Pacific B usiness R eview I nternational

A Refereed Monthly International Journal of Management Indexed With THOMSON REUTERS(ESCI)

|

Ajinkya Bhagwat (K003) Management Student, Mukesh Patel School of Technology Management & Engineering, NMIMS, Mumbai. |

SujaanMasani (K018) Mukesh Patel School of Technology Management & Engineering, NMIMS, Mumbai. |

Harshet Sharma (K034) Management Student, Mukesh Patel School of Technology Management & Engineering, NMIMS, Mumbai. |

Geetha Iyer Assistant Professor, Mukesh Patel School of Technology Management |

On 8 November 2016, the Government of India announced he demonetisation of all ₹500 and ₹1,000 banknotes of the Mahatma Gandhi Series. This paper elucidates the impact of such a move on the availability of credit, spending and level of activity in the Real Estate sector of the country. Initially, we referred to diverse articles to understand and evaluate the short run and medium-term impacts that such a shock is expected to have on the economy. This was followed by first formulating a framework and then a hypothesis which listed the possible factors that could be most affected by the demonetization. A questionnaire was prepared and 50+ responses were recorded. A reliability test was conducted to ascertain the dependence on the data set. The responses were analyzed using factor analysis and regression. It was found that demonetization did not primarily have a significant effect on the real estate sector because existing slump in the sector spanning the last three years.

Keywords: Demonetization, Real Estate Sector, India

The real estate sector is one of the most globally recognised sectors. In India, real estate is the second largest employer after agriculture and is slated to grow at 30 per cent over the next decade. The real estate sector comprises four sub sectors - housing, retail, hospitality, and commercial. The growth of this sector is well complemented by the growth of the corporate environment and the demand for office space as well as urban and semi-urban accommodations. The construction industry ranks third among the 14 major sectors in terms of direct, indirect and induced effects in all sectors of the economy. The Indian real estate sector has been facing significant challenges in the past few years in terms of sales and overall growth. With a lot of measures, the sector was clearly pointing towards a slow and gradual, but sure recovery.

The property sector in India has been a haven for unaccounted money due to the unorganised nature of the industry and transactions in the secondary housing market and land deals having a high component of cash involved. The government’s efforts to crack down on such unaccounted money led to the demonetization on November 8th, 2016.Demonetisation brought a lot of confusion and uncertainty. Considering the structure of the deals involved, with scarcity of cash, many buyers went off the market and sellers could do little but wait. This also resulted in the reduction of prices, thereby benefitting buyers though the magnitude of reduction was not enough to pull the buyers back to the market.

Demonetisation has already resulted in a major reduction of home loan rate interest rates, and they are expected to reduce further. Developers offering good deals and discounts are maintaining their position in a market which is now ideal for serious end-users. Hence, studying the effects of demonetization in depth was imperative.

To understand the effects of demonetization on the cash dependent real estate sector in India.

Chatterjee Biswajit (2016), The Impact of Demonetization in India states the takeaway for the public in general from the announcement was as follows:Exchange of old currency notes for new ₹500 and ₹2,000 currency notes have been permitted until 31 December 2016 (i.e. 50 days from the date of the announcement).Such currency exchanges have been limited to certain specified amounts announced from time to time and excess amounts are required to be deposited with banks subject to applicable KYC requirements.Cash withdrawals have been limited to ensure adequate supply of new currency notes.Usage of old currency notes has been permitted for certain specified periods and purposes, such as at hospitals and pharmacies, gas stations and foreign currency exchange for tourists.With respect to the topic of our concern, real estate has always had an informal funding in the form of cash transactions for various reasons such as tax evasion, wages to contract workers, etc. Also, the luxury end buyers would prefer resorting to payment in cash, the event thus resulted in a lack of such transactions.With this move from the government is expectation is to bring out a transparency in the market and bring about equilibrium in the market volatility. The real estate sector especially in the small and middle segment has been unorganized, fortunately the investments in the following field has been conventionally through private players.With demonetization in the picture and better governance of the real estate sector we can expect a higher percentage of foreign direct investment into the market through electronic transfers.

