Pacific B usiness R eview I nternational

A Refereed Monthly International Journal of Management Indexed With THOMSON REUTERS(ESCI)

|

Dr Imran ul Amin Department of Business Studies Islamic University Of Science and Technology Awantipora, Pulwama Jammu & Kashmir Contact No.:- 9906868004 E-mail:- imran.amin@islamicunivesity,edu.in |

Dr Anisa Jan Department of Business Studies Islamic University Of Science and Technology Awantipora, Pulwama Jammu & Kashmir |

The purpose of present research is to explain the role of credit source in marketing of apple in Jammu & Kashmir and the research is carried out in apple producing districts of Jammu and Kashmir by selecting respondents through multi-stage sampling design. Various financing/credit sources as well as marketing channels were evaluated and opinions of peasants related to impact of credit on choice of marketing channel were evaluated by using mean and percentile methods.

Results of the study shows that choice exercised by peasants in selecting a particular marketing channel and location depends on the nature of contract signed by peasants while raising the credit for effective farming. It is the credit providing player/source who exercises the choice in selecting the selling location ad channel. Further, the flexibility related to marketing and peasant’s contact with market is more where the financers are institutional sources. The possible limitations of the study are that data includes only five districts of Jammu & Kashmir and study is confined to apple financing schemes and sources, so results may not always fully generalize to all regions of India, for all situations .

Keywords- Apple, institutional sources, moneylenders, flexibility, marketing, Jammu & Kashmir.

Present study tries to cover concerns regarding marketing aspects of apple industry of Jammu and Kashmir. A detail account of impacts of financial intermediaries on marketing in apple industry of the state shall be discussed. The study will elaborate various marketing channels, locations of selling the produce, flexibility of marketing channel and attempts shall be made to explore various credit sources and their impact on selection of marketing location (fruit selling location) as well as channels. Further the impacts of the source of credit and the intervention of various channel members in selection of marketing channels and selling locations will be discussed.

The Indian Horticulture sector is affected because of poor market intelligence system, inefficient supply chain, low productivity and due to postharvest inefficiencies such as lack of storage, poor transport facilities and inappropriate packing (Sinha, 2012; Mittal, 2007).The horticulture sector of Jammu & Kashmir is adversely affected due to lack of marketing strategy(Rather et al., 2013) and current marketing arrangements are facing difficulties due to the reasons such as lack of marketing knowledge, difficulty in contacting the consumers directly, lack of marketing credit within the growers, small farm size and small production and lack of institutional measures in this context(Bhat &Aara, 2012).

Apple represents the 98% of the total fruit production in the horticulture industry of Jammu and Kashmir(Bhat, 2013). The apple marketing and selling is dominantly controlled by the middle channel members who are responsible for controlling the apple prices in the market also. Apple marketing in the valley is virtually in its entirety carried out by the private sector comprising of pre-harvest contractor, forwarding agent, commission agents, wholesalers and retailers (Taili, 2014). Grading and packaging of the produce are still done on a voluntary basis and commission agents insist on over-packing of apple cartons, with the result that around 1-2 kilograms of fruit per box arrives in urban markets severely damaged. (GAIN Report, 2013).

Marketing of the fruit don’t provide the healthy benefits to the producers because the producers share in the consumers rupee varies from 35.71% and 81.25% in the existing marketing channels operational in state(Singh, R. S., 2005). The patterns of marketing are directly affecting the growers, as 70% profit is consumed by middle man and growers are solely dependent on traders and commission agents for marketing of their cultivated crops (Prasad, 2005). Further, there is mismatch in supply and demand of apples is because of lack in cold and conditional atmosphere storage in the valley. Thisoften forces peasants to sell their produce at lower prices. The mismatch in demand and supply of fruit at times makes them net losers (Huain, 2007). Further price risk is faced by growers and contractors, since there is no guarantee of increasing trend in the market price of the fruit as it fluctuates. There is no support from in the home market and perishability of product also becomes proximate cause of dwindled price. It is also observed that valley fruit growers lack regulated market and cooperative marketing societies. Due to the non regulated system of marketing, growers are at the mercy of middle man, various malpractices such as deduction of more charges, payment by installment, quoting of lower prices than actual, deduction of undue charges etc. are generally seen fallowed by these middle men. Moreover the farmers consent is not being taken before selling the produce.

Asghar (2015) in the study of supply chain management and marketing of apple in Kashmir region of Jammu and Kashmir highlighted the four channels of marketing which are:

Channel I: Producer ─ Pre-harvest contractor ─ Commission agent cum wholesaler ─ Retailer ─ Consumer

Channel II: Producer ─ Village trader ─ Wholesaler (local) ─ Commission agent (distant) ─Wholesaler (distant) ─ Retailer (distant) ─ Consumer

Channel III: Producer ─ JKHPMC ─ Wholesaler ─ Retailer ─ Consumer

Channel IV: Producer ─ Consumer

The producer’s share in consumer’s rupee was the highest in channel IV since it is the shortest channel, as compared to other channels.

Reshi et al (2010) while assessing the problems faced by the apple marketing in Jammu and Kashmir find that biggest whole sale market for apple is fruit and vegetable market Azadpur Delhi, where about 70 percent of the total traded apple is distributed which is followed by Mumbai, Bangalore, Ahmadabad and others. The season of market arrivals from Kashmir is August to November with a peak in September to October. They highlighted the fallowing marketing channels which are operational in Kashmir.

1. Farmer – Pre-harvest contractor – Commission agent – whole seller – Retailer – Consumer.

2. Farmer – Forward agent – Commission agent – whole seller – Retailer – Consumer.

3. Farmer – Commission agent – Whole seller – Retailer – Consumer.

Further, they suggested that sale through pre-harvest contractor is the most important system of marketing. Normally the small orchardists sell their crop at flowering stage to contractor who organizes plant protection, plucking and packaging of fruit. The medium and large orchardists prefer to marker their produce through 2nd and 3rd channels respectively.

The horticulture department of J&K state is not providing facilities as required by the apple growers so horticulture department should frame the beneficial policies for apple growers. 80% of the growers are dissatisfied with the efforts of the government as far as the marketing arrangements of the apple are concerned. Further, the industry is lacking the effective promotional programmes which could have helped in the increase in the market demand for the Kashmir apple(Mir, 2014). There should be enhancement of grading and quality control act, economic packing system, establishment of horticulture marketing training institute, improved marketing channel, cold storage facilities, improvement in transport facility, financial facilities to the poor growers, promotion of cooperative marketing, establishment of marketing information and news service etc (Sheikh & Tripathi, 2013 ).

Thus, previous studies have highlighted the various issues related to the marketing of the apple and the existing channels operating in the system were studied; but the impact of credit source on the final marketing of fruit and selection of particular channel is not studies by earlier studies. Thus the present study shall explore the impact, if any, of the source of finance/credit on the marketing of produce.

OBJECTIVE OF STUDY

· To evaluate the impact of credit/finance source on selection of marketing channel, location and flexibility in selling of produce.

For the collection of primary data, multistage sampling design was used to cover various geographical regions of the state. Four districts namely Shopian, Kulgam, Anantnag & Baramullah from valley and district Doda from Jammu region were selected. On an average five apple producing villages were selected sharing good heritage of apple production. Conveniently, respondents from each village were selected and mainly 10-15 orchardists [1] (families) from each village. Apart from the door-to-door study, the respondents were randomly selected in the various horticultural meets [2] organised by government and commercial banks operating in the region and money lenders associated with the horticultural lending practices were also taken into consideration to collect primary data.

Table 1:- Sample Design- Selection of Village

|

Region |

Major Apple Producing Districts |

District Selected |

Villages Selected |

|

Jammu |

Doda, Kishtwar, Ponch, Ramban |

Doda |

Pooneja, Dandi,Rutna, Bhalra, Chakka. |

|

Kashmir |

Anantnag, Bandipora, Baramullah, Budgam, Ganderbal, Kulgam, Kupwara, Pulwama, Sopian, Srinagar |

Anantnag |

Larkipora, Achabal, Shanghas, Nowgam, Gopalpora |

|

Baramullah |

Palhalan, Sopore town, Kreri, Rafiabad, Nowpora |

||

|

Kulgam |

Palnoo, Zaban, Katapora, Kokergund, yaripora |

||

|

Shopian |

Awneera, Reban, Loosdenew, chetragam, zainapora |

For evaluation of marketing structure, conduct and performance, study of marketing channels is preliminary. Marketing channels involve passage through which a commodity travels from producers to consumer. The consumers are generally located in a dispersed manner, far away from production centers which results in the absence of direct contact between producers and consumers. Large scale producers and buyers have developed highly specialized agencies under their own control to perform marketing operations.

Almost all apples produced in India are used for fresh consumption with limited use of processing. The fruit is transported to and sold in India’s largest whole sale fruit and vegetable markets like Azadpur Delhi followed by Mumbai, Bangalore, Ahmadabad, Kanpur, Jaipur and other small scale fruit selling outlets. Marketing of apple in valley of Kashmir is carried out by private sector comprising of pre-harvest contractors, commission agents, forwarding agents, wholesalers and retailer chains. Earlier commission agents were playing a dominant role in marketing, now an orchardist has a number of alternate marketing channels to choose from.

There are number of marketing channels patronized by the apple growers. But the choice of selling through particular marketing channel is affected by source of finance preferred by grower. The marketing channels mainly operating in the valley of Kashmir are as follows.

Channel (1): Producer- commission agent- Wholesaler - Retailer - Consumer.

Channel (2): Producer- Money lender - Commission agent- Wholesaler- Retailer - Consumer.

Channel (3): Producer- Pre harvest Contractor- Commission Agent – Wholesaler - Retailer- Consumer.

Channel (4): Producer-Wholesaler - Retailer- Consumer.

Selecting any source of the finance has direct impact on selection of marketing channel and selling location. This is because; contract signed on the time while raising credit necessitates growers to sell produce through their patronized marketing channels. The flexibility of selling and channel selection is only available with the institutional financing sources because there is no such clause in their contract which forces growers to sell their produce on the financer’s will. In present investigation marketing channels have been divided into various categories on the basis of the conditions accepted in contract for raising credit.

1. Money lender initiated marketing channel:

This channel is usually the channel number 2 as stated above. Here location of the final marketing remains with money lender. Money lender plays a dominating role in said channel. The selling of produce is being monitored by the moneylender and grower is not responsible for the selection of the market. Further, sale proceeds of the trade remain with moneylender which makes the process objectionable.

2. Commission Agents Channel:

While loan is raised from commission agents, contract signed demands growers to sell fruit through commission and forwarding agent’s marketing channel. The dominant player in this kind of marketing channel is commission agent. The practice involves raising of 12% commission on gross sales of apple by commission and forwarding agent. This raised commission acts as interest charged by commission and forwarding agents on loan forwarded by them to growers. Among above discussed channels, the channel 1 is showing the operating characters like this.

3. Open Marketing Channel:

Here choice remains with growers and they remain dominating players in marketing channel. The flexibility of selling is high and marketing returns are higher as compared to other channels. So this is most efficient marketing channel. In above cited channels, the channel 3 and 4 are falling in this context. Usually institutional financing sources don’t interfere with grower’s choice regarding selling of final produce.

The choice of above channels is reliant on financial intermediary used to raise the credit. As we have discussed it in earlier chapters that the choice of marketing channel is affected by source of finance used because these conditions are implicit with contract signed between two parties.

The process of selecting above channel is dependent on source of finance used. But location/place of selling final produce varies in present industry as shown in table below.

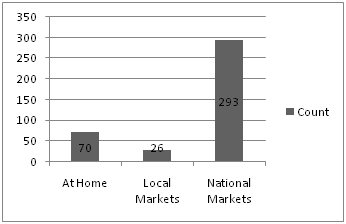

I. Selling produce at Home

This choice remains only with those growers who either use bank as source of finance or don’t require any financing source (they are self reliant to bear costs of inputs and allied operations). Banks don’t put any restriction on selling produce at particular location or choosing any particular marketing channel. In present investigation 18.0% of people were selling their produce at their flexible choice and marketing location/channel.

Table 2. Apple selling of locations

|

S. No. |

Market location |

Count |

Percent |

|

1 |

At Home |

70 |

18.0% |

|

2 |

Local Markets |

26 |

6.7% |

|

3 |

National Markets |

293 |

75.3% |

|

Total |

389 |

100% |

Fig 1: - Distribution of respondents on the basis of selling locations in various markets

II. Local Fruit Markets

Growers who are self-sufficient or use bank as source of finance or have raised finance from local commission agents which are merely operational in the state, are free to use this market location/channel for selling of fruit. In our study only 6.7% of respondents said that this marketing channel is used by them.

III. National Markets

This channel can be used by all growers irrespective of source of finance used. Because moneylenders commonly sell fruit in these markets and commission agents are operational enormously in these markets. One of the advantages related to national markets is that after selling produce, the grower can easily clear accounts whenever they wish. So this is most adapted marketing channel and more than 75% of respondents are using this channel.

It is evident from the table 3 that selling of produce is directly proportional on the financing source opted by orchardists. The growers raising credit from the institutional sources or loan from friends and relatives are open to sell their fruit at their choosy location. But, usually preferred marketing locations are markets operating at national level. The growers opting moneylenders as their financers are bound to sell their produce through moneylenders generated marketing channels and location. As shown in the table 3, out of 171 respondents who raise finance from moneylenders, 153 (89.4%) respondents reveal that they sell fruit in the national markets. This is because as cited above, the national markets are the pet market places of the moneylenders.

In case of commission agents as financing source, the growers have to sell fruit through commission agents. As shown in the table 3, all respondents who raise loan from commission and forwarding agents have to sell their produce in national markets or local markets where respective commission and forwarding agents are operating. None of the growers who raise loan from commission agents are selling the produce at home. Usually the commission and forwarding agents use to dominate marketing channel and are operating outside the state of Jammu and Kashmir.

Table 3:- Comparison between financing source and location of selling fruit.

|

S. No. |

Market location |

Financer |

Total |

|||||||||

|

Bank |

Money Lender |

Commission & Forwarding Agent |

Friends & Relatives |

Any Other |

||||||||

|

Count |

%age |

Count |

%age |

Count |

%age |

Count |

%age |

Count |

%age |

|||

|

1 |

At Home Local Markets National Markets |

42 |

27.27 |

18 |

10.53 |

0 |

0 |

6 |

42.85 |

4 |

28.57 |

70 |

|

2 |

4 |

2.59 |

0 |

0 |

18 |

50.00 |

2 |

11.76 |

2 |

11.76 |

26 |

|

|

3 |

108 |

70.12 |

153 |

89.47 |

18 |

50.00 |

6 |

42.85 |

8 |

57.14 |

293 |

|

|

Total |

154 |

100% |

171 |

100% |

36 |

100% |

14 |

100% |

14 |

100% |

389 |

|

So it is clearly shown in the statistics as shown above that location of market is dependent on source of the finance used. Further it is clear that the mostly chosen and reliable marketing locations are national markets operating outside the state. Out of 389 respondents 293 respondents were selling the final produce at national markets.

CONTROL ON SELLING PRICE AND CONTACT WITH THE MARKET

For effective marketing programs and getting best outcome from selling process, it is important to have timely updates and direct contact with market (both within the state and outside state markets). Governmental initiatives such as web based information by Jammu and Kashmir horticulture produce marketing and processing cooperation (HPMC), Radio Kashmir and Local government sponsored free air TV channels (DD Kashir) broadcast programs and agricultural related news and market rates. The information helps the peasants to monitor price trends in local and national markets. Another source is informal transfer of market information which is disseminated through word of mouth and some well educated guesses and myths about price change such as market rates before Deepawali [3] and after Deepawali. Another issue related with marketing price is information about the quantity and quality of fruit which is expected in advance in other fruit growing regions of the country such as Himachal Pradesh and Arunachal Pradesh etc.

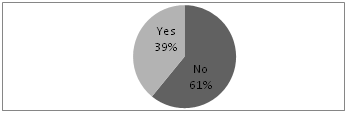

The study revealed that about 40% of orchardists are in direct contact with the markets. This is because major portion of produce is sold through moneylender sponsored marketing channels, so peasants don’t remain present at the time of selling of fruit. So, the biggest issue and drawback related with this (money lender finance) source of finance decreases its efficacy in marketing functions. While as the institutional financing sources are not producing any hindrances in marketing of final produce, so they are becoming choicely since last few years.

Table 4:- Orchardist’s contact with the market/fruit selling location.

|

S. No. |

Direct contact market |

Count |

Percent |

|

1 |

No |

237 |

60.9% |

|

2 |

Yes |

152 |

39.1% |

|

Total |

389 |

100% |

Fig. 2:-Respondents contact with the fruit selling market

The lack of the contact with the market and poor information of selling prices among growers make this process less efficient from the grower’s point of view. So control on the market prices is not in the hands of the growers.

MARKET FLEXIBILITY

By flexibility of market here we mean exercising of will/choice by the growers in selling fruit at their own choice. But in existing system, credit raised for working capital requirements impose some restrictions in doing so. Because clause in contract signed at the time of the raising credit demands the growers to act as per wishes of financer in selling of fruit. The flexibility in marketing after availing loan from a particular source of finance involves two choices viz.

1. The freedom/choice available with grower in selecting particular marketing channel and selling destination for their final produce.

2. The freedom/choice in selecting time of selling of produce. This means that under normal circumstances, the grower if finds sluggish market conditions can defer time by putting perishable fruit in cold stores.

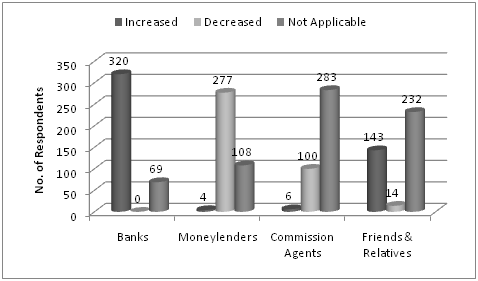

In table 5 as well as figure 3 perceptions of respondents regarding the flexibility in selling of produce in market is clearly visible while availing credit from various financing sources.

I. Flexibility in Marketing when Loan from Institutional Sources of Finance

We have tried to explore issues in flexibility of marketing in preview of above mentioned choices. About 82.3% of respondents revealed that they possess freedom in exercising control over marketing operations when loan is raised from banks. This is because; banks are interested with healthy maintenance of their bank accounts rather than interfering in farming and selling activities. Thus choice of selecting particular period and channel of marketing remains with horticultural growers. Growers can sell produce at home or any likable market and even flexibility of selling the produce to pre-harvest contractors is also available with them. Although 17.7% respondents didn’t responded to question stated.

II. Flexibility in Marketing when Loan from Moneylenders

On the other hand when loan is offered by moneylenders, flexibility of choosing the marketing channel and destination of selling produce remains with moneylenders only. Peasants are bound to sell their produce through moneylender initiated marketing channels as already defined in the contract. More than 70% of peasants find this source of finance inflexible as far as marketing of produce is concerned. In case of money lenders, peasants can ask them to wait for some time if they find the market in sluggish condition, but only for less than a week’s time. The choice of selling produce in late season such as in January and February is not with peasants because money lender did not allow them to keep produce in cold storage houses. The reason behind the money lenders unwillingness is that they have to clear accounts with peasants as soon as possible at the end of harvesting season.

Table 5:- Orchardist’s perception related to the flexibility of credit sources

|

S. No. |

Market Flexibility |

Banks |

Moneylenders |

Commission & Fwd. Agents |

Friends & Relatives |

||||

|

Count |

%age |

Count |

%age |

Count |

%age |

Count |

%age |

||

|

1 |

Increased |

320 |

82.3 |

4 |

1.0 |

6 |

1.5 |

143 |

36.8 |

|

2 |

Decreased |

0 |

0.0 |

277 |

71.2 |

100 |

25.7 |

14 |

3.6 |

|

3 |

Not Applicable |

69 |

17.7 |

108 |

27.8 |

283 |

72.8 |

232 |

59.6 |

|

Total |

389 |

100 |

389 |

100 |

389 |

100 |

389 |

100 |

|

Fig. 3:- Change in market flexibility while raising credit from various sources of finance.

III. Flexibility in Marketing when Loan from Commission and Forwarding Agents.

Likewise in our research only 106 respondents answered this question based on their experiences with commission agents and more than 95% of them gave similar response as is evident in case of moneylender as source of finance. That is, they feel this source is inflexible in terms of marketing aspects of fruit. But this channel has one advantage because unlike moneylenders, here concerned commission agent is directly involved with selling of produce and thus they try to sell product of their clients at relatively bargained higher prices to provide advantage to their clients. Also the forwarding and commission agents provide choice to growers to store their produce to sell it in late seasons by giving them cold storage facilities [4] .

IV. Flexibility in Marketing when Loan from Friends and Relatives.

In case, if loan is raised from friends and relatives, options are open regarding final marketing of fruit. Thus this source is found to be flexible. But in some cases, relatives and friends offer loans on pre conditions like selling produce through their sponsored channels, there thee flexibility in marketing gets hampered.

Thus from above it is evident that flexibility in marketing is high in case if loan is raised from institutional source and from friends and relatives. This is because; these sources are not concerned with choice of selling location and channel by the growers.

Selling of the fruit is dependent on the financing source utilized by orchardists. Growers, who are choosing the moneylenders as their financers, are bound to sell their fruit through moneylender generated marketing channel.

The selling location is also chosen by the moneylenders. The growers don’t remain present at the time of selling of fruit. So this is the biggest issue and drawback related with this (money lender finance) source of finance and thus decreases its efficacy. While as the institutional financing sources are not acting as the obstacle in the marketing of final produce, so they are becoming choicely since last few years. The flexibility of marketing, when financing source is bank or any institutional source, has increased. 82% of respondents said that they feel freedom in exercising control in marketing process because banks are interested with healthy maintenance of their bank accounts rather than interfering in farming and selling activities. Thus, the choice of selecting particular time for selling and channel of marketing remains with them. Growers can sell produce at home or any likable market and even the flexibility of selling the produce to pre-harvest contractors is also available to them. In case of moneylender financing, the grower is bound to sell their produce only through moneylender initiated marketing channel. This is the result that more than 70% of growers find this source of finance less flexible as far as the marketing of produce is concerned.

Asghar S. (2015). “Study of Supply Chain Management And Marketing Of Apple In Kashmir Region Of Jammu And Kashmir, India” Unpublished doctoral dissertation. Telangana State Agricultural University. Hyderabad.

Bhat J. A. &Aara, R. R. (2012). Marketing Efficiency of Kashmir Apple. Marketing , 35 (227.17), 50-64.

Bhat Javid. (2013). Problem of Apple Marketing in Kashmir. Journal of Research in Commerce and Management, Vol. 1( 6).

Chand Ramesh. (2014). “From Slowdown to Fast Track: Indian Agriculture since 1995”. Working Paper 01/2014. National Centre for Agricultural Economics and Policy Research. Indian Council of Agricultural Research. New Delhi.

Dastagiri M. B. (2010). Estimation of Marketing Efficiency of Horticultural Commodities Under Different Supply Chains in India. ICAR research data repository for knowledge management (An Institutional Publication and DataInventoryRepository) http://krishi.icar.gov.in/jspui/handle/123456789/806 .

Deodhar, S. Y., Landes, M., & Krissoff, B. (2006). Prospects for India's Emerging Apple Market . US Department of Agriculture, Economic Research Service.

GAIN (Global Agricultural Information Network) Report Number: IN3069. June 2013.

GOI. (2011). “Report of a Expert Group to Formulate a Job Plan for the State of Jammu and Kashmir”. Government of India. New Delhi.

Kumar Sant., P. K. Joshi & Suresh Pal. (2004). “Impact of Vegetable Research in India”. NCAP Workshop Proceedings No.13.National Centre for Agricultural Economics and Policy Research. ICAR. New Delhi.

Malik Z. A. (2013). Assessment of apple production and marketing problems in Kashmir valley. Journal of Economic and Social Development . 9( 1).pp.152-156.

Mir S. M. (2014). Problems of Apple Industry in J&K with Special Reference to Sopore Town. International Journal in Management & Social Science . 2( 3).pp. 33-46.

Mittal Surabhi. (2007). Strengthening Backward and Forward Linkages in Horticulture: Some Successful Initiatives. Agricultural Economics Research Review . 20.pp.457-469.

Prasad Jagdish. (2005). Encyclopedia of Agricultural Marketing . Mittal Publications. New Delhi.

Rather N. A., Lone P. A., Reshi A. A. & Mir M. M. (2013). An Analytical Study on Production and Export of Fresh and Dry Fruits in Jammu and Kashmir. International Journal of Scientific and Research Publications . 3 (2).pp.1-7.

ReshiMohmad Iqbal, Muzaffer Ahmad Malik & Vijay Kumar. (2010). Assessment of Problems and Prospects of Apple Production and Marketing in Kashmir Valley, India. Journal of Environmental Research and Development. Vol. 4 ( 4).

Sharma V. K. (2004). Advances in Horticulture. Deep and Deep Publishers. New Delhi.

Sheikh S. H. &Tripathi A. K. (2013). Socio-economic conditions of apple growers of Kashmir Valley: A case study of district Anantnag. International Journal of Educational Research and Technology . 4( 1).pp.30-39.

Singh R. S. (2005). “Marketing of Citrus Fruits in Mid-hills of Jammu and Kashmir”. (Edn.) Prasad Jagdish. Encyclopedia of Agricultural Marketing. Mittal Publications. New Delhi

Sinha Piyush Kumar (2012). “Organized Retailing of Horticultural Commodities”. Indian Institute of Management Ahmedabad, W.P. No. 2012-12-03 December 2012.

Sinha R.P., Gupta S.P. & Singh U.K. (2005). Analysis of Flow of Credit to Different Categories of Farmers- A Study in Nalanda District of Bihar. Indian Journal of Agricultural Economics. Vol-60. No-3.

Taili A. H. (2014). Dynamics of horticulture in Kashmir India. International Journal of Current Science . 11: E 15-25.

[1] Head of family was selected as respondent.

[2] Fruit growers associations. KissanMela.

[3] Hindu festival. This acts as a break in market for 2-3 days. Buyers in fruit markets visit their families in these days. Thus the markets get flooded with fruit which is sold then on the low prices. Also before the festival, demand of the fruit increases because apple is the most chosen gift to greet relatives in advance.

[4] The cold storage facility is chargeable. On an average 35/box/month