A Refereed Monthly International Journal of Management

A Study on Impact of Demonetization on Indian Stock Market and Selected Sectors of Indian Economy

Ashok Bantwa

Assistant Professor,

Faculty of Management,

GLS University, Ahmedabad,

Gujarat.

Address: S-501, ICB Flora,

Opp Silvernest, Gota Cross Road,

Gota, Ahmedabad .

Contact No: 9727575382

Abstract

While addressing India in his historical speech on 8th November, 2016, prime minister of India, Narendra Modi announced that two highest denomination currency notes in India (500 rupee notes and 1000 rupee notes) will not remain legal tender. Demonetization is one of the most remarkable decisions of Indian government aimed at eradication of black and counterfeit money and control of terror funding. This decision is expected to bring significant change in mode of payment used by Indian people and will transit India towards the cashless economy. Undoubtedly the exact impact of demonetization on Indian economy can be figured out only in long run but in short run demonetization has considerable impact on people, businessmen, small and medium scale industries, companies and economy. This paper examines the impact of demonetization decision on Indian stock exchange as represented by NIFTY index of National Stock Exchange .The paper further examines the impact of demonetization decision on various sectors of Indian economy as represented by various sectoral indices of National Stock Exchange. These sectors include Automobile, Banking, FMCG, Information Technology, Media, Metals, Pharmaceuticals, Real estate, Infrastructure, Private sector banks, Public sector banks, Financial services and Service sector. The result of this study indicated that demonetization has statistically significant impact on all the indices under study. Considering the absolute percentage change in closing price of indices within 30 days of demonetization decision, demonetization has negative impact on all the indices except IT index. Except media index and pharma index the volatility of all other indices under study has increased considerably due to demonetization. Average closing price of NIFTY for 30 days after the demonetization is 5.78% lower than the average closing prices for 30 days before the demonetization. The absolute fall in NIFTY after one month of demonetization is 5.64%. Among the sectoral indices the highest impact of demonetization is on real estate sector followed by media and automobile sector whereas the lowest impact is on metal index followed by PSU banks and IT sector.

Keywords:Demonetization, Black Money, Liquidity Crunch

Introduction

Demonetization is an act of stripping a currency unit of its status as legal tender. The old currency unit is superannuated and replaced with new currency unit. There might be multiple reasons behind the demonetization of local currency unit. Few objectives of demonetization include fighting inflation, fighting corruption and discouraging cash system. Technically demonetization is a liquidity shock, a sudden stop in terms of availability of currency that is expected to disturb the economic activities. The inadequate supply of currency is expected to hamper consumption, production, investment, employment etc.

In year 2015 government of Zimbabwe decided to demonetize Zimbabwean dollar to fight with the problem of hyperinflation that was hovering to 231, 00,000%. The process that lasted for three months involved purging the Zimbabwean dollar from the financial system of the country and to strengthen the other currencies including US Dollar, South African Rand and Botswana Pula as a country’s legal tender in a bid to stabilize the economy. Another example of demonetization occurred in year 2002 when Euro was adopted as common currency by the nations of European Monetary Union. To switch to Euro zone authorities first fixed exchange rates between various national currencies and Euro. With introduction of Euro the old currencies of various nations of European Monetary Union were demonetized. However to ensure smooth transition through demonetization the old currencies were kept convertible into Euro for a specific period. In 1929 US federal Bank has removed 30% of money in circulation. This decision of federal bank resulted into great depression from 1929 to 1933. Historically the earlier Indian governments also demonetized currency notes. In January 1946, currency notes of Rs.1000 and Rs.10,000 were withdrawn and new currency notes of Rs.1000, 5000 and 10,000 were introduced in 1954. In order to fight with counterfeit money and black money the Janta Party coalition government had again demonetized currency notes of Rs.1,000, 5,000 and 10,000 on January 16, 1978.

