Pacific B usiness R eview I nternational

A Refereed Monthly International Journal of Management Indexed With THOMSON REUTERS(ESCI)

|

Vinmalar J Research Scholar PG and Research Department of Commerce (Shift1) Madras University Loyola College, Chennai |

Dr. T. Joseph Associate Professor and Head PG and Research Department of Commerce (Shift1) Madras University Loyola College, Chennai |

Retirement is defined as seclusion or privacy, or withdrawal from work due to age.The retirement age of government employees is been fixed as per the 7th pay commission, but there is no fixed retirement age under private sector working individuals.This study is framed to find out how far the working individuals of both gender and both sectors are aware in investing the avenues like rental income, mutual fund, equity shares, national pension scheme, public provident fund and life insurance policy as a source of income after their retirement by setting of all their expenses to have a secure retirement life.

Key Words: Retirement plan, Working individuals, Government employees, Private sector, Investment in avenues, Source of Income, Retirement life.

Retirement is defined as seclusion or privacy, or withdrawal from work due to age. In India the Government is bifurcated into central and state, where the retirement age range within 58-65 as per 7th pay commission based upon the profession.Individuals working under private sector has no such retirement age. Pension is a periodic monthly payment made to public servants who have completed their service but on or after 2004 pension payment has been stopped for government employees and a new scheme called Contributed Pension Scheme was introduced where, the employees from their salary 10% plus Dearness Allowance is been allocated and the government share an equalamountfor Tier-I employees. Government doesn’t share their contribution to Tier-II employees.Individuals who work under private sector receive Employee Provident Fund (EPF) monthly which is also considered as a type of pension. (L M Bhole)The EPF scheme for industrial workers was introduced with the passage of the Employees’ Provident Fund Act, 1952. Originally, public sector units were not covered under this Act, but since 1958 they have also been brought under it.

In India the pension system coverage was very small by handling Employees’ Provident Fund (EPF), Employees’ Pension Scheme (EPS), and Public Provident Fund (PPF). In recent years the government has brought National Pension Scheme (NPS) and Atal Pension Yojana (APY) under pension system. Apart from government lending pension plans, working individuals can initiate themselves by investing in certain avenues, hence this study deals with the initiatives taken by the common working individuals in Chennai City as a part of their retirement plan.

RETIREMENT PLAN

Retirement planning is the most important financial goal for the people when they start to work. The most important reasons for people to frame out a retirement plan is to “Enjoy their retired life and to take care of family”. The best period to plan for retirement is at the age of 25 where most would have started to work. Before planning an individual has to gather up his own financial data such as his income, debt level, commitments, etc., then one has to check up his fitness whether he is suffering from any dis-order, if so he need to plan out keeping in mind by setting as side the necessary amount that is needed for his treatment. In this study investment options like buying a house and leave for rent/lease, investing in mutual fund, equity shares, NPS, PPF, APYand Insurance policyare considered and how far working individuals have invested are analysed in this study. Pension plans provide financial security and stability during old age when people don't have a regular source of income. Pension scheme gives an opportunity to invest and accumulate savings and get a sum amount as regular income through annuity plan on retirement. According to United Nations Population Division World's life expectancy is expected to reach 75 years by 2050 from present level of 65 years. The better health and sanitation conditions in India have increased the life span. As a result number of post-retirement years increases. Thus, rising cost of living, inflation and life expectancy make retirement planningessential part of today's life.

RENTAL INCOME

People who are wealthier buy a land and construct a house plus an extra floor/house in order to leave for rent and earn as rental income on monthly basis or leave it for lease and get a lump sum amount as a source of income. Individuals who are not much wealthier take loan from bank and also utilize their part of savings amount to construct a house where they plan out in such a way to receive a rental income in future.

MUTUAL FUND

(R.P.Rustagi) Small investors who are unable to participate in capital market, can access the stock market through the medium of mutual funds. The investment may be diversified to spread risk and to ensure a good return (dividend or capital gains or both) to the investors. Investment can be made on monthly or lump sum. In the current financial year 2017 the minimum investment for mutual fund has been reduced to Rs. 500 per month which encourages a normal person to invest on a monthly basis called as Systematic Investment Plan. By investing in mutual funds, you could diversify your portfolio across a large number of securities so as to minimize the risk.

EQUITY SHARES

(R. P. Rustagi) The motive for investment in equity shares is twofold: To get a dividend income and to earn a capital profit at the time of sale. Equity shares are one of the main source of financial plan where it can be converted into liquidity at the needed time. Equity shareholders are the actual owners of the company and they bear the highest risk. Dividend payable to equity shareholders is out of appropriation of profit but the rate of dividend is not fixed. Equity shares are transferable, i.e. ownership of equity shares can be transferred with or without consideration to other person.

NATIONAL PENSION SCHEME

Government of India established Pension Fund Regulatory and Development Authority (PFRDA) on 10th October, 2003 to develop and regulate pension sector in the country. The National Pension System (NPS) was launched on 1st January, 2004 with the objective of providing retirement income to all the citizens. NPS aims to institute pension reforms and to inculcate the habit of saving for retirement amongst the citizens. Initially, NPS was introduced for the new government recruits (except armed forces). With effect from 1st May, 2009, NPS has been provided for all citizens of the country including the unorganised sector workers on voluntary basis. Additionally, to encourage people from the unorganised sector to voluntarily save for their retirement the Central Government launched a co-contributory pension scheme, ' Swavalamban Scheme- External website that got released in the Union Budget of 2010-11, where the government will contribute a sum of Rs.1,000 to each eligible NPS subscriber who contributes a minimum of Rs.1,000 and maximum Rs.12,000 per annum. This scheme was applicable up to FY 2016-17.

PUBLIC PROVIDENT FUND

The Public Provident Fund (PPF) Scheme, 1968 is a tax-free savings avenue that was introduced by the Ministry of Finance (MOF) in India in the year 1968. Interest earned on deposits in the PPF account are not taxable. Deposits made towards PPF accounts can be claimed as tax deductions. This makes the PPF Scheme one of the most tax efficient instruments in India. It was launched to encourage savings among Indians in general, especially to encourage them to create a retirement corpus. Since this scheme was launched to encourage savings across income classes, minimum deposit amount is Rs. 500 for a year and current interest rate for FY 17-18 is 7.9%.

LIFE INSURANCE POLICY

(L M Bhole) Life Insurance and General Insurance is one of the fastest growing sector in India since 2000 opened to the entry of Private domestic and foreign companies; mixed sector of public and private sector units; oligopoly of public sector companies (12 life insurance and 12 general insurance companies). Life Insurance in India was nationalised by incorporating Life Insurance Corporation (LIC) in 1956. All private life insurance companies at that time were taken over by LIC.In 1993, the Government of India appointed RN Malhotra Committee to lay down a road map for privatisation of the life insurance sector. By 2000 Insurance Regulatory and Development Authority IRDA—started issuing licenses to private life insurers. New schemes were added along with LIC like LIC with Retirement plan and other beneficial plans made many to invest in LIC to have a secured source.

ATAL PENSION YOJANA

The Atal Pension Scheme will bring security to ageing Indians while at the same time promote a culture of savings and investment among the lower and lower middle class sections of society. One of the greatest benefits of the scheme may be enjoyed by the poorer sections of society. The government of India has decided to contribute 50 percent of the user’s contribution or INR 1,000 a year (whichever is lower) for a period of five years. This contribution will, however, be enjoyed only by those who are not income tax payers and those who join thescheme before 31 December 2015. APY is the guaranteed pension after retirement and there is no premature withdrawal allowed except death or special condition. The scheme intends to bring pension benefits to people of the unorganised sector so that they can enjoy social security with a minimum contribution per month. People who work in the private sector are employed in occupations that do not give them the benefit of pension can apply for this scheme. They can opt for a fixed pension of INR 1,000 or 2,000 or 3,000 or 4,000 or 5,000 on attaining the age of 60. The amount of contribution and the individual’s age will determine the pension. The amount collected under the scheme is to be managed by Pension Funds Regulatory Authority of India (PFRDA) as per the investment pattern specified by the Government of India.

NEED FOR THE STUDY

To have a peaceful life after retiredby handling all the expenses in the same way as in the period of earning a regular income, the working individuals need to set a retirement plan while they work. The need for the study is to find out how far working individuals are aware of the available savings schemes and how far they have invested in those schemes as a secured retirement plan.

Anita and Pestonjee (2000) “Investment pattern and Decision making: The role of working women” studied that there is no significant difference among the respondents across the cities with respect to age, family size, type of family, marital status, level of education, occupation and annual income. No cultural and demographics patterns are associated with decision making of working women. In nuclear family women take independent decisions in the house hold related activities.

Gupta and Lepeng (2004) has categorised retirement planning into two phases as pre-retirement and post-retirement on the basis of four inter related models such as health evolution, wealth evolution, long term care insurance premium and cost structure. Two-way branching models were used to model stochastic health events and asset returns. He has stated that one assumes insurance is purchased for good and other assumes it may be purchased, relinquished and re-purchased.

Antolin (2010) , has found that current economic and financial crisis has shaken confidence in funded pension systemsin general and in defined contribution (DC) pension plans in particular. The study was conducted to provide recommendations on how to ensure adequate retirement income from DC pension plans. He concludes that in order to deliver adequate retirement income from DC pension plans with a certain degree of certainty, there is a need for comprehensive measures which include: higher contributions; increasing the contribution period by postponing retirement; setting as default options relatively conservative investment policies including life-cycle strategies; and managing risk in the pay-out phase with inflation indexed life annuities.

Krishna Moorthy (2012) under took a Study on Retirement Planning Behaviour of Working Individuals in Malaysia. In his study he identified several significant variables in the prediction of working individuals’ retirement planning behaviour, including age, education level and income level. The results of this study have implications for working individuals to do early planning for retirement to enable them to have a strong financial base after retirement.

Pereira T et al., (2016) under took a Study on retirement plan among dental professionals in Navi Mumbai, India. A comprehensive questionnaire survey was conducted and it was revealed that many senior dentists advised the younger dentists to begin investing early. The most important factor in preparing for a sound retirement life is to start an early financial planning. Doctor recommends getting a “financial check-up periodically – at least once a year – just like a medical check-up.”Through the present study, dentists can review their current level of savings and look for ways to increase it to a level identified to ensure they are on a path to a safe and secure retirement life. The assessment of the dentist's assets and asset sources leads to the conclusion that dentists are well prepared for their retirement.

Shailesh Singh, et al., (2017) has established a study on perception of individuals towards retirement planning. In his study he found, that there is impact of financial advice on saving towards the retirement objectives and the analyses revealed that majority of the respondents are investing with their own belief which is not advisable. He found that majority of the respondents were positive when asked the question do you think retirement planning is important irrespective of their income, age and occupation.

Research Methodology is presented as under:

OBJECTIVES OF THE STUDY

1. To examine their early retirement plan by investing in various schemes after setting off their expenses to have a secure retirement life.

2. To analyse that investment done in avenues is due to non-eligibility to receive pension.

3. To analyse the habit of saving a sum on monthly basis.

SAMPLING DESIGN

Universe of the study : Working individuals of all type of sector (public and private) within Chennai location.

Sampling unit: The study was carried out basically in three divisions of Chennai. The research was carried out considering Chennai North (38 respondents), Chennai South (24 respondents) and Chennai West (38 respondents). Working individuals includes all kinds of sector like IT, Professionals, Business holders, government employees and private employees in Chennai city.

Sample Technique: Simple random sampling technique

Sample Size: Data were collected from 100 respondents in Chennai.

Methods Of Data Collection

The data were collected by circulating questionnaires towards the target sample of working individuals of all type of sector within Chennai location. Secondary data were collected from websites, newspaper reports, books and trade journal.

Research Tools

We used Kruskal Wallis Test to test the association between demographic data and investment behaviour. Mann-Whitney U Test was applied to analyse theassociation between investment in avenues and marital status. Mean rank was used to find out the level of investment pattern between married and unmarried working individuals. Frequency analysis was used to rank the amount kept set aside as savings on monthly basis.

Hypothesis

In order to meet the objectives following Null Hypotheses are proposed

Ho1: There is no association between demographic factors and investment pattern.

Ho2: There is no association between investment done in avenues and marital status.

LIMITATIONS

1. The data were collected randomly from all type of working sectors where the study was not confined to figure out which sector of people are more aware in planning their retirement life.

2. A convenience sample of this study was selected from Chennai city.

3. The sample size is limited to 100.

4. Respondent’s bias could not be ruled out in questionnaire method.

Table 1 Inferential Analysis between Demographic Factor and Investment pattern in various saving schemes

|

Serial No |

Hypothesis |

Data Analysis Technique |

F-value |

Result |

|

1 |

There is no association between age and investment behaviour. |

Kruskal Wallis Test |

0.103 |

p = 0.103 > 0.05 (Null Hypothesis is accepted) |

|

2 |

There is no association between gender and investment behaviour. |

Kruskal Wallis Test |

0.624 |

p = 0.624 > 0.05 (Null Hypothesis is accepted) |

|

3 |

There is no association between occupation and investment behaviour. |

Kruskal Wallis Test |

0.154 |

p = 0.154 > 0.05 (Null Hypothesis is accepted) |

|

4 |

There is no association between years of service and investment behaviour. |

Kruskal Wallis Test |

0.126 |

p = 0.126> 0.05 (Null Hypothesis is accepted) |

|

5 |

There is no association between monthly income and investment behaviour. |

Kruskal Wallis Test |

0.007 |

p = 0.007 < 0.05 (Null Hypothesis is rejected) |

|

6 |

There is no association between area of location and investment behaviour. |

Kruskal Wallis Test |

0.280 |

p = 0.280 > 0.05 (Null Hypothesis is accepted) |

|

7 |

There is no association between marital status and investment behaviour. |

Kruskal Wallis Test |

0.187 |

p = 0.187 > 0.05 (Null Hypothesis is accepted) |

|

8 |

There is no association between family size and investment behaviour. |

Kruskal Wallis Test |

0.142 |

p = 0.142 > 0.05 (Null Hypothesis is accepted) |

Source: Primary data compiled by the scholar

*values significant at 5%

Interpretation

Table 1 depicts the results of Kruskal Wallis Test, of the association between demographic factors andinvestment pattern. It is very clear that demographic factors like age, gender, occupation, year of service, area of location, marital status and family size has no association with investment pattern since the F-value of each is more than 0.05.These values are obtained at a significant level of 5%.By testing the demographic variable monthly income depicts that the F-value 0.007 is less than 0.05 at a significant level of 5%, where Null hypothesis is rejected.Therefore, there is an association between monthly income and investment pattern. This reveals that to invest in any avenues money plays a very important role by comparing with other demographic factors. Hence on the basis of monthly income earned each working individual plan and invest in either of the avenues.

Table 2 – Analysis of Investment in avenues and Marital Status

|

Hypothesis |

Data Analysis Technique |

F Value |

Result |

|

There is no association between investment done in avenues and marital status. |

Mann-Whitney U Test |

0.187 |

P = 0.187> 0.05(Null Hypothesis is rejected) |

Source: Primary data compiled by the scholar

*values significant at 5%

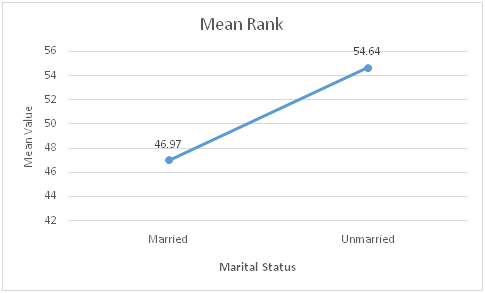

Chart 1-Mean Rank of investment in avenues based on Marital Status

Source: Primary data compiled by the scholar

Interpretation:

In Table 2, Mann Whitney U Test was used to test that there is no association between investment done in avenues and marital status. The test depicts that the F-value 0.187 is more than 0.05, the null hypothesisis accepted. Therefore, there is no association between investment done in avenues and marital status.

From chart1, investment in avenues married working individuals were ranked first with the value 46.97 percent and unmarried working individual were ranked second with the value 54.64 percent. Married people have many commitments like spending on provisions, medical expenses, School/college fees, and setting off debts if any, etc., After managing all these expenses they set aside a sum as a part of savings for their retirement life. Unmarried people’s commitments are lesser than married and free from responsibility which makes those to spend their life without any plan where the habit of saving is less when compared with married people.

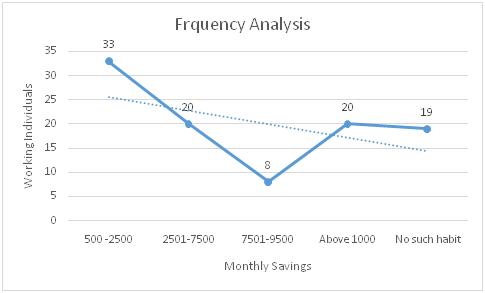

Table 3: Frequency analysis of amount kept set aside as savings on a monthly basis

|

Serial No |

Monthly savings |

Frequency |

Rank |

|

1 |

500-2500 |

33 |

1 |

|

2 |

2501-7500 |

20 |

2 |

|

3 |

7501-9500 |

8 |

4 |

|

4 |

Above 10,000 |

20 |

2 |

|

5 |

No such habit |

19 |

3 |

Source: Primary data compiled by the scholar

Chart 2 -Frequency analysis of amount kept set aside as savings on a monthly basis

Source: Primary data compiled by the scholar

Interpretation

From the above table and chart, majority of respondents have habit of saving within rs500 to rs2500 on monthly basis. 20 percent of them save a sum of rs 2501 to rs7500 and another group of 20 respondents save above rs10,000. It were also analysed that 19 percent of respondents have no such habit of saving even at least a sum of rs500. The reason could be due to lots of commitments, inflation rate, payment towards their debts, medical expenses and other expenses which they face in their daily life.

Following are the suggestions that could be considered by every individual to plan out for their basic investment in any avenues to develop their savings habit and for their retirement life as well.

1. The moment when people start to work each individual need to analyse and verify what all ways are there to save a sum for future needs, so that each one can frame an investment pattern at an earlier stage to grow up the amount.

2. Make sure that while investing diversify the risk by segregating the whole savings amount into bids like Rs500 towards PPF, Mutual fund and in Equity etc.

3. Before investing in any plan an individual must calculate the lump sum receivable after the duration of the scheme, based on this an investment plan can be framed out.

4. Working individuals should analyse their financial strength and financial issues or gaps in order to have a clear goal for the retirement planning and it should be achievable and attainable.

5. Working individuals need to have positive attitude toward the retirement planning and sound financial planning in the absence of pension benefits to achieve adequate retirement income and relax. Attitude of working individuals toward the retirement planning also play an important role in retirement planning behaviour.

As the population is increasing day by day, the family size also increases automatically where the expense ratio also gets high because of this many fail to save a part of amount at their current stage of working life in order to bear any expenses which arises at any point of time. This study is done to find out how working individuals are aware and in which avenues they opt to invest for their retirement life as well as to utilize the fund at any emergency time or for handling their monthly expenses. The findings of the study indicate that there is no association between demographic factors and investment behaviour, except the factormonthly income.There is no association between investment done in avenues and marital status. Married working individuals invest in avenues on a huge basis towards their retirement life when compared with unmarried ones.The study reveals that, majority of respondents have habit of saving within rs500 to rs2500 on monthly basis and 19 percent of respondents have no such saving habit even at least a sum of rs500 due to lots of commitments, inflation rate, payment towards their debts, medical expenses and other expenses which they face in their daily life.

GuptaAparna and LiLepeng (2004), A Modeling Framework for Optimal Long-Term Care Insurance Purchase Decisions in Retirement Planning. Health Care Management Science , Vol 7, Issue 2, pp 105–117.

Moorthy Krishna (2012), A Study on the Retirement Planning Behaviour of Working Individuals in Malaysia. International Journal of Academic Research in Economics and Management Sciences Vol. 1, No. 2, 2012 ISSN: 2226-3624.

Bhole L M (2004), Financial Institutions and Markets. Tata Mc Graw – Hill publishers, ISBN 0-07-05-8799-X, New Delhi.

Mishra, M N (1991): Life Insurance Corporation of India, R.B.S.A. Publishers, Jaipur.

Antolin Pablo (2010), Private pensions and the financial crisis: How to ensure adequate retirement income from DC pension plans. OECD Journal: Financial Markets and Trends, Vol. 16, Issue. 2, pp: 153-179, ISSN: 1995-2872.

Pestonjee D. M. and Balsara Anita. H (2000). Investment Pattern And Decision Making: The Role of Working Women (No. WP2000-12-04). Indian Institute of Management Ahmedabad, Research and Publication Department.

Reserve bank of India (2003): Report of the group to study the pension liabilities of the state governments, RBI Bulletin, October.

Rustagi R. P. (2012), Investment Analysis and Portfolio Management. Sultan Chand & Sons Publishing company, ISBN 978 -81- 8054 – 881 – 9, New Delhi.

Thakur Shailesh Singh, Jain SC and Soni Rameshwar(2017) A study on perception of individuals towards retirement planning. International Journal of Applied Research Vol. 3(2), 2017, pp. 154-157, ISSN Print: 2394-7500.

Pereira Treville, Shetty Subraj and Chande Mayura (2016),Study of retirement plan among dental professionals in Navi Mumbai, India: A comprehensive questionnaire survey. Annals of Tropical Medicine and Public Health Vol. 9, 2016 Issue. 3, pp. 159-164.

Websites

www.tn.gov.in/dop/p2.htm

http://www.pensionersportal.gov.in/salient%20features-f.asp

http:// www.yourdictionary.com/retirement

http://www.7thpaycommissioninfo.in/retirement-age-government-employees/

http://www.mapsofindia.com/my-india/government/atal-pension-yojana-for-social-security-in-india

https://sapost.blogspot.in/2012/03/central-and-state-government-employees.html -

http://www.simplifiedlaws.com/is-there-any-law-which-prescribes-the-retirement-age-in-india/#ixzz4fwIFjkak . Accessed 3 December 2014.

http://www.franklintempletonindia.com/en_IN/investor/investor-education/fund-basics/how-mutual-funds-work .

http://www.yourarticlelibrary.com/financial-management/equity-shares-meaning-features-advantages-and-disadvantages/43828/

https://india.gov.in/spotlight/national-pension-system-retirement-plan-all

https://www.bankbazaar.com/saving-schemes/ppf.html

https://en.wikipedia.org/wiki/Life_insurance_in_India