Pacific B usiness R eview I nternational

A Refereed Monthly International Journal of Management Indexed With THOMSON REUTERS(ESCI)

|

Zahra Iranmehr Management Department Bandar Anzali Branch Islamic Azad University Anzali, Iran E-mail:- Bahar.iranmehr1@gmail.com |

Badri Abbasi Management Department Bandar Anzali Branch Islamic Azad University Anzali, Iran E-mail:- bdrabbasi@yahoo.com |

The main purpose of this research is to investigate the effect of learning organization on financial performance with respect to knowledge-based performance of the branches of Islamic Azad University of Guilan. So the main question of the research is whether the learning organization affects the financial performance of the Islamic Azad University of Guilan in terms of knowledge-based performance? The population of the study was 132 financial and accounting experts (n = 132) who were used by census method. Three hypotheses were raised in this research. The results of the study showed that there is a significant relationship between learning organization and financial performance in terms of knowledge-based performance of branches of Islamic Azad University of Guilan. Also, the results showed that there is a significant relationship between learning organization and knowledge-based performance and financial performance of Islamic Azad University of Guilan. In addition, the findings showed that there is a significant relationship between knowledge-based performance and financial performance of Islamic Azad University of Guilan. Finally, some suggestions were made for future researchers.

Keywords : Learning organization, Financial performance, Knowledge-based performance

Today, given the highly competitive environment, achieving top financial performance is one of the most important concerns for universities. In this regard, universities as knowledgeable organizations are not excluded of this matter. One of the most important indicators of University performance is financial performance which has been studied by researchers. Meanwhile, some scholars have expressed the importance of a more accurate look at financial performance and believe that financial performance is the health and development of existing financial resources for the purpose of carefully controlling risk and controlling costs (Karen and Zhinqiu, 2017). Several factors have been mentioned in the studies to improve the management style of organizations in order to improve financial performance and includes motivation, strategic leadership, continuous learning, empowerment, information systems, knowledge-based subjects (Watkins and Dirani, 2013). Meanwhile, knowledge performance will also have an effect on the organization financial performance, because it is the ability to manage information and knowledge of the organization and controlling the appropriate type of knowledge and sharing it provides the organization with a competitive environment. Knowledge is necessary in the long-term success of an organization because intangible factors of knowledge have a positive relationship with the future performance of the organization (Banker and Srinivasan, 2000). Knowledge management is one of the new concepts in management science and it is one of the vital sources for the success of current organizations. One of the foundations for the establishment of knowledge management in organizations is organizational learning (Allameh and Moghadami, 2010). The nature of organizational learning or learning organization is a major factor affecting financial performance. The learning organization is also examined for the emerging phenomenon of organizations called knowledge-based performance that affects financial performance, because ensuring the optimal performance of academic elements such as intellectual capital and knowledge-based performance is essential in addition to financial performance for the sustainability of the university's institution. Hence, the learning organization allows the organization to integrate knowledge of individuals and organization as a living system in a universal way and enables the interaction between these sectors. Studies have shown that organizational learning is considered as a driving force for financial performance (Kaplan and Norton, 2004). In this way, Karen and Zhenqiu (2017) provide their research to examine the impact of the learning organization on financial performance and knowledge performance, which includes both dimensions, which is derived from the Marcic and Watkins conceptual model. It states that the dimensions of the learning organization have a direct effect on the performance of knowledge and financial performance and the dimensions of the learning organization have an indirect effect on financial performance through knowledge performance.

It should be noted that since learning organizations have developed a culture of learning at individual, team and organizational levels, therefore, it is able to meet its goals in responding to the crisis and adverse conditions and to respond appropriately to developments and by acquiring continuous knowledge and awareness, it will provide its own organizational improvement and continuity. Organizational learning is a continuous, dynamic and interactive process between individuals, groups and organizations and has a personal and social dimension. Its individual dimension refer to individual knowledge; a knowledge that one transfer to the organization. Also, its social dimension refers to common knowledge; a knowledge that all members transfer to the organization (Khanlari and Sabzeh Ali, 2014). Peter Senge (1990) was the first to define the learning organization: A learning organization is an organization that changes and improves its performance by using individuals, values and other sub-systems, relying on lessons and experiences, which are obtained (Safamanesh, 2015)

According to the above, the impact of the learning organization on financial performance, with a focus on knowledge-based performance is inevitable for organizations, especially organizations such as higher education institutions and universities. Since universities is considered as knowledge-based organizations for the growth and development of human beings, have their life and sustainability as the continuation and development of human knowledge, their life and durability are considered as the continuation and development of human knowledge and considering their financial performance as the most fundamental measure of sustainability in a competitive and volatile environment today is considered very important. Paying attention to financial performance, regardless of the knowledge-based performance that is the learning organization's output can provide major challenges at the university level. Knowledge-based performance can be defined as follows: Integrated approach to identifying, extracting, marketing, evaluating, sharing and creating all organizational knowledge resources and helps the organization achieve its long-term and short-term goals. Its purpose is to communicate the experts of organization with those who need specific knowledge. Creating such communication is facilitated by knowledge management processes and tools. Success in the field of knowledge-based performance requires the creation of a new environment for knowledge and experience to be easily shared (Fathihān, 2014).

After evaluating studies and research, it seems that although universities, which are among the most important organizations that play a major role in the growth and development of society, limited studies on the role of learning and financial performance and knowledge performance of this organization had been taken place. Therefore, these organizations have developed processes that not only have not caused a change in financial performance, but have caused a financial loss. This has led to the loss of the share of targeted markets in their competitive environment, and these organizations have suffered a financial crisis (Bafandeh Zendeh, 2011).

Outdated methods are still used; financial innovation has been faced with challenge, and paying attention to factors affecting financial performance seems to have diminished. Therefore, the researcher is trying to explain the influences of these three variables in the university. Therefore, the research question can be put forward as follows: What is the effect of learning organization on financial performance of Islamic Azad University of Guilan with regard to knowledge-based performance?

Higher education institutions and executive agencies and organizations, with each mission, goals and vision, ultimately operate in a national or international realm and are required to respond to customers, clients and stakeholders to be accountable to an organization whose goal is profitability and customer satisfaction, and an organization that aims to fully and precisely fulfill its legal tasks and assist in the research of the country's development goals. Therefore, the study of performance results is considered as an important strategic process

The learning organization is an organization that helps to enhance organizational learning through building structures and strategies. This organization has the skill and ability to create, acquire and transfer knowledge. Maquardt (1995) sees the learning organization as an organization that is capable and collectively learns. It constantly changes itself so that it can better collect, manage and use information for the purpose of the success of whole organization (Foruzandeh, 2009).

A learning organization is an organization in which members continuously develop themselves in the pursuit of the goals and desires they really seek. New patterns are used to expand the scope of thinking; there is space for collective aspiration; and finally, it is an organization whose members constantly learn how to learn collectively (Bahramzadeh, 2000).

Desirable organizations will be learning organizations. These organizations create opportunities for responsibility; they learn from experience; take risks and satisfied with the results and from the lessons learned (Talebi, 2002).

Learning organization is an organization in which learning is a constant need for all employees. It emphasizes how to learn and absorb and distribute new knowledge to create and produce new and needed information and knowledge and all of this knowledge is manifested in behavior and actions (Ghahramani, 2004).

There are different types of learning organizations. However many studies have been conducted on private organizations as learning organizations, there is few studies in the field of learning organization in public institutions and, principally, higher education institutions or universities (Bui & Baruch, 2012). Many scholars, instructors and policymakers have said that schools and universities should be redefined as learning organizations. This way, it can be faster to respond to the changing environment and provide more innovations in the organization and ultimately improve student's educational efficiency (Janežič, 2018).

Financial performance is a set of activities an organization performs in terms of the effectiveness of its financial structure. Financial performance based on the nature, mission and objectives of an entity can take place in the field of financial management, risk control and cost control (Kyoungshin, 2017)

Financial performance can be considered as a set of actions and information that is used to increase the level of optimal use of resources and resources to achieve goals in an economical manner with efficiency and effectiveness. Some part of the organizational performance indicators are financial indicators that are used to measure financial performance. In general, there are two economic perspectives on the basis of stakeholder groups in the organization. One view was that for-profit companies are looking for their own financial interests and do not think socially. Therefore, interest groups such as government, customers and people must enter the scene and impose their goals with companies using different mechanisms. The other group believes that for-profit companies are best placed to boost economic efficiency and productivity, with a view to gaining profit and it is not necessary to consider a goal other than the objectives of the owners of capital (increase the company value) (Fathi, 2006).

The most important financial goal of organizations is to maximize equity. It is believed that the incentive of equity holders to invest in organizations is to acquire the financial benefits from it, and increasing the material wealth of shareholders is among the most important of these benefits. The value of the stock depends on the organization's profit, because it is used to pay dividends or reinvest in productive assets (which will facilitate profit in the coming years). In addition to the organization's profits, the level of risk associated with investing is also important for shareholders. Sometimes the company's investment activities and subsidiary objectives may increase short-term corporate earnings but threaten the company's long-term stock worth. In this regard, it is usually the shareholders who are interested in earning profit in order to minimize the risk level of future profits in the coming years. Thus, according to the theory of Capital Asset pricing Model (CAPM), shareholders' goals are pursued in the form of increasing the value of wealth by increasing stock returns and reducing its risk. Given the definition of organizational effectiveness and organizational performance, and with respect to the goals that are considered in financial performance, its definition will be as follows: Financial performance is the degree to which the company achieves the financial goals of shareholders in order to increase their wealth (Fathi, 2006).

The concept of knowledge-based operation is a collection of activities and actions of organizations in the direction of scientific organization processes (Kyoungshin, 2017).

The concept of knowledge in the management of human resources of the university and its management of information systems is considered as the backbone of value creation units. One of the requirements for KM is to identify and provide its infrastructure (Hasanzadeh, 2008). Otherwise, knowledge-based performance can not be considered the focus of development and national economy. Of course, in many organizations, knowledge-based is viewed as a secondary action routine, that this look is mainly due to the inexplicable value added of knowledge in the short term. But in the university as a knowledgeable institution, this approach takes on an essential and vital role (Rafiee, 2009).

The knowledge-based approach is introduced as an approach by which the organization identifies, creates, achieves and uses knowledge to improve productivity in the organization. Today, the role and importance of knowledge management has become more and more evident and its successful implementation can have a significant impact on the efficiency and effectiveness of the organization. In today's complex world, organizational knowledge is rapidly becoming the main competitive advantage of organizations (Gu, 2017). Organizational knowledge in the fast-paced world is a good opportunity for organizations that know and manage it well. And at the same time, it is a serious threat to organizations that are not aware of environmental developments. Over the past decade, it has become clear that universities need to properly manage their intellectual capital and their technical tools within the realm of information. In this regard, performance management at the university is a methodology for producing, maintaining and exploiting all the facilities of a vast body of knowledge that each organization uses in its daily activities. Knowledge-based performance is a process that helps organizations to find, select, organize, disseminate and transfer information for activities such as problem solving, dynamic learning, strategic planning and decision-making. Considering the importance of knowledge-based performance management and its support, creates favorable conditions for the university. In addition to being able to survive in a complex competitive environment, it can take over from other academic institutions and lead the various fields of educational activities and research (Nekudary, 2011).

Using a conceptual model can well describe the interrelations between independent and dependent variables. The formulation of such a conceptual framework helps us to examine and test certain relationships to improve our understanding of the dynamics of the situation, and to provide a basis for conducting research studies.

According to the above, the conceptual model of the research can be drawn as follows:

Direct impact

Indirect effect

Figure 1) Conceptual Model of Research (Kim Karen, 2017)

There is a significant relationship between learning organization and financial performance according to knowledge-based performance of Islamic Azad University Branches of Guilan province.

Sub- hypothesis

1- There is a significant relationship between the learning organization and the knowledge-based performance of Islamic Azad University Branches in Guilan province.

2- There is a significant relationship between the learning organization and the financial performance of Islamic Azad University Branches in Guilan province.

3- There is a significant relationship between the knowledge-based performance and financial performance of Islamic Azad University Branches in Guilan province.

This is a field study. A questionnaire on the effect of learning organization on financial performance was distributed according to the knowledge-based performance of the Islamic Azad University Branches of Guilan province. Finally, by collecting questionnaires, data were analyzed using SPSS 22 software and smart pls 2 and the relationship between variables were investigated. The statistical population of the study is 132 financial managers and accountants of Islamic Azad University of Guilan province. The sample size was considered as the same as statistical population (132 people) and the questionnaires were distributed among them. In the present study, due to the limited research population, sampling in this study was not carried out and sampling was done in a census form. It should be noted that according to the nature of the research variables, the unit of analysis is organizational. In fact the University Branches are the basis of the study's analysis. Therefore, the available Branches of the researcher, namely 15 academic Branches eligible for study, were included in the research. Of course, units responded to the questionnaire was all financial and accounting experts at the University.

Inferential statistics

In this research, due to the low volume of the sample, structural equation modeling with partial least squares approach (PLS) and Smart PLS software for testing the hypotheses are used.

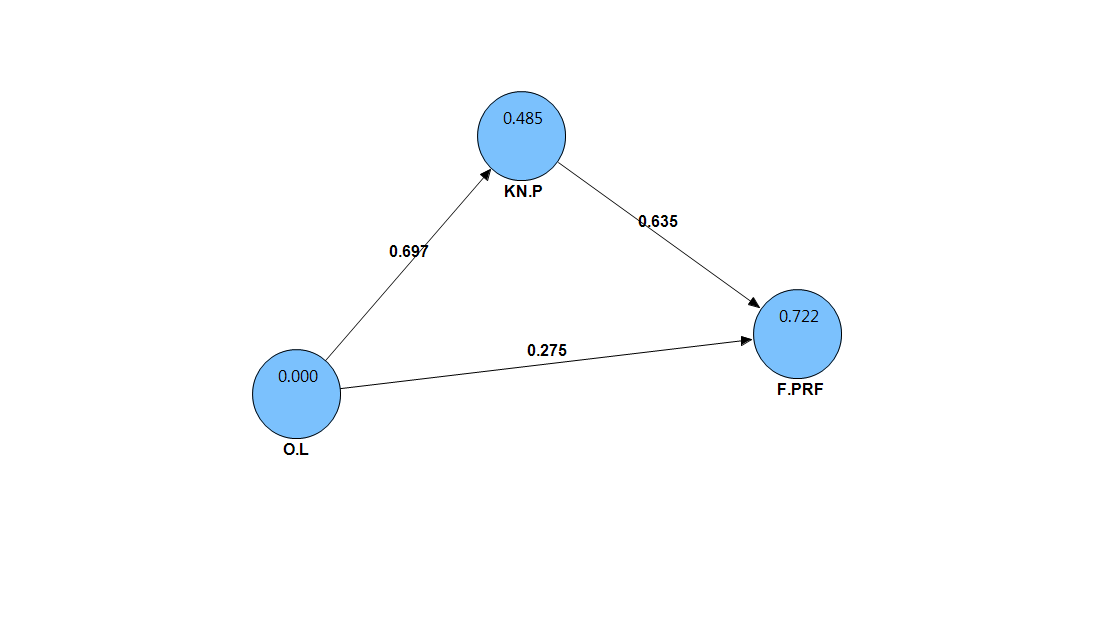

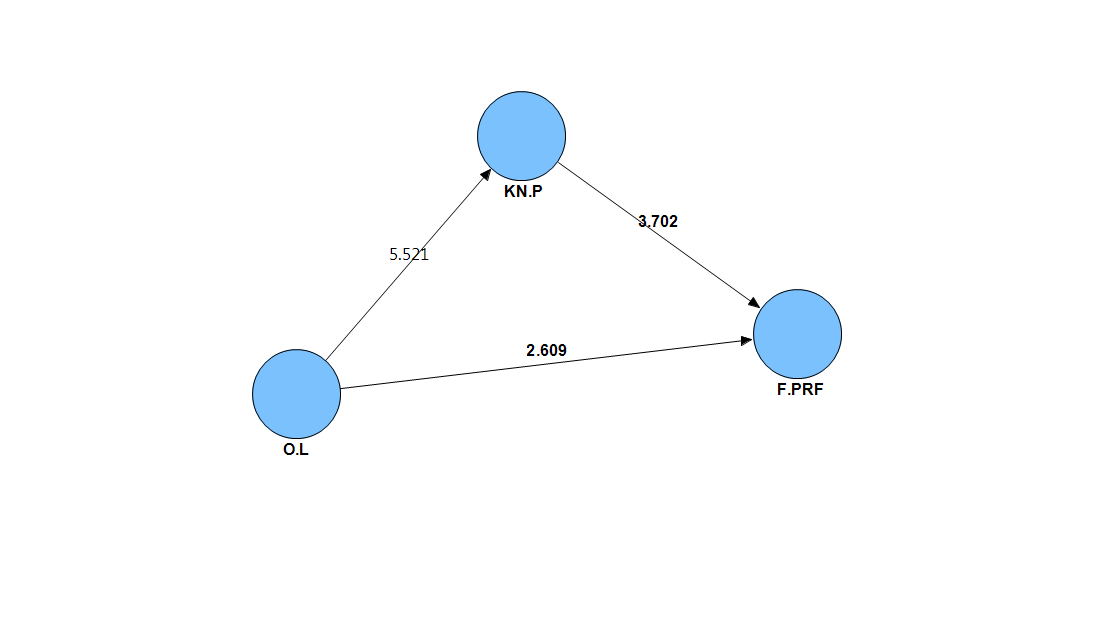

The fitting of the model is carried out in three parts of the model measurement, structural model and general model which examines to what extent the research model is appropriate to the data collected from the statistical sample. After verifying the fit of the model, the researcher is allowed to examine and test the research hypotheses. PLS software after obtaining data about variables presented the final model of the research, which includes a large part of the analysis as Fig. 2 in the estimation of standardized coefficients and model (3) in the t value coefficients.

Figure2. Final model of the research in the estimation of standardized path coefficients

Figure3. The final model of the research in the case of t value

Hypotheses Testing

Table 1: Study of the main hypothesis of the research

|

Hypotheses |

Standard path coefficient |

t value |

P (sig) |

Confirm

|

Result |

|

learning organization |

0.697 |

5.521 |

P<0.05 |

Confirm |

The variables of knowledge-based performance act as a mediator variable in the relationship between learning organization and financial performance. |

|

knowledge based performance

|

0.635 |

3.702 |

P<0.05 |

Confirm |

|

|

learning organization |

0.275 |

2.609 |

P<0.05 |

Confirm |

|

|

Direct path coefficient=.0275 |

Indirect path coefficient=0.442 |

||||

|

t=2.609 Direct |

Indirect t=3.074 |

||||

|

Total path coefficient=0.717 |

|||||

Sub- hypothesis

1- There is a significant relationship between the learning organization and the knowledge-based performance of Islamic Azad University Branches in Guilan province.

According to the structural model of the research, in the case of significant coefficients, the t-value between the two variables of the learning organization and the knowledge-based performance is outside the range (-1.96 & 1.96), so the hypothesis is accepted. The intensity of the relationship between the learning organization and the knowledge-based performance is also equal to 0.697. Compared with previous studies, we can say that the results obtained from this hypothesis is consistent with Shams et al (2014), that there is a relationship between learning organization and knowledge-based performance.

Table 2: Analysis results of the first hypothesis

|

Hypothesis |

T-Value |

Standard path coefficient |

Results |

|||

|

H1 |

learning organization |

|

knowledge-based performance |

5.521 |

.0697 |

Confirm |

2- There is a significant relationship between the learning organization and the financial performance of Islamic Azad University Branches in Guilan province .

According to the structural model of the research, in the case of significant coefficients, the t-value between the two variables of the learning organization and financial performance is outside the range (-1.96 & 1.96), so the hypothesis is accepted. The intensity of the relationship between the learning organization and the financial performance is also equal to 0.275. Compared with previous studies, we can say that the results obtained from this hypothesis are consistent with Khanlari and Rezvan (2014), Beiranvand and et al (2013) that there is a relationship between learning organization and financial performance.

Table 3: Analysis results of the second hypothesis

|

Hypothesis |

T-Value |

Standard path coefficient |

Results |

|||

|

H2 |

learning organization |

|

Financial performance |

2.609 |

0.275 |

Confirm |

3- There is a significant relationship between the knowledge-based performance and financial performance of Islamic Azad University Branches in Guilan province .

According to the structural model of the research, in the case of significant coefficients, the t-value between the two variables of the knowledge-based performance and financial performance is outside the range (-1.96 & 1.96), so the hypothesis is accepted. The intensity of the relationship between the learning organization and the financial performance is also equal to 0.635. Compared with previous studies, we can say that the results obtained from this hypothesis are consistent with Taheri (2013) that there is a relationship between knowledge-based performance and financial performance

Table 4: Analysis results of the third hypothesis

|

Hypothesis |

T-Value |

Standard path coefficient |

Results |

|||

|

H3 |

knowledge-based performance |

|

Financial performance |

3.702 |

0.635 |

Confirm |

For the main hypothesis, that there is a significant relationship between learning organization and financial performance according to knowledge-based performance of Islamic Azad University Branches of Guilan province, given the confirmation of direct relationship between learning organization and financial performance, knowledge-based performance has a full mediator role. Compared with previous studies, we can say that the results obtained from this hypothesis is consistent with Rezaei (2016), Nemati (2015), Harati and Poursafee (2011), that there is a relationship between learning organization, financial performance and knowledge-based performance.

Given that there is a significant relationship between learning organization and financial performance according to knowledge-based performance of Islamic Azad University Branches of Guilan province, it is suggested to managers to change their way of thinking (cultural, social, etc.) to manage value, and use value management to save costs (service costs, functional, support, etc.). They should understand the purpose and value of the implications of the university's executive programs and enhance financial plans, because the allocation of resources required for management does not have the required quality. Managers should identify the capacity and limitations of the accounting and cost control system at the university and let the staff speak freely about their problems and objections.

Given that there is a significant relationship between the learning organization and the knowledge-based performance of Islamic Azad University Branches in Guilan province, it is suggested to managers to be more committed to their organization, because the managers and leaders are more committed, knowledge management is better deployed. Organizations need effective and efficient employees to achieve their goals for comprehensive development and development. In general, the efficiency and effectiveness of organizations depend on the efficiency and effectiveness of human resources and employees in that organization. The dissemination of knowledge and creating a learning environment is one of the most important factors affecting the performance of employees. Universities have a close relationship with students due to the production of services. Because of the importance of knowledge and knowledge dissemination and knowledge learning at universities, these types of organizations have a very high level of learning in terms of learning. Hence, financial managers of universities should begin to move towards learning. In fact, that is in such an environment where creativity, innovation, self-confidence and fertility of ideas and their transformation into knowledge will take place.

Given that there is a significant relationship between the learning organization and financial performance of Islamic Azad University Branches in Guilan province, it is suggested that to further enhance the system visibility of all employees, different departments should have a clear view of organizational goals and to know how to help develop these goals. Organizational learning uses knowledge, understanding and shared beliefs and along with the common language and the involvement of all employees, the speed of this process will increases. Therefore, the existence of a common language creates the integration of knowledge, which is a key aspect of the development of organizational learning. As a result, efforts to improve and maintain the knowledge work of experts will be one of the most important preconditions for improving their performance. Prerequisite to reach this object is more attention of the authorities and policy makers of universities to learn the experts and provide innovative and creative ways to reform the structure and function of the organization, including studying the causes of the problems, facilitating and encouraging learning at various levels and individual and group goals for the achieve organizational goals.

Given that there is a significant relationship between the knowledge-based performance and financial performance of Islamic Azad University Branches in Guilan province, it is suggested to managers use financial mechanisms as an important tool in policy making and educational policy development. By allocating financial resources to training groups and delegating the necessary powers to utilize financial resources, more incentives are created for financial managers to work. Managers are advised to accept their mistakes and seek to resolve them. They will pay more attention to new ideas for people to apply more knowledge. Managers should pay more attention to continuous learning and educational needs. Managers should establish a system for evaluating performance and designing and implementing a proper system. Based on performance, they must have suitable pay systems and rewards to keep employees knowledgeable and thus enhance the financial performance of the organization.

Limitations and suggestions for future researchers

In this study, the most significant problems can be categorized as follows : The first thing to keep in mind is that the findings of this research are limited to the spatial scope of the research. It should be noted that this research was carried out at the Branches of Islamic Azad University of Guilan province, therefore, before generalizing recent findings to other provinces, in order to understand the effect of learning organization on financial performance, according to the knowledge-based performance of Islamic Azad University of Gilan Branches, similar research should be done in other provinces. In this research, the knowledge sharing variable that could affect knowledge-based performance has not been used . In this research, only a questionnaire was used for collecting data.

Given the geographic scope of the research and the organization under study, future research can be done in other geographical areas as well as in other public and private organizations. In the forthcoming study, it is suggested that, given the limitations, the knowledge sharing variable being used that can affect knowledge-based performance. It is suggested that other data gathering methods, such as interviews, be used to collect information in addition to the questionnaire method.

. Allameh, Seyyed Hassan and Moghadami, Mohsen (2010), "Investigating the Relationship between Organizational Learning and Organizational Performance", Research Journal of Scientific-Research Executive, 10 (1). 100-75

. Asadollahi, Ehsan (2014), The Relationship Between Knowledge Management Structure and the Learning Organization from the Perspective of Physical Education Experts, Knowledge Management Basics Studies, 1(1). pp. 57-51

. Bafandeh Zendeh, Alireza (2011), Investigating the Impact of Environmental Uncertainty on Selection of Knowledge Management Strategies in the Product Area (Case Study: Universities and Higher Education Institutions of Khorasan Razavi), Scientific Journal, 27(4). pp. 840-823

. Bahramzadeh, Hossein Ali (2000), "Organizational Learning and Systemic Thinking", Scientific Research Journal of Management, Tehran; Organization of Publications and Publications of the Ministry of Culture and Islamic Guidance, 44

. Banker, R.D., Potter, G. and Srinivasan, D. (2000), “An empirical investigation of an incentive plan that includes nonfinancial performance measures”, The Accounting Review, 75 (1). pp. 65-92

. Beiranvand, Abuzar and Zainab (2013), Comparative study of factors affecting organizational learning and creating learning organizations, National Conference on New Approaches to Business Management, Tabriz University and Industrial Management Organization, August

. Bui, H. T., & Baruch, Y. (2012). Learning organizations in higher education: An empirical evaluation within an international context. Management Learning, 43(5), 515–544.

. Fathi Saeed (2006), Designing Influence of Information Technology Influence on Financial Performance Measures with Meta-Analysis Approach, Ph.D, Tarbiat Modares University

. Fathihan, Mohammad (2014), The Effect of Knowledge Management on Organizational Performance Using Balanced Scorecard, Sharif Management, 147-139

. Feyzi, Tahereh (2010), Relationship between knowledge management and its components with dimensions of learning organization in Islamic Azad University, Science and Research Branch of Tehran, Public Administration, 1(1). PP 184-155

. Foruzandeh, Lotfollah. (2009). Study of the Learning System in Telecommunication Company Based on Learning Organization Model. Peyk-e Noor Journal, 7(4). PP 3-12

. Ghahremani, Ali Adineh (2011), Study of the Status of Knowledge Management Infrastructures in Tabriz University from the Viewpoints of Faculty Members, Journal of Library and Information Science Research, 58(57). pp. 85-63.

. Gu, Q., Jitpaipoon, T., Yang, J., (2017), The impact of information integration on financial performance: A knowledge-based view, International Journal of Production Economics, doi: 10.1016/j.ijpe.2017.06.005

. Hassanzadeh, Mohammad (2008), Investigating the Infrastructural Factors of KM in the Government of the Islamic Republic of Iran. Shahed University Journal of Science and Research, 16 (35). pp. 28-11

. Janežič, Matej; Vlado Dimovski, Milan Hodošček (2018), Modeling a learning organization using a molecular network framework, Computers & Education 118 (2018) 56–69

. Kaplan, R. S. and Norton, D. P. (2004), Strategy Maps: Converting Intangible Assets intoTangible Outcomes. Harvard Business School Press, Boston, MA

. Khanlari, Amir and Sabzeh Ali, Rezvand (2014), "Investigating the Relationship between Organizational Learning and Performance through the Innovation Process", Business Management, 6(4). Pp773-790.

. Kyoungshin, Kim Karen. E. Watkins, Zhenqiu (Laura) Lu , (2017)," The focusing on knowledge performance and financial performance ",European Journal of Training and Development, 41(1).

. Marquardt, Michael (2006), Creating a Learning Organization. Translated by Mohammad Reza Zali, Tehran: University of Tehran, Entrepreneurship Center

. Nekodari, Maryam (2011), Investigating the Facts of Knowledge Management Facilitator in Crisis Management Organization, Public Management Research, 4(13). pp. 119-95

. Nemati, Mohammad Ali (2015), Relationship between Knowledge Management Dimensions and Educational Performance of Academic Members, 8 (4). pp. 208-203

. Rezaei, Behrooz (2016), Factors Affecting the Creation of a Learning Organization, Industrial Management Studies Quarterly, 13(2). pp. 146-123

. Rafiei, Saeed Hossein (2010), Linking the Knowledge Management System and Performance Evaluation, an Effective Human Resources System A CASE STUDY OF KNOWLEDGE MANAGEMENT SYSTEM AND ANALYSIS OF THE KNOWLEDGE OF NETWORK OF IRANIAN TECHNOLOGY ANALYSIS, TECHNOLOGY DEVELOPMENT, 6(22). P. 18-11

. Senge, Peter & Associates (2008), Fifth Commandment in the Field of Practice: Strategies and Tools for Creating a Learning Organization, Translated by Mehdi Khademi Grashchi, Masoud Soltani and Abbas Ali Rastegar, Tehran: Asia, First Edition

. Shams, Gholamreza, Pardakhtchi, Mohammad Hassan and Maleki, Hatam, (2014), "The Impact of Learning Organization on Organizational Performance through Organizational Learning: A Case Study", New Educational Ideas, Faculty of Educational Sciences and Psychology, Alzahra University,10 (3). Pp45-23

. Safmanesh, Parisa (2015), The Effect of Components of a Learning Organization on Employer's Performance of Employees of an Insurance Company, Insurance Survey / MSCM / 1(3). pp. 124-95

. Taheri, Morteza (2013), Exploring and Designing an Execution Model for the Effectiveness of Organizational Training: A Study Based on Theory, Quarterly Journal of Human Resource Education and Development, 3(9. pp.161-137

. Talebi Kadouei, Fazl (2002), "Learning Organization; An Evolutionary, Dynamic and Desirable Organization", Managing Scientific Journal, Tehran, Organization for the Publishing of the Ministry of Culture and Islamic Guidance, 64(63).

. Harati, Marzieh, Parsahafi, Hadi and Khamassan, Ahmad (2011), "The relationship between learner organization capabilities and performance of organizational learning levels", Iranian Institute of Science and Technology

. Watkins, K.E. and Dirani, K.M. (2013), “A meta-analysis of the dimensions of a learning organization questionnaire looking across cultures, ranks, and industries”, Advances inDeveloping Human Resources , 15(2). pp. 148-162

knowledge

based performance

knowledge

based performance