Pacific B usiness R eview I nternational

A Refereed Monthly International Journal of Management Indexed With THOMSON REUTERS(ESCI)

Assistant Professor, University Institute of Applied Management Sciences (U.I.A.M.S), Panjab University, Chandigarh.

Impact of New Product Announcements on Stock Prices

(Evidence from the Indian Automobile Industry)

New products are often seen as a sine qua non for fuelling future success of any organization. Designing, manufacturing and marketing new and innovative products has the potency to lend competitive advantage to a firm. The contribution of new products to the top-line as well as the bottom-line can be accurately gauged after they have been launched and are made available to the target market. At the outset however, the importance of the new product to the organization and the stakeholder’s sentiment can be captured in the stock price when the new product announcement is made.

The present study analyzes the market reaction to new product announcements made in the Indian automobile industry. A total of 19 new product announcements made between 2010 and 2016 by 3 different automobile manufacturers in India have been examined in the study.

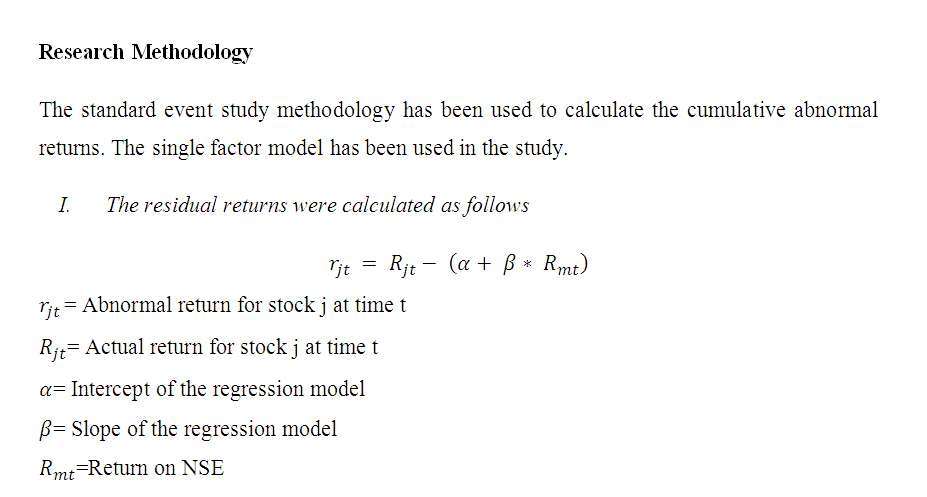

The standard event study methodology has been used to examine whether cumulative abnormal returns accrue to the firm when new product launch announcements are made. The study findings suggest that market reaction to various new product announcements can be termed as a mixed bag so far as individual manufacturers are concerned. However, collectively the automobile manufacturing companies have benefitted on the announcement date and (-2, +2) event window.

Keywords: New Product Announcements, New Product Launch, CAR, Cumulative Abnormal Returns, Event Study, Indian Automobile Sector

In the present day competitive world, innovation and new product introduction in the market place has become a sine qua non for suceess. New product introductions have earned the tag of being ‘engines of growth’. Companies, across industries, invest heavily in R&D with the objective of designing and developing products that cater to the needs of the customers in a superior manner. New product introductions can lead to increase in market share and can be a source of competitive advantage. It is widely hypothesized that the value of innovation is more for companies operating in technology based industries as compared to their counterparts in industries that rely less on technological innovation.

The concept of product life cycle operates at category level, product level and brand level. This suggests that new product introductions are necessary as existing marketing offerings would eventually outlive their utility. From a strategic point of view, new market introductions help keep a company maintain a balanced portfolio. The mature products generate current cash flows, while the new ones have the potency to generate future cash flows. Companies can introduce completely new-to-the-world products or redesign existing products and reintroduce them as new and improved models and variants of existing brands.

The automobile industry relies heavily on manufacturing and marketing new and innovative products. Different models[i] aimed at different segments of the society are launched every year. This study examines the impact of new product announcements made in the Indian automobile sector on shareholder’s wealth.

Introduction of new products is a risky but critical activity that drives a company towards success (Lee & Chen, 2009). By announcing the introduction of new products, firms send a message that they will earn superior economic returns in the future (Cohen, Eliashberg and Ho 1997). This important piece of information is likely to be interpreted by the stakeholders and their sentiment will be captured in the stock price (Mishra & Bhabra, 2001).

The extant literature on new products announcements and shareholder value is inconclusive. Chaney, Devinney, and Winer (1991) found that new product announcements result in creation of shareholder value. The study was conducted on varied announcements across different industries and also included test marketing announcements. On the other hand, Eddy &Saunders (1980) found no evidence that new product announcements create shareholder value.

