Pacific B usiness R eview I nternational

A Refereed Monthly International Journal of Management Indexed With THOMSON REUTERS(ESCI)

|

Shikha Goyal Research Scholar Punjabi University, Patiala |

DDr Ambika Bhatia Associate Professor Punjabi University Regional Centre, Mohali |

Banking Sector, being a main player of Money and Capital market in India, performs an essential role in the economic development of the country. Now a day, banks are engaged in wide range of activities, offering variety of financial products and services to huge number of customers. They have also entered into the consultation market and provide comprehensive service package to individual customers and corporate. These customers and corporate need special responsiveness and services that will lead to high customer satisfaction and loyalty and that will lead to high earnings and growth. Focus on upgradation of internal business process is a primary strategic objective to survive in the fierce competition. This paper describes the impact of internal business process perspective while analyzing banks’ performance by taking 4 public sector banks and investigating whether this perspective was same across all the banks. Also the significant variables under internal business process perspective were taken out from the analysis on which banks should focus more.

Keywords: Service, Competition, Internal Business, Customer Satisfaction, Strategic.

1.1 Banking Sector

“With the monetary system we have now, the careful saving of a life time can be wiped out in an eye blink”

Larry Parks, Executive Director, FAME

Could you imagine a world without banks? At first, this might sound like a great thought! But banks (and financial institutions) have become cornerstones of our economy for several reasons. They transfer risk, provide liquidity, facilitate both major and minor transactions and provide financial information for both individuals and businesses.

“Thank God, in joy & sorrow, to deposit & borrow, BANKS ARE THERE, Otherwise, The question would be funny, to keep & get money, HOW & WHERE .........?”

These words of Montek Singh Ahluwaliya indicate the importance of Banks. Banking system occupies an important role in the economy of a nation. In fact, banking system of any country is the lifeblood of an economy. A banking institution is indispensable in the modern society. It plays a pivotal role in the economic development of a country and forms the core of the money market for the country. The banking sector performs three primary functions in an economy; first, the operation of the payment system, second, the mobilization of savings and finally, the allocation of savings to investment projects.

Banking industry has been changed after reforms process. The Government has taken this sector in a basic priority and this service sector has been changed according to the need of present days. Banking sector reforms in India Strive to increase efficiency and profitability of the banking institutions as well as brought the existing banking institutions face to face with global competition in globalization process. Worldwide experience confirms that countries with well developed and market oriented free banking system grow faster and more consistently.

The banking system which constitutes the core of the financial sector plays a critical role in transmitting monetary policy impulses to the entire economic system. An efficient banking structure can promote greater amount of investment which can further help to achieve a faster growth rate of economy. The strength of the economy of any country basically hinges on the strength and efficiency of its financial system, which in turn depends on a sound and solvent banking system.

1.2 Internal Business Process Perspective:

This perspective refers to internal business processes. Metrics based on this perspective allow managers to know how well the Bank is running, and whether its products and services conform to customer requirements (the mission). These metrics have to be carefully designed by those who know these processes most intimately; with Bank’s unique missions these are not something that can be developed by outside consultants.

In addition to the strategic management process, two kinds of business processes may be identified: a) resource management processes, and b) core business processes. Resource management processes are business processes that both acquire and provide appropriate and sufficient resources to the other business processes. By their nature resource management processes are the province of management. They are also often more difficult to measure directly or to find appropriate peer group comparisons. Core business processes are the processes that develop, produce, sell, and distribute an entity’s products and services. These processes do not follow traditional organisational or functional lines, but reflect the grouping of related business activities. Core business processes because of their often more repetitive nature are easier to measure and benchmark using generic measurements and peer group comparisons.

1.3 Key Performance Indicators:

Specific weight of administered if expenses in total revenue, Ratio of timely completed orders, Average product labor-output ratio, Average development time of a new product, Average time from placing the order to its completion, Supplier frequency, Average decision-making time, Turnover of material assets, Labor productivity growth, Efficiency of information systems, Increasing number of IT Systems and Computer Equipment, Specific weight of expenses on IT Systems in the total amount of administrative expenses, Emission of hazardous substances to the environment, Influence of company products to the external environment, Expenses related to correction of mistakes in managerial decisions, Number of properly executive orders, Administrative expenses per employee and many more.

Stan Davis , , Tom Albright (2004): In this quasi-experimental study, they had investigated that bank branches implementing the Balanced Scorecard (BSC) outperformed bank branches within the same banking organization on key financial measures. They had evidently proved that financial performance for branches implementing the BSC are superior when compared to performance of non-BSC implementing branches.

Manjit Singh and Sanjeev Kumar (2007): This paper has concluded that the BSC is both a performance measurement and management system that enables the organizations to clarify their vision and strategy and translate them into action. It provides feedback around both the internal business process and external outcomes in order to continuously improve strategic performance and results. It captures both the financial and non-financial aspects of a company's strategy and discusses cause and effect relationship that drives business success. The Scorecard can be used at different levels: throughout the total organization in a subunit or even at the individual employee level as a "personal scorecard".

P. K. Chakraborty(2007): This study has proved that Balanced Scorecard integrates strategic management, performance measurement, strategic thinking and planning, change management and performance budgeting into a structured framework for building a strategic management system. The BSC is not a Management Control System but itself a Management System with focus on four major areas that can go a long way in successfully implementation of BSC in any organization, be it a manufacturing company or service providing company.

T.K.Mukherjee, Smita Pandit(2009): In this study, Business Balanced Scorecard(BBSC) has been implemented in line with the quality policy at Phoenix Yule Limited(PYL) to improve teamwork, better downtime, efficient processes and customer orientation.In conext of PYL, the balanced scorecard approach provides a clear prescription as to what the company should measure in order to ‘balance’ the financial and operational perspectives.The BBSC concept has provided strategic feedback and learning to the management with a comprehensive picture of business operations.

Zhang and Li (2009) in their theoretical paper on “Study on balanced Scorecard of Commercial Bank in Performance Management System”, examined commercial banks in China and they proposed the BSC as tool to improve the overall performance of commercial banks in China. They advised a method and a strategy for Application in conjunction with restrictions of the BSC. Governance Mechanism for the Balanced Scorecard and performance goals assessment and feedback processes should be established. Update mode of banking services can broaden the field of financial services and improve the quality and the efficiency of financial services. To achieve innovation model, it is necessary to improve the “Smile” services, personal mechanism and incentive mechanism. Banking industry should accelerate the transformation of service delivery model to accelerate the pace of mixed services to enhance international competitiveness. They found that the BSC raised the value of Performance Management Appraisal System based on the introduction of customer factors, internal business processes, employee learning and growth and financial factors.

Giuseppe Tardivo, Milena Viassone(2010): In this study, it has been proved that BSC is a very effective tool for activating a model of transparent and shared governance in the social/assistential system, also if it needs some adjustments. The performance model created in this study is based on economic/financial, learning, internal process and user's need variables and it's able to reflect the contribution of different stakeholders to the final performances of the system both on the demand and the offer side. The results of this study represent only a starting point for the activation of new paths of action by policy makers.

Wu (2012) in his article on “Constructing a Strategy Map for Banking Institutions with Key Performance Indicators of the Balanced Scorecard” presented a structured evaluation methodology to link performance indicators into a strategy map of the Balanced Scorecard for banking institutions. The DEMATEL method was used to determine the casual relationship and strengths of influence among the KPI’s to establish a strategy map and found Customer Satisfaction, Sales Performance and Customer Retention Rate as the three most essential evaluation indicators of banking performance. The results suggested that as there is no one performance indicators that fit to all scenarios so performance indicators should be tailored according to objectives of each individual unit to meet organization’s goals.

Ozturk & Coskun (2014), in their article on “A Strategic Approach to Performance Management in Banks: The Balanced Scorecard”, concluded that BSC is comprehensive method to offer quality and efficient financial services. It is important to adopt innovations in banking sector especially for international competitiveness. They found that it is more beneficial to prepare the balanced scorecard for the banks than to report financial performance only in terms of evaluating performance with a holistic approach. The study basically reveals the balanced scorecard practices in the Literature.

Tariq et al. (2014) in their study on “Investigating the Impact of Balanced Scorecard on Performance of Business: A study based on the Banking Sector of Pakistan” investigated the practicability and effectiveness of setting and implementing the Balanced Scorecard in improving the overall performance of an organization. They found that BSC model in Banks provides favourable outcomes and improves bank’s performance significantly. For the study, Data was collected using Non probability sampling technique through questionnaires which were filled by employees of banks at middle level through survey interview. The regression test and ANOVA was used to test the reliability and validity of the data series. They suggested financial, customer , internal process and learning and growth perspectives has remarkable contribution in improving Bank’s overall performance but the vision & strategy perspective could have insignificant role in Bank’s performance.