Square Yards (2016), The Impact of Demonetization on Indian Real Estate report that the demonetization move will lead to exponential increase in institutionalization funding i.e. banks, private equity houses. This will also result in the short to mid-term notable price correction in the secondary real estate could be seen due to higher involvement of cash.

Impact on the Primary market segment: Minimal, since this market is highly consolidated of the housing department with much of the transactions requiring the support of home loan facilities.

Impact on the Resale market segment: This market will take a hit, as the prices were inflated as they involved cash transactions to minimize capital gains and tax evasions.

Impact on the Land sales: The effects of demonetisation should be reflected immediately due to price correction as a junk of the transactions consisted of a relatively higher percentage in the cash component.

MotilalOswal (2016), The Impact of Demonetization on Real Estate assert that the whitepaper released by the Indian Government in 2011, real estate accounted for 11% of the nation’s GDP of which consisted of 50% in black money.Therefore, a price correction of 20-30% is expected in the luxury segment. Though, projects by reputed and credible builders should not face a price or dip in the demand.With new acts like RERA (Real Estate Regulation and Development Act 2016) and Benami Transactions act, the sector will soon churn to be more transparent.This move will trouble the buyers with a delay in delivery of the projects due to the cash crunch resulting in unproductive days.

NIPFP (2016), Demonetisation: Impact on the Economybelieves the middlemen in resale of properties usually were paid in cash and would then lead to creation of unaccounted wealth. Such an issue seems to be tackled, though this has led to a drop in the income of this sphere of work. This has also resulted in lower earnings for the middlemen due to drop in prices.Apart from the above, a contraction is widely visible in the employment factor of the construction industry. All the skilled and unskilled labourers are day workers and are on contract basis. Thus, they are paid in cash. Most of these labourers do not have bank accounts as their daily income does not see any savings.

Knight Frank (2016), India Economic Update Decemberobserved an average of ₹2.36 lakh crore worth of investments in a quarter but due to demonetisation this quarter received only ₹1.25 lakh crore, a significant drop in the figure.In the following regard to the construction industry, the complimentary industries such as the cement and steel showcased a dip in growth rates of 6.2% and 16.9% respectively.In short with promises from the government for remonetisation we can expect an improvement in such figures and sentiments across the industry and people.

Money Control (2016), Demonetisation: Dissecting the impact on real estate sector identified that the market will experience a lull. The sudden restriction on Rs 500 and Rs 1000 money notes has brought about a circumstance of constrained or no trade out the market to be stopped in land resources. This has hence converted into a sudden fall in housing demand across all classes for the time being. While a share of this dwindled demand could be credited to diversions brought on by the move, numerous industry specialists opine this is a consequence of a trust shortage in the market. Cash has ended up dearer, prompting to careful spending and negligible exchanges.

ET Bureau (2016), Why property is likely to be cheaper after demonetisation?State that as per CARE Ratings points out in its report; developers are already grappling with the problem of slow sales, which is leading to rising inventory levels in all major micro markets. Given the growing uncertainty and negative impact on demand caused by demonetisation, people are likely to postpone their plans to buy property, which would lead to further increase in inventory levels. Because of this, developers and sellers could be compelled to cut down prices to drive sales. Most experts believe this will lead to the secondary market slowing down due to a shortfall of cash.

The Indian Express (2016), Real Estate demonetisation: Measuring the impact of Demonetisationascertained that it brought a lot of confusion, uncertainty along with it and, most of all, rumour-mongering especially when it came to the realty sector. Everyone was affected by this radical measure, and initially, all possible economic activities slowed down. It is important to understand how important this sector is to the Indian economy. The sector contributes 5-6 per cent of the country’s GDP, and any misinformation in a sector that is largely sentiment-driven can lead to chaos.