Rundle (1999) and Crawford (1994) document abnormal stock price behaviour with regard to specific companies. The former found substantial and positive cumulative abnormal returns in case of a pharmaceutical company announcing the introduction of drug to cure a debilitating disease. The latter study established that abnormal returns accrued to Apple when the company announced the launch of its Macintosh line of computers. Mishra & Bhabra (2001) study the impact of product preannouncements on stock price. The authors argue that that vapourware, a case where the product launch is announced but the product does not see the light of the day, may be used as a strategy to pre-empt competition. However, Sorescu, Shankar, & Kushwaha (2007) caution that pre announcements may enhance the risk of unwanted competitive action and may vapourware may generate negative consequences.

Kirmani and Rao, 2000; Klien & Leffler, 1981 have stated that firms use product announcements as signals to create a positive mindset amongst the investors.

Some researchers have added completely new perspective related to new product announcements. Lin & Chang, 2012 highlight the role of corporate governance in influencing the share price when new products are announced. Lee & Chen (2009) have explored the role of firm size and resources and impact of new product introductions on shareholder value.

[i] In the automobile industry, the words ‘make’ and ‘model’ are generally used to represent the manufacturer and the brand respectively. For instance, if Maruti Ertiga is being referred to, the make (manufacturer) is Maruti and the model is Ertiga. For the purpose of this study, the word new product is used to represent the model that the manufacturer has launched.

Rationale of the Study

Product is an important element of the marketing mix. Researchers have explored various dimensions of new product development including market testing, consumer attitude and demand forecasting. Likewise, the announcement of a product launch has strategic importance and is likely to have a bearing on the stock price. The present study has used the well-accepted event-study methodology to evaluate the impact of such strategic marketing decisions. Research literature is replete with studies that assess the impact of new product introductions on various facets of business. However, no study appears to have been conducted that specifically examines the impact of new product announcements in the Indian context. The present study fills this research gap and links economic worth of strategic decisions and shareholder value.

Research Objective

The present study aims to assess whether cumulative abnormal returns accrue to automobile manufacturers when they announce the launch of new products/models. The 3 companies; MSIL, M&M, and Tata Motors, whose new product introductions are being examined in this study, collectively hold close to 60% of market share in the Indian passenger car industry (Sengupta, 2016)[i]. The study will assess the effect of each individual new product announcement as well as the combined impact of 19 announcements on the stock price of automobile companies.

Sample Selection

Maruti Suzuki India Ltd. (MSIL), Mahindra & Mahindra (M&M) and Tata Motors Ltd. are prominent players in the Indian automobile marketplace. MSIL has launched many new models from 2010 through 2016 as a part of its line filling strategy. M&M too has made further inroads in the Indian passenger car market in recent years. The Tata Group, well known in India for manufacturing trucks and commercial vehicles, too has increased its toehold in the Indian passenger car market.

Put together, these 3 manufacturers made 19 new product announcements between 2010 and 2016. The announcements refer to new models only. Companies do modify existing models and launch the modified versions from time to time. The launch of modified versions has been excluded from the study. The name of model and date of launch is enumerated in Table 1A to Table 1C. New variants of existing models that are introduced in the market from time to time have been excluded from the study.

The date of launch has been taken from the press releases issued by the manufacturers. The date of press release has been taken as the announcement date/event date/Day Zero for the purpose of this study.

The NSE stock price of MSIL, M&M and Tata Motors has been used for this study and the Nifty 50 has been used as the market index.

Table 1A: New Models Launched by Maruti Suzuki India Ltd. (2010-2016)

| S. No | Model | Year | Date of Launch |

| 1 | Kizashi | 2010 | 02 February 2010 |

| 2 | Ertiga | 2012 | 12 April 2012 |

| 3 | Alto 800 | 2012 | 16 October 2012 |

| 4 | Celerio | 2014 | 06 February 2014 |

| 5 | Ciaz | 2014 | 06 October 2014 |

| 6 | S Cross | 2015 | 05 August 2015 |

| 7 | Baleno | 2015 | 26 October 2015 |

| 8 | Vitara Brezza | 2016 | 08 March 2016 |

Source: Press Releases Issued by MSIL

Table 1B: New Models Launched by M&M Ltd. (2010-2016)

| S. No | Model | Year | Date of Launch |

| 1 | Thar | 2010 | October 4, 2010 |

| 2 | Verito | 2011 | April 26, 2011 |

| 3 | Xuv 500 | 2011 | September 29, 2011 |

| 4 | Rexton | 2012 | October 3, 2012 |

| 5 | TUV 300 | 2015 | August 14, 2015 |

| 6 | KUV 100 | 2016 | January 15, 2016 |

| 7 | Nuvo Sport | 2016 | April 4, 2016 |

Source: Press releases Issued by M&M

Table 1C: New Models Launched by Tata Motors Ltd. (2010-2016)

| S. No | Model | Year | Date of Launch |

| 1 | Aria | 2010 | October 12, 2010 |

| 2 | Safari Storme | 2012 | October 17, 2012 |

| 3 | Zest | 2014 | August 12, 2014 |

| 4 | Bolt | 2015 | January 22, 2015 |

Source: Press Releases Issued by Tata Motors

[i] Hyundai, Honda and Toyota are other leading automobile manufacturers in India and collectively account for close to 27% market share. Since these companies are not listed on the Indian bourses, they have been excluded from this study.