While addressing India in his historical speech on 8th November, 2016, prime minister of India Narendra Modi announced that two highest denomination currency notes in India (500 rupee notes and 1000 rupee notes) will not remain legal tender. The demonetization decision was announced at midnight on November 8. Through this decision nearly 86% of the currency in circulation was withdrawn. This historical decision was aimed at manifold objectives like curbing black money, eradicating counterfeit currency notes, combating terror financing, controlling tax evasions and a shift towards cashless economy. The decision was further aimed at bringing more people under formal banking system. According to Reserve Bank of India’s annual report for the period April 2015 to March 2016, the total value of currency notes at the end of March 2016 was 16.42 Indian trillion rupees. The 500 and 1000 currency notes consisted of 86.4% of total value of currency in circulation. RBI database also indicates that at the end of March 2016, total 6, 32,926 fake Indian currency notes were in circulation. The withdrawal of Rs. 100 and Rs. 1000 currency notes resulted into huge gap in currency composition as after Rs.100, Rs.2000 is the only denomination. It would not be a hyperbole that demonetisation announced by the Prime Minister of India have been one of the largest self-inflicted macroeconomic shocks on a country in the absence of a short term crisis. Such a large and unexpected policy change naturally carries with it a large collateral damage at least in the short run. This is particularly true for India where a large section of the economy is comprised of the informal or unorganized sector (not registered with the government and hence not subject to taxation) which functions on cash, but is not illegal.

The demonetization would be a memorable experience of this generation and is going to be the most remarkable event of our times. The decision is expected to have far reaching impact on India Economy. However during the days following demonetization banks and ATMs across the country have witnessed long queues of people struggling to exchange their old currency notes and withdrawing scarcely available new currency notes. People across the country have witnessed the acute shortage of new currency notes from ATMs and banks. Many tried to save their dying cash by making investment in gold whereas many relied on their near and dear ones to transfer their unrecorded cash piled at their home. Demonetization resulted into several detrimental effects on small businesses, workers, laborers, shopkeepers, agriculture and transportation. Reacting strongly to the announcement of demonetization decision two major stock market indices in India BSE SENSEX and NSE NIFTY 50 plunged sharply for two days. At an aggregate level, this move will significantly eliminate the existing stock of black money, fake currency and will benefit the economy in the medium- to long-run, but, the question as to how the creation of black money in the future will be prevented still remains unanswered.

Reviews of Literature

The effects of demonetization is an unexplored and untouched topic by researchers. Furthermore the demonetization in India is of very recent time so no good number of studies have been conducted on this topic. This results in scarcely available reviews of literature for the topic under study. However I referred to the following literature available about the demonetization.

Sunita (2014) undertook a study to understand the reasons and steps taken by the government on the major demonetizations that took place in India. The study was further aimed at examining the implications of depreciation of rupee on Indian economy. The author also studied the impact of depreciating rupee on Indian economy and concluded that in long run with weakening rupee, Indian economy has more to lose and less to gain. The paper also threw light on the importance of the central bank’s intervention to control the situation.

Chatterjee and Banerji (2016), discussed the general impact of demonetization on Indian economy and specific impact on various sectors. As per them the demonetization of 500 and 1000 notes will have significant and immediate impact on Indian economy. Demonetization resulted into increase in bank’s deposit level due to more number of deposits with banks. Further financial savings are expected to increase as a result of shift from unproductive physical asset based savings to interest bearing financial assets. This in turn is expected to increase the banks liquidity position, which can be leveraged by them for lending purposes. As the demonetization is expected to result in low preference for informal funding sources, the real estate sector is expected to have an adverse impact in terms of demand. Luxury property rates are expected to fall as result of fewer purchasers with substantial liquidity. The demonetization measures are also expected to affect the cash transactions in Automobile Industry, predominantly in auto ancillary and two wheelers industry.

Rao Kavita and Mukherjee Sacchidananda, (2016) evaluated short and medium run impact of demonetization on economy through a working paper. They opined that the impact of demonetization would depend upon the extent to which government decides to go for remonetization. The paper throws light on the impact of demonetization on various factors like availability of credit, level of activity, spending and government finances. They concluded that the demonetization is a large shock for the economy and the medium term impact of this shock will depend upon the extent to which currency is replaced by the government and the extent to which currency in circulation is extinguished. Further they stated that extinguishment of huge portion of exiting currency would result in contraction of economic activities and that would be the material cost that need to be considered while evaluating the impact of demonetization. They also emphasized on acute need for significant up gradation of banking system and telecom infrastructure that would serve as backbone for digital transactions and behavioral change in people to adapt the substitutes of cash for both making and receiving payments.

