|

C.A. (Dr.) Pramod Kumar Pandey Associate Professor School of Management Presidency University, Itgalpur Rajanakunte,Yelahanka, Bengaluru, Karnataka, India |

The paper has examined the impact of tax structures on economic growth in India. Data regarding Personal Income Taxes, Corporate Taxes, and Gross Domestic Product have been collected from the website of Reserve Bank of India from 1973-74 to 2018-19. The study applies Johansen Cointegration, Vector Error Correction Model followed by Wald Test to analyze the long-run and short-run relation between the variables. The results indicate that Corporate Taxes and Indirect Taxes have a positive impact while Personal Income Tax negative impact on the economic growth of India in the long run. Thus, the findings of this study do not support the decision taken by the Government of India regarding Corporate Tax rate cuts.

Keywords:Personal Income Tax, Corporate Tax, Indirect Tax, Gross Domestic Product, Tax Buoyancy, Goods and Services Tax JEL classification:H25, H21, E21, E23

|

C.A. (Dr.) Pramod Kumar Pandey Associate Professor School of Management Presidency University, Itgalpur Rajanakunte,Yelahanka, Bengaluru, Karnataka, India |

The paper has examined the impact of tax structures on economic growth in India. Data regarding Personal Income Taxes, Corporate Taxes, and Gross Domestic Product have been collected from the website of Reserve Bank of India from 1973-74 to 2018-19. The study applies Johansen Cointegration, Vector Error Correction Model followed by Wald Test to analyze the long-run and short-run relation between the variables. The results indicate that Corporate Taxes and Indirect Taxes have a positive impact while Personal Income Tax negative impact on the economic growth of India in the long run. Thus, the findings of this study do not support the decision taken by the Government of India regarding Corporate Tax rate cuts.

Keywords:Personal Income Tax, Corporate Tax, Indirect Tax, Gross Domestic Product, Tax Buoyancy, Goods and Services Tax JEL classification:H25, H21, E21, E23

“Taxes are indeed very heavy, and if those laid on by the Government were the only Ones we had to pay, we might more easily discharge them; but we have many others, and much more grievous to some of us. We are taxed twice as much by our Idleness, three times as much by our Pride, and four times as much by our Folly” (Benjamin Franklin, 1733)

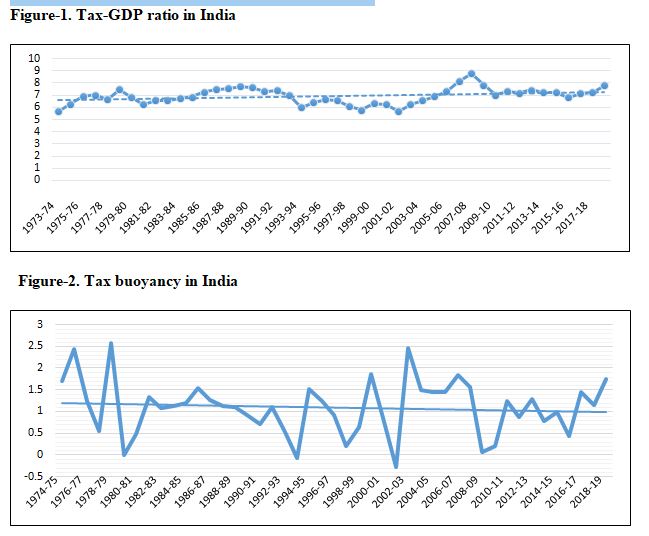

The above quote by Benjamin Franklin rightly describes the burden of taxes. Everyone pays multiple taxes due to binding obligation of law however the return they get for payment of taxes always remains in dark. Tax is one of the most important sources for the Government’s revenue in any country. Taxes act as a source for financing public expenditure. Taxes thus reduces the borrowing requirements of the Government and helps to discharge several responsibilities for social welfare. Even after seventy-two years of independence, tax culture has not been properly established in India. Still, a general tendency to avoid tax is predominant in the Indian economy. This is more because people are more concerned about fairness and justice in treatments (Ashraf, Camerer & Loewenstein, 2005). Every country has a unique tax structure. Tax structure includes the combinations of direct and indirect taxes levied to pursue revenue goals of the Government of a country. The tax policy decides the tax structure. It is not simply the tax but the proper tax structure that may flourish long term growth. Proper tax structure should be conducive to growth and at the same time, it should encompass the required features like equity, fairness, and simplicity. The aim of taxes should be to uplift economic growth without sacrificing human welfare. Tax policy extends beyond the country’s borders and hence requires serious deliberations before setting up a tax policy. Many economic works of literature discuss the effect of taxes on economic growth. The endogenous growth model emphasizes that taxation affects both the short-run and long-run growth of any economy. Whereas Direct Taxes reduce disposable income, Indirect Taxes reduce the efficiency of disposable income. India has a blend of progressive and proportionate taxation. Progressive taxation is levied to reduce the income inequality gap. However, it also reduces encouragement to generate more income and many times individuals start misrepresenting their income and taxes (Slemrod, 1990). The Indian tax structure is shifting from Direct Taxes to Indirect Taxes for reducing the fiscal deficit gap. Recently, personal income taxes have been exempted up to Rupees five lakhs vide budget 2019-20 (MOF, GOI, 2019) and corporate taxes have been brought down to twenty-two percent only for domestic companies. Savings and investments are two pillars for the economic growth of any nation. Taxes directly affect savings and investments. Policymakers while devising any tax policy should fix up the desired savings and investment goals both short term and long run (Harrod, 1939). Reduction in tax rates and providing more avenues for investments may speed up economic growth. Bringing down the tax rates will have the effect of pushing encouragement towards working, investing and saving (Gale &Samwick, 2014). Further, the importance of labour and capital as predominating factors of production cannot be ignored. Taxes directly impact both labour and capital which are used in the production process. Neo-classical economists viewed ease of substitution between labour and capital through technological advancement to ensure a steady growth rate (Solow, 1956). However, every factor substitution has unique tax implications and different growth impacts. The main objective of this paper is to analyze the impact of the existing tax structure on Indian economic growth. For measuring economic growth, the growth rate of Gross Domestic Product (GDP) is a widely accepted criterion among the researchers. GDP is affected by many factors however taxes have a long-lasting impact on GDP. The tax-GDP ratio shows a percentage increase in taxes due to a one percent increase in GDP. The tax-GDP ratio in India is quite inconsistent ranging between 7 percent to 8 percent in the last forty-five years (Figure-1). However, Tax buoyancy which shows the growth rate of taxes to the growth rate of GDP is depicting a falling trend for the same period (Figure-2).