This study has examined the cumulative abnormal returns that accrued to the firm on Day 0 (Announcement Day). In addition this four other event windows have been examined to check any abnormal stock price behaviour; 1 day before to 1 day after the announcement (- 1, + 1), 2 days before to 2 days after the announcement (-2, +2), 5 days before to 5 days after the announcement (- 5, + 5) and 10 days before to 10 days after the announcement (-10, +10).

The markets process information quickly and the impact of the information is incorporated in the stock price immediately. Therefore Day 0 returns have been examined. However, there is a possibility that the news of the new product may have been revealed through informal sources before the formal announcement was made. Therefore the stock price reaction for days prior to the event date has also been considered.

For the purpose of this study, 81 day period; 40 days before to 40 days after the announcement has been taken as the window period while. The 200 day clean period includes 100 days before and 100 days after the window period. The detail of clean period data and window period data for new product announcements is given in Table 2A to Table 2C.

Table 2A: Clean Period &Window Period Dates (MSIL New Product Announcements)

| Model | Event Date/Announcement Date | Clean Period Dates | Window Period Dates |

| Kizashi | February 2, 2010 | July 7, 2009 to December 1, 2009 and April 6, 2010 to August 24, 2010 | December 2, 2009 to April 5, 2010 |

| Ertiga | April 12, 2012 | September 16, 2011 to February 13, 2012 and June 11, 2012 to October 29, 2012 | February 14, 2012 to June 8, 2012 |

| Alto 800 | October 16, 2012 | March 29, 2012 to August 17, 2012 and December 12, 2012 to May 3, 2013 | August 20, 2012 to December 11, 2012 |

| Celerio | February 6, 2014 | July 17, 2013 to December 9, 2013 and April 9, 2014 to September 4, 2014 | December 10, 2013 to April 7, 2014 |

| Ciaz | October 7, 2014 | March 7, 2014 to August 4, 2014 and December 9, 2014 to May 11, 2015 | August 5, 2014 to December 8, 2014 |

| S Cross | August 5, 2015 | January 9, 2015 to June 9, 2015 and October 6, 2015 to March 1, 2016 | June 10, 2015 to October 5, 2015* |

| Baleno | October 26, 2015 | March 31, 2015 to August 24, 2015 and December 24, 2015 to May 24, 2016 | August 25, 2015 to December 23, 2015* |

| Vitara Brezza | March 8, 2016 | August 11, 2015 to January 7, 2016 and May 11, 2016 to October 4, 2016 | January 8, 2016 to May 10, 2016 |

Source: Compiled by Author

Table 2B: Clean Period &Window Period Dates (M&M New Product Announcements)

| Model | Event Date/Announcement Date | Clean Period Dates | Window Period Dates |

| Thar | October 4, 2010 | March 16, 2010 to August 5, 2010 and December 2, 2010 to April 28, 2011 | August 6, 2010 to December 1, 2010 |

| Verito | April 26, 2011 | September 30, 2010 to February 22, 2011 and June 23, 2011 to November 21, 2011 | February 23, 2011 to June 22, 2011 |

| XUV 500 | September 29, 2011 | March 8, 2011 to July 29, 2011 and December 5, 2011 to May 3, 2012 | August 1, 2011 to December 2, 2011 |

| Rexton | October 3, 2012 | March 7, 2012 to July 31, 2012 and December 6, 2012 to May 3, 2013 | August 1, 2012 to December 5, 2012 |

| TUV 300 | August 14, 2015 | January 20, 2015 to June 18, 2015 and October 15, 2015 to March 15, 2016 | June 19, 2015 to October 14, 2015 |

| KUV 100 | January 15, 2016 | June 19, 2015 to November 16, 2015 and March 16, 2016 to August 10, 2016 | November 17, 2015 to March 15, 2016 |

| Nuvo Sport | April 4, 2016 | September 1, 2015 to February 2, 2016 and June 3, 2016 to November 1, 2016 | February 3, 2016 to June 2, 2016 |

