effects of experience. Computers in Human Behavior , 26 (6), 1296-1304.

- Yu J, Ha I, Choi M, Rho J. Extending the Tam for a t-Commerce. Inf Manag 2005;42(77):965–76.

- Laforet, S., & Li, X. (2005). Consumers' attitudes towards online and mobile banking in China. International Journal of Bank Marketing, 23(5), 362-380.

- Heikki, K., Minna, M., & Tapio, P. (2002). Factors underlying attitude formation towards online banking in Finland. The International Journal of Bank Marketing, 20(6), 261

- Calin, G. (2002). Online banking in transition economies: The implementation and development of online banking systems in Romania. The International Journal of Bank Marketing, 20(6), 285.

- Tero, P., Kari, P., Heikki, K., & Seppo, P. (2004). Consumer acceptance of online banking: an extension of the technology acceptance model. Internet Research, 14(3), 224.

- Kari, P., Tero, P., Heikki, K., & Seppo, P. (2006). The measurement of end-user computing satisfaction of online banking services: empirical evidence from Finland. The International Journal of Bank Marketing, 24(2/3), 158.

- Ouma, B. O., Ndirangu, A. W., Munyaka, F. G., George, G. E., Mandere, E. N., Maringa, A. K., Javan M. Nguthuri, Susan N. Nyokabi, Mercy Njenga, Kagumba, A. M., Bichanga, J. Owusuah, L (2012), ‘A Cognitive Model of the Antecedents and Consequences of Satisfaction Decisions’, Journal of Marketing Research, Volume 17, No 2

- Cvent (2013), Customer Retention, www.cvent.com retrieved on Friday, 10th May, 2013

Fatma, S. (2014). Antecedents and Consequences of Customer Experience Management-A Literature Review and Research Agenda. International Journal of Business and Commerce, 3(6), 32-49.