Sihra Kirandeep (2015), in her research project on. “The Application of Balanced Scorecard as a Strategic Management Tool at National Bank of Kenya” identified the extent of the adoption of the BSC at National Bank of Kenya and the challenges involved in the adoption of the Balanced Scorecard. A sample of 10 informants from senior management of NBK was taken for the study and data was collected through in depth interview and analysed through content analysis. The study found that NBK uses the BSC as a strategic management tool to help align key objectives to various departmental objectives. It is used in each and every stage of the organization when adopting strategy from formulation, implementation and then evaluation and control. Challenges faced in adoption of BSC included inadequate skills and knowledge on the BSC, cultural changes which lead to lot of confusion within the bank and having KPI’s that are too difficult when staff performance is appraised departmentally. She suggested that all these above challenges should be taken into consideration by any organization when adopting the BSC as a strategic management tool.

3.1 Data collection

Data collection is an integral part of research methodology. It is very important task for the research study. The universe of this paper is restricted with the reference to selected banks, which are providing services in Haryana region. So, researcher has selected 4 public sector banks. Questionnaire was prepared for collecting the data by way of personal in-depth interviews with the public sector bank employees of different branches and through e-mail send to the employees to ask about the factors to be considered under each perspectives of Balanced Scorecard for performance measurement.

Secondary data has been collected from the annual report of the banks, bank’s newsletters, intranet, strategic papers, performance development articles, in-house journals and related websites. The Annual Reports of all the four banks of the 5years i.e. 2010-2011; 2011-2012; 2012-2013; 2013-2014; 2014-2015 has been collected. It includes all ratios which includes the financial ratios, training expenses, credit worthiness, growth in services and products etc. In actual, these reports cover all the prospective question related to analyse the performance of the bank.

3.2 Sample size & sampling method

For the data collection 86 branches were selected randomly on the strata of Scale level and Ratio proportion of branches with total number of branches in the respective district from the four selected banks in Haryana region viz. Bank of India, State Bank of India, Punjab National Bank and Central Bank of India. A total of 400 questionnaires were sent to these 86 branches with a request to get these filled from the bank employees of Scale I, Scale II, Scale III and Scale IV level.

3.3 Statistical Technique:

In this research, for analysing the relationship between the variables under Internal process perspective of Balanced Scorecard with bank performance, One –way ANNOVA was used.

|

Impact of Internal Business Process Perspective while analyzing bank’s performance |

|||

|

Bank Name |

Frequency |

Percent |

|

|

Bank of India |

No |

0 |

0 |

|

Yes |

28 |

100.0 |

|

|

Central Bank of India |

No |

23 |

26.1 |

|

Yes |

65 |

73.9 |

|

|

Punjab National Bank |

No |

32 |

20.5 |

|

Yes |

124 |

79.5 |

|

|

State Bank of India |

No |

27 |

21.1 |

|

Yes |

101 |

78.9 |

|

|

Overall |

No |

82 |

20.5 |

|

Yes |

318 |

79.5 |

|

Table 4.1: Impact of Internal Business process perspective while analyzing the bank’s performance

(Source:Author)

Internal business process means the managers’ knowledge regarding the conformity of products and services of the bank to the requirements of the customer. Bank managers should know the internal processes of the banks to design and deliver the products and services to meet the customer’s need. Out of four banks under study, the maximum consideration to the business process perspective in their bank performance has been given by Bank of India (100%), followed by Punjab National bank (79.5%) and SBI (79% each). Overall, 79% managers consider the importance of internal bank processes perspective in their banks’ performance.

Internal processes are very important for the delivery of products and services to meet the customers’ needs. There is greater need to work on it.

The analysis of internal process perspective for banks under study has been discussed using one way Anova technique. Through one way Anova, the fact was tried to investigate if the above said perspective was same across all the banks.

The following hypothesis was formulated.

Hypothesis -

Ho (d): The internal process perspective was same across all the banks.

H1 (d): The internal process perspective was not same across all the banks.

Table 5.1 exhibits the descriptive statistics of internal business processes perspective of the banks under study. The Bank of India exhibited the highest level of internal processes perspective (4.71, SD = 0.27), followed by State Bank of India (3.39, SD = 1.07). The Central bank exhibited the lowest level of Internal processes perspective (2.70, SD = 1.16). Standard errors (SE) revealed the standard deviation expected in population. The lower and upper bound explains the confidence interval within which the population mean was expected to lie.

