|

Dr. Muhammad Ishtiaq Assistant Professor Lyallpur Business School, Government College University Faisalabad |

Aisha Imtiaz Assistant Professor, Department of Business Administration, Government College Women University Faisalabad. |

Ahmad Mohmad Albassami University Putra Malaysia (UPM) |

Shahbaz Hussain College of Commerce, Government College University Faisalabad |

In this study we examine the impact of financial self-efficacy on the financial behavior of the working women, along with the different personal attitudes including financial anxiety, self-esteem, self-control and financial stress. Impacts of the financial literacy and risk preferences on the financial behavior also examined in this study. Data has been collected from the working women in public sectors banks. For collecting the data we used the questionnaire survey method and collect responses from the 300 participants. Data has analysed through the different statistical technique including, descriptive statistics, correlation and OLS regression analysis. We find that self-esteem, selfcontrol, risk preferences has the significant impact on the financial behavior of the women. While self-efficacy and financial literacy has ambiguous results in our study we find no relation with financial behavior. Financial stress and financial anxiety also have no significant relationship with financial behavior of the working women in public sector banks.

Key words: Financial self-efficacy, Financial Behavior, Financial Literacy, Risk preferences, working women and Public sector banksPsychological factors have the great impact on the financial decisions of an individual, it is highly acknowledged and recognized by the consumer educators that only financial education cannot helps to improve the capability to deal with all financial products (Schuchardtet al., 2009). Behavioral economists have explained that only education and information of financial products are not enough for induced change in Behavior. Mostly it is agreed that financial education and financial skills helps to understand and deal with the financial matters but there are some other factors also influence one's personal financial management that includes 'emotional control' of a person, assuredness level of their 'decision making' and consumers 'financial capabilities' to deal with financial products (Atkinson and Messy, 2011) .Financial concepts understanding and self-efficacy is important to determine how well people manage their money and response to their financial obstacles. Person possessing these abilities can make more competent and rational actions, they have the positive control over their financial It is widely excepted truth that consumers has behavioral biases and also lack of self-control that cannot be addressed only by financial education. One of the major factor that influence the consumer's behavior is the 'self-efficacy (Hira, 2010). Self-efficacy refers to the sense of individual's self-agency and believe that a person can accomplish the task successfully and it is related to the optimism, motivation and self-confidence and believe that one can cope with the variety of challenges (Gecas, 1989). Self-efficacy can be observed through many elements of individual behavior, that how they perceive about their future, are they optimistic or pessimistic (Bandura, 2006). High self-efficacy motivates a person to achieve their goals with the positive approach, due to this a person can handle the obstacles easily to fulfill its desired goals rather than the low self-efficacy become the reason to focus on potential losses. Need of psychometric scale in terms of personal financial management comes from NEFE Quarter Century project which gathered the experts of financial literacy to review the 25 years of study on financial literacy and give the future directions. Attitudes of persons and personal beliefs understanding are the main competencies for financial well-being (Hira, 2010). Financial behavior of individual influenced by large numbers of internal factors including personality, individual's cogitation and psychology, environment and family history. Financial self-efficacy developments helps the professionals and educators helps consumers to identify the barriers and pathways give pathways for productive financial management (Xiao et al., 2001).Importance of behavioral factors has been increasing due to its influence on financial actions and decisions (Gilovich et al., 2002; Montier, 2007; Thaler and Sunstein, 2008). In financial literacy measures women consistently scores less than men and this gender-based gap impacts negatively on the financial well-being of women (Fonseca et al., 2012). For example financial literacy has been nodded with the number of crucial outcomes, such as participation in stock market, accumulation of wealth and planning for retirement. Lower levels of financial literacy among women impeding their abilities to manage and accumulate assets, and a planned financial future (Stango and Zinman 2009; Yoong, 2010). Women face more challenges than men because they have less knowledge about debt. Due to less literacy about debt, women engage in high interest rate debts and high-cost borrowing. Women above age of 60 have costly credit cards as compare to men, such as, late payments of fee and have balance in credit card (Allgood Investors shows the different behavioral biases such as Overconfidence, Disposition effect, Herding and Home Bias (Kahneman and Taversky, 1979; Kumar and Goyal, following the large to make their investments and some of them believe on their previous experiences to protect their investments (Lee et al.,2004). Home bias is that in which people don't invest in socks and foreign markets that because of lack of knowledge, interest and transaction cost. Individual's attitudes towards risk an important factor towards financial decision making behavior. In contrast with men, women's have less ability to tolerate risk so they do not make investment in risky products. They are more towards the saving accounts and secure future financial planning, due to this behavior they face poverty in their young age and have no sufficient accumulation of wealth for their retirement (Jianakoplos and Beasek 1998) researchers that in which way individuals manage their personal finances and which factor contributing in financial dissatisfaction and financial stress. People who do not take financial recommendations and advices from experts mostly dip into financial stress (Lea, Webley and Walker 1995). Financial knowledge and self-esteem has impact on the personal financial management and as well as self-esteem has association with the financial behavior of individuals. Researchers have find the positive relationship between high self-esteem and good financial behavior and abilities of an individual to manage their personal finances effectively. While lower self-esteem dips individuals in financial stress and anxiety that may lead to poor financial behavior and undesirable outcomes (Yurchisin and Johnson 2004; Asaad 2015). In examined the personal finance behavior of individuals, there is more scope of economic models that tends to fully incorporate in the psychometric instruments such as individuals sense of control over and confidence in their personal financial management. That helps to create the more accurate pictures of the factors that positively or negatively contributes in financial outcomes of individuals. There is need of more studies to encompass the personal financial behavior of individual through the psychometric theories (Xiao, 2008). 2012). For example financial literacy has been nodded with the number of crucial outcomes, such as participation in stock market, accumulation of wealth and planning for retirement. Lower levels of financial literacy among women impeding their abilities to manage and accumulate assets, and a planned financial future (Stango and Zinman 2009; Yoong, 2010). Women face more challenges than men because they have less knowledge about debt. Due to less literacy about debt, women engage in high interest rate debts and high-cost borrowing. Women above age of 60 have costly credit cards as compare to men, such as, late payments of fee and have balance in credit card (Allgood

The aim of the study is to examine the relationship between financial self-efficacy and women personal finance behavior of working women in banking sector. For this purpose, study includes the following objectives: To identify and understand the relationship between financial self-efficacy and financial behavior of women. To examine the impact of self-esteem on the financial behavior of working women. To access the significance of financial literacy on the personal financial behavior. To investigate the impact of financial stress on the financial behavior with in the female banking staff. To identify the importance of risk-preferences on the women personal financial behavior. To examine the relationship between the financial stress and the financial behavior of working women. To determine the relationship between the financial behavior and Individual financial products.

The individual financial Self-efficacy is an important factor in explaining one's personal financial behavior. Different psychometric instruments such as financial self- efficacy, self-esteem, self-control financial stress and financial anxiety in this regard provide clearer picture of individuals' sense of confidence, capacities and control towards personal financial management and how financial literacy helps to induce change in behavior regarding selection of financial products. It is valuable to explore all these attributes in female bankers working in Public sector banks (Lusardi and Mitchell, 2010; Lown, 2011; Farrell, Fry and Risse, 2016).