Firstpost (2016), Demonetisation: Strong foundation laid for real estate but price correction could be limitedemphasise thatwe must understand the cash-economy of real estate transactions, and, the demand-mechanism. There is a general anticipation of the removal of 20-30 percent cash-dealings from the transaction process. It leads people to conclude that the prices would fall by 20-30 percent. The reason for such expectations is the climbing down of prices coupled with at least two other factors such as an eventual interest rate decline and the consequent rise in demand. There could be more factors. But even if we account for these, the anticipated price-decline of 20-30 percent will get cushioned. In the final form, the price-correction may not be more that 5-8 percent, which is evident already.

Mint (2016), Opinion divided over impact of demonetisation on real estate pricesthink that many property advisers have predicted land and property prices, particularly that of luxury houses, could fall as much as 30% in the next three to six months. However, several developers and brokers said there is little room for any major price cuts due to rising input costs, and given that property prices in key markets have remained stagnant due to a three-year slowdown in the real estate sector. Some other developers said as banks are awash with money following demonetisation as customers deposited tonnes of cash, home loan rates may come down in the coming months, helping push property sales.

JLL (2016), Impact of Demonetization on Residential Real Estateidentify that the sector has traditionally seen a very high involvement of black money and cash transactions. However, almost all such incidences have been in the secondary sales market. There has for long been a strident demand to bring transparency in the sector so that the it becomes more organized, and cash dealings must necessarily be the first symptom of the disease to be dealt with.The luxury and high-end segments of residential real estate will also see a major impact from this exercise, since it is another area which has seen a lot of payments done in cash. The legal banking/financing channels have accounted for only a small part of all transactions in this space. The demonetization move is likely to result in luxury property prices dipping by as much as 25-30%

Indian CEO (2016), SWOT On Impact Of Demonetization On Real Estate Industry state that theIndian Housing sector itself contributes to 5-6% of country’s GDP and this sector owing to its behaviour of huge cash dealings is bound to face major challenges in near future. The sector which has always been the prodigy of black money has suddenly closed its doors and refused to be tainted further. This will bring about a correction in property prices. The step will also eradicate land mafias and curtail price inflations.

Tax Guru (2016), Impact of Demonetization on Real Estate in Indiareport that another factor that may add to correction in Real Estate Pricing is the increase in piling of Inventory for developers and real estate sellers and the corresponding increase in working capital pressures. With the reduction in cash component, there is bound to be a sluggish demand in real estate for short term at least which will increase the inventory with the developers. Another very important cycle that the demonetization will initiate is cheaper lending of borrowed funds by Routine Banking Network. Due to increase in funds flow with the bank the Marginal Cost of Lending Rate (MCLR) is bound to reduce which will help the house buyers to buy at affordable EMI’s. The commercial real estate will see the minimum impact on office/industrial leasing and transactions business; given that cash components do not play a significant role in such transactions and ever increasing demand for this asset.

International Journals (2016), Impact of Demonetisation on Construction Industryreport that the first and foremost is fleeing of labour force from the sites. They were not paid money for the days they worked. They could not prolong in a new place without liquid cash. The local people were also reluctant to extend credit facility to migrant workers, as they themselves were badly hit by poor cash sales. Consequently, the labourers were returning to their villages. Many of the ongoing projects came to a standstill. Majority of workers do not have bank account at all. As they are the floating population seeking job, it is literally impossible for them to open bank accounts from place to place. The Contractors, though they had sufficient balance, could not draw from bank in view of the restrictions on the amount and number of transactions per week. They were only silent spectators to the fleeing of workers from the site. The new bookings were virtually nil. The Builders who made a massive investment are in troubled waters. India’s decade long construction boom created one in three new jobs as tens of millions of people made journey from rural areas to towns seeking livelihood, came to a grinding halt. This sparked a blow also on the Cement and Steel makers who faced a sudden slump in demand.

India Infoline (2016), Dissecting the impact on the real estate sectorbelieve that thedemonetisation could also mean fresh sources of funding for developers to complete their projects. Some of the alternate sources may include the following:Developers will be forced to clean up their balance sheets so that they can avail funding from legitimate sources, however, this may come at extremely high costs from the Non-banking financial companies (NBFC) segment.Developers can avail short-term loans from their existing buyers at market price with a promise to deliver the project on time and at an interest rate as per the agreement in the sales deed.Investments from private equity firms would usher positive sentiment across the market, helping developers to source funding and strengthen end-user demand.

