Pacific B usiness R eview I nternational

A Refereed Monthly International Journal of Management Indexed With THOMSON REUTERS(ESCI)

|

Prof. Padmapriya R. Katagal Asst. Professor BET’s Global Business School Old P.B. Road, B.C. No 188, Belagavi, Karnataka Contact No.:- Off- 0831- 4200247 / 9900421002 E-mail:- padmapriya@betgbs.in |

Dr. Rohit R. Mutkekar Asst. Professor Goa Institute of Management, Goa Contact No:- 919145530970 E-mail:- rohitrm@gim.ac.in |

Dr. Anilkumar G. Garag Entrepreneur, Hubli, Karnataka Contact No:- 9341105794 E-mail:- agarag@gmail.com |

Purpose: The paper focuses on studying the perceptions of customers towards e banking service quality in North Karnataka. It underlines the important e service attributes from customer point of view. It also evaluates the important of e- service dimensions on developing customer satisfaction.

Design: The descriptive research design is adopted. The survey method is used for data collection.The e banking customers of north Karnataka are the respondents for the research. Data is tested using the factor analysis, correlation analysis and Regression analysis.

Findings of the study: The various E- service quality dimensions identified by the different researchers were explored. The factor analyses explored the five dimensions named as Reliability and Convenience, Website Aesthetics, Privacy and Confidentiality; Responsiveness and Safety. Regression analyses confirmed that the identified dimensions of e-services of banks are important predictors of customer satisfaction in North Karnataka.

Key words : e- banking, e services, service quality, customer satisfaction.

Services sector is gaining importance in developing economies due to its ability to generate employment. Within the services sector financial institutions such as banks are the important service institutions of an economy. After liberalisations Indian banking system has undergone many changes including the customer delivery processes. The competition from foreign banks with the high tech services forced private and public banks to reforms the service process. Due to increase in the customer expectations from the banks it is challenging to retain and attract new customers for the banks. Banks have become customer centric with the use advanced technology in their process.

E services provide strategic benefits to service provider by enhancing operational efficiency, profitability by reducing time and cost involved in service delivery. They also provide convenience of availing service 24/7 to customers. E-service quality is gaining importance as it is directly linked to customer satisfaction and retention. Service quality is determinant of success not only in a traditional environment but also in an online market space. (Wolfinger and Gilly).

Zeihaml et. al, introduced the concept of e- SQ and their role in service quality delivery to customer. They define service quality as “the extent to which a website facilitates efficient and effective shopping, purchasing and delivery of products and services.”

Customer satisfaction and loyal customer base is the outcome of providing quality services. Many studies have conducted to know the influence of service quality on customer satisfaction.The significance of service quality as an antecedent of customer satisfaction and customer loyalty is approved. (Zeithml et.al.,Rust,). Service providers can achieve competitive capabilities by providing quality e services. (P. Olivier et.al)

There are range of research done to uncover the dimensions of E-service quality in general, in many parts of the world. The purpose of this paper is to know the e- service quality of banks in North Karnataka and to reveal the dimensions of e service quality from customer’s point of view.

1) To analyze the E-service quality of banks operating in North Karnataka.

2) To underline the important E- service quality dimensions as per the customer perceptions

3) To know the impact of E- service quality on customer satisfaction.

A.Parasuraman, Valarie A Zeithaml, Arvind Malhotra( 2005) conceptualized and tested and developed multiple Item Scale for Assessing Electronic Service Quality delivered by websites, known as E-S-QUAL. The scale is limited to measure online service quality of sites on which customers shop online.

They have developed the preliminary scale identifying various website features and categorized them into 11 dimensions with 121 items. The 11 e-SQ dimensions are: Reliability, Responsiveness, Access, Flexibility, Ease of Navigation, Efficiency, Assurance, Security/Privacy, Price knowledge, Site aesthetics, customization/ personalization.

After conducting exploratory factor analysis on the items the final E-S-QUAL scale consisting of 4 dimensions with 22 items was expressed as follows.1) Efficiency: The ease and speed of accessing and using the site. 2) Fulfillment: The extent to which the site’s promises about order delivery and item availability are fulfilled.3) System availability: The correct technical functioning of the site4) Privacy: The degree to which the site is safe and protects customer information.

The e recovery service quality scale - E-RecSQUAL, consisting of 11 items on 3 dimensions was expressed as follows:1) Responsiveness 2) Compensation 3) Contact.

Zhilin Yang, ShaohanCai, Zheng Zhou, Nan Zhou (2004), in their research paper, developed instrument to measure service quality of information presenting web portals. Researchers after extensive literature review believe that service quality of websites is under defined construct & there is considerable confusion in understanding service quality for websites They have identified five service quality dimensions perceived by users of an information presenting web portals they are: Usability, Usefulness of content, adequacy of information, accessibility, and interaction. Questionnaire was drafted based on these dimensions and data was collected. Through simple random sampling technique. The analysis proved the model excellent statistically. It passed through the reliability and validity tests. The study provided five service quality dimension to measure information presenting web portals.

BoongheeYoo& Naveen Donthu (2001), in their research paper have worked on internet shopping sites and focused on perceived service quality of consumers of such sites. They found out that previous measures were having many limitations and the measures do not show the structure of the dimensions of site quality. To develop the scale, they have generated items based mainly on consumers own descriptions The SITEQUAL comprised nine items representing four dimensions. The dimensions are: Ease of Use, Aesthetic Design, Processing Speed and Security.

They investigated five relevant constructs such as attitude towards the site, site loyalty, site equity, purchase intention, and site revisit intention. These constructs were regressed on the SITEQUAL. The series of regression analysis shows the SITEQUAL dimensions are important predictors of the examined variables. Attitude toward the site & site revisit intention were the function of Ease of Use, Aesthetic design & Security. Purchase intention was function of two dimensions Ease of Use & Security. In the regression analysis two dimensions Ease of Use & Security were consistently proved more significant than other dimensions. Therefore, Ease of Use & Security are important quality criteria of internet shopping sites that influence consumer attitudes and behaviours.

Various researches have conducted to know the dimensions of e- service quality in Online retailing, internet banking, online financial service etc. Majority of the studies have dimensions of traditional service quality and website interface quality dimensions. The following table provides the list of studies undertaken to explore the dimensions of e- service quality.

Table no. 1 providing the e- service quality dimensions identified by researchers.

|

Author |

Scale |

Industry |

Dimensions |

|

Lociano et.al. ( 2000) |

WEBQUAL |

Online Retailing |

Informational fit to task, Interaction, Trust, , Response time, Design, Intuitiveness, Visual appeal, Innovativeness, flow, Integrated communication, business process and sustainability |

|

Zeithml et.al. (2000) |

Online Retailing |

Reliability, Responsiveness, Access, Flexibility, Ease of Navigation, Efficiency, Assurance/trust, Securuty/privacy, Price knowledge, Site aesthetics, Customisation/personalisation |

|

|

Liu & Arnett( 2000) |

Company websites |

Quality of information, service, system use, playfulness by consumers, design of websites |

|

|

Yang Peterson et. al. |

Internet Pharmacies |

Ease of Use, content of website, accuracy of content, Timeliness of content, Aesthetics, Privacy |

|

|

Boonghee Yoo et.al ( 2001) |

SITEQUAL |

Shopping site |

Ease of Use, Aesthetic Design, Processing Speed , Security |

|

Wolfinger ( 2002) |

.comQ |

Retailing websites |

Website Design, Reliability, Privacy/ Security |

|

Szymanski et.al |

Retailing |

Online convenience, merchandising, site design, financial security |

|

|

Zeithml et.al. (2002) |

eSERVQUAL |

Websites |

Efficiency, Reliability, Fulfillment, Privacy |

|

Zeithml et.al. (2002) |

Recovery e-SERVQUAL |

Websites |

Responsiveness, compensation, contact |

|

Mathew Joseph et.al |

E- banking |

convenience/accuracy; 2 feedback/complaint management; 3 efficiency; 4 queue management; 5 accessibility; and 6.customisation. |

|

|

Siu and Mou (2005) |

Internet banking |

credibility, efficiency, problem handling and security |

|

|

Jayawardhena (2004) |

Internet banking |

access, web site interface, trust, attention and credibility |

Based on the literature review the dimensions considered to measure the e- service quality of banks in North Karnataka are:

1) Reliability, 2) Convenience 3) Privacy 4) Safety 5) Responsiveness

6) Website Aesthetics 7)Financial Product Information

The descriptive research is undertaken to study the research questions. The primary data is collected through the survey method. The questionnaire was used to collect the required data. The area of study was restricted to surveying the customers of e- banking in North Karnataka. The districts covered under the survey are Belagavi, Vijayapur, Bagalkot, Dharwad, Haveri, Uttara Kannada & Gadag. The purposive sampling technique is employed to collect the data. The sample size of the study is 1000. The samples were collected from the various offices of Govt, private and educational institutes, shops etc.

Exploratory factor analysis (EFA) using principal component analysis (PCA) under the restriction that the Eigen value of each generated factor is more than one was conducted on 23 service quality measures. The suitability of data for factor analysis was assessed by computing the correlation matrix. The regression analyses is conducted to know the impact of E-service quality dimensions on customer satisfaction.

. Reliability Test Using Cronbach alpha

To measure the reliability or internal consistency of 23 test items Cronbach alpha is used. Cronbach alpha measures of any given instruments consistency, that is the extent to which it is consistent to measure the concept.

Table No 2: Reliability statistics

|

Cronbach’s Alpha |

N of Items |

|

.897 |

23 |

As per the table No 2, the Cronbach’s Alpha co-efficient for Part E (0.897) is sufficiently reliable (>0.7) which validates the scale reliability for the statements in the questionnaire.

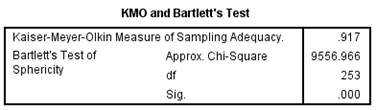

KMO and Bartlett’s test.: Table No 3 :KMO and Bartlett’s Test

From Table no 3, we observe that the data satisfies KMO test for sampling adequacy (0.917 > 0.5) and Bartlett’s test sphericity is significant (p-value < 0.5). The data is fragmented into five components based on the volume of variance generated.

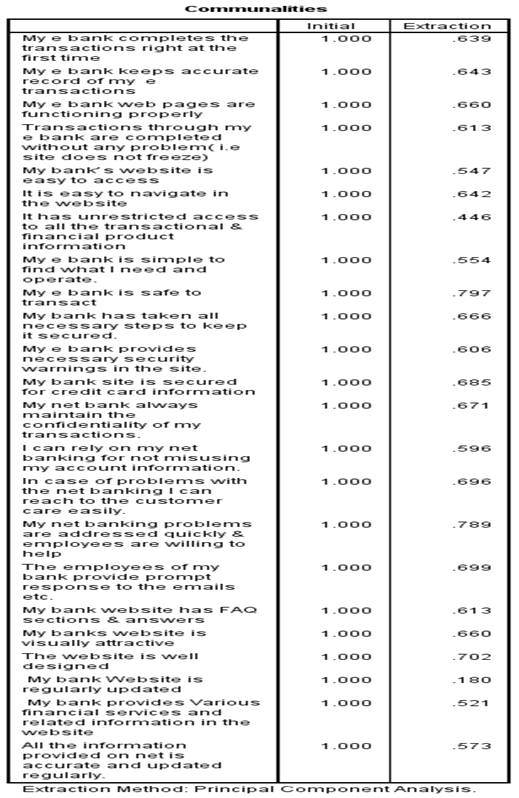

Table 4: Communalities

Table no 4 gives the extraction level of the variables obtained through principal component extraction method.

Various attributes which contribute to service quality of internet banking

for a bank is incorporated in this section of the questionnaire. Factor

analysis is performed using the principal component extraction method with

varimax rotation.

Various attributes which contribute to service quality of internet banking

for a bank is incorporated in this section of the questionnaire. Factor

analysis is performed using the principal component extraction method with

varimax rotation.

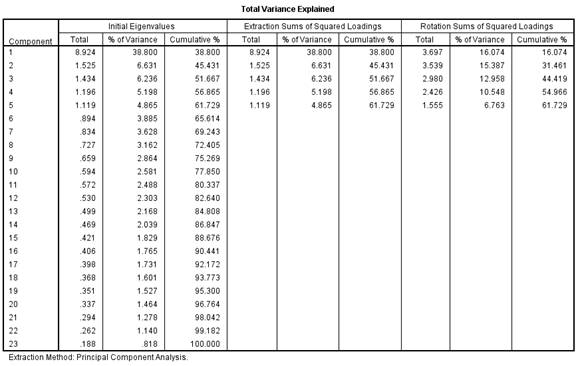

Table No 5 : Total variance of Variable

Table number 5 provides details of the total variance as explained by the variables contributing to service quality of internet banking. Here we observe that the data is fragmented into five components based on the volume of variance generated. From the rotation sums of squared loadings, we observe that 61.729% of the total variation is being explained by the data.

Table no.6 : Sorted rotated factor loadings with varimax rotation

|

Variable Number |

Variable Definition |

Components |

||||

|

1 |

2 |

3 |

4 |

5 |

||

|

Var 1 |

My e bank web pages are functioning properly |

0.732 |

||||

|

Var 2 |

My e bank completes the transactions right at the first time |

0.722 |

||||

|

Var 3 |

Transactions through my e bank are completed without any problem( i.e site does not freeze) |

0.688 |

||||

|

Var 4 |

My e bank keeps accurate record of my e transactions |

0.687 |

||||

|

Var 5 |

My bank’s website is easy to access |

0.619 |

||||

|

Var 6 |

It is easy to navigate in the website |

0.520 |

||||

|

Var 7 |

It has unrestricted access to all the transactional & financial product information |

0.517 |

||||

|

Var 8 |

My e bank is simple to find what I need and operate. |

0.432 |

||||

|

Var 9 |

The website is well designed |

0.739 |

||||

|

Var 10 |

My banks website is visually attractive |

0.718 |

||||

|

Var 11 |

All the information provided on net is accurate and updated regularly. |

0.648 |

||||

|

Var 12 |

My bank website has FAQ sections & answers |

0.646 |

||||

|

Var 13 |

My bank provides Various financial services and related information in the website |

0.615 |

||||

|

Var 14 |

My bank Website is regularly updated |

0.398 |

||||

|

Var 15 |

My bank site is secured for credit card information |

0.765 |

||||

|

Var 16 |

My net bank always maintain the confidentiality of my transactions. |

0.712 |

||||

|

Var 17 |

My bank has taken all necessary steps to keep it secured. |

0.628 |

||||

|

Var 18 |

I can rely on my net banking for not misusing my account information. |

0.624 |

||||

|

Var 19 |

My e bank provides necessary security warnings in the site. |

0.622 |

||||

|

Var 20 |

My net banking problems are addressed quickly & employees are willing to help |

0.827 |

||||

|

Var 21 |

The employees of my bank provide prompt response to the emails etc. |

0.768 |

||||

|

Var 22 |

In case of problems with the net banking I can reach to the customer care easily. |

0.740 |

||||

|

Var 23 |

My e bank is safe to transact |

0.873 |

||||

Table No 6, Provides details of factor loading associated with various variables in sorted form. Generally, factor loading represents how much a factor explains a variable. High loading indicates that the factor strongly influences the variable. Assuming a factor loading of more than 0.75 as having very high impact; between 0.60 to 0.75 as high impact; between 0.45 to 0.59 as moderate impact and below 0.45 as low impact on the variables, it can be concluded from Table 6 that some variables which have moderate and low impact need attention for the quality improvement of e-banking.

Based on the results of factor analysis, the variables are classified into five dimensions which are suitably named. The dimensions and the corresponding variables are shown below:

Table no 7 showing the dimensions and respective variables of e-banking

|

Dimensions |

Variables |

|

Reliability and Convenience |

Var1, Var2, Var3, Var4, Var5, Var6, Var7, Var8 |

|

Website Aesthetics and Financial Product Information |

Var9, Var10, Var11, Var12, Var13, Var14 |

|

Privacy and confidentiality |

Var15, Var16, Var17, Var18, Var19 |

|

Responsiveness |

Var20, Var21, Var22 |

|

Safety |

Var23 |

The responses of all respondents are averaged across the five dimensions as given in Table 5-

Table No 8: Descriptive Statistics of Factor analysis

|

|

N |

Mean |

Std.Deviation |

|

Safety ReliaAndconv PrivacyAndConfi WebAesth Responsiveness Valid N (listwise) |

961 961 961 961 961 961 |

4.14 4.07 4.00 3.90 3.63 |

.780 .588 .682 .664 .857 |

The descriptive statistics of five dimension is given in Table 8. The customers were asked measure the e banking service quality of their respective banks. From Table 8, we can conclude that the customers perceive that the safety measures taken by the banks is of high quality and it is ranked no. one amongst the other factors. Reliability and convenience factor stands second in providing quality to customers followed by Privacy and confidentiality which is ranked third by the customers. Website aesthetics and Financial product information is ranked fourth by the customers followed by Responsiveness. Responsiveness is the least appreciated dimension to provide the service quality to customers.

Based on the above table we can infer that the safety dimension is the most influential factor in measuring the E-service quality of banks in North Karnataka, and is Ranked no.1 by consumers, followed by Reliability and convenience, Privacy and confidentiality, website aesthetics. Responsiveness is the least influential factor in measuring the Eservice quality in north Karnataka.

Analysing the association between the identified E- Service dimensions through Correlation Analysis:

Correlation Analysis: Statistical relationships are about which elements of data hang together and which ones hang separately. It is about categorizing variables that have a relationship with one another and categorizing variables that are distinct and unrelated to each other.

To find the degree of association between the identified service quality dimensions, correlation analysis is applied. The correlation coefficients between various dimensions are computed and shown as below in Table 9

Table number 9: correlation between various dimensions of E-service quality

|

|

Reliability and Conv |

WebAesth

|

PrivacyAndConfi

|

Responsiv

|

Safety

|

|

ReliabandConv Pearson Correlation Sig ( 2-tailed) N |

1 961 |

.634** 961 |

.618** 961 |

.523** 961 |

.556** 961 |

|

WebAesth Pearson Correlation Sig ( 2-tailed) N |

.634** 961 |

1 961 |

.632** 961 |

.515** 961 |

.490** 961 |

|

PrivacyandConf Pearson Correlation Sig ( 2-tailed) N |

.618** 961 |

.632** 961 |

1 961 |

.506** 961 |

.674** 961 |

|

Responsiveness Pearson Correlation Sig ( 2-tailed) N |

.523** 961 |

.515** 961 |

.506** 961 |

1 961 |

.371** 961 |

|

Safety Pearson Correlation Sig ( 2-tailed) N |

.556** 961 |

.490** 961 |

.674** 961 |

961 |

1 961 |

**correlation is significant at the 0.01 level(two tailed)

From the table no 9, correlation matrix we observe that all the dimensions exhibit significant positive correlation. It shows that the all dimensions are interrelated which effectively measure the E-service quality of banks. The dimensions Reliability, Website aesthetics, Privacy, Responsiveness and safety play impactful role collectively in measuring the E- service quality.

Analysis of relation between customer satisfaction and e- service quality attributes through regression analysis:

Regression is a well-known statistical technique to model the predictive relationship between several independent variables (DVs) and one dependent variable.*

The regression model is described as linear equation that follows. Y is the dependent variable, that is variable being predicted. X is independent variable or the predictor variable. There could be many predictor variable and only one dependent variable in the regression equation.

To understand the relationship between the overall customer satisfaction of e-banking and the identified dimensions, regression analysis is used. Here, overall customer satisfaction of e-banking as perceived by the customers is treated as dependents variable (Y) and the five identified service quality dimensions are treated as independent variables(Xi, i=1,2,3,4,5)respectively.

The regression model in the given case will be-

Y=b0+b1X1+b2X2+b3X3+b4X4+b5X 5 (1)

Where Y denotes the dependent variable (Overall service quality), X i, i=1,2,3,4,5 denotes the independent variables (Reliability and Convenience;Website Aesthetics; Privacy; Responsiveness and Safety respectively), b0 denotes the intercept and b1…b 5

denote the coefficients that represent the estimated change in mean value of dependent variable for each unit change in the values of the independent variable.

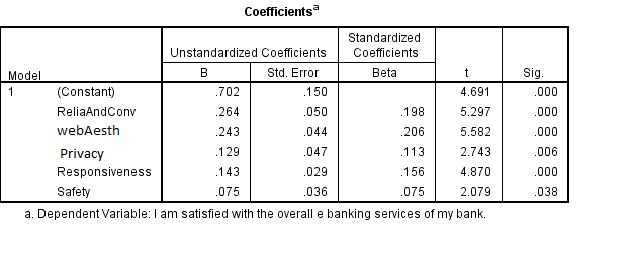

Table 10: Coefficients table

From, above Table the regression model for the given data would be,

Y= 0.702+0.264X1+0.243X2+0.129 X3+0.143X 4 + 0.075X5

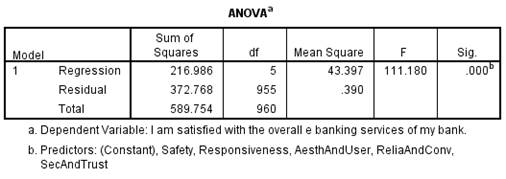

Table 11: Anova

From Table 11, we observe that all the service quality dimensions are statistically significant as the p-values are significantly small and also from Table 8 we observe that the regression model is statistically significant. This means that overall customer satisfaction can be predicted based on the identified e-service quality dimensions. Hence the relationship between Overall customer satisfaction and identified e-service dimension is established.

With the increasing internet banking penetration in India it is important for the banks to analyse the E-service quality provided by them. It is important to identify the factors which measure the E-services of banks. The purpose of the paper is to explore the significant E-service dimensions which can measure the customer services effectively. The factor analyses explored the five dimensions named as Reliability and Convenience, Website Aesthetics, Privacy and Confidentiality; Responsiveness and Safety. The correlation analyses on the emerged factors found significant. Safety dimension is ranked no.1 in providing quality to customers and is influential dimension. The regression analyses proved the role of E- service quality dimensions play important role in determining overall customer satisfaction. The Reliability & convenience dimension and Website Aesthetics are contributing towards customer satisfaction as B-value is higher than the Safety and Responsiveness and privacy dimensions. The improvement areas identified are Privacy and Responsiveness.

1. Anil Maheshwari, Data Analytics ,Mc Graw Hill Education (India) Private Limited ISBN-13: 978-93-5260-418-0

2. B. Yoo, and N. Donthu, (2001), “Developing a scale to measure perceived quality of an internet shopping site SITEQUAL”, Quarterly journal of electronic commerce, vol 2, No 1, pp.31-46.

3. Joseph M, McClure C, Joseph B (1999) Service Quality in Banking Sector: The Impact of Technology on Service Delivery. International Journal of Bank Marketing 17: 182-191. 19.

4. Jayawardhena, C. (2004), “Measurement of Service Quality in Internet Banking: The Development of an Instrument”, Journal of Marketing Management, Vol. 20, No. 1/2, pp.185-207.

5. Jun, M. and Cai, S. (2001), “The key determinants of Internet banking service quality: a content analysis”, International Journal of bank Marketing, Vol. 19, No. 7, pp.276-291

6. Khan, M. S., Mahapatra, S. S. and Sreekumar (2009), “Service quality evaluation in Internet banking: an empirical study in India”, International Journal of Indian Culture and Business Management, Vol. 2, No. 1, pp.30-46.

7. Liu. C and Arnett, K.P,(2000), “Exploring the factors associated with web site success in the context of electronic commerce” , Information & Management , Vol 38, pp23-34

8. Mathew Joseph, Cindy McClure and Beatriz Joseph Service quality in the banking sector: the impact of technology on service delivery International Journal of Bank Marketing 17/4 [1999] 182±191

9. M.F. Wolfinger, and M.C. Gilly(2002)”.comQ: Dimensionalizing, Measuring and predicting quality of the e-tailing experience”, Working paper, Marketing Science Institute, Cambridge MA, pp-183-198.

10. Parasuraman, A., Zeithaml, V. and Berry, L. (1988), ``SERVQUAL: a multiple-item scale for measuring consumer perceptions of service quality'', Journal of Retailing, Vol. 64, Spring, pp. 12-40.

11. Robert Johnston “The determinants of service quality: satisfiers and dissatisfiers “, International Journal of Service Industry Management, Vol. 6 No. 5, 1995, pp. 53-71. © MCB University Press, 0956-4233

12. Siu, N. Y. M. and Mou, J. C. W., (2005), “Measuring service quality in Internet banking: The case of Hong Kong”, Journal of International Consumer Marketing, Volume 17, No. 4, pp.99 - 116.

13. Valarie A. Zeithml, “Service quality Delivery Through Websites: A Critical Review of Extant Knowledge”,Journal of the Academy of Marketing Science, Volume 30, No 4, Pg- 362-375

14. Wong DH, Rexha N, Phau I (2008) Reexamining Traditional Service Quality in an E-banking Era. International Journal of Bank Marketing 26: 526-545

15. Z. Yang, R. T. Peterson, and S. Cai, ( 2003), “ Service quality dimensions of Internet Retailing: An exploratory analysis”, Journal of Services marketing, Vol. 17, No 7, pp. 685-701

16. Zhilin Yang, Shaohan Cai, Zheng Zhou, Nan Zhou, “Development and validation of an instrument to measure user perceived service quality of information presenting web portals”, Journal of Information & Management 42, 2005, pg- 575-589.