Table5.1: Descriptive statistics of Internal Processes Perspective

|

N |

Mean |

Std. Deviation |

Std. Error |

95% Confidence Interval for Mean |

||

|

Lower Bound |

Upper Bound |

|||||

|

Bank of India |

28 |

4.71 |

0.27 |

0.05 |

4.61 |

4.82 |

|

Central Bank of India |

88 |

2.70 |

1.16 |

0.12 |

2.45 |

2.94 |

|

Punjab National Bank |

156 |

2.97 |

0.99 |

0.08 |

2.82 |

3.13 |

|

State Bank of India |

128 |

3.39 |

1.07 |

0.09 |

3.20 |

3.57 |

|

Total |

400 |

3.17 |

1.13 |

0.06 |

3.06 |

3.28 |

(Source:Author)

The homogeneity of variance was also examined using Levene test. The Levene’s test suggested that the variance was not homogeneity across all groups (p<.05). Therefore, robust test of equality of means was used to compare the means instead of F-test. As shown in table 5.2, the Welch and Brown-Forsythe tests suggested that the means were statistically highly significant (p<.05). Which means, the hypothesis4 may be rejected. The internal business processes were not found to be same across the banks.

Table 5.2: Robust Tests of Equality of Means for Internal Processes

|

Statistica |

df1 |

df2 |

Sig. |

|

|

Welch |

171.86 |

3 |

184.92 |

.000 |

|

Brown-Forsythe |

39.66 |

3 |

312.94 |

.000 |

(Source:Author)

Table 5.3 exhibits the results of Bonferroni post hoc test of multiple comparison. The internal process perspective of Bank of India was significantly different from all other banks (p<.05). The internal processes perspective of Central bank of India was found to be different from internal processes perspective of Bank of India and SBI (p<.05) but insignificantly different from PNB (p>.05). The business performance of PNB was found to be significantly different form Bank of India and State Bank of India (p<.05), but not different from Central bank. Internal processes perspective of SBI was significantly different from all other banks (p<.05)

Table 5.3: Bonferroni Post Hoc Test of Multiple comparison

|

(I) Bank Name |

(J) Bank Bank Name |

Mean Difference (I-J) |

Std. Error |

Sig. |

95% Confidence Interval |

|

|

Lower Bound |

Upper Bound |

|||||

|

Bank of India |

Central Bank of India |

2.01732* |

.22211 |

.000 |

1.4284 |

2.6063 |

|

Punjab National Bank |

1.73993* |

.21010 |

.000 |

1.1828 |

2.2970 |

|

|

State Bank of India |

1.32887* |

.21357 |

.000 |

.7626 |

1.8952 |

|

|

Central Bank of India |

Bank of India |

-2.01732* |

.22211 |

.000 |

-2.6063 |

-1.4284 |

|

Punjab National Bank |

-.27739 |

.13647 |

.257 |

-.6393 |

.0845 |

|

|

State Bank of India |

-.68845* |

.14175 |

.000 |

-1.0643 |

-.3126 |

|

|

Punjab National Bank |

Bank of India |

-1.73993* |

.21010 |

.000 |

-2.2970 |

-1.1828 |

|

Central Bank of India |

.27739 |

.13647 |

.257 |

-.0845 |

.6393 |

|

|

State Bank of India |

-.41106* |

.12208 |

.005 |

-.7348 |

-.0874 |

|

|

State Bank of India |

Bank of India |

-1.32887* |

.21357 |

.000 |

-1.8952 |

-.7626 |

|

Central Bank of India |

.68845* |

.14175 |

.000 |

.3126 |

1.0643 |

|

|

Punjab National Bank |

.41106* |

.12208 |

.005 |

.0874 |

.7348 |

|

|

*. The mean difference is significant at the 0.05 level. |

||||||

(Source:Author)

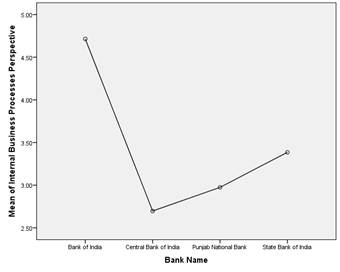

Figure 5.1 exhibits the mean plots of internal processes perspective of four banks. As it can be seen that the mean internal perspective score of Central bank of India was lowest and Bank of India was highest. SBI had second highest mean internal processes perspective score and it was followed by PNB.

Figure 5.1: Mean plot of internal processes perspective

(Source:Author)

5.1 Relationship between Internal Processes Perspective and Banks’ Performance

The effect of internal processes perspective on business performance of banks’ was studied using simple linear regression. The following section exhibits the results of simple linear regression. As shown in table 5.1.1, the internal process perspective was found to be significant predictor of banks’ performance as F statistics was found to be highly significant (p<.05). The value of R2 revealed that the internal processes explained 4.2% variation in bank’s performance. One unit change in business process would bring an average change of .13 units in banks performance.