Source: Compiled by Author

Table 2C: Clean Period &Window Period Dates (Tata Motors New Product Announcements)

| Model | Event Date/Announcement Date | Clean Period Dates | Window Period Dates |

| Aria | October 12, 2010 | March 25, 2010 to August 13, 2010 and December 10, 2010 to May 6, 2011 | August 16, 2010 to December 9, 2010 |

| Safari | October 17, 2012 | March 22, 2012 to August 14, 2012 and December 20, 2012 to May 17, 2013 | August 16, 2012 to December 19, 2012 |

| Zest | August 12, 2014 | January 16, 2014 to June 13, 2014 and October 16, 2014 to March 17, 2015 | June 16, 2014 to October 14, 2014 |

| Bolt | Jan 22, 2015 | June 23, 2014 to November 24, 2014 and March 25, 2015 to August 18, 2015 | November 25, 2014 to March 24, 2015 |

Source: Compiled by Author

Findings of the Study

The findings of the study are reported in this section.

MSIL New Product Announcements

The CAR recorded during MSIL new product announcements are given in Table 3A to Table 3H.

February 2, 2010: Kizashi

MSIL recorded CAR of -0.66%, -1.90%, -0.83% and -2.87% on the announcement date (Day 0) and during the (-1, +1), (-2, +2) and (-5, +5) event window respectively when Kizashi was launched. The CAR on Day 0 as well as across all event windows was statistically insignificant.

Table 3A: Cumulative Abnormal Returns- Kizashi Launch

| Window | CAR | T-Stat |

| Day 0 | -0.66% | -0.32 |

| (-1,+1) | -1.90% | -0.95 |

| (-2,+2) | -0.83% | 0.00 |

| (-5,+5) | -2.87% | -1.43 |

| (-10,+10) | 2.26% | 0.06 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

April 12, 2012: Ertiga

MSIL shareholders earned positive, substantial and statistically significant returns at the time of Ertiga launch announcement. The Day 0 returns of 2.28% were statistically insignificant (T-Stat 1.25). However, the returns during (-1, +1) and (-2, +2) event window at 3.58% (T-Stat 2.12) and 4.14% (T-Stat 2.27) respectively were statistically significant at 5 percent level. Likewise, the returns during (-5, +5) and (-10, +10) event window at 5.39% (T-Stat 2.96) and 6.97% (T-Stat 3.83) respectively were statistically significant at 1 percent level.

Table 3B: Cumulative Abnormal Returns- Ertiga Launch

| Window | CAR | T-Stat |

| Day 0 | 2.28% | 1.25 |

| (-1,+1) | 3.85%** | 2.12 |

| (-2,+2) | 4.14%** | 2.27 |

| (-5,+5) | 5.39%*** | 2.96 |

| (-10,+10) | 6.97%*** | 3.83 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

October 16, 2012: Alto 800

MSIL did not earn substantial or statistically significant CAR during the Alto 800 launch announcement. The only exception to this was the (-10, +10) event window when the company recorded CAR of 4.39% (T-Stat 2.39).

Table 3C: Cumulative Abnormal Returns- Alto 800 Launch

| Window | CAR | T-Stat |

| Day 0 | 2.76% | 1.50 |

| (-1,+1) | -0.20% | -0.01 |

| (-2,+2) | 0.54% | 0.29 |

| (-5,+5) | -1.56% | -0.84 |

| (-10,+10) | 4.39%** | 2.39 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

February 6, 2014: Celerio

At the time of Celerio launch announcement, MSIL earned positive CAR of 1.61% (T-Stat 1.15), 1.14% (T-Stat 0.82) and 2.43% (T-Stat 1.74) on the announcement day and (-1, +1) and (-2, +2) event window period. The returns turned negative at -2.09% (T-Stat -1.50) during the (-5, +5) event window. All the aforesaid returns were however statistically insignificant. MSIL shareholders lost value during the (-10, +10) event window of Celerio launch announcement as the company registered substantial, negative and statistically significant CAR of -7.15 % (T-Stat -5.14)

Table 3D: Cumulative Abnormal Returns- Celerio Launch

| Window | CAR | T-Stat |

| Day 0 | 1.61% | 1.15 |

| (-1,+1) | 1.14% | 0.82 |

| (-2,+2) | 2.43% | 1.74 |

| (-5,+5) | -2.09% | -1.50 |

| (-10,+10) | -7.15%*** | -5.14 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

October 6, 2014: Ciaz

The CAR recorded by MSIL was negative across all event windows except the (-10, +10) event window when the launch of Ciaz was announced. The negative returns on announcement date, and during the (-1, +1) and (-2, +2) event window were statistically insignificant. The returns at -4.12% (T-Stat -2.89) were substantial, negative and statistically significant in the (-5, +5) event window.