Hence, this paper has been organized as follows. The next section reviews empirical evidence of the impact of tax on GDP. The third section conducts the multivariate analysis to assess the impact of taxes on the Indian GDP. The fourth section incorporates discussions highlighting the problem areas in the Indian tax structure which are acting as hurdles in the economic growth of the country. Finally, the paper ends in the fifth section with concluding remarks to assist policymakers to draw an appropriate tax structure that may boost the growth of the Indian economy.

The effect of taxes on the economic growth of a country has been a long-lasting debate. Many research studies have been conducted on the topic. Among researchers, there is a wider acceptance of the view that taxation influences economic growth (Slemrod, 1990, Engen & Skinner, 1996, Myles, 2000, Scully, 2003) However, their opinions vary regarding the impact of direct and indirect taxes. The majority of authors have found the positive influence of indirect taxes while the negative influence of direct taxes on economic growth in the long run (Matallah&Matallah, 2017, Vazquez et al 2009, Dackehag& Hansson, 2012, Ferede&Dahlby, 2012, McBride, 2012). Two major components of direct taxes are corporate income taxes and personal income. Many studies suggest the negative impact of corporate taxes as having more harmful than personal income taxes (McBride, 2012,Johansson et al 2008, Veronika&Lenka, 2012). Studies also suggest Tax structure based on selective consumption taxes, taxes on personal income and property is more conducive to Economic growth (Stoilova, 2017). Ahmad, Sial& Ahmad (2018) found that Indirect taxes bring negative effects in the long run as compared to the short run. There was a multiplicity of taxes in indirect taxes domain before the Goods and Services Tax came into practice with effect from 1st July 2017. Venkataraman, &Urmi, 2017 found that Economic growth is more affected by Customs duty as compared to Excise duty. It is also argued that Shift in tax structure from trade to domestic consumption taxes is having positive effects for economies classified as lower-middle-income (McNabb, 2016). India follows a progressive taxation mechanism where the tax rate increases with an increase in income. This many times frustrates the high earner group and induce them towards misrepresenting their income and taxes. Slemrod, J., 1990 argued towards bringing a flat rate of personal taxes as a safeguard to minimize tax misrepresentations. Further, Tax rate cuts have been found to create inducement towards working, saving and investing (Ogbonna, George &Odoemelam, Ndubuisi. (2015). Attitude, behavior, and norm also play an important role in deciding tax compliance (Engen & Skinner, 1996). Ullmann, Robert &Watrin, Christoph. (2008) found different reactions of individuals towards different taxes. Subject to certain assumptions any behavioral reactions towards taxes in the form of evasion or avoidance are symptoms of inefficiency (Slemrod, 2018). There is always a growth maximizing rate (Scully. 2003). Below the maximum rate positive impact of taxes on economic growth may be seen, however, once the threshold limit crossed the negative impact of taxes starts (Huňady&Orviská, 2015). Further, the higher tax rate may have the effect of curtailing consumptions and may also induce leakages (Caulkins, et al 2015). The role of foreign capital cannot be ignored for economic growth. Tax structures built up to give concessions to foreign investors may invite more foreign capital. Sinevicienea&Railieneb (2015) suggested that the Taxation structure is an important driving force for private investment. Further, the higher the corporate income tax, the lower will be private investment and slower will be economic growth (Ferede&Dahlby, 2012). On the capital taxation side it has been argued that where growth is driven by domestic innovation activity, positive rates of capital taxation can increase the long-run growth rate (Kate & Milionis, 2019). It goes without saying that for designing an optimal tax system, the use of both direct and indirect taxes are required. Taxes have the effect of bringing inequality. A buffet rule for individuals and companies with wealth tax will have the effect of making the system more equitable (Passant, 2017). There is evidence of molding tax systems to bridge the gap of gender inequality. Economic policies should focus to incorporate social justice and gender equality (Hodgson &Sadiq