Importance of outcomes of behavioral research in understanding of societal issues and giving recommendations of public policy is necessary and evident. Study of financial self-efficacy is crucial for the understanding that why some people are successfully managing their personal finances while the others are not even in the same economic circumstances and demographics. There is the obvious need for the measure of self-efficacy scale for use by the educators, consumer researchers, advisors and counselors and also for the individuals to understand their behavior towards the financial products. Consumer researchers and educators revealed that there is more need to pay attentions towards the physiological factors of individual behaviors to deal with the financial decisions based on their financial capacities. Current study focused on significance of financial self-efficacy to explain the personal financial behavior of woman's and the financial behavior of the women influenced by their risk preferences, level of self-esteem, self-control, financial stress and financial anxiety. This study reveals the self- efficacy and personal finance behavior of woman's in Pakistan, specially pays attention to the type of financial products holds by consumers and how well they manage their personal finance. Also determine that how much responsible and forward thinking are individuals towards financial future (Lusardi and Mitchell, 2010; Lown, 2011; Fernandes, Lynch and Netemeyer 2014; Farrell, Fry and Risse, 2016). In this study we focused on the significance of financial self-efficacy in explaining the women personal finance behavior (Farrell, Fry and Risse, 2016) of working women in banking sector. In this study the data collected from women working in Public sector banks. Also focused on the other variables that play important role in individual's financial behavior such as financial literacy, financial stress, financial anxiety, self-esteem, self-control, risk personal abilities of an individual to manage their finances and power of making financial decisions it cannot be ignorable that individuals with the higher self-efficacy have the assuredness about their financial future and are more able to encounter the challenges rather than avoids due to threats (Bandura, 1994). These kind of attitudes results in ones goals accomplishments and favorable financial outcomes. Mohamad (2010) presented in his study the comparison of gender and working sector with panning of personal financial, because personal financial management helps to face less financial difficulties . In this study he examined the difference between working sector and gender with regard to personal financial management, attitude to financial planning and financial literacy. To measure personal financial management he included five items under this credit management, insurance planning, retirement planning, saving planning and investment planning. For collecting the data used questionnaire survey, which rotated among the public and private sectors staff of This study also focus on the financial anxiety and stress levels which may impact on the financial behavior of the women (Heckman, Lim and Montalto 2014). There is also an important variable which impacts the financial behaviour of i8ndividuals is self-control, in this study we also aces the relationship between the self-control level and financial behavio0r of the individuals (Limerick and Peltier, 2014).

Psychologists recognized that there are some internal beliefs and external variables that influence individual's behavior. In order to have the ability to understand the financial beliefs and financial self-efficacy of consumers can helps the educators and counselors to give individuals the best directions regarding the financial decisions that would not only be beneficial for their own self's but also for economy too.

Financial self-efficacy is related to beliefs of people on Household financial decisions are also related with their capabilities to control over functions and events that subjective expectations. could affect their lives. Behavior of people, motivation, and how they feel also determined by the level of self-efficacy. (Bandura, 1994). People who develop their skills, competencies and beliefs in personal efficacy have array of choices that expand their actions freedom and successful in future which they desired rather than those who have less self-beliefs (Schunk and Zimmerman, 1994).If we apply the concept of self-efficacy in order to know about the Mostly it is agreed that financial education rational actions, they have the positive control over their financial future, therefore they can achieve favorable future outcomes (Guo, et al., 2013).

Farrell, Fry and Risse (2016) analyzed personal finance behavior of women and significance of financial selfefficacy. By using the survey of 2013 Australian women, they concluded that self-efficacy plays important role in what kind of financial products women used to hold. Financial self-self-efficacy related to level of assuredness, financial capabilities and one's decision making power of investments and financial management. They concluded that women with the higher self-efficacy used to invest in riskier products as compare to risk free saving plans. Self- efficacy in women also related with their level of financial knowledge, capabilities, age, household income and risk preferences. Danes and Haberman (2007) investigated the relationship between financial self-efficacy, financial behavior and financial knowledge. They collected data from male and females (n=5329) through the questionnaire survey rotating in school. They concluded that gained greater knowledge about investments, insurance and on credit as compare to males, and males have already had knowledge before entering thin the finance course. Managing money affects the future indicated by females, and males were more confident regarding their money decisions rather than females. Study revealed that male's goals achieving ability is more than female and they discuss less about financial matters with families as compare to females. Females were more interest to get knowledge about which they are unfamiliar and male reinforces existing knowledge. Shim, Serido and Tang (2012) examined the impact of saving behavior and future oriented financial behaviors on the young adult's well-being. For this study they used the two times longitudinal data, which collected from before and during financial crises. They tested the psychological process model. Efficient Market Hypothesis shows that the investors behave rationally in the financial markets. In financial markets investors have to choose the best alternative in the world full of uncertainties, while the expected utility theory (EUT) describes that the investors are rational but they make the decision by choosing the best among all alternative on the basis of associated risk and their utilities, make decisions with good balance study of private health insurance market described the negative behavior for private health insurance. An analysis of individual indicated that lower financial risk takers dropped insurance due to increase in premiums. Financial risk taking behavior of an individual also linked with the price of product, benefits and cost associated with product. Mostlly risk averse people resist to purchase the health insurance because they think that benefit of product is less then cost in comparison and also dropped due to no or lower returns (Knox et al., 2007).

Montford and Goldsmith (2015) analyzed that how the self-efficacy and gender influence the risk taking behavior on investments. Most of the studies shows that in US people have less amount of money left in their retirement age, especially women make investments very rarely. According to an estimate women live longer than the men so they believe on the accumulated saving rather than the riskier investments. For this study they collected the data from the US students (n=182). They concluded that the women take less risk while making investments and financial self-efficacy positively linked with the gender and risk taking behavior of the individuals. Sung and Hanna (1996), examined the effect of demographic and financial variables on the level of risk tolerance, which they estimated for the household, they used the Survey of Consumer Finances in 1992 and collected the data from employed individuals. Results of logistic regression analysis showed that female head of household is tolerate less risk than the men or married couple. Sunden and Surrrette (1998) also concluded that single women's do not invest in riskier investments because they tolerates less risk as compare to men. Women found more risk averse then the men while examining the gender differences in contribution of pension allocations and women are conservative in taking advice regarding financial matter than men (Bejtelsmit and Bernasek 1996; Bejtelsmit, Bernasek and Jianakopolos 1996). Women are most likely to hold the certificates of deposits while the men are more interested to hold the stocks, it also shows the risk taking behavior of men and (Kahneman and Tversky, 1979). Efficient markets women, their belief on efficacy (Xiao, 1995).Saving challenged by behavioral finance, to know that why behavior of men and women are different on the basis of investors behave in the particular manner while investing their investment approaches and level of risk tolerance. in assets. Kahneman and Tversky, 1979 introduced the Fisher et. al (2010) investigated the saving behaviors by Prospect theory as an alternative of EUT for explaining the using the Survey of Consumer Finance (SCF) 2007, he decision making strategies of investors under collected the data from women (n=702) and men (n=469). He concluded that the poor health affects the short term Household Survey (DHS)1 2005. They concluded that lack investments of women negatively but do not impacts on the of financial knowledge has the significant impact on the short term investments men and also low risk tolerance stock ownership and it also prevents the households from negatively affect the women's savings. So understanding participating in stock market. the investment behaviors of both can help the educators and financial professionals. Lusardi, Mitchell and Cutto (2010) presented the financial literacy levels of the youth by using National Longitudinal In the study of Jianakoplos and Bemasek (1996) survey Survey 1977. They showed, only 27% young adults have revealed that evidence about self-reported level of risk the basis knowledge of inflation, interest rate and risk tolerance that women recognize themselves less inclined diversification. They also mentioned that the high school towards risk taking. For their study they collected the data boys whose parents are educated and known to some stock from single and married women, from the given four market knowledge have better capability to manage statements in the survey regarding risk-return tradeoff 57% finance and risk diversification as compare to those high married and 63% single women stated that they are not school girls whose parents are not educated. So that the ready to take any financial risk in the comparison of 41% of factor like socio-demographic variables in the way that married men and 43% of single men in the sample. high education, wealth and higher age related to the better Confidence of achieving positive investment outcomes also related with the acceptance and tolerance of financial risk but only at the possibility of investment returns due to unrealistic expectations of return and excessive trading financial literacy. But some of the studies has found that there is no significant effect of the financial literacy on financial behaviour (Fernandes, Lynch Jr, and Netemeyer, 2014). (Looney et al., 2006). Participation on individuals in risky Shim et.al (2010) studied the First-Year college students financial products may lead to the greater wealth creation, financial socialization and role played by education, work trading of assets frequently leads to maximize the and parents. They conducted the survey in which 2098 transaction cost, wealth erosion and low appreciation of students participated. They concluded that parents has the portfolios (Baber and Ordean, 2000). greater influence on the children financial socialization Garcia and Teesada (2013) analyzed impact of education on participating in financial markets. They gathered the quantitative data from 1985 to 2011 by using the CASEN survey 2009. He concluded that High school increases the probability of participating in financial markets by 3%. Lower education attainments also decrease the participation level in financial markets. High school other than school and work place. Kim, Yang and Lee (2015) investigated that which parental style influence the children consumer socialization for that they collected the data by questionnaire that was distributed among the parents of high school students in East Canada. They concluded that the mother practices and parental style more influence the children instead of father practices. education is also provide some evidence of house hold Agarwalla et al.,(2015) investigated about the financial having health insurance and risk aversion. There is another literacy in the young working generation of India. They factor described by (Zimmerman et al., 1992) that found that working people have low financial knowledge individuals with the higher self-efficacy are tends towards and inferior attitude especially women's have very minute more confident regarding their investments. They invest in information regarding the financial products and unfamiliar, higher yielding and riskier assets for consultative financial decision making with family has the consistency and patience in investment behavior. positive impact rather than joint family system has the

Financial Literacy is the ability of individuals and households to manage their finance efficiently. It becomes very important now-a-days to have the ability of managing personal finance. People have to plan for short-term as well as long-term to manage their finance for children education, marriage, and retirement. Rooji, Lusardi and Alessie (2011) devised two modules for the De Nederlandsche Bank (DNB) to measure the study its association with the stock market and financial literacy. They collected the data from De Netherlandsche Bank

and inferior attitude especially women's have very minute information regarding the financial products and consultative financial decision making with family has the positive impact rather than joint family system has the negative effect on the financial literacy. They also recommended that with the financial literacy there is also equal importance of the financial knowledge among the working individual is also important so the government should include the financial education related courses and conduct the financial education related programs and seminars for the working persons. Prete (2013) examined the relationship among the economic literacy, financial development and inequality in income levels. They concluded that higher level of economic literacy impact passively the income equalities but financial development is negatively correlated with the income inequalities. While the financial development in the country is depend on the level of economic literacy.

Andrews and Willding (2004) conducted the study to explain the association between the financial stress, financial anxiety and depression. He collected the data from the 351undergraduated UK-domicile students and conducted survey before entry and mid of university. They concluded that financial stress and other difficulties increase the financial depression and financial anxiety among the students, it effects on their academic performance negatively. Students of another British university found that financial stress is reason for poor mental health conditions in students. Financial stressors like they unable to pay their utility bills on time due to financial barriers (Robert et al., 1999).Engelberg (2007) analysed the impact of self-efficacy perceptions in term of coping economic risks. They included money attitudes variables, emotional management such as negative emotions and stress arises from demands to control economic aspects of life. Link between these variables and self-efficacy were examined through the survey questionnaire filled by 120 respondents. Finds reveals that there is positive relationship between self-control, emotions and financial self-efficacy. They successfully determined the discrimination between high and low-self- efficacy. Future more the results revealed self-perception and self-control linked with self-efficacy which helps to deal with economic changes. Beenakers et al., (2016) studied self-control and financial strains role in terms of explaining behaviours and income inequalities. Risk of bearing financial strains become increase due to the lower income and this situation leads to less self-control and extensive unhealthy behaviour. They used the cross-sectional data survey in their studies, data obtained from participants (25-75 years old). They examined the association between self-control, healthy behaviour, income and financial strain. Data analysed by generalized linear models and linear regression. They concluded that the unhealthy behaviour associated with low self-control and financial strains. Self-control is linked with unhealthy behaviour and financial strains. Romal and Kaplan (1995) conducted study to know about that psychological variables impacts on saving behaviour of individuals. By a survey questionnaire he collected data from 98 member of credit union (aged 20-61 years), less self-control and also suggested that there is more need to understand the psychological factors that directly impacts on saving behaviour of individuals Perry and Morris (2005) study indicated that financial resources, financial knowledge and perceived control of consumers prosperity to save and budget finances. Ethnicity and race revealed the mix results as moderator. Gathergood, (2012) identified relationship between financial literacy, over indebtness and self-control on UK consumers of credit. Lack of financial knowledge and selfcontrol are significantly related with the non-payments of debt and consumers financial burdens of debt. Consumers of with less self-control make extensive use of high-cost credit due to quick access such as payday loans and store cards. Self-control problems owing consumers suffers from unusual withdrawals, unforeseen expanses and frequent income shocks. Varity of risk regarding financial management also increase with decrease in self-control. Self-control and financial literacy association with the over-indebtedness of credit debt. Self-control lapses impacts the debt of credit card as well as due to this debt consumer's leads to more self-control lapses and life stress. Peltier, Dahl and Schibrowsky (2016) developed a model and tested pre-/post-debit decisions of college students, how it impact on self-control and how failure of pre and post debt decision affects the financial anxiety. They concluded that the debit decisions have great impacts on self-control and financial anxiety, it is better to understand time-order mechanism of self-control. It could happen through the financial literacy and by making useful interventions for self-control lapses before decision making process. Debt loads and financial worries affects the wellness of students negatively, factor associated with financial stress among the students explored by using Roy Adoption Model, which used in application of health care. Heckman, Lim and Montalto (2014) conducted Financial Wellness Survey which was analysed in 2010 by Ohio students. Used the proportion test and multivariate logistic regression. Results of analysis showed that 71% of the students under the financial stress due to personal finances. The results multivariate logistic regression and proportion test also described that study is also a reason of financial stress among students. There are two main stressors among the from 98 member of credit union (aged 20-61 years), students was that they have no enough money to participate questionnaire assessing the respondents financial in the activities in which their peers do and the other reason characteristics and demographics. They analysed the is that student have debt burden. Results of survey also influence of, self-control, locus of control, age, sex, marital indicated that students with the higher self-efficacy have status and rent their own home affects the saving or not. low level of financial stress. There are two main basic They concluded that people with higher self-control concepts linked with the financial stress one is optimism manage their money more efficiently else than who have and other is self-efficacy. Perceived self-efficacy 202 Paula and Cambell (2002) conducted two studies about self-esteem, rumination and persistence in the failures face. In the first study they manipulated about the availability of alternatives and degree of failure. Students with the higher self-efficacy (HSE) persisted more than the lower selfefficacy (LSE) students when the alternatives was available after a failure. There was no difference in persistency when there was no alternative available, while the LSE was more ruminated as compare to HSE students. In their second study they studied the rumination and persistency among the students on the basis of 10 goal achievements in one year. Students with HSE was dominant in their performances, goal achievements and have high grade points in academics and have lower rumination. While students with LSE have high rumination level. So HSE students were more effective in goal directed behaviour and self-regulation.

(Bandura, 1993) is an individual ability to handle different situations efficiently, for this social, component cognitive and behavioural skills required for actions. Locus of control and mastery associated with self-efficacy. So person with higher level of self-efficacy have lower level of financial stress and he can achieve the desired outcomes (Bandura, 1977; Bandura 1982). Limerick and Peltier (2014) analysed the self-control behaviours in term of psychological, social constructs and behavioural and checked their impact on the usage of credit card debt among college students. Antecedent variables included locus of control (psychological), failure of debt management (psycho-Behavioral), impulsivity, anxiety (psychological) and status (social) are also examined. Credit card debt increases due to financial anxiety and poor financial management is associated with self-control failure. Excessive debts and status oriented society have negative impacts on self-control.

Owens (1993) described the negative and positive ranking of self-depression, self-esteem and self-confidence. They argued that recent developments in the positive-striving

theory and self-verification in association with self-esteem, enhance the knowledge of social scientist, so they can make the positive and negative use of global self-esteem. They used longitudinal youth in transition data for analysis. They developed the two models for self-esteem unidimensional and dimensional, these models showed self-esteem is dimensional construct of self-confidence and self- depression. Implications of study indicated to understand the positive and negative impacts of social well-being and self-evaluation.

Financial behaviour of individuals not only depend on study has the positive attitude towards the Quantitative methods and Qualitative methods. This study used the Quantitative techniques which give the insights and reviews of qualitative study. In this study financial behaviour of the working women is studied, because bank staff has the financial knowledge, there are opportunities and guidelines regarding the financial products are available. Either in this case women financial behaviour is positive or negative or financial self-efficacy impacts on

In this study we adopts the quantitative method to provide financial knowledge, there is also need of positive evaluation to deal with finances and persistency while making decisions. Tang and Baker (2016) checked the impact of self-esteem on financial behaviour directly as well as indirectly through subjective financial knowledge, they also distinguished between the subjective knowledge and objective knowledge. They collected the data from the US national results of the study indicated that individual financial behaviour is significantly impacted by selfesteem after controlling socio demographic variables and financial knowledge. Association between financial behaviour and self-esteem could be direct and indirect with the subjective knowledge. Findings of study also highlighted that financial behaviour also vary due to psychological trails like self-esteem.

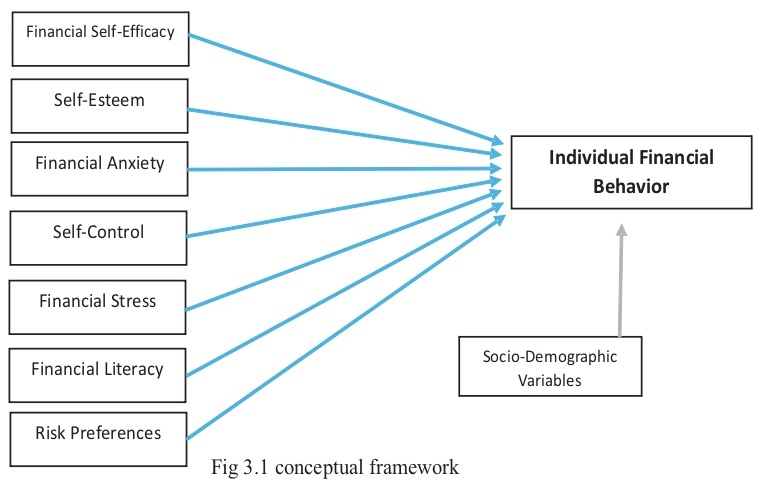

By considering research questions regarding current study, this research use the pragmatic philosophical position, which indicate that there are many ways to interpret and undertaking research because there are multiple realities of the world and single point cannot give the clear picture. The main goal of this research is identify the impact of financial self-efficacy (FSE) on the personal financial behaviour of the working women in the banking sector of Pakistan. This study also gives the deeper ideas about how the financial literacy effects on financial behaviour of women regarding the financial products, either the women are risk takers or the risk averse. Financial behaviour of the women in this study also indicated by their personal factors such as self- esteem, self-control, financial anxiety and financial stress.

This research is viewed as the 'holistic endeavour', this ir behaviour (Onwuebuize and Leech, 2005). This study used the approach of deductive reasoning for the empirical findings. The research mechanism of this study start with the review of the literature regarding the variables. On the basis of contextual understanding of the background hypothesis has been generated. Primary data has been collected to prove the hypothesis. Collected data is used in this study statistically to confirm the rejection or acceptance of hypothesis to modify and prove the theory. There are only five public sector banks in the Pakistan the comprehensive results of our study and to answer the questions of this research and also to meet objectives of the study. Research design of the study refer to the detailed plan about the data collections of the study and analysis that depends on the research question of the study (Sekaran and Bougie, 2013). In this study we use the survey design for the study, this data is collected for the more than one case in the single point. The collected data is examined quantitatively to analyse patterns of association in the independent variables and dependent variables (Sekaran and Bougie, 2013). Current study has undertaken the cross-sectional method for the research purpose and collected the data once during the whole research course. The Longitudinal study was not undertaken because it was not required for this study, or rather it might be difficult due to the limited time.

The population is refers to universe of units, from which researchers select the targeted sample (Brayman and Bell, 2011). (Robson, 2011) population study may be the literal population such as the people, regions, cities, firms and many others. The population of this study contain the female working staff of the public sector banks. Public sectors banks are state owned banks, government holds 50% or more of the share of public sectors banks. which includes the, First Women bank ltd (42 branches), National Bank of Pakistan (1451 branches), Bank of Punjab (450 branches), Sindh Bank (260) and Bank of Khyber (157 branches). The technique of satisfied random sampling for used for the targeted sample that is arranged in the systematic way and also represents the certain proportion of working women in banks such as the Public sector banks.

Primary data collection is known as the first hand data collected by the researcher. Researcher collects the primary data, when data for the variable is inappropriate or unavailable or secondary data is not sufficient for the research criteria (Sekaran and Bougie 2013). Primary data can be collected from the various ways such as from interviews, questionnaire survey and observations (Bryman and bell 2011). This study used the questionnaire method for the data collection. Self-completed (self- administrated) questionnaires are completed and answered directly by the participants of the study (Bryman and Bell, 2011). In this researcher personally deliver and collect the questionnaire from the participants (Bryman and Bell, 2011).In this research used the self-delivery and self- staus collection method.

Question items used in this study has also been taken from the existing literature by considering the above points in the view (Tangney, Baumeister and Boon, 2004; Behrman et

population (Bryman and Bell, 2011). Current research has conducted pilot study for the findings and also for consideration of questionnaire.

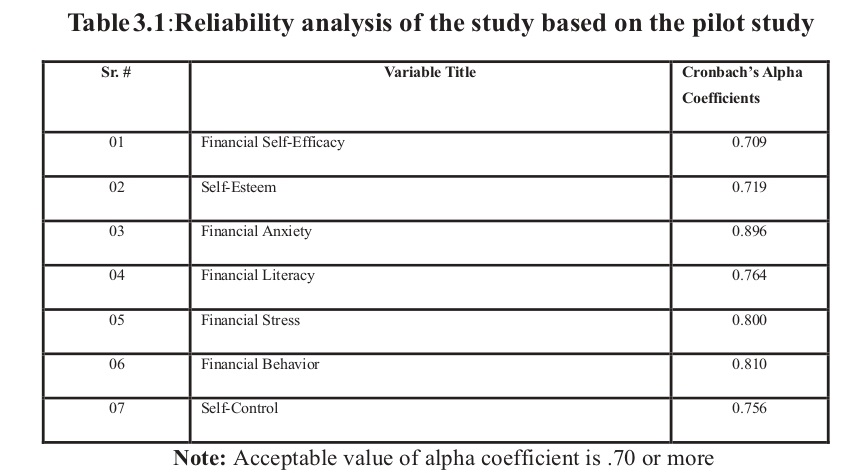

al.,2010; Archuleta, Dale, and Spann, 2013; Fernandes, Lynch and Niemeyer 2014; West and Worthington, 2014;Farrel, Fry and Risse, 2016).The questionnaire used in study is basically comprised on the three section (appendix). This is evident to conduct a piloting (testing or pilot study) before using the instrument with the targeted sample or To check the reliability and effectiveness of items used in the questionnaire there is the most common statistical test known as the Cronbach's Alpha test, it is adopts to test the reliability and validity of all measures used in instrument (Selltiz, Wrightsman and Cook, 1976).The acceptable level of the coefficient is 0.7 and above (Nunnally, 1978). Additionally, this study also undertaken the correlation analysis for determining the relationship between the variables. The results of reliability analysis are reported in the Table 3.4.The results of the pilot study indicated the validity and reliability of the questionnaire. The coefficient value of all the key variables is above coefficient 0.7. Based on the outcomes of the pilot study, this research developed more confidence in questionnaire for gathering the data. Three hundred (300) working women at managerial posts in the banking sector has been randomly chosen for getting the responses from the five public sector banks of Pakistan. Current study has been decided to use the self-delivery and self-collection method to collect data of questionnaires

Note: Acceptable value of alpha coefficient is .70 or more The required data for the research has been collected from has situated in the major cities of Pakistan such as, the managers of banks working in the public sector banks, Faisalabad, Islamabad, Karachi and Lahore

For analysing the data of questionnaire different statistical techniques have been used. To describe the data of the questionnaire descriptive statistics has been applied. This study has applied the inferential statistical analysis to testify the hypothesis of the study. Statistical Package for Social Sciences (SPSS 20.0) has run to implement the different tools regarding the reliability, descriptive statistics, multicollinearity, Correlation and OLS regression analysis.

Descriptive statistics helps to attain the wider picture of the data and also supports to describe the data in the userfriendly and more orderly manner (Baily. 1987; Tabachnick and Fidell, 2007). Descriptive statistics also describes the measure of data central tendency (mean, mode and median) and dispersion measures such as range, variance and standard deviation (Groebner et al., 2005) . Most commonly two methods are used in the analysis of data for determine the basic feature, which includes both the means and standard deviation (Dancey and Reidy, 2004; Tabachnik and Fidell, 2007). In this study used the descriptive statistics to determine the values of mean and standard deviation for all the variables dependent and independent. For observing the average response mean value has been measure and for checking the variability standard deviation analysis has used.

Person Correlation This study used the person correlation for determine the association between the variables of used in this research, because the interval data is used in this research for this use the person correlation (r) (Tbachnick and Fidell, 2007). This study has interpret the correlation of variables on the basis of following citations which deduce the size of correlation coefficient of variables (Gujarati and Porter, 2009).

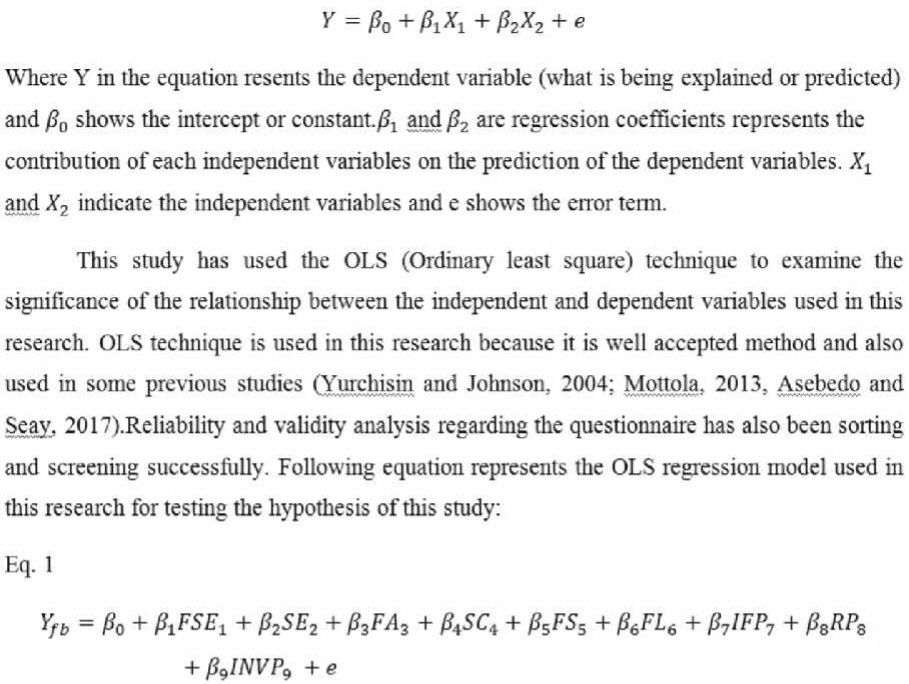

Regression analysis is used in the study to measure the relationship between the single dependent and several independent variables (Tabachnick and Fidell, 2007; Guajrati and porter 2009). In the multiple regression analysis following equation is formed:

In this study we used the questionnaire survey method for collecting the data from the targeted respondents. We collected the data from the working women in the public sector banks in Pakistan. Questionnaire items has adopted from the available literature on the dependent (financial behavior) and independent variables (FSE, self-esteem, self-control, financial anxiety, financial stress, financial literacy, risk preferences and financial products) used in this study (Danes and Haberman, 2007; Guttor, Copur and Garrison, 2009; Fernandes, Lynch and Netemeyer, 2014; Montford and Goldamith, 2015, Farrell, Fry, and Risse, 2016). Questionnaire used in this study was comprised of three section detailed analysis of each section is given below. This study used SPSS (20.0) to perform the following: Descriptive Analysis Correlation Regression Analysis

The results of descriptive statistics of each individual item of the variable. It is always a good idea to take a look at the descriptive statistics of the underlying variables. The number of observation for all questions n = 300. While this study reports mean and standard deviation for all items starting from financial behavior. In this study 18 items have been used to measure financial behavior, where the mean of items 1- 8 ranges between (3.40 – 3.09). Items 9 - 18 have relatively lower means within (1.67 - 2.49). However, the overall value of the mean is (2.5456), which shows a sign of healthy measurement of the variable. That value also indicates the positive financial behavior among sampled women in Pakistan.

The next variable of concern is financial self-efficacy, which is also measured by using a 5 point Likert scale (see appendix questionnaire for more detail). Financial self- efficacy scale utilized 6 items to assess whether the respondent has higher or lower level of financial self- efficacy. The average responses of this variable also remain encouraging as the average values move between (2.91- 3.68). On the measurement and statistical point of view this values correspond to a valid construct of this variable. This further strengthen the argument with an average value of the overall score (3.313) and standard deviation (0.7144). In this variable item 1 has the highest mean (3.68) that corresponds to the progress towards achieving financial goals.

In the first section of the questionnaire, used the demographic variables, through which collects the demographic data of the respondents. Demographic variables include the age, work experience, household income, mother's level of education, father's level of education and also include the other socio-demographic variables such as the parented, remoteness, nationality, language and depended children. Demographic variables used as the control variables in this study. Self-collection and delivery method is used to obtain the data from the 300 working women in the bank. The brief summary of demographic variables of the respondents. Age group of the respondents is between 18 to 60 years and majority (255) respondents has the age between 10 to 30 years. Majority respondents has the work experience up to 5 years. Household income of the working women is up to 40,000. While the mothers and fathers level of education of the respondents (majority) is also below than the 12 years. The other-socio demographic variables used in this study briefly. 57.3% of the women are parented out of the total responses and 41.7% and 54.3% women have no dependent children and also they have the remoteness. 71.3 % responses shows that they speak language other than Urdu at their home and 99% of the respondents are Pakistani born

order to measure self-esteem of the respondents this study incorporates a ten item indicator on a 5 point Likert scale. Average values of the items ranging (2.08 - 3.97). Item 1 comes out with the highest mean and lowest standard deviation (0.906). The overall mean of selfesteem is (3.304) with standard deviation of (0.528). This value also confirms the exceedance of mean value from the standard midpoint. The next variable of this study is selfcontrol which considers 10 items. It is also based on a 5point Likert scale, to determine the level of self-control of the respondents. All items show handsome value of the mean with a minimum value of (2.68) for item 1 and (3.66) for item 6. The corresponding standard deviation also ranges between 0.990 and 1.21. Furthermore, the overall mean value of self-control construct (3.04) with a standard deviation of (0.61). These values highlight the moderate level of self-control in the selected sample.

To measure the financial stress of the respondents takes 3 items. The average of each item is below a general midpoint 3 and ranges 2.72 – 2.81. The overall mean and standard deviation of this variable are (2.79) and (1.53) respectively. The lower value of the financial stress construct indicates lower levels of financial stress among the respondents and vice versa. Along the same line, financial anxiety has been measured on a five point Likert scale and consists of 7 items. The average of all these items remains below the value of 3 and lie between (2.31 – 2.95). The highest mean value corresponds to the anxiety about personal financial situation. That implies respondents are overly anxious about the financial situation. Mean of the 7 items is (2.792) with a standard deviation of (1.531). This also indicates the lower variation between the items of financial anxiety variable.

To approximate financial literacy of the respondents this study uses 13 questions following related literature in this domain. These questions have been widely used to assess an individual's level of financial market knowledge. These questions mainly intent to measure how well a respondent possess knowledge about inflation, interest rate, savings, and risk diversification. In addition, questions regarding retirement planning and financial planning are also part of this measure. This set of questions also includes information about long term investments and rate of returns on the different types of financial assets. Indicator of financial literacy has been constructed by the number of correct answers. First question of the financial literacy got reasonable response with (45%) correct answers, (note that only percentages of the correct answers reported here due to space constraints, however the detailed results can be obtained from the author). Risk diversification question came out to be a more frequent correct answer among the study sample with nearly (70%) answering it correctly. Around (42%) of the respondents could answer question three correctly while (64%) were able to answer question four correctly. Question five also shows encouraging response with (48%) of correct responses, while question six which is about investment in stock and mutual funds gets a response of (31%). Moreover, question seven about stock mutual fund is well known by the sample respondents with response of (64%). In contrast, question eight and that have been asked about retirement got relatively lower response of (38%), due to less awareness of retirement planning in Pakistan. Question ten assesses the financial planning of the

question thirteen about credit card payments was the least corrected question with a very low response rate of (5%). Financial literacy around the world is very low. Pakistan is a developing country; thus lower levels of financial literacy is not a strange finding. Even developed countries like USA report suboptimal financial literacy scores. In addition, retirement planning does not seem to be a proffered topic for Pakistani sample, as a few people are concerned about post retirement financial life due to joint family system or inheritance. However, empirical evidence reveals that financial literacy could improve the individual financial management and household financial well-being. Moreover, it could contribute to the overall financial stability of the country. Thus, financial literacy programs along with retirement planning courses should be organized to create the awareness of financial products and functioning of financial markets to improve household welfare, entrepreneurship development, financial stability and economic growth of the country.

This study also collects information regarding the use of financial products. Several financial products have been listed in an open ended question where survey respondents have been given the choice to select more than one financial product. The highest mean value (1.96) comes from the “Mortgage” followed by “Loan” (1.95). That indicates that the sampled respondents possess greater mortgage than any other financial products. Furthermore, the average value of the private health insurance is (1.86) followed by life insurance (1.72), these values show the averages of responses in favour of the possession of private and/or life insurance products. On the other hand, Investment, saving account and credit card average responses recorded as (1.71, 145, 1.72) respectively. The next variable of this study asked respondents about financial risk preferences. This indicator combines five items on self-reported risk preferences. Based on the data this study finds that majority of the respondents were reluctant to take risk either willingly or due to lack of sufficient funds. The average value of the respondents who answered that they had not spare cash that can be used to take risks is (3.74). While on average (2.89) responses were those who were not willing to take any financial risk.

Similarly, two questions were asked to determine the business ownership status of the respondents i.e., direct share ownership with two options (yes or no) and business ownership (yes, no). The latter leads the former with an average value of (1.24). It means that in the selected sample business ownership surpasses the direct share ownership.

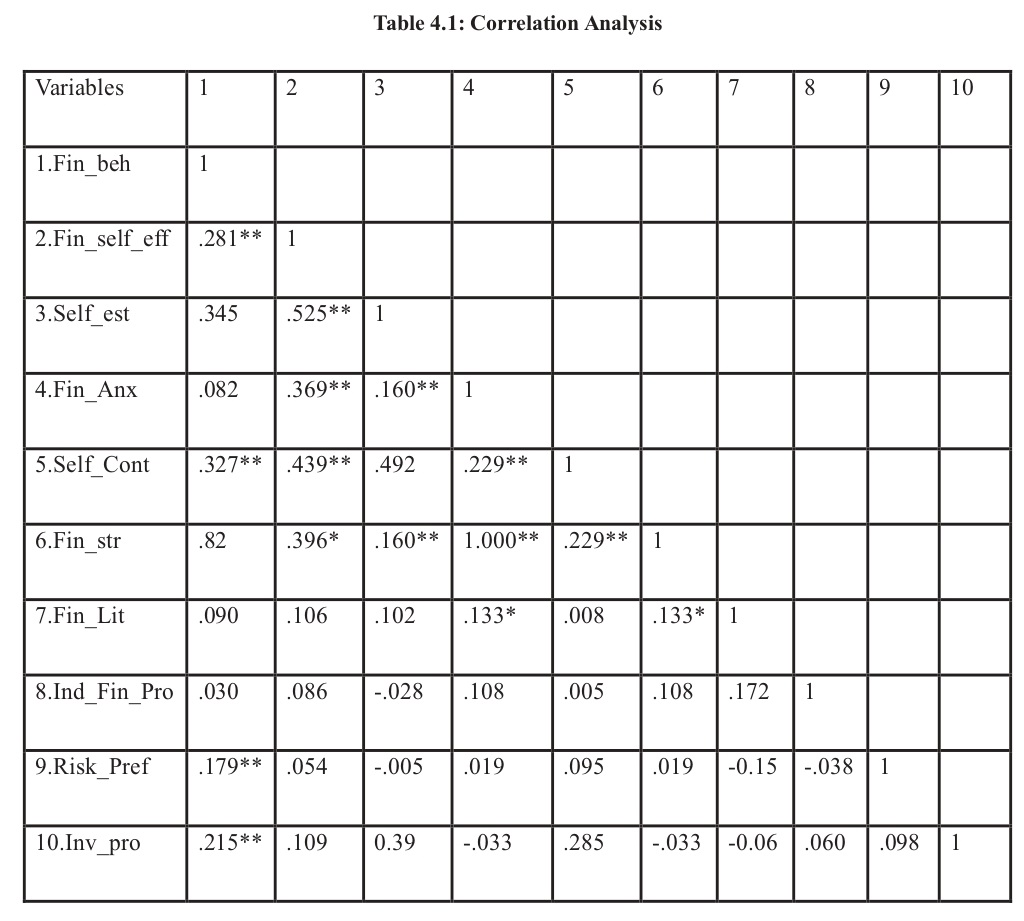

Correlation analysis used to determine the relationship among the variables. A key of all the variables is given in the table. In this research used the person correlation to analyse the relationship between variables.After descriptive statistics the next step of data analysis involves to investigate the association between underlying variables. Table 4.15 reports the correlation coefficients for all constructs used in the further analysis. It can be observed that financial self-efficacy is positively and responses. True false questions eleven and twelve barely got respondents which was able to get (45%) correct reasonable correct responses, around (28%) of the respondents could answer them correctly. Finally, the significantly related to the individual financial behavior. However, the value of the correlation coefficient (0.281) falls within the weak correlation regime. In addition, moderate positive correlation has been noted between financial behavior and individual self-esteem. The value of this relationship (0.345). Similarly, self-control (0.327), financial stress (0.82), risk preferences (0.17) and investment products (0.215) show positive correlation with financial behavior of the individuals. More detailed picture reveals that self-control has moderate positive relationship with the financial behavior, while financial stress found to have strong positive relationship with financial behavior. Whereas, risk preferences and investment products seem to have weak to moderate relation with financial behavior.

After descriptive statistics the next step of data analysis involves to investigate the association between underlying financial anxiety and financial stress is strongly positive and significant with the value of (1). This might be due to

variables. Table 4.1 reports the correlation coefficients for all constructs used in the further analysis. It can be observed that financial self-efficacy is positively and significantly related to the individual financial behavior. However, the value of the correlation coefficient (0.281) falls within the weak correlation regime. In addition, moderate positive correlation has been noted between financial behavior and individual self-esteem. The value of this relationship (0.345). Similarly, self-control (0.327), financial stress (0.82), risk preferences (0.17) and investment products (0.215) show positive correlation with financial behavior of the individuals. More detailed picture reveals that self-control has moderate positive relationship with the financial behavior, while financial stress found to have strong positive relationship with financial behavior. Whereas, risk preferences and investment products seem to have weak to moderate relation with financial behavior. Column 2 of the table reports the relationship of financial self-efficacy with the other indicators. The association between financial self-efficacy and self-esteem turned out to be positive and significant with the coefficient of (0.525). In statistical terms, it might be possible to say the financial self-efficacy is strongly correlated with selfesteem and the other way around. Financial self-efficacy also demonstrates positive correlation with financial anxiety. However, this indicates a moderate relationship with a value of (0.369). Similarly, results show moderate correlation of financial self-efficacy with financial self-

control (0.439) and financial stress (0396). In contrast, the constructs used in this study. Correlation analysis only relationship of financial self- efficacy becomes insignificant with financial literacy (0.106), individual financial products (0.086), risk preferences (0.054), and investment products (0.109). This finding suggests that financial self-efficacy has no relationship with financial literacy, financial products, and risk preference and investment products. gives the indications of the existence or non-existence of the relationship. However, to further examine the causal linkages, in the next step this study applies regression analysis to investigate the hypothesized relationships. This study utilizes Ordinary least square (OLS) to examine whether the psychometrics (sometimes referred as cognitive factors) have any impact on the financial In column 3 of the table, the results of the correlation of self-esteem with the other under studied indicators is reported. It is observed that the correlation coefficient of self-esteem with financial anxiety is weak and positive (0.160). Analogous to the previous result, the correlation of self-esteem with financial self-control (0.492), investment the fact that the both financial anxiety and financial stress measure the same indicator. That is the reason they show strong positive bivariate correlation. It also shows positive weak association with financial literacy (0.133). In contrast, financial anxiety demonstrates very weak and negligible correlation with individual financial products (0.108), risk preferences (0.01) and investment products (0.03). Column 5 of the correlation table presents the results of the association of financial control with the other variables. It shows that financial control has weak positive association with financial stress (0.229) and investment products (0.285). Apart from these correlations this column does not report any notable relationship. Similarly, column 6 has to offer only one weak correlation between financial literacy and financial stress with a corresponding value of (0.133). All remaining correlation coefficients found to be statistically insignificant and present near to zero correlation coefficient.

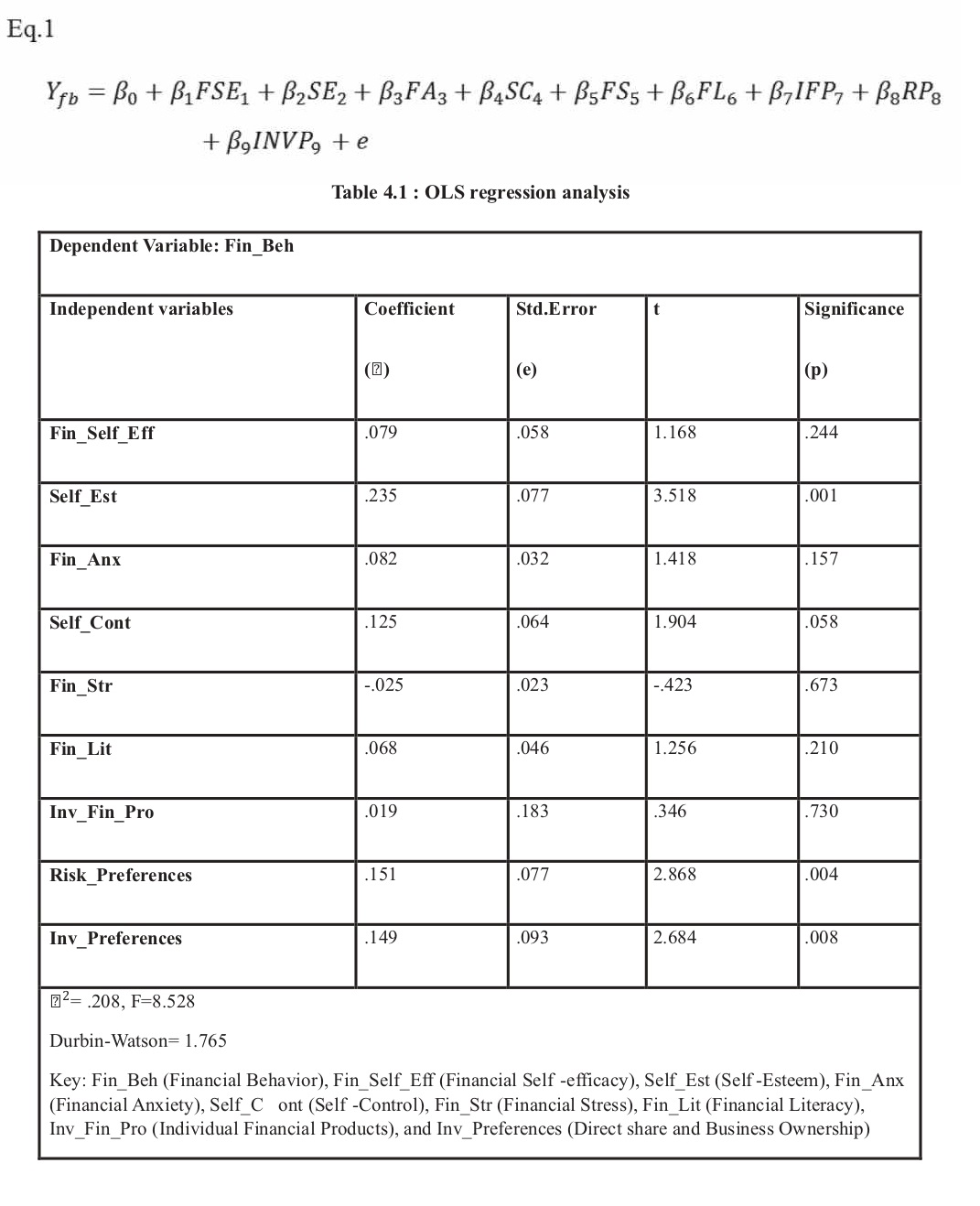

To check the relationship between the dependent and independent variables is study has used the Ordinary Least Square (OLS) technique to identify the significance level between the dependent and independent variables. This technique is used by keeping in view some facts that it is most commonly used and accepted technique. This technique is also used in some previous studies (Yurchisin and Johnson, 2004; Mottola, 2013).Multiple regression analysis has been used to determine the relationship between dependent and independent variables, the following model has been used for analysis:

Table shows the outcomes of OLS regression analysis. There are four variable indicated the significance relation with the financial behavior which includes the self-esteem, self-control, risk preferences and share and business ownership. While the financial self-efficacy, financial literacy, financial stress and financial anxiety has the insignificant impacts on the financial behavior. Besides this above Table represents that over all model is not significant. R square value (.208) report that the nine independent variables has the 20.8% variation in the outcome variable. Variance Inflation Factor (VIF) is not greater than 1.688 in this study which shows that there is no issue of multi collinearity (Gujarati and Porter, 2009; Garson, 2012). OLS regression analysis reports the value of Durbin-Watson 1.765 which is close to the 2, it shows that there is no problem of serial correlation in the variables.

In the first section of analysis we analyze the demographic and socio-demographic variables of the respondents. That indicated that working women who do not belong to the literate background also have impact on their household income. Most of the respondents have the household income less than Rs, 40,000. Demographic variables has impact on the financial behavior at some extent, because there are a lot of personality factors that contributes in the financial behavior. The following sections of describes the descriptive, correlation and regression results of the dependent and independent variables. Also the acceptance and rejection of the hypothesis will be reported in the substantial section of this chapter.

Namely financial self-efficacy belongs to the selfassuredness and self-belief level towards making financial decision. Descriptive statistics results of this study revealed that working women in the banks have average level of financial self-efficacy and they are engorging towards the higher self-efficacy as the mean score indicated the value (3.313). Which shows the women in banking have normal to high level of financial selfefficacy. Correlation coefficient (0.281) indicated the weak relationship between the financial self-efficacy and financial behavior. Regression analysis indicated that there is insignificant relationship between the financial behavior and financial self-efficacy. By considering these results we accept the null hypothesis of our study. Financial selfefficacy of an individual is based on the cognitive ability and utilization of that ability. Individuals have the different types of experience regarding efficacy altering. (Bandura, 1977) As the prospect theory described that people make Financial stress and financial anxiety has the negative effects on the mental health condition of the individual and factor like lower level of income and high levels of debts cause the reason of the decision only on the basis of potential gains, if the same product is describes with two different aspects of potential gain and losses. They will chose t eh products on the basis of gains. Sothe financial self-efficacy is depend on the different factors that change from person to person and their choices. It would not be appropriate to associate the self-efficacy with the financial behavior of individuals.

By giving the empirical support for the relationship between the financial behavior and financial self-esteem. Descriptive statistics of this study represents that selfesteem has the high values of the mean (3.304) and lower value of the standard deviation (0.528). Correlation coefficient indicated that there is moderate positive relationship between the financial behavior and selfesteem. OLS regression analysis results (.001) indicated that the self-esteem has the significant relationship with the financial behavior. Tang and Baker (2016) identified that direct and indirect impact of the self-esteem on the financial behavior they also results that there is the positive relationship between the self-esteem and financial behavior of individuals. On the basis of results of statistical analysis we accept the alternative hypothesis that there is significant relationship between the financial behavior and self-esteem. working women in banks. Descriptive statistics shows the respondents are over anxious about their financial situation. The overall mean (2.79) indicated the lower level of financial stress among the respondents. There is positive correlation between the financial anxiety and financial behavior. Also the financial stress has the strong association with the financial behavior (Hekman, Lim and Montalto, 2012; Lim et al, 2014). Regression analysis results of our study indicated the insignificant the relationship of the financial stress and financial anxiety with financial behavior. Because we collected the data from the working women in the banking sector it might be reason that while during the financial stress and anxiety they have interaction with the financial products.

To check the impact of the self-control on financial behavior in this study we determine by the descriptive coefficient, correlation and regression. Correlation coefficient (.327) indicated that there is positive relationship between both the variables. Descriptive analysis of this study results the moderate level of self- control of respondents. Regressions analysis has accepted the alternative hypothesis of this study that there significance relationship between the self-control level of working women and financial behavior. Perry and Morris (2005) also revealed the positive association between the level of self-control and financial behavior. They indicated that self-control is linked with the saving behavior of the individuals. Lower level of self-control is also related with the higher level of debts (Gathergood, 2012).

financial stress and financial anxiety. In current study we check the impact of the financial stress and financial anxiety of the financial behavior of the In this study we also analyze the risk-preferences of individuals and their impact on the financial behavior. Descriptive statistics indicated the risk averse behavior of the women that they are not willing to take the financial (age, work experience, household income, and mother's level of education and father's level of education) and socio-demographic variables (parented, remoteness, language, nationality and dependent children's). In second

For determine the relationship between financial literacy and financial behavior we also applied the descriptive, correlation and regression analysis. Descriptive statistics indicated the lower level of financial literacy among the working women. Correlation coefficient (0.09) also indicated that there is no relationship between the financial literacy and financial behavior. Also regression analysis of study accepted the null hypothesis, that there is no relationship between the financial literacy and financial behavior (Mandell and Klein, 2009). Financial literacy has impacts on the good financial management and financial well-being.

Individual financial products used in this study are the investments, mortgage, saving account, loan, credit card, private health insurance and life insurance. This study analyze the relationship between the availability of the relationship between the risk preferences and financial behavior while the regression analysis indicated that there is the significant relationship between the financial behavior and risk preferences (West and Worthington, 2012; Farrell, Fry and Risse, 2016).

financial products choices and their impact on the financial behabi9or of individuals. Descriptive statistics indicated that the women have low consideration towards the risker products. There is the weak correlation between the financial products and financial behavior. OLS regression also revealed the insignificant relationship between the individual financial products and financial behavior. Selection of the variable may depend on the level of financial self-efficacy of the individuals (Farrell, Fry and Risse, 2016).Descriptive statistics indicated that women are more interested in business ownership as compare to share ownership. There is the moderate correlation between the share and business ownership and financial behavior. Regression analysis of the study also indicated the significant relationship between financial behavior and share and business ownership

The main objective of the study is to find the relationship between the financial behavior and different psychometric instruments which include financial self-efficacy (FSE), self-esteem, financial anxiety, self-control and financial stress. This study has also focused on identifying the impact of financial literacy on the financial behavior. Risk preferences of the individuals has the positive or negative impacts on the financial behavior also determined by this research. Along with this study also analyze the impact of financial behavior, direct share ownership and business ownership on the financial behavior of the women.Primary data has been collected from the women working in the Public sector banks of Pakistan. There are five banks, First women bank ltd (FWBL), Bank of Punjab (BOP), National Bank of Pakistan (NBP), Sindh Bank and Bank of Khyber (BOK) working as the public sector banks. In this study selected the sample size of 300 working women for gathering the data. Data has been collected from the major cities of the Pakistan (Faisalabad, Lahore, Karachi and Islamabad). This study used the questionnaire survey technique for collecting the data from the targeted respondents. Survey questionnaire items has been selected from the available literature (Jacob, 2002; Tangney, Baumeister and Boon, 2004; Behrman et al., 2010; Archuleta, Dale, and Spann, 2013; Fernandes, Lynch and Niemeyer 2014; West and Worthington, 2014; Farrel, Fry and Risse, 2016). Questionnaire used in this study comprised on three sections, first section contains the demographic variables

In this study we collected the data from the public sector banks only which may not sufficient for describing the clear relationship of the psychometric variables with the financial behavior. For measuring the self-efficacy levels of the women there is also need to collect data from the entrepreneurs on the higher and lower levels for analysing their abilities to deal with the financial terms, financial financial stress and financial anxiety. In current study we check the impact of the financial stress and financial anxiety of the financial behavior of the In this study we also analyze the risk-preferences of individuals and their impact on the financial behavior. Descriptive statistics indicated the risk averse behavior of the women that they are not willing to take the financial (age, work experience, household income, and mother's level of education and father's level of education) and socio-demographic variables (parented, remoteness, language, nationality and dependent children's). In second section of the question

Agarwalla, S. K., Barua, S. K., Jacob, J., & Varma, J. R. (2015). Financial literacy among working young in urban India. World Development, 67, 101-109. Allgood, S., &Walstad, W. (2011). The effects of perceived and actual financial knowledge on credit card behavior. Andrews, B., & Wilding, J. M. (2004). The relation of depression and anxiety to life-stress and achievement in students. British Journal of Psychology, 95(4), 509-521. Atkinson, A., & Messy, F. A. (2011). Assessing financial literacy in 12 countries: an OECD/INFE international pilot exercise. Journal of Pension Economics and Finance, 10(04), 657-665. Asaad, C. T. (2015). Financial literacy and financial behavior: Assessing knowledge and confidence. Financial Services Review, 24(2), 101. Bailey, K.D. (1987). Methods of social research (3rd ed.). New York, USA: Macmillan USA. Behrman, J. R., Mitchell, O. S., Soo, C., & Bravo, D. (2010). Financial literacy and pension wealth accumulation. NBER Working Paper, 16452. Bajtelsmit, V. L., &Bernasek, A. (1996). Why do women invest differently than men?. Bajtelsmit, V., Bernasek, A., &Jianakoplos, N. (1996).

Gender effects in pension investment allocation decisions. Center for Pension and Retirement Research, 145-156. Barber, B. M., &Odean, T. (2000). Too many cooks spoil the profits: Investment club performance. Financial Analysts Journal, 17-25 Bandura, A. (2006). Toward a psychology of human agency. Perspectives on psychological science, 1(2), 164-180. Bandura, A. (1993). Perceived self-efficacy in cognitive development and functioning. Educational psychologist, 28(2), 117-148. Bandura, A. (1994). Self-efficacy. In. VS Ramachaudran. Encyclopedia of human behavior, 4, 71-81. Bandura, A. (1977). Self-efficacy: toward a unifying theory of behavioral change. Psychological review, 84(2), 191.

Beenackers, M. A., Oude Groeniger, J., Kamphuis, C. B. M., & van Lenthe, F. J. (2016). The role of financial strain and self-control in explaining income i n e q u a l i t i e s i n h e a l t h b e h a v i o r s : MariëlleBeenackers. The European Journal of Public Health, 26(suppl_1), ckw166-058. Bryman, A., and Bell, E. (2011). Business research methods (3rd ed.). Oxford: Oxford University Press. Danes, S. M., & Haberman, H. (2007). Teen financial knowledge, self-efficacy, and behavior: A gendered view. Dancey, C.P. and Reidy, J. (2004). Statistics without Maths for Psychology. Essex, United Kingdom: Prentice Hall. Di Paula, A., & Campbell, J. D. (2002). Self-esteem and persistence in the face of failure. Journal of personality and social psychology, 83(3), 711. Engelberg, E. (2007). The perception of self-efficacy in coping with economic risks among young adults: an application of psychological theory and research.