H0: The payment in cash for sale and lease agreements in the real estate has led to a fall in quantity of transactions.

Ha: There has not been a fall in quantity of transactions due to payment in cash.

H0: Due to unavailability of cash in the market, there has been no drop in misleading transactions to reduce the net tax to be paid.

Ha: Due to unavailability of cash in the market, there has been drop in misleading transactions to reduce the net tax to be paid.

H0: With major cities witnessing a rapid re-monetization process, there will no effect in the number of transactions in real estate.

Ha: With major cities witnessing a rapid re-monetization process, will there be a boost in the number of transactions in real estate.

H0: Given the already downfall in the real estate, the timing of demonetization will not have any effect as the market is already down.

Ha: Given the already downfall in the real estate, the timing of demonetization will lead to a further depression which will take a long time to recover.

H0: Despite the sales figures the sector had inflationary ask price, now due to demonetization there will be lesser transactions thus inflating the prices.

Ha: Despite the sales figures the sector had inflationary ask price, now due to demonetization there will be lesser transactions thus a correction (fall) in the prices.

H0: The policies by the government like 100% FDI in real estate and upcoming RERA act will suppress the demonetization impact.

Ha: The policies by the government like 100% FDI in real estate and upcoming RERA act. These counter measures will have no impact on the current scenario.

To understand effects of demonetization we will be forming a questionnaire and circulating it to relevant respondents. All the major variables for the study were identified using data from secondary sources.

The universe for this research is all people across India.

The population consists of all such people across Mumbai.

Minimum sample size will be 50

Sampling method used is non-probability convenience sampling.

6 factors identified areas follows:

| Reliability Statistics | |

| Cronbach's Alpha | Number of Items |

| .880 | 6 |

| Cronbach's alpha | Internal consistency |

| α ≥ 0.9 | Excellent |

| 0.9 > α ≥ 0.8 | Good |

| 0.8 > α ≥ 0.7 | Acceptable |

| 0.7 > α ≥ 0.6 | Questionable |

| 0.6 > α ≥ 0.5 | Poor |

| 0.5 > α | Unacceptable |

As per the above ranges our questionnaire’s consistency falls in the “Good” category and can be considered as a reliable data source.

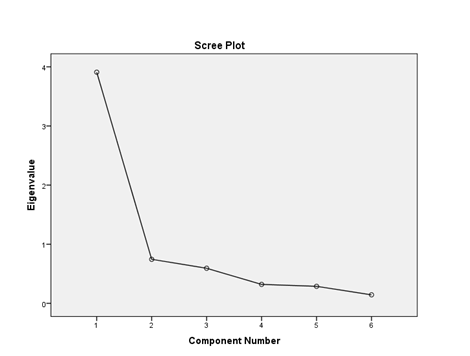

Preliminary analysis was done to understand the factors leading up to the variability. Therefore a factor analysis was done on the basis on Eigen values expected to be 1.

The results of the analysis are as follows:

| Communalities | ||||||

| Initial | ||||||

| Cash_Payment | 1.000 | |||||

| Effective_Taxes | 1.000 | |||||

| Reversal | 1.000 | |||||

| Timing | 1.000 | |||||

| Correction | 1.000 | |||||

| Government | 1.000 | |||||

| Extraction Method: Principal Component Analysis. | ||||||

| Total Variance Explained | ||||||

| Component | Initial Eigenvalues | |||||

| Total | % of Variance | Cumulative % | ||||

| 1 | 3.910 | 65.164 | 65.164 | |||

| 2 | .745 | 12.415 | 77.579 | |||

| 3 | .593 | 9.889 | 87.468 | |||

| 4 | .320 | 5.337 | 92.805 | |||

| 5 | .288 | 4.797 | 97.602 | |||

| 6 | .144 | 2.398 | 100.000 | |||

| Extraction Method: Principal Component Analysis. | ||||||

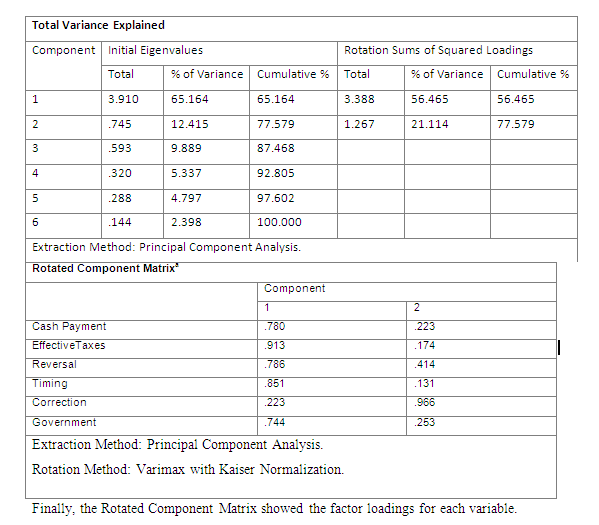

Therefore, as eminently visible component 1 “Cash Payment” describes the highest variation.

Looking at the Scree plot, we can see that it might lead you to a slightly different conclusion—it looks like the slope of this curve levels out after just two factors, rather than three.

The first 5 subtests loaded strongly on Factor 1, which was “Performance of Real Estate” --Picture Completion through Object Assembly all loaded strongly on Factor 2, which was “Impact of Demonetization”

| Component Transformation Matrix | ||

| Component | 1 | 2 |

| 1 | .914 | .406 |

| 2 | -.406 | .914 |

| Extraction Method: Principal Component Analysis. Rotation Method: Varimax with Kaiser Normalization. | ||

From the above analysis, we can safely conclude that the performance of Real Estate was not primarily affected by demonetization.

| Descriptive Statistics | |||

| Mean | Std. Deviation | N | |

| Cash_Payment | 3.94 | .890 | 50 |

| Effective_Taxes | 3.94 | .682 | 50 |

| Reversal | 3.88 | 1.081 | 50 |

| Timing | 3.96 | .968 | 50 |

| Correction | 3.46 | .994 | 50 |

| Government | 4.16 | .738 | 50 |

| Correlations | |||||||

| Cash_Payment | Effective_Taxes | Reversal | Timing | Correction | Government | ||

| Pearson Correlation | Cash_Payment | 1.000 | .666 | .650 | .684 | .401 | .450 |

| Effective_Taxes | .666 | 1.000 | .792 | .707 | .372 | .748 | |

| Reversal | .650 | .792 | 1.000 | .658 | .527 | .612 | |

| Timing | .684 | .707 | .658 | 1.000 | .359 | .552 | |

| Correction | .401 | .372 | .527 | .359 | 1.000 | .398 | |

| Government | .450 | .748 | .612 | .552 | .398 | 1.000 | |

| Sig. (1-tailed) | Cash_Payment | . | .000 | .000 | .000 | .002 | .001 |

| Effective_Taxes | .000 | . | .000 | .000 | .004 | .000 | |

| Reversal | .000 | .000 | . | .000 | .000 | .000 | |

| Timing | .000 | .000 | .000 | . | .005 | .000 | |

| Correction | .002 | .004 | .000 | .005 | . | .002 | |

| Government | .001 | .000 | .000 | .000 | .002 | . | |

| N | Cash_Payment | 50 | 50 | 50 | 50 | 50 | 50 |

| Effective_Taxes | 50 | 50 | 50 | 50 | 50 | 50 | |

| Reversal | 50 | 50 | 50 | 50 | 50 | 50 | |

| Timing | 50 | 50 | 50 | 50 | 50 | 50 | |

| Correction | 50 | 50 | 50 | 50 | 50 | 50 | |

| Government | 50 | 50 | 50 | 50 | 50 | 50 | |

| Variables Entered/Removeda | ||||||||

| Model | Variables Entered | Variables Removed | Method | |||||

| 1 | Government, Correction, Timing, Reversal, Effective_Taxesb | . | Enter | |||||