Table 3E: Cumulative Abnormal Returns- Ciaz Launch

| Window | CAR | T-Stat |

| Day 0 | -0.17% | -0.11 |

| (-1,+1) | -2.84% | -1.98 |

| (-2,+2) | -1.06% | -0.74 |

| (-5,+5) | -4.12%*** | -2.89 |

| (-10,+10) | 2.51% | 1.76 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

August 5, 2015: S Cross

The CAR recorded during the S Cross launch announcement was pretty similar to the CAR recorded during the earlier launch Baleno. The CAR on announcement date and during (-1, +1) and (-2, +2) event window were not statistically significant. The CAR was positive, substantial and statistically significant at 7.17% (T-Stat 5.20) and 12.60% (T-Stat 9.13) during the (-5, +5) and (-10, +10) event windows respectively.

Table 3F: Cumulative Abnormal Returns- S Cross

| Window | CAR | T-Stat |

| Day 0 | 0.22% | 0.15 |

| (-1,+1) | 0.15% | 0.17 |

| (-2,+2) | 2.15% | 1.84 |

| (-5,+5) | 7.17%*** | 5.20 |

| (-10,+10) | 12.60%*** | 9.13 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

October 26, 2015: Baleno

The launch of Baleno stemmed the tide of negative CAR that had accrued to MSIL during the earlier launches of Celerio and Ciaz. MSIL did not register substantial returns during the event windows closer to the announcement date. The returns of .48% on announcement date, .61% during (-1, +1) and .60% during (-2, +2) were statistically insignificant. However, the shareholders of MSIL benefitted as the company registered substantial, positive and statistically significant CAR of 3.82% (T-Stat 2.70) and 7.95% (T-Stat 5.64) during the (-5, +5) and (-10, +10) event window respectively.

Table 3G: Cumulative Abnormal Returns- Baleno

| Window | CAR | T-Stat |

| Day 0 | 0.48% | 0.34 |

| (-1,+1) | 0.61% | 0.42 |

| (-2,+2) | 0.60% | 0.42 |

| (-5,+5) | 3.82%*** | 2.70 |

| (-10,+10) | 7.95%*** | 5.64 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

March 8, 2016: Vitara Brezza

The launch of Vitara Brezza did not yield positive CAR for MSIL. The announcement day CAR of -2.81% (T-Stat -2.27) was substantial and statistically significant. The CAR recorded during the (-10, +10) event window was also negative, substantial and statistically significant at -6.76% (T-Stat -5.47).

Table 3H: Cumulative Abnormal Returns- Vitara Brezza

| Window | CAR | T-Stat |

| Day 0 | -2.81%** | -2.27 |

| (-1,+1) | -2.13% | -1.72 |

| (-2,+2) | -1.97% | -1.59 |

| (-5,+5) | -0.60% | -0.48 |

| (-10,+10) | -6.76%*** | -5.47 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

M&M New Product Announcements

The CAR recorded during M&M new product announcements are given in Table 4A to Table 4G.

October 4, 2010: Thar

M&M generated substantial, positive and statistically significant returns of 5.03% (T Stat 2.88) during the (-1, +1) event window. The returns during the other event windows were not statistically significant.

Table 4A: Cumulative Abnormal Returns- Thar

| Window | CAR | T-Stat |

| Day 0 | 1.76% | 1.01 |

| (-1,+1) | 5.03%*** | 2.88 |

| (-2,+2) | 1.86% | 1.07 |

| (-5,+5) | -.032% | -0.18 |

| (-10,+10) | -1.48% | -0.85 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

April 26, 2011: Verito

M&M recorded negative, but statistically insignificant CAR of -0.97% on Day 0 when Verito was launched. The CAR in other event windows was positive but was statistically insignificant.

Table 4B: Cumulative Abnormal Returns- Verito

| Window | CAR | T-Stat |

| Day 0 | -0.97% | -0.53 |

| (-1,+1) | 1.31% | 0.71 |

| (-2,+2) | 1.53% | 0.84 |

| (-5,+5) | 0.38% | 0.21 |

| (-10,+10) | 0.17% | 0.09 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

September 29, 2011: XUV

The XUV launch generated substantial, positive and statistically significant cumulative abnormal returns of 4.69% (T Stat 3.01) during the (-2, +2) event window. The returns on Day 0 at 1.47% (T Stat 0.94) as well as during the (-1, +1) and (-5, +5) event window at 1.44% (T Stat 0.92) and 2.65% (T Stat 1.70) respectively were also substantial and positive but they were not statistically significant.

Table 4C: Cumulative Abnormal Returns- XUV

| Window | CAR | T-Stat |

| Day 0 | 1.47% | 0.94 |

| (-1,+1) | 1.44% | 0.92 |

| (-2,+2) | 4.69%*** | 3.01 |

| (-5,+5) | 2.65% | 1.70 |

| (-10,+10) | -0.77% | -0.49 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

October 3, 2012: Rexton

The launch of Rexton led to generation of positive, substantial and statistically significant CAR of 4.61% (T Stat 3.78) during the (-10, +10) event window. The CAR was insignificant in all other event windows during the Rexton launch announcement.

Table 4D: Cumulative Abnormal Returns- Rexton

| Window | CAR | T-Stat |

| Day 0 | -0.17% | -0.14 |

| (-1,+1) | -1.79% | -1.47 |

| (-2,+2) | 0.67% | 0.55 |

| (-5,+5) | 1.40% | 1.15 |

| (-10,+10) | 4.61%*** | 3.78 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

August 14, 2015: TUV 100

The CAR generated during at the time of TUV 300 launch was substantial and positive during the event windows closer to the announcement date and was substantial and negative during the event windows father from the announcement date. However, the CAR was statistically insignificant across all event windows.

Table 4E: Cumulative Abnormal Returns- TUV 300

| Window | CAR | T-Stat |

| Day 0 | 1.20% | 0.75 |

| (-1,+1) | 2.62% | 1.65 |

| (-2,+2) | 1.88% | 1.18 |

| (-5,+5) | -2.50% | -1.57 |

| (-10,+10) | -2.01% | -1.26 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

January 15, 2016: KUV 300

The CAR generated during the KUV 300 launch was not statistically significant in any of the event windows.

Table 4F: Cumulative Abnormal Returns- KUV 100

| Window | CAR | T-Stat |

| Day 0 | 0.30% | 0.24 |

| (-1,+1) | -0.68% | -0.55 |

| (-2,+2) | -1.80% | -1.46 |

| (-5,+5) | 1.44% | 1.17 |

| (-10,+10) | 0.26% | 0.21 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

April 4, 2016: Nuvo Sport

M&M shareholders earned substantial, positive and statistically significant CAR of 3.64% (T Stat 2.99) on Day 0 of Nuvo Sport launch announcement. The positive and substantial CAR of 1.99% (T Stat 1.64), 1.47% (T Stat 1.21) and 3.04% (T Stat 1.50) generated during (-1, +1), (-2, +2) and (-10, +10) was not statistically significant.

Table 4G: Cumulative Abnormal Returns- Nuvo Sport

| Window | CAR | T-Stat |

| Day 0 | 3.64%*** | 2.99 |

| (-1,+1) | 1.99% | 1.64 |

| (-2,+2) | 1.47% | 1.21 |

| (-5,+5) | -0.49% | -0.41 |

| (-10,+10) | 3.04% | 1.50 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

Tata Motors New Product Announcements

The CAR recorded during Tata Motors new product announcements are given in Table 5A to Table 5D.

October 12, 2010: Aria

Tata Motors registered substantial, positive and statistically significant returns of 5.17 % (T Stat 2.91) and 5.91% (T Stat 3.32) during the (-5, +5) and (-10, +10) event window respectively when the launch of Tata Aria was announced. The returns were positive and substantial in all other event windows during this launch; however they were not statistically significant.

Table 5A: Cumulative Abnormal Returns- Aria

| Window | CAR | T-Stat |

| Day 0 | 1.50% | 0.84 |

| (-1,+1) | 2.66% | 1.50 |

| (-2,+2) | 2.60% | 1.43 |

| (-5,+5) | 5.17%*** | 2.91 |

| (-10,+10) | 5.91%*** | 3.32 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

October 17, 2012: Tata Safari Storm

The shareholders of Tata Motors did not earn statistically significant CAR during any of the event windows when the launch of Tata Safari was announced.

Table 5B: Cumulative Abnormal Returns- Safari Storm

| Window | CAR | T-Stat |

| Day 0 | 0.82% | 0.40 |

| (-1,+1) | -0.06% | -0.03 |

| (-2,+2) | -0.43% | -0.21 |

| (-5,+5) | -1.91% | -0.92 |

| (-10,+10) | 1.25% | 0.61 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

August 12, 2014: Zest

The launch announcement of Tata Zest led to the generation of positive, substantial and statistically significant CAR across all event windows. The CAR surged from 4.24% (T Stat 2.76) on Day 0 to 10.57% (T Stat 6.89) during the (-10, +10) event window.

Table 5C: Cumulative Abnormal Returns- Zest

| Window | CAR | T-Stat |

| Day 0 | 4.24%*** | 2.76 |

| (-1,+1) | 6.08%*** | 3.97 |

| (-2,+2) | 6.90%*** | 4.50 |

| (-5,+5) | 10.79%*** | 7.03 |

| (-10,+10) | 10.57%*** | 6.89 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

January 22, 2015: Bolt

Except the CAR of statistically insignificant CAR of 2.36% (T Stat 1.47) on Day 0, Tata Motors registered substantial and statistically significant CAR across all event windows during the Tata Bolt launch announcement.

Table 5D: Cumulative Abnormal Returns- Bolt

| Window | CAR | T-Stat |

| Day 0 | 2.36% | 1.47 |

| (-1,+1) | 3.43%** | 2.12 |

| (-2,+2) | 6.71%*** | 4.16 |

| (-5,+5) | 5.09%*** | 3.15 |

| (-10,+10) | 7.20%*** | 4.46 |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

Combined CAR

The combined CAR is reported in Table 6. The findings reveal that MSIL shareholders did not earn abnormal returns at the time of new product announcements. However shareholders of M&M as well as Tata Motors benefitted on announcement dates. The positive, substantial and statistically significant CAR reported by these 2 manufacturers propelled the overall CAR of all 19 announcements to 1.05% (T Stat 2.92). M&M shareholders also benefitted during the (-1, +1) event window as the company recorded CAR of 1.99% (T Stat 2.10). All the 19 new product announcements generated a positive CAR of 1.71% (T Stat 2.13) in the (-2, +2) event window. In the larger event window of (-10, +10), the CAR overall CAR is positive and substantial but is not statistically significant.

Table 6: Cumulative Abnormal Returns- Combined

| Window | MSIL | M&M | Tata | Total |

| Day 0 | 0.46% (0.84) | 3.64%*** (6.68) | 2.23%** (2.43) | 1.05%*** (2.92) |

| (-1,+1) | -0.14% (-0.15) | 1.99%** (2.10) | 3.03% (1.91) | 1.10% (1.77) |

| (-2,+2) | 0.80% (0.65) | 1.47% (1.20) | 3.95% (1.93) | 1.71%** (2.13) |

| (-5,+5) | 0.64% (0.35) | -0.49% (-0.27) | 4.79% (1.58) | 1.41% (1.19) |

| (-10,+10) | 2.85% (1.12) | 3.04% (1.21) | 4.58% (1.49) | 2.71% (1.65) |

*** Significant at 1 per cent, ** Significant at 5 per cent

Source: Author’s Calculations

The present study found that new product announcements made in the automobile industry in India generated positive and substantial CAR of 1.05% (T Stat 2.92) on the announcement date. The CAR is also significant at 1.71% (T Stat 2.13) in the (-2, +2) event window. Chaney, Devinney, & Winer (1991) had reported a CAR of 0.75% over a 3-day period (-1, +1) event window. Mishra & Bhabra (2001) had found average abnormal returns of 0.44% on the Day 0. This study thus corroborates the findings of earlier research and establishes that shareholder wealth is created on new product announcements in the Indian automobile industry.

For MSIL, the positive gains earned during the Ertiga’s launch announcement were negated when Celerio and Ciaz were launched. Interestingly, the shareholders were not rewarded when MSIL launched Alto 800, a new brand derived from two immensely popular models of the same company; Maruti 800 and Maruti Alto. The positive sentiment was also witnessed during the launch of S Cross. However, the market reaction again turned negative when Vitara Brezza was launched in 2016. Overall, MSIL did not earn statistically significant CAR in any of the event windows. On the other hand, M&M shareholders have gained substantially on Day 0 as well as during the (-1, +1) event window. Tata Motors shareholders too benefitted on Day 0 as the company generated CAR of 2.23% (T Stat 2.43).

Chaney, P., Devinney, T., & Winer, R. (1991). The Impact of New Product Introductions on the Market Value of Firms. The Journal Of Business , 64(4).

Cohen, Morris A., Jehoshua Eliashberg and Tech H. Ho (1997). An Anatomy of a Decision

Support System for Developing and Launching Line Extensions. Journal of Marketing

Research, 34 (February), 117-129.

Crawford, C.M. (1994). New Products Management. 4th Ed. Richard, Homewood, IL

Mishra, D. & Bhabra, H. (2001). Assessing the economic worth of new product pre‐announcement signals: theory and empirical evidence. Journal of Product & Brand Management , Vol. 10 Issue: 2, pp.75-93, doi: 10.1108/10610420110388645

Eddy, R.A. and Saunders, G.B. (1980). New Product Announcements and Stock Prices. Decision Sciences , Vol. 11, pp90-97

Kirmani, A. & Rao, A. R. (2000). No pain, no gain: a critical review of the literature on signalling unobservable product quality. Journal of Marketing , Vol. 64 No. 2, pp66-79.

Klein, B. & Leffler, K.B. (1981). The role of market forces in assuring contractual performance. Journal of Political Economy, Vol. 89No. 4, pp 615-641

Lee, R., & Chen, Q. (2009). The Immediate Impact of New Product Introductions on Stock Price: The Role of Firm Resources and Size. The Journal Of Product Innovation Management , 26, 97-107.