Sabnavis, Sawarkar and Mishra (2016) in their report on economic policy review of CARE ratings they highlighted the probable consequences of demonetization decision on different economic variables and entities. Talking about the impact on parallel economy they opined that the decision will eradicate the huge chunk of black money and counterfeit money from the economy and will significantly curb the funding for the various anti-social activities like terrorism, smuggling, espionage etc. Explaining the impact on overall demand they expected the large contraction in overall demand and particularly in sectors like consumer goods, real estate, automobiles etc. They further forecasted improvement in liquidity position of banks, which can be leveraged for lending purposes. It was further observed that with cash transactions facing reduction, the alternative forms of payment will experience sharp increase in demand.

Litwack M. John (2000) studied the causes and impacts of demonetization in Russia in his paper titled “The Demonetization of Russian Economy: causes and policy options”. They stresses two primary structural factors that have contributed to demonetization: the conditions under which natural monopolies and subnational administrations operate in the Russian Federation. The former causes are related to the particular status of natural monopolies as quasi-fiscal organizations in Russia. The demonetization process can be understood largely as a consequence of the combination of these factors, the tightening of monetary policy, and administrative increases in relative prices of natural gas between 1994-98.

Rationale for study

Overnight, on the orders passed by our Prime minister Narendra Modi all Rs.500 and Rs.1000 currency rupee notes in circulation that consisted near about 86% of currency in circulation were declared obsolete. This decision seemed to catch everyone on hop. The decision is being flaunted as a surgical strike on black money and counterfeit money aimed at breaking down the parallel economy running on unaccounted cash accumulated through tax evasion. The decision was expected to have a significant impact on Indian economy in general and on various sectors of Indian economy in particular in short, medium and long run. Though the long term impact of the decision is to be observed in times to come, this paper is aimed at studying the impact of demonetization decision on Indian stock market and on various sectors of Indian economy, over the period of one month since the demonetization decision was announced. The paper examines the impact of demonetization decision on Indian stock exchange as represented by NIFTY index of National Stock Exchange. The paper further examines the impact of demonetization decision on various sectors of Indian economy as represented by various sectoral indices of National Stock Exchange. These sectors include Automobile, Banking, FMCG, Information technology, Media, Metals, Pharmaceuticals, Real estate, Infrastructure, Private sector banks, Public sector banks, Financial services and Service sector.

Methodology

This paper examines the short term impact of demonetization decision on NIFTY and various sectoral indices over the period of one month from the announcement of demonetization decision. Impact of demonetization on NIFTY and various indices is studied by comparing the data of closing prices of these indices for 30 days before(26th September 2016 to 7th November 2016) and 30 days after (9th November 2016 to 21st December 2016) the demonetization decision. The paper also study the impact of demonetization decision on the volatility of various indices by comparing the volatility for 30 days before and 30 days after the demonetization decision. To study the statistical significance of the impact of demonetization decision paired t-test is used. Paired t-test is a way to test for comparing two related samples, involving small values of ‘n’ that does not require the variances of the two populations to be equal, but the assumption that the two populations are normal must continue to apply. Symbolically,

with (n -1) degree of freedom

The paper further examines the impact of demonetization on above indices for the period of one week, two weeks, three weeks and four weeks from the date of announcement of the decision. The data of closing prices of various indices under study has been collected from the website of national stock exchange.

Hypothesis

The following hypothesis have been made and tested using the paired t-test

H0: There is no significant difference between average closing price of index for 30 days before and 30 days after the demonetization decision.

H1: There is significant difference between average closing price of index for 30 days before and 30 days after the demonetization decision.

Empirical findings and Analysis

This section of paper covers empirical findings and analysis of the topic under study. The demonetization was one of the bold decisions expected to have significant impact on Indian stock market and various sectors of Indian Economy. The market responded strongly to the decision.

Table – 1 – Impact of Demonetization on various indices under study

|

Indices

|

Change in Index Level

|

Change in Volatility

|

|

30 Days Average (Before)

|

30 Days Average (After)

|

% Change in average

|

Absolute % Change from Nov 9 to Dec 21

|

30 Days Volatility (Before)

|

30 Days Volatility (After)

|

% Change volatility

|

|

NIFTY

|

8647.76

|

8148.15

|

-5.78

|

-5.64

|

93.30

|

122.24

|

31.02

|

|

Auto

|

10107.65

|

9062.88

|

-10.34

|

-10.58

|

140.06

|

252.01

|

79.93

|

|

Bank

|

19447.63

|

18621.04

|

-4.25

|

-7.26

|

244.14

|

507.30

|

107.79

|

|

Fin Services

|

8012.60

|

7540.63

|

-5.89

|

-8.59

|

101.48

|

170.34

|

67.85

|

|

FMCG

|

21603.87

|

20300.55

|

-6.03

|

-9.55

|

239.98

|

416.17

|

73.41

|

|

Infrastructure

|

2842.00

|

2735.43

|

-3.75

|

-2.68

|

38.11

|

40.12

|

5.27

|

|

IT

|

10226.18

|

9862.69

|

-3.55

|

2.20

|

172.41

|

273.53

|

58.64

|

|

Media

|

2961.48

|

2612.67

|

-11.78

|

-10.79

|

82.56

|

79.28

|

-3.98

|

|

Metal

|

2642.37

|

2742.71

|

3.80

|

-1.15

|

71.82

|

81.56

|

13.56

|

|

Pharama

|

11467.02

|

10839.79

|

-5.47

|

-2.85

|

257.01

|

212.84

|

-17.19

|

|

Private Banks

|

10861.38

|

10269.42

|

-5.45

|

-9.00

|

145.25

|

295.46

|

103.41

|

|

PSU Banks

|

3149.59

|

3196.51

|

1.49

|

-0.42

|

69.46

|

99.83

|

43.72

|

|

Real Estate

|

206.63

|

165.31

|

-19.99

|

-15.41

|

4.62

|

4.76

|

2.97

|

|

Service Sector

|

10957.99

|

10390.27

|

-5.18

|

-5.23

|

126.75

|

147.57

|

16.43

|

Source: NSE website

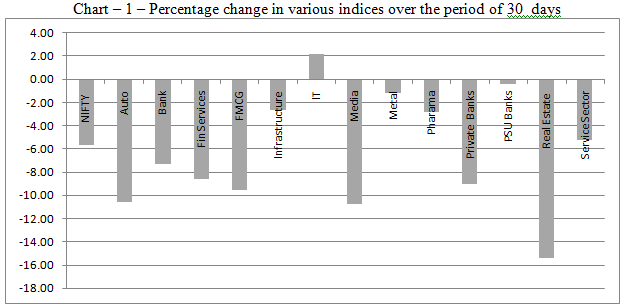

Chart – 1 – Percentage change in various indices over the period of 30 days

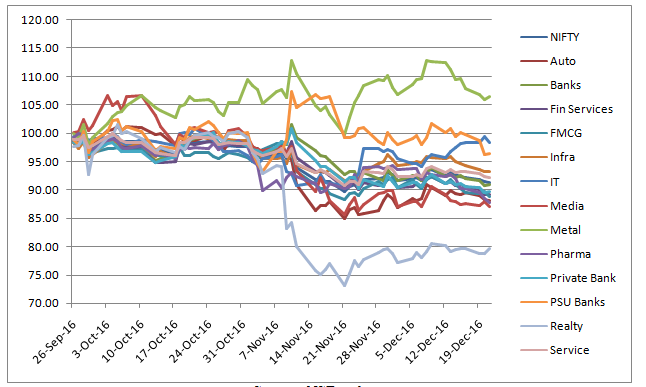

Chart 2 Movement in various common size indices

Source: NSE website

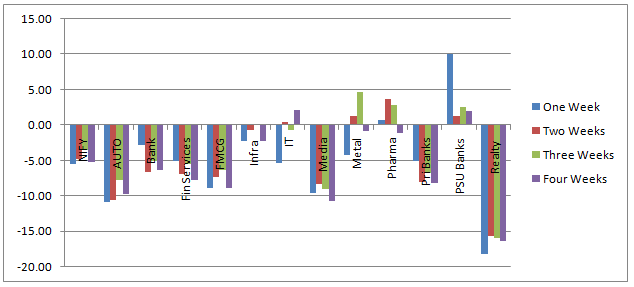

Chart 3 Percentage change in various indices over the different time periods

Source: NSE website

Table 2 Result of paired t-test

|

Indices

|

Calculated Value

|

Tabudlated Value

|

P-Value

|

Result

|

|

NIFTY

|

19.16

|

2.05

|

0.00

|

Null Rejected

|

|

Auto

|

17.85

|

2.05

|

0.00

|

Null Rejected

|

|

Bank

|

9.23

|

2.05

|

0.00

|

Null Rejected

|

|

Fin Services

|

16.05

|

2.05

|

0.00

|

Null Rejected

|

|

FMCG

|

18.45

|

2.05

|

0.00

|

Null Rejected

|

|

Infrastructure

|

11.76

|

2.05

|

0.00

|

Null Rejected

|

|

IT

|

4.50

|

2.05

|

0.00

|

Null Rejected

|

|

Media

|

15.30

|

2.05

|

0.00

|

Null Rejected

|

|

Metal

|

-5.48

|

2.05

|

0.00

|

Null Rejected

|

|

Pharama

|

13.90

|

2.05

|

0.00

|

Null Rejected

|

|

Private Banks

|

10.99

|

2.05

|

0.00

|

Null Rejected

|

|

PSU Banks

|

-2.23

|

2.05

|

0.03

|

Null Rejected

|

|

Real Estate

|

33.44

|

2.05

|

0.00

|

Null Rejected

|

|

Service Sector

|

16.20

|

2.05

|

0.00

|

Null Rejected

|

Table 1 summarizes the impact of demonetization on NIFTY (Representing Indian Stock Market) and various sectoral indices (Representing various sectors of Indian Economy) by comparing average closing prices for the period of 30 days before and 30 days after the announcement of demonetization decision. It also depicts the impact of demonetization on volatility of NIFTY and other sectoral indices. Chart 1 portrays the absolute percentage change in closing prices of NIFTY and various sectoral indices after 30 days from the date of announcement of demonetization decision. Chart 2 represents the movement in various common size indices over the period of 30 days before and 30 days after the demonetization decision. For this purpose all the indices under study are converted into common size indices by taking the closing price of 26th September as base price. All indices are converted into common size by taking base of 100. In order to study the statistical significance of the demonetization’s impact on various indices, paired t-test is conducted. Table 2 depicts the result of paired t-test.

- Impact on NIFTY

NIFTY index is considered as barometer of Indian economy. Demonetization is expected to have an adverse impact on overall economic activities. During the aftermath of demonetization severe cash crunch has been experienced by people, small businessmen, small and medium scale industries as well as by large companies. Reduced liquidity caused a sharp decline in availability of disposable income that resulted into sharp fall in demand of various products and put the economic activities on hold. Because of this, demonetization was expected to have an adverse impact on stock market. Data shows that as expected, NIFTY responded adversely to demonetization. Average closing price of NIFTY for 30 days after the demonetization is 5.78% lower than the average closing prices for 30 days before the demonetization (Refer to table 1). The absolute fall in NIFTY after one month of demonetization is 5.64%. Demonetization also made NIFTY more volatile. The volatility for 30 days after demonetization is more than the volatility before, by 31.02%. Chart 3 shows that the impact of demonetization on NIFTY diluted gradually over the period of second and third week. Result of paired t-test indicates that at 5% significance level the impact of demonetization on NIFTY is statistically significant. Based on above it can be said that demonetization has significant negative impact on NIFY for short term of one month.

- Impact on Auto Sector

In terms of impact of demonetization on Automobile industry of India it was expected that the demonetization will adversely affect the cash transactions in Indian automobile industry especially for two-wheelers and used car market where most of transactions are cash driven. Further it was expected that demonetization will have significant impact on automobile sector in rural and semi urban regions that caters mostly to two-wheelers and used vehicle markets. As expected, Auto Index of NSE responded negatively to the announcement and average closing price during 30 days post demonetization fell by 10.34%. Among all the indices under this study the third largest negative impact is one auto index. Absolute decline in auto index after one month of announcement is 10.58%. As in case of NIFTY, the extent of impact on auto index also declined gradually after one week. The volatility of Auto index increased by 79.39%. At 5% significance level I failed to accept null hypothesis, this indicates that demonetization had statistically significant impact on Auto Index of NSE over the period of one month.

- Impact on Banking Sector

Demonetization resulted into large deposits of Rs. 500 and Rs.1000 rupee notes with the Banks. Many people have also deposited their black money with the banks to convert it into white money. It was expected that demonetization will bring large amount of cash in circulation within the purview of formal banking system through deposits. Huge inflow of deposits in banks was expected to improve liquidity position of banks, which can be leveraged by the banks for further lending purposes. This entire move was expected to benefit banks by reducing its dependence on high cost borrowings. However in short run Banking sector index of NSE responded negatively to demonetization as evidenced by 4.25% decline in average closing prices for 30 days after demonetization and an absolute decline of 7.26% after one month of announcement. Contrary to NIFTY and Auto index, the impact on banking index has increased gradually during second and third week. The volatility of banking index increased by 107.79%, this is the largest increase in volatility among the selected indices for this study. At 5% significance level the impact on banking index is statistically significant.

- Impact on Financial Services

Due to liquidity crunch and panic among the investors it was expected that there would be short run downfall in demand of financial and investment products. Led by this financial service index of NSE experienced sharp decline of 8.59% over the period of one month of demonetization. Average closing price for 30 days after the demonetization is lower than average closing price for 30 days before demonetization by 5.89%. The extent of volatility during post demonetization has increased by 67.85%. As in case of banking index the extent of impact increased gradually during second and third week. At 5% significance level I failed to accept null hypothesis, this indicates that demonetization had statistically significant impact on financial services index of NSE over the period of one month.

- Impact on FMCG Sector

Acute scarcity of cash among the individuals was expected slowdown the demand of FMCG products in short run. Responding to this FMCG index of NSE fell by 9.55 over the period of one month from the date of demonetization decision. The volatility of FMCG index has increased by 73.41% after the demonetization. The level of impact diluted over the period of second and third week. The impact of demonetization on FMCG sector is statistically significant at 5% significance level.

- Impact on Infrastructure sector

Among other sectors, Infrastructure is one of the least affected sectors of Indian economy. As majority of transactions in infrastructure sector are not driven by cash demonetization has milder impact on infrastructure sector. Index fell by mere 2.68% after on month of demonetization. The average closing price for 30 days after demonetization is lower than the average closing price before demonetization by 3.75%. Increase in volatility of Infrastructure index is 5.27%, that is very low as compared to volatility increase in other indices. At 5% significance level the impact of demonetization on infrastructure index of NSE is statistically significant.

- Impact on IT sector

IT sector is also one of the least affected sectors of Indian economy. As the mode of payment for most of the transactions in IT sector is other than cash, demonetization had milder impact on IT sector. The slighter impact of demonetization was very quickly absorbed by the IT index and it successfully closed positive by 2.20% after one month of demonetization. IT index is the only index out of selected indices that closed positive after 30 days of demonetization. This shows that demonetization has lowest impact on IT sector. However the volatility of IT index has increased by 58.64%. The impact of demonetization on IT index is statistically significant at 5% significance level.

- Impact on Media

After real estate the largest negative impact of demonetization is on media sector. NSEs media index fell by 10.79% after one month of demonetization. The average closing price for 30 days after demonetization is lower than the average closing price before demonetization by 11.78%. Surprisingly the volatility of media index has declined by 3.98%. At 5% significance level demonetization has significant impact on media index of NSE.

- Impact on Metal Index

Metal index is also one of the least affected index among the selected indices. After falling in first week, metal index recovered during the second and third week. 30 days after the demonetization metal index fell slightly by 1.15%. The volatility of metal index has increased slightly by 13.56%. At 5% significance level impact of demonetization on Metal index is statistically significant.

- Impact on Pharmaceutical Sector

As the need for pharmaceutical products like medicines etc. is inevitable and as medical stores and government hospitals were allowed to accept old currency notes, demonetization did not have much higher impact on pharmaceutical sector. Within 30 days from demonetization decision pharma index of NSE fell slightly by 2.85%. The average closing price for 30 days after demonetization is 5.47% lower than the average price for 30 days before demonetization. Index closed positive in first second and third week. The volatility of index fell by 17.19%. At 5% significance level demonetization has significant impact on pharma index of NSE.

- Impact on private sector Banks

Private sector banks were highly affected by demonetization decision. Private sector bank’s index of NSE fell by 9% within 30 days of demonetization. Average closing price for 30 days after demonetization was lower than the average closing price for 30 days after demonetization by 5.45%. The volatility of index has increased by 103.41%. At 5% significance level demonetization had significant impact on private sector bank’s index.

- Impact on public sector banks

Apart from IT companies demonetization also has positive impact on public sector banks. Average closing price of NSE’s Public Sector bank index for 30 days after demonetization is 1.49% higher than the average closing price for 30 days after demonetization. Index closed positive during each of the four weeks after demonetization. The volatility of index has increased by 43.72% after demonetization. At 5% significance level demonetization has significant impact on PUS bank’s index.

- Impact on real estate sector

The worst impact of demonetization is on real estate sector. In real estate sector as majority of transactions are driven by cash and funded by black (unaccounted) money, demonetization has put most of the activities in real estate sector on hold. Cash crunch among the individuals has brought in heavy pressure on demand of homes in real estate sector. Further liquidity shortfall on the part of real estate developers has affected the supply side also. Investors in real estate market are expected to adopt the policy of wait and watch in expectation of decrease in prices. Average closing price of real estate index for 30 days after demonetization is 19.99% lower than average closing average closing price for 30 days after demonetization. The volatility of Index has increased by 2.97% during the post demonetization period. At 5% significance level the impact of demonetization on real estate Index of NSE is statistically significant. In the long run however this measure along with Real Estate Regulation and Development Act 2016 (RERA) will align the real estate sector to the international standards of doing business resulting in more fund flow from institutional investors, banks and higher unit sales.

- Impact on Service Sector

Service sector index of NSE fell by 5.23% after 30 days from the date of announcement of demonetization decision. Average closing price for 30 days after demonetization is 5.18% lower than the average closing price for 30 days before demonetization. The volatility of Index has increased by 16.43%. The absolute decline in index within 30 days of demonetization is 5.23%. At 5% significance level the impact of demonetization on service sector Index of NSE is statistically significant.

Conclusion

Demonetization is one of the most remarkable decisions of Indian government aimed at eradication of black and counterfeit money and control of terror funding. This decision will bring significant change in mode of payment used by Indians and will transit India towards the cashless economy. Undoubtedly the exact impact of demonetization on Indian economy can be figured out only in long run but in short run demonetization has considerable impact on people, businessmen, small and medium scale industries, companies and economy. The result of this study indicated that demonetization has statistically significant impact on all the indices under study. Considering the absolute percentage change in closing price of indices within 30 days of demonetization decision, demonetization has negative impact on all the indices except IT index. Except media index and pharma index the volatility of all other indices under study has increased considerably due to demonetization. Average closing price of NIFTY for 30 days after the demonetization is 5.78% lower than the average closing prices for 30 days before the demonetization. The absolute fall in NIFTY after one month of demonetization is 5.64%. Among the sectoral indices the highest impact is on real estate sector followed by media and automobile sector whereas the lowest impact is on metal index followed by PSU banks and IT sector.

References

- Sunita (2014), Demonetization of Indian rupee against us $: A historical perspective, Discovery , 2014, 23(78), 108-112

- Chatterjee and Banerji (2016), The Impact of Demonetization in India, Squire Patton Boggs

- Rao Kavita and Mukherjee Sacchidananda, (2016), Demonetisation: Impact on the Economy, NIPFP Working paper series , No. 182, 14-Nov-2016, New Delhi.

- Sabnavis, Sawarkar and Mishra (2016), Economic consequences of demonetization of 500 and 1000 Rupee Notes, Economics: Policy View CARE Ratings , November 09, 2016.

- Litwack M. John (2000), Economics Directorate OECD, 75775 Paris Cedex 16, France, March 2000