Table 5.1.1: Effect of internal business processes perspective on bank performance

|

B |

Std. Error |

t-stat |

Sig. |

F |

Sig. |

R square |

|

|

(Constant) |

3.27 |

.105 |

31.13 |

.000*** |

17.47 |

0.000 |

.042 |

|

Internal Processes Perspective |

.130 |

.031 |

4.18 |

.000*** |

*** = significant @ 1% level; Dependent variable= Bank performance

(Source:Author)

From the simple liner regression results, it may be inferred that the customer perspective and internal business processes were significant predictor of banks performance, but their individual effects were not very high as suggested by individual R2.

The Welch and Brown-Forsythe tests showed that the means were statistically highly significant i.e. p<.05. It implies that Internal Business Process is not same across all the branches of four selected banks.

The results found by doing Descriptive statistics of Internal Business Process perspective showed that Bank of India focused most on this perspective followed by State Bank of India while Central Bank of India exhibited the lowest level of Internal Business Process Perspective even lesser than Punjab National Bank.

From the Bonferroni post hoc test of multiple comparison of Internal Business Process perspective following findings were exhibited:

· The internal process perspective of Bank of India was significantly different from all other banks (p<.05) i.e. PNB, SBI and CBI.

· While comparing Central Bank of India, the internal processes perspective of Central Bank of India was found to be different from internal processes perspective of Bank of India and SBI (p<.05) but insignificantly different from PNB (p>.05).

· The business performance of PNB was found to be significantly different form Bank of India and State Bank of India (p<.05), but not different from Central bank of India.

· The internal process perspective of State Bank of India was significantly different from all other banks (p<.05) i.e. PNB, BOI and CBI.

6.1 Significant variables under Internal Process perspective:

For increasing the Internal Business Process, it has been found that the two most important variables are “Core banking solutions” and “Real time customer support functionality with a bank advisor through chat and SMS” and banks have to focus more on these variables.

Table 6.1: Importance of Internal Business Process perspective

|

Internal Business Process Perspective |

|

|

IBPP9 Core Banking Solutions |

0.88 |

|

IBPP8 Real time customer support functionality with a bank advisor through chat and SMS |

0.858 |

(Source:Author)

Internal process perspective aimed at the desired internal process to meet the expectations of the customers. After all, excellent customer performance derives from processes, decisions, and actions occurring throughout an organization. Bankers need to focus on those critical internal operations that enable them to satisfy customer needs. During this research, an attempt has been made to identify and measure the banking sector core competencies, the critical technologies needed to ensure continued market leadership. Banks should decide what processes and competencies they must excel at and specify measures for each.

Since much of the action takes place at the branch levels, top managers tried to decompose overall cycle time, quality, product, and cost measures to branch levels. This way, the measures link top management’s judgment about key internal processes and competencies to the actions taken by employees that affect overall bank objectives. This linkage ensures that employees at branch levels in the bank have clear targets for actions, decisions, and improvement activities that will contribute to the banks overall mission.

Cheng-Ru Wua, Chin-Tsai Linb and Pei-Hsuan Tsai(2010), “Evaluating Business Performance of Wealth Management Banks”, European Journal of Operational Research, page 971-979.

Komal,Vandana Rai (2012), “ Progress of Banking in India: Customer’s Perspectives”, Business Intelligence Journal ,Volume 5(1),January 2012.

Manoj Anand, B S Sahay, and Subhashish Saha(2005), “Balanced Scorecard in Indian Companies”, Vikalpa, Volume 30(2), April-June 2005,page 11-25.

P.A. Phillips (2007) “The Balanced Scorecard and Strategic Control:A Hotel Case Study Analysis” ,The Service Industries Journal, Vol.27(6), September 2007, pp.731–746

P. K. Chakraborty (2007) “Balanced Score Card - A Comprehensive Guide to Performance Evaluation”, Banking and finance Journal, April 2007, page 1625-1630.

Rahat Munir, Sujatha Perera, Kevin Baird(2011) “An Analytical Framework to Examine changes in Performance Measurement Systems within Banking Sector”, Australasian Accounting Business and Finance Journal, Volume 5(1),page 93-115.

Souad Moufty (2009) “The role of Balanced Scorecard in UK banks as a performance measurement”, BBS Doctoral Symposium, March 2009, page 1-9.

Stan Davis, Tom Albright (2004) “An investigation of the effect of Balanced Scorecard implementation on financial performance”, Management Accounting Research , Volume 15(2 ), June 2004, Pages 135–153

Stephen C. Schoonover(2004), “Upgrading the people perspective in Balanced Scorecards”, BPT Column, Behavior Matters, January 2004

T.K.Mukherjee, Smita Pandit(2009), “Role of Business Balanced Scorecard(BBSC) in Performance Mangement”, GMJ, Volume 3(1),January-June 2009,page 50-55.