Lin, W., & Chang, S. (2012). Corporate governance and the stock market reaction to new product announcements. Rev Quant Finan Acc , 39, 273-291.

Mahindra Rise. (2011). Mahindra launches a new SUV, the XUV500 . Retrieved from http://www.mahindra.com/news-room/press-release/1317274090

Mahindra Rise. (2016 ). Mahindra drives into an all new segment with the young SUV, KUV100. Retrieved from http://www.mahindrakuv100.com/pdf/press%20release_kuv100.pdf

Mahindra Rise. (2016). Mahindra launches the Sporty & Bold looking NuvoSport . Retrieved from http://www.mahindranuvosport.com/press_releases/press_release_nuvosport_april_4_2016.pdf

Mahindra Rise. (2012). Mahindra to debut SsangYong Rexton in India on October 17 . Retrieved from http://www.ssangyongrexton.in/downloads/press%20release_rexton%20launch.pdf

Mahindra Rise. (2015). Mahindra to launch its all new TUV300 on September 10. Retrieved from http://www.mahindratuv300.com/pdf/press%20release_launch%20date%20announcement_aug%2014_2015.pdf

Mahindra Rise. (2010). Mahindra launches its Off-roader, the Thar-in India . Retrieved from http://www.mahindra.com/news-room/press-release/1294915608

Mahindra Rise. (2011). Mahindra launches 'Verito', the Logan with Mahindra badge . Retrieved from http://www.mahindra.com/news-room/press-release/1303803622

Maruti Suzuki (2017). Way of Life! Retrieved 23 May 2017, from http://www.marutisuzuki.com/

Maruti Suzuki India Limited. (2016). Maruti Suzuki Vitara Brezza storms into the SUV space . Retrieved from http://www.marutisuzuki.com/press-release-8-march-2016.aspx

Maruti Suzuki India Limited. (2015). Global launch of Premium Hatchback Baleno . Retrieved from http://www.marutisuzuki.com/press-release-26-oct-2015.aspx

Maruti Suzuki India Limited. (2015). India gets its first premium cross-over, S-CROSS. Retrieved from http://www.marutisuzuki.com/press-release-scross.aspx

Maruti Suzuki India Limited. (2014). Global debut of Maruti Suzuki’s mid-size premium sedan Ciaz. Retrieved from http://www.marutisuzuki.com/press-release-06-oct-ciaz-may-2014.aspx

Maruti Suzuki India Limited. (2014). Maruti Suzuki announces global debut of ‘Celerio’ with revolutionary Auto Gear Shift . Retrieved from http://www.marutisuzuki.com/pressreleasesfeb62014.aspx

Maruti Suzuki India Limited. (2012). Maruti Suzuki introduces all new Alto 800 delivering 22.74kmpl . Retrieved from http://www.marutisuzuki.com/press-releases-oct2.aspx

Maruti Suzuki India Limited. (2012). Maruti Suzuki unveils India's first Life Utility Vehicle - 'Ertiga'. Retrieved from http://www.marutisuzuki.com/press-releases-apr6.aspx

Maruti Suzuki India Limited. (2010). Maruti Suzuki unveils its luxurious sporty sedan Kizashi . Retrieved from http://www.marutisuzuki.com/press-releases-feb4-2011.aspx

Rundle, R.L. (1999). Amgen has good news on quarter’s net, full-year forecast and arthritis drug. Wall Street Journal .

Sengupta, N. (2017). Top 3 auto companies hold 70% market share. Times Of India . Retrieved from http://timesofindia.indiatimes.com/business/india-business/Top-3-auto-companies-hold-70-market-share/articleshow/50749746.cms

Sorescu, A., Shankar, V., & Kushwaha, T. (2007). New Product Preannouncements and Shareholder Value:Don’t Make Promises You Can’t Keep. Journal Of Marketing Research , XLIV, 468-489.

Tata Motors. (2011). Tata Motors completes its luxurious Crossover range with the Tata Aria 4×2 . Retrieved from http://www.tatamotors.com/press/tata-motors-completes-its-luxurious-crossover-range-with-the-tata-aria-4x2/

Tata Motors. (2012). Tata Safari Storme, the Real SUV, hits the road . Retrieved from http://www.tatamotors.com/press/tata-safari-storme-the-real-suv-hits-the-road/

Tata Motors. (2015). The All-New Sporty Hatchback BOLT from Tata Motors, Launched Nationally . Retrieved from http://www.tatamotors.com/press/the-all-new-sporty-hatchback-bolt-from-tata-motors-launched-nationally/

Tata Motors. (2014). ZEST from Tata Motors, the All-new Stylish Compact Sedan, Launched Nationally . Retrieved from http://www.tatamotors.com/press/zest-from-tata-motors-the-all-new-stylish-compact-sedan-launched-nationally/