| a. Dependent Variable: Cash_Payment | ||||||||

| b. All requested variables entered. | ||||||||

| Model Summary | ||||||||

| Model | R | R Square | Adjusted R Square | Std. Error of the Estimate | ||||

| 1 | .755a | .570 | .522 | .616 | ||||

| a. Predictors: (Constant), Government, Correction, Timing, Reversal, Effective_Taxes | ||||||||

| b. Dependent Variable: Cash_Payment | ||||||||

The R value represents the simple correlation and is 0.616 (the "R" Column), which indicates a high degree of correlation. The R 2 value (the "R Square" column) indicates how much of the total variation in the dependent variable, can be explained by the independent variable. In this case, 57% can be explained, which is in the median.

| ANOVAa | ||||||

| Model | Sum of Squares | df | Mean Square | F | Sig. | |

| 1 | Regression | 22.141 | 5 | 4.428 | 11.682 | .000b |

| Residual | 16.679 | 44 | .379 | |||

| Total | 38.820 | 49 | ||||

| a. Dependent Variable: Cash_Payment | ||||||

| b. Predictors: (Constant), Government, Correction, Timing, Reversal, Effective_Taxes | ||||||

This table indicates that the regression model predicts the dependent variable significantly well. Look at the "Regression" row and go to the "Sig." column. This indicates the statistical significance of the regression model that was run. Here, p < 0.0005, which is less than 0.05, and indicates that, overall, the regression model statistically significantly predicts the outcome variable (i.e., it is a good fit for the data).

| Coefficientsa | ||||||

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | ||

| B | Std. Error | Beta | ||||

| 1 | (Constant) | .722 | .590 | 1.224 | .227 | |

| Effective_Taxes | .457 | .272 | .350 | 1.681 | .100 | |

| Reversal | .136 | .149 | .166 | .917 | .364 | |

| Timing | .349 | .132 | .380 | 2.640 | .011 | |

| Correction | .102 | .107 | .114 | .958 | .343 | |

| Government | -.203 | .183 | -.169 | -1.110 | .273 | |

| a. Dependent Variable: Cash_Payment | ||||||

This table also includes the Beta weights (which express the relative importance of independent variables) and the collinearity statistics.

| Residuals Statisticsa | |||||

| Minimum | Maximum | Mean | Std. Deviation | N | |

| Predicted Value | 2.01 | 4.93 | 3.94 | .672 | 50 |

| Residual | -1.222 | 1.755 | .000 | .583 | 50 |

| Std. Predicted Value | -2.869 | 1.467 | .000 | 1.000 | 50 |

| Std. Residual | -1.985 | 2.850 | .000 | .948 | 50 |

| a. Dependent Variable: Cash_Payment | |||||

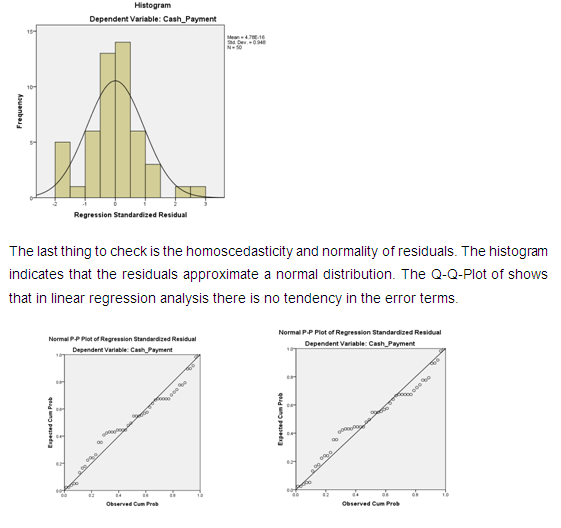

Charts

Impact of demonetization of the Real Estate sector.

Through this analysis, it has been found that the three major and most important factors:

After analysing the various factors and performing a factor analysis it can be noticed that the effect of variables the real estate sector was already in a bad shape and further demonetisation pushed the sector to it limits and thus the recovery of the sector has been delayed further by another 18 months.

Thus, we can say that the main factors for the impact on real estate are: