Pacific B usiness R eview I nternational

A Refereed Monthly International Journal of Management Indexed With THOMSON REUTERS(ESCI)

|

Monika Soni Senior Research Fellow Department of Accountancy and Statistics Mohanlal Sukhadia University, Udaipur |

Dr. Shurveer S. Bhanawat Head and Professor Department of Accountancy and Statistics Mohanlal Sukhadia University, Udaipur |

More than 100 million people will die and global economic growth will be cut by 3.2% of GDP by 2030 if the world fails to tackle climate change, a report commissioned by 20 governments said on September 12, 2016, Survey conducted by humanitarian organisation DARA

The above statement explains the need of tackling global warming. The simplest way to control the GHGs is to stop using fossil fuels. But this is neither practically feasible nor commercially viable. Countries do not want to compromise in their growth rate hence reduction of carbon emissions seems very difficult. A common viable plan has thus been devised to systematically reduce the emission of GHGs that will not force us to change our present life style. This process is known as Carbon Trading. When trade arises, accounting and taxation comes to action.

This research paper primarily focuses on the accounting and taxation issues of certified emission reduction (CERs) (generated through clean development mechanism or voluntary emission trading schemes). The main objective of the study includes- understanding the accounting treatment of CERs and taxation issues of CERs. Primary data are collected from 148 respondents. Six hypothesis are framed based on recognition of CERs in book of accounts, valuations of CERs held for inventory, different methods of recognition of revenue from sale of CERs in books of accounts, different points of time at which revenue from sale of CERs is recognized in the books of accounts, different heads of direct tax when it is imposed on sale of CERsand different heads of indirect tax when it is imposed on sale of CERs. Chi square test is applied to test the hypotheses. The result shows that out of six, five hypotheses are rejected. The results shows that there exist significant difference between recognition of CERs in book of accounts, valuations of CERs held for inventory, different methods of recognition of revenue from sale of CERs in books of accounts, different heads of direct tax when it is imposed on sale of CERsand different heads of indirect tax when it is imposed on sale of CERs.Based on the responses, 73.33% of respondents believed that the CERs should be valued at cost or net realizable value whichever is less. 42.55% believed that income from sale of CERs should be included in “Income from Business /Profession” head. Tables and charts are drawn to analyses the data. This paper can foster for further research.

Keywords : Carbon Credit, Emission, Trading, Accounting and Taxation.

Global warming, climate change and greenhouse effect are the most common words used nowadays. Global leaders poise a serious concern on these environmental issues. Sustainable development becomes very much uncertain because we want to develop at the cost of environmental degradation. Global climate change (GCC) issues have been given a serious thought in recent times and it has become imperative, to reduce the increased concentration of greenhouse gases International consensus is gradually being developed to tame global environmental issues. With the objective to combat against global warming and its devastating consequences countries around the globe have entered into an international and legally binding environmental treaty -‘Kyoto Protocol’ under the United Nations Framework Convention on Climate Change (UNFCCC) on 16th February 2005. Kyoto Protocol identified the six greenhouse gases. The GHGs constitutes following allied gases such as: CO 2 - Carbon dioxide, CH4 – Methane, N2O - Nitrous oxide, PFCs - Per fluorocarbons, HFCs - Hydro fluorocarbons and SF 6 – Sulphur hexafluoride.

By setting limits to the maximum amount of emission of greenhouse gases by the developed countries that ratified the protocol, referred to as Annex- I countries, the treaty aims at stabilizing the concentration of greenhouse gases in the planetary atmosphere at a level that would prevent dangerous human interference with the climate system. As per the Protocol, however, the developing and least-developed countries (referred to as Non Annex-I countries) do not have any emission limit at present. Under the Protocol, binding countries i.e., Annex I countries are issued emission allowances equal to the amount of emissions allowed where an allowance represents an allowance to emit one metric tonne of carbon dioxide equivalent in the atmosphere. To meet the emission reduction targets, binding countries in turn set limits on the emissions by their local businesses and entities. Now, in order to enable the developed countries to meet their emission reduction targets as well as to encourage the Non Annex-I countries to contribute towards emission reduction efforts, the Protocol provides three market-based and flexible mechanisms – Joint Implementation, International Emission Trading and Clean Development Mechanism (CDM) among which the CDM is only relevant to India at present. The units which may be transferred under the scheme, each equal to one tonne of CO2, may be in the form of:

1. A removal unit (RMU) on the basis of land use, land-use change and forestry (LULUCF) activities such as reforestation.

2. An emission reduction unit (ERU) generated by a joint implementation project

3. A certified emission reduction (CER) generated from a clean development mechanism project activity

The Clean Development Mechanism is a flexible mechanism to enable countries with GHG emission reduction commitments, i.e., Annex I countries to meet their commitments by paying for GHG emission reductions in developing countries (non- Annex I countries). Such CDM projects earn saleable Certified Emission Reduction (CER) units, each equal to one metric tonne of carbon Dioxide equivalent, which can be counted towards meeting Kyoto targets (given Compendium of Guidance Notes – Accounting 440 in Annexure B of Kyoto Protocol). This mechanism encourages the non-Annex I countries, i.e., developing and least developed countries which at present are not bound by Kyoto Protocol to reduce GHG emissions. India, being a non- Annex I country, has emerged to be a beneficiary as Indian entities can set up CDM projects which reduce GHG emissions and thereby generate CERs which can be sold to Annex I countries and used by the latter to meet their binding emission reductions. To be eligible for CDM benefits, the proposed project must have the feature of additionally, i.e., the CDM project must provide reductions in emissions that are additional to that would occur in the absence of the project. For example, an entity can generate CERs under CDM, if it installs a waste heat boiler that saves energy. This is because reduced fuel use reduces the amount of carbon dioxide emitted. However, if an entity has to undertake the project activity because of law, for example, if the industry is legally mandated to have a waste heat recovery boiler, such a project is generally not eligible for CDM benefits.

Under CDM, a developed country can set up an emission reduction project (like generation of electricity with solar panel, installation of more energy efficient equipment’s, etc.) in a developing country and earn carbon credits on the basis of emission reductions of the project which can be used to meet a part of the Kyoto target of the entity from developed nation. Besides, the entities in developing and least developed countries can also set up an emission reduction project, generate carbon credits on the basis of emission reduction achieved by the project and then sell such carbon credits at prevailing market prices to entities of developed countries that need such credits to meet their emission reduction targets. The carbon credit so generated is measured by the unit ‘Certified Emission Reduction’ (CER) where one CER is equal to one tonne of carbon dioxide equivalent not emitted. The mechanism, through carbon trading, serves the objective of both the developed countries with emission reduction targets (who are the buyers of carbon credits) as well as of the developing and least developed countries with no emission targets at present (who are the sellers/suppliers of carbon credits) with ultimate objective to reducing emission of GHGs in the atmosphere and promoting sustainable development.

As of 30 June 2015, 7,645 CDM project activities were registered, of which 2,587 have already issued about 1.6 billion of CERs. China hosted more than 49% of total projects between 2004 and 2015, followed by India with 20.6% and Brazil with 4.4%.

Under the Clean Development Mechanism, entities in India have set up GHGs reduction project to generate carbon credits and earn revenue. An entity desirous of undertaking a CDM project activity to generate carbon credits, needs to go through several stages. An entity desirous to set up a CDM project and generate carbon credits there from has to get the project registered with the CDM Executive Board of the UNFCCC following the procedures and guidelines formulated by the Board. At first, the entity needs to prepare a Project Design Document (PDD) along with a Project Concept Note (PCN) which contain all the details of the proposed CDM project including viability, additionally, expected emission reductions and many other technical and non-technical matters. Then the project has to be approved by the national CDM authority. After getting national approval, the proposed project is required to be validated by a Designated Operational Entity (DOE), an independent auditor accredited by the CDM Executive Board which checks the PDD and verifies whether the proposed project meet the CDM criteria. If DOE validates the project then it submits the validation report along with all other necessary documents to the CDM Executive Board for project registration. The Board hosts all these documents on UNFCCC’s website. If within 8 weeks no request for review of the proposed CDM project is received by UNFCCC, the project is automatically registered. After the project is being registered with the UNFCCC, the performance (i.e., emission reduction) of the project is monitored and verified periodically by a DOE appointed by the entity and after successful verification, the DOE submits the verification report and other necessary documents to the Board with a request for issuance of CERs. UNFCCC hosts all these documents on its website and if within 15 days of making the request no request for review is received, CERs are certified and issued to the entity. The carbon credits (CERs) obtained by the entity can be sold at the prevailing market price to the entities who need it. Businesses can exchange, buy or sell carbon credits in international market at the prevailing market price which is determined, inter alia, by the demand and supply of such. At present, carbon credits are traded at the Chicago Climate Exchange, the European Climate Exchange and the Multi-Commodity Exchange of India (MCX), which launched futures trading in carbon credits in 2009.

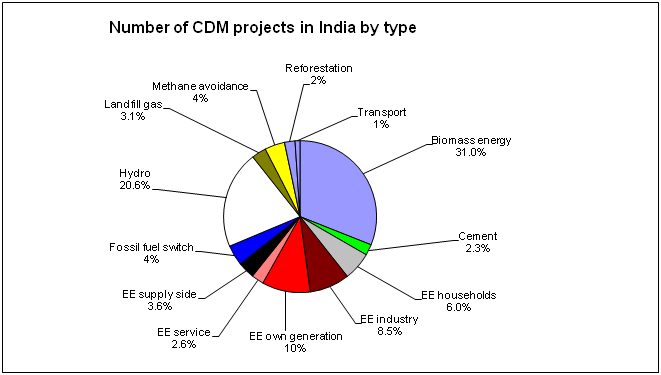

The Indian Government and Industry have been very proactive in their approach to carbon market. This has helped them gain an early mover advantage in CDM. In the global CDM market, India is amongst the leading pack of the top 8 countries (in order of CERs issued) with a combined share of 72% of the total CERs issued in the market. India along with China is collectively hosting about 70% of the total CDM projects in the world. As on June 2016, the Indian Designated National Authority (DNA) has approved 1711 CDM projects of which 1633 have been registered by the UNFCCC. Renewable energy (44%), energy efficiency (27%) and renewable biomass (18%) type of projects are the highest number in the Indian portfolio of CDM projects. For registered projects energy efficiency (38%), renewable energy (22%) and industrial process (15%) are the top categories in terms of expected CERs. The CER potential from the 1633 registered projects is 661 million, whereas the total approved (1711) is expected to yield 1200 million up to 2020. The total projects is divided into various types which is explained in the following pie chart-:

Source-: http://cdmpipeline.org/cdm-projects-region.htm as on 1st September, 2016

Indian Industry has successfully demonstrated its commitment to greenhouse gas mitigation. Market based mechanisms such as the Clean Development Mechanism have provided a major boost to industry and have mobilized the interest of corporates and technology providers towards enhancing use of energy efficiency and renewable energy technologies. The most significant achievement of CDM is that it mobilized industry action on climate change mitigation across all sectors of the economy. There are more than 1600companies who are actively engrossed in the implementation of CDM projects. The top 10 sectors in terms of number of companies involved in CDM projects in these sectors are wind, power, hydro, iron & steel, sugar, textiles, agro industry, solar, chemicals and pulp & paper. Companies like Banyan Environmental Innovations Private Limited, Enercon (India) Limited and ONGC Ltd have more than twenty CDM projects. Companies like Thermax Sustainable Energy Solutions Ltd, ITC, Reliance Industries limited have 15 to 20 CDM projects. Enking International Indian Oil Corporation Limited, Tata Steel Limited, Steel Authority of India Limited, Essar Steel Limited, Bajaj Hindusthan Ltd, Birla Corporation Ltd, Gujarat State Fertilizers and Chemicals Limited, Hindustan Zinc Limited, Tata Chemical Limited etc are few among the active holders of CDM projects. These companies are generating revenues through sale of CERs. Such CERs calls for various questions to be answered like accounting treatment of CERs, Measurement and Disclosure of CERs and Taxation issues of CERs. The present paper focuses on the current guidelines provided by Chartered Accountant of India for accounting treatment of CERs. It also focuses on the taxation issues. An opinion survey is conducted to know the views of general public about how the accounting and taxation aspects should be dealt with.

V Raju P. (2012) stated that due to the lack of any mandatory guidance on for the accounting of carbon emissions and credits, there are currently divergent accounting practices in vogue. Differences exist on the accounting for the development of the projects under CDM mechanism, generation of CERs, timing of recognition, sales and inventory valuation, etc. Currently carbon related transactions can be accounted with reference to IAS 2 (Inventories), IAS 20 (Government Grants), IAS 37 (Provisions) IAS 38 (Intangible Assets) and IAS 39 (Financial Instruments).

N Bothra (2012) revealed that since there is no cost of acquisition or cost of improvement in case of carbon credits, it does not qualify to be a capital asset u/s 45 read with 48 of the IT Act 1961. Carbon Credits compared with calves in dairy. In case of dairy farm, cow is a capital asset, milk is a product and dung is a by-product. However, calves are none of the above. In case of Sri Krishna Dairy And Agricultural Farm vs. Commissioner Of Income-Tax, 1987 (4) TMI 39 (HC), the AP High Court held that sale value of calves cannot be taxable as capital gains, as there is no cost of acquisition.

S K. Agrawal (2006) states that emergence of the opportunity of revenue generation by taking up structured Clean Development Mechanism (CDM) projects has given a new dimension to Accounting and Taxation. As the concept of Carbon Trading is totally new, even at the international level, there are some issues to be settled before arriving at a common opinion.

R Shivanesh (2008) concluded that proper accounting procedure may bring us to the end of debate for Carbon Credits but not on Carbon Credit emissions. With the largest emitters i.e. US, Canada and China excluded from the provisions of emission reductions, Carbon Credits have no real impact on emission reduction. Let us positively look forward for the days when US and China would agree for emission reduction and make this world a better place to live.

OBJECTIVES-:

· To understand the accounting and taxation issues of CERs

· To analyze the opinion of the respondents with regards to accounting and taxation aspects of CERs

HYPOTHESES

H1: There is no significant difference between recognition of CERs in book of accounts.

H2: There is no significant difference between valuations of CERs held for inventory.

H3: There is no significant difference between different methods of recognition of revenue from sale of CERs in books of accounts.

H4: There is no significant difference between different points of time at which revenue from sale of CERs is recognized in the books of accounts.

H5: there is no significant difference between different heads of direct tax when it is imposed on sale of CERs

H6: there is no significant difference between different heads of indirect tax when it is imposed on sale of CERs

Data Collection-: Primary data is collected from 148 respondents about the accounting and taxation issues of CERs through questionnaire.

Sample Size-: A total of 200 questionnaire was distributed, among them 148 completed the questionnaire. So a sample size of 148 respondents is taken.

Statistical Technique-: In order to test the null hypothesis, Chi Square test is applied.

Carbon credit is a relatively new area both at national and international levels and at present there is no specific accounting standard or guidance either from the International Accounting Standards Board (IASB) or Financial Accounting Standards Board (FASB) on accounting for carbon credits. In 2004, IASB issued IFRIC 3 on Emission Rights to provide guidance on this aspect but withdrawn later in June 2005 due to criticism on account of its reporting aspects. In the US, Emerging Issues Task Force (EITF) issued guidance on this aspect under EITF 03-14, but the same was also dropped from the agenda. In 2007, the two boards have again taken up a joint project to formulate a comprehensive framework for emissions accounting addressing its various aspects and dimensions but have not yet published the final decision on the issue. In case of our country, the Institute of Chartered Accountants of India (ICAI) issued ‘The Guidance Note on Accounting for Self generated Certified Emission Reductions (CERs)’ in 2012 which provides comprehensive guidance on accounting principles to be applied in recognition, measurement and disclosures of self-generated CERs generated by the CDM projects. But, there still exists some ambiguity as well as some issues remained untouched.

(i) The first issue discussed in the guidance note is that whether the self generated CERs can be considered as assets of the generating entity. The ‘Framework for the Preparation and Presentation of Financial Statements’ (FPPFS) issued by the ICAI, defines an ‘asset’ as –‘An asset is a resource controlled by the enterprise as a result of past events from which future economic benefits are expected to flow to the enterprise.’ But, at the stage when the emission reductions are taken place by a CDM project, CERs do not arise because issuance of CERs is subject to verification by the DOE appointed by UNFCCC. So, at the time of emission reductions CERs can be treated as contingent assets as per Accounting Standard (AS) 29 and CERs meet the definition of an asset only when the communication regarding issue of CERs is received by the generating entity from UNFCCC. After issuance of CER, CER becomes a resource controlled by the generating entity from which future economic benefits in the form of sale proceeds are expected to be received. But, here it can be argued that as soon as emission reductions take place these can be considered as assets since after the actual emission reductions, issuance of CERs is just a procedural aspect. Again, according to the FPPFS, once an item meets the definition of the term ‘asset’, it has to meet the criteria of recognition of an asset so that it may be recognised in the financial statements. As CERs come into existence when these are credited by UNFCCC, CERs can not be recognised as assets before that stage.

(ii) Though CERs are non-monetary assets without a physical form, they do not strictly fall within the meaning of ‘intangible asset’ as per AS 26 as CERs are not held for use in the production or supply of goods or services, are not used for renting to others or used for administrative purposes rather CERs generated by the entity are held for the purpose of sale. The guidance note states that intangible assets held for the purpose of sale in the ordinary course of business are excluded from the purview of AS 26 and therefore, are to be accounted for as per AS 2, ‘Valuation of Inventories’ and finally concluded that even though CERs are intangible assets these should be accounted for as per the requirements of AS 2.

(iii) Regarding measurement of CERs, the guidance note states that as CERs are inventories for the generating entity, the valuation principles as prescribed in AS 2 should be followed for CERs. As per AS 2, inventories should be valued at the lower of cost and net realizable value. Following AS 2, cost of inventories should comprise all costs of purchase, costs of conversion and other costs incurred in bringing the inventories to their present location and condition. But, all costs incurred by the generating entity do not give rise to CERs (such as research and development costs, costs of preparing the Project Design Document; fees paid to National Authority for approval, fees of registering with UNFCCC, costs incurred for monitoring the emission reductions, etc.) and hence can not be considered as the costs of CERs. Costs which are incurred to bring CERs into existence are the costs of certification of CERs by UNFCCC and hence these costs constitute costs of inventories of CERs. UNFCCC imposes two types of levies on the generating entity. Firstly, a specified percentage (presently 2%) of the CERs earned by the entity is deducted at the point of issuance and CERs are issued net of this levy. In addition, a cash payment per unit of CER is imposed by the UNFCCC towards meeting its administrative expenses. Apart from these, the generating entity normally pays a consultation fee for rendering services to certify the CERs. Thus, the costs at which the inventory of CERs should be valued include the consultation fee and the cash payment made to the UNFCCC. The deduction of CERs by UNFCCC increases the per unit cost of the CERs issued to the generating entity. On the other hand, as per the guidance note the net realizable value of the inventory of CERs is the estimated selling price in the ordinary course of business less the estimated costs necessary to make the sale.

(iv) On income recognition the guidance note states that as CERs are recognized as inventories, the entity should apply AS 9 (revenue recognition) to recognize revenue in respect of sales of CERs.

(v) The guidance note also states that the generating entity should show CERs as part of inventories in the balance sheet separately from other categories of inventories (such as Raw Materials, Work-in-process, etc.) with information on number of CERs held as inventory; basis of valuation; number of CERs under certification; depreciation, operating and maintenance costs of Emission Reduction equipments during the year.

At present there is no authoritative accounting guideline is available under generally accepted accounting principles of India or US or international Financial Reporting Standards. Here an attempt has been made to identify alternative accounting treatment of carbon credit trading.However, there is no need to issue a separate accounting standard for carbon trading. A little change in accounting standard no.2, 9 and 26 can help to bring out a correct accounting of carbon credit.

The Income Tax Department has trained its sights on the carbon credits trading business in the country with a view to crack down on tax evasion in the sector, which has been estimated at Rs 1,000 crore. Income tax department has estimated that about 200 small and large Indian companies are trading in carbon credit and have also stated this in their annual reports (Source: The Hindu August 22, 2011). But there is different opinion about the inclusion of such income in the different heads of income. The tax treatment of credits is an issue that has been a subject matter of considerable debate. Tax issues may arise at the time of entitlement of the credit, since the same could be viewed as a benefit arising from the carrying on of a business specifically taxable under section 28(iv) of the Income-tax Act (‘Act’), or on its sale, where questions may arise whether the receipt is on a capital or revenue account and in the case of the former whether there could be any taxable capital gains.

1. CERs as Business Income

Section 2 (24): In CIT V. G.R Karthikeyan (1993) 2001ITR 866 (SC) it explains that even if a receipts does not fall within the ambit of any of the sub clauses in section 2(24), it may still be income if it part takes the nature of income. Hence sale of CERs is included in the definition of income.

Section 28(vii): if an assesse received any compensation for not carrying out any activity in relation to any business, such compensation is taxable under section 28.

If it considered as Business Income than it is taxable at normal rate and eligible for set off against business losses.

2. CERs as income from capital gains-:

CERs will be treated as capital assets. As there would be no cost of acquisition for self-generated CER credits, section 55(2) of the Income Tax Act will come into operation, and total sale consideration will be liable for Capital Gains Tax (long term/short term) according to the period of holding.

If it is considered as income from capital gains than concessional tax rate will be put if held for more than 36 months.

3. CERs as income from other source-:

A source of income which does not specifically fall under any one of the other four heads of income is to be computed and brought to charge under section 56 under the head “income from other sources

If it is considered as income from other source than it is taxable at normal rates

Many researchers claim that Income from sale of CERs should be accounted for under the head Business & Profession and in case of sale of Intangible, it would be taxable under the head Capital Gains though most companies in India are recording earnings from carbon credit trading as Income from Other Sources. Trading in CER is carried out either in spot market or in futures. Service tax will be applicable on account of dealing in CERs on the exchange platform and in case of contracts resulting in delivery VAT will be applicable. Typically carbon credits in India are sold to overseas buyers; hence there would be no VAT applicable on these goods.

Since, the accounting guidelines are vague in nature and companies are adopting the accounting treatment of CERs as per their convenience, therefore to know the opinion of the general public regarding the accounting treatment and taxation issues of CERs,an questionnaire was prepared and respondents were asked to give their opinion. Responses were collected from 148 respondents. The analysis and findings are explained in the below paragraph.

Carbon trading based on the concept of buying and selling of certified emission reductions, this poses several question regarding the accounting and taxation aspects of certified emission reductions. The questionnaire was designed to know the opinion of the respondents regarding the same. It was divided into three parts which included general, accounting and taxation related questions. Responses were collected from a sample size of 148 respondents.

Table No. 1: General Questions

|

Questions |

Yes |

No |

Neutral |

Respondents |

|

Q1. Do you know the concept of Certified Emission Reduction? |

148 (100%) |

0 |

0 |

148 |

|

Q2. India has a huge potential to generate certified emission reductions (CER’s)? |

134 (90.54%) |

10 |

4 |

148 |

|

Q3. Are you aware about clean development mechanism projects through which CER's are generated? |

130 (87.83%) |

18 |

0 |

148 |

|

Q4. Do you think that total number of CER’s generated in a year by a company should be disclosed in financial statement? |

138 (93.24%) |

8 |

2 |

148 |

The above table shows the responses for general questions regarding the carbon market scenario. It is observed that all the respondents (100%) are aware about the concept of certified emission reduction. This shows that the popularity and crucial component of global warming is gaining the importance. People are getting aware about the climate change and its effects. They are updating themselves with the climate conference and are well aware about the carbon market and its concept. The table also reveals that more than 90% of the respondents believes that India has a huge potential for generating certified emission reduction. The same was also reported by The Federation of Indian Chambers of commerce and Industry (FICCI)report on “Impacts, Governance and Future of CDM”, (2012) which stated that India is amongst the leading pack of the top 8 countries (in order of CERs issued) with a combined share of 72% of the total CERs issued in the market. This shows that India has high growth for future carbon market. The market will expand. As we know, after COP21, on 5th October, 2016, Paris agreement have been ratified by 86 parties (Source-: UNFCCC). The Paris agreement will enter into force on 4th November, 2016. So soon, carbon market will see the boom. Therefore India being a developing country has huge potential for carbon market. More than 87% of respondents are aware about clean development mechanism through which CERs are generated in India. They are aware about the clean, green and renewable technology being adopted by the organizations, government and other institute to combat global warming. More than 93% of respondents believed that total number of CERs generated and verified by UNFCCC should be disclosed in financial account of the company. This shows that investors, customers are demanding clarity regarding the disclosure aspects of CERs. They want transparency in such information so that they are aware about the environmental efforts undertaken by the company.

For accounting related opinion, following important questions were asked-:

How CER's (total number generated in financial year) should be recognized in the books of accounts?

Table No. 2

|

As an asset- inventory (Current assets) |

As an asset- intangible |

As an liability- contingent liability |

Total |

Calculated Chi Square Value |

Significant or Not |

|

60 |

82 |

6 |

148 |

62.01404 |

Yes |

|

40.50% |

55.40% |

8.10% |

100% |

Table value @ 5% level of significance for 2 degree of freedom is 5.991 |

|

The calculated value of chi square 62.01404 is more than the table value of chi square (5.991) at 5 % level of significance for 2 degree of freedom. The null hypothesis is rejected. This shows that there exist significant difference between how CERs should be recognized in books of accounts. It is matter of concern that whether it should be treated as intangible asset, inventory or contingent liability. Based on opinion survey we can say that maximum number of respondents favored for CERs to be recognized an intangible assets. The above tables’ shows that 55.40% of the respondents gave the opinion that CERs should be treated as Intangible asset. As per the “guidance note on accounting for self-generated certified emission reductions (CERs) in 2012” issued by Institute of Chartered Accountant of India (ICAI) states that though CERs are non-monetary assets without a physical form, they do not strictly fall within the meaning of ‘intangible asset’ as per AS 26 as CERs are not held for use in the production or supply of goods or services, are not used for renting to others or used for administrative purposes rather CERs generated by the entity are held for the purpose of sale. The guidance note states that intangible assets held for the purpose of sale in the ordinary course of business are excluded from the purview of AS 26 and therefore, are to be accounted for as per AS 2, ‘Valuation of Inventories’ and finally concluded that even though CERs are intangible assets these should be accounted for as per the requirements of AS 2.

If CER's are held for inventory then how is it be valued?

Table No. 3

|

Cost price of CER |

Net Realizable value of CER |

Cost or Net realizable value whichever is less |

Total |

Calculated Chi Square Value |

Significant or Not |

|

12 |

4 |

44 |

60 |

44.8 |

Yes |

|

20% |

6.67% |

73.33% |

100% |

Table value @ 5% level of significance at 2 degree of freedom is 5.991 |

|

In table 3, the calculated value of chi square 44.8 is more than the table value of chi square (5.991) at 5 % level of significance for 2 degree of freedom. The null hypothesis is rejected. This shows that there exist significant difference between how CERs should be valued when it is held for inventory. Valuation of CERs as an inventory is important. Based on the responses, 73.33% of respondents believed that the CERs should be valued at cost or net realizable value whichever is less. As per the guidelines of ICAI, as CERs come into existence when these are credited by UNFCCC, CERs cannot be recognized as assets before that stage. Regarding measurement of CERs, the guidance note states that as CERs are inventories for the generating entity, the valuation principles as prescribed in AS 2 should be followed for CERs. As per AS 2, inventories should be valued at the lower of cost and net realizable value. Thus the respondents favors the same.

The revenue recognition opinion can be found in the following questions. When CER's are sold, the revenue/sale should be recorded as

Table No. 4

|

Operating Income |

Sale and included with sale of product or services |

Other income |

Total |

Calculated Chi Square Value |

Significant or Not |

|

10 |

54 |

84 |

148 |

56.14697 |

YES |

|

6.77% |

36.48% |

56.75% |

100% |

Table value @ 5% level of significance at 2 degree of freedom is 5.991 |

|

In table 4, the calculated value of chi square 56.14697 is more than the table value of chi square (5.991) at 5% level of significance for 2 degree of freedom. The null hypothesis is rejected. This shows that there exist significant difference between how revenue from sale of CERs is recorded in books of accounts. The above table’s reveals that more than 56% of the respondents believe that when CERs are sola the revenue should be recorded as other income. On income recognition the guidance note of ICAI states that as CERs are recognized as inventories, the entity should apply AS 9 (revenue recognition) to recognize revenue in respect of sales of CERs.

At what point of time, revenue from sale of CER's should be recognized in the books of accounts?

Table No. 5

|

At the time of approval of CER from UNFCCC |

At the time of contract with purchasing party |

At the time of cash realization |

Total |

Calculated Chi Square Value |

Significant or Not |

|

62 |

40 |

46 |

148 |

5.244905 |

NO |

|

41.89% |

27.02% |

31.08% |

100% |

Table value @ 5% level of significance at 2 degree of freedom is 5.991 |

|

In table no. 5, the calculated value of chi square 5.244905 is less than the table value of chi square (5.991) at 5% level of significance for 2 degree of freedom. The null hypothesis is accepted. This shows that there exist no significant difference between at what point revenue from sale of CERs is recognized in books of accounts. There exist no significant difference between the three options.

When asked to the respondents that whether Income from sale of CER's should be included in the definition of Income under section 2(24). More than 63% of respondents favor that Income from sale of CERs should be included in the definition of Income under section 2(24).

For the taxation related opinions, the respondents were asked that whether the revenue generated through sale of CERs by companies should be taxable or not. For this out of 148 respondents, 144 respondents said YES. They are of opinion that the revenue from CERs should be taxable. This brings an interesting point. Companies who have been escaping tax on such revenues from last so many years either by not disclosing the sale of CERs or by disclosing manipulative data needs a strict tax rate and clarity on this. The tax collected from such companies can be utilized towards carbon finance and promoting green technology in India.

When tax is levied a question arises what type of tax should be charged. The following questions were asked from the respondents (144) and the result are as follow.

Sale of CER's should be treated as which tax

Table No. 6

|

Direct Tax |

Indirect Tax |

Total |

|

|

No of Respondents |

94 |

50 |

144 |

|

Percentage |

65.27% |

34.73% |

100% |

The above table no. 6 reveals that out of 144 respondents who said that tax should be levied on sale of CERs, around 65.27% respondents believed that direct tax should be levied on such revenue and 34.73% believed that Indirect Tax should be levied on the revenue generated on such revenue. When direct tax comes, there are again several categories in which the income may fall. Since the tax rate differs in different heads, therefore where income from sale of CERs should be include is again critical.

If direct tax than under which head it should be taxable?

Table No. 7

|

Income from capital gain |

Income from business/ profession |

Income from other sources |

Total |

Calculated Chi Square Value |

Significant or Not |

|

|

No of Respondents |

10 |

40 |

44 |

94 |

22.03518 |

Yes |

|

Percentage |

10.65% |

42.55% |

46.80% |

100% |

Table value @ 5% level of significance at 2 degree of freedom is 5.991 |

|

In table no 7, the calculated value of chi square 22.03518 is more than the table value of chi square (5.991) at 5 % level of significance for 2 degree of freedom. The null hypothesis is rejected. This shows that there exist significant difference between the different heads of direct tax considering the fact that direct tax is imposed on revenue generated from CERs. It is matter of concern that under which head revenue from sale of CERs should be included.

When asked from the respondents, around 46.80% respondents believed that income from sale of CERs should be included in “Income from other sources” Head and 42.55% believed that it should be included in “Income from Business /Profession” head. Moreover, Section 2 (24): In CIT V. G.R Karthikeyan (1993) 2001I TR 866 (SC) it explains that even if a receipts does not fall within the ambit of any of the sub clauses in section 2(24), it may still be income if it part takes the nature of income. Hence sale of CERs is included in the definition of income. Thus the income from sale of CERs should be taxable as direct tax under Business and Profession head.

50 respondents believed that income from sale of CERs should be charged as indirect tax. Then again the question arises, which type of indirect tax should be levied? The respondents gave the following response.

If Indirect tax in than under which head it should be taxable?

Table No. 8

|

Service Tax |

VAT |

Import Duty |

Excise Duty |

Total |

Calculated Chi Square Value |

Significant or Not |

|

|

No of Respondents |

36 |

0 |

2 |

12 |

50 |

70.48611 |

Yes |

|

Percentage |

72% |

0 |

4% |

24% |

100% |

Table value @ 5% level of significance at 3 degree of freedom is 7.815 |

|

In table no. 8, The calculated value of chi square 70.48611 is more than the table value of chi square (7.815) at 5 % level of significance for 3 degree of freedom. The null hypothesis is rejected. This shows that there exist significant difference between the different heads of indirect tax considering the fact that indirect tax is imposed on revenue generated from CERs. It shows that it is matter of concern that what kind of Indirect tax should be imposed on revenue generated from CERs. The above table reveals that if Indirect tax is to be charged on the sale of CERs than 72% respondents believed that it SERVICE TAX should be charged on the sale of CERs. 24% respondents believed that excise duty should be charged. When asked whether CER's should be treated as goods under sales tax. Around 70% respondents said no.

At present there is no authoritative accounting guideline is available under generally accepted accounting principles of India or US or international Financial Reporting Standards. Here an attempt has been made to identify alternative accounting treatment of carbon credit trading. However, there is no need to issue a separate accounting standard for carbon trading. A little change in accounting standard no.2, 9 and 26 can help to bring out a correct accounting of carbon credit. Income from sale of CERs should be accounted for under the head Business & Profession and in case of sale of Intangible, it would be taxable under the head Capital Gains though most companies in India are recording earnings from carbon credit trading as Income from Other Sources. Trading in CER is carried out either in spot market or in futures. Service tax will be applicable on account of dealing in CERs on the exchange platform and in case of contracts resulting in delivery VAT will be applicable. Typically carbon credits in India are sold to overseas buyers; hence there would be no VAT applicable on these goods.

ChotaliyaMeghna (2014) Accounting for Carbon Credits in India, Indian Journal of Applied Research, Volume: 4 Issue: 5 May 2014 ISSN - 2249-555X.

DharSatyajit (2012),’’Carbon Emissions trading in India, A study on Accounting & Disclosures Practice’’, The Chartered Accountant Journal, December 2012, Pg 85-91.

Agrawal, S.K. (2006) Accounting and Taxation Aspect of Carbon Trading, Chartered Accountant, October, pp.510-513.

Kerr, S.G. (2008) Accounting Policy and Carbon credits, Journal of Business and Economic Research, 6(8), pp.77-88.

Lovell, H. and MacKenzi, D. (2011). The Role of Accounting Professional Organisations in Governing Climate Change, Antipode, 43(3), pp. 704-730.

Ratnatunga, J. (2008), Carbonomics: Strategic Management Accounting Issues, Journal of Applied Management Accounting Research, 6(3), pp. 1-8.

Singh, S. and Koshy, J. (2008) India to have new accounting norms for carbon trading.

Stern, N. (2006) The Economics of Climate Change: The Stern Review (Cambridge: Cambridge University Press).

United Nations (1998) Kyoto Protocol to the United Nations Framework Convention on Climate Change. Available at: http://unfccc.int/ resource/docs/convkp/kpeng.pdf

UNWCED (1987) Report of the World Commission on Environment and Development: Our Common Future (Oxford: Oxford University Press).

Rajendran G, “Carbon Credit- Tool for Global Environmental Protection”, Chartered Secretary, The Institute of Chartered Secretaries of India, New Delhi,vol.:xxxvii, no.2,p179,February 2008.

MaheshwariJitendra , basuAmbarish, “Carbon Credit”, Chartered Secretary, The Institute of Chartered Secretaries of India, New Delhi,vol.:xxxvii, no.7, p892,July 2007.

S.Gururaj, “Towards Greener Tomorrow- Understanding Carbon Credit” The Chartered Accountant, Journal of ICAI,New Delhi, Vol.55,No.12,June 2007 p1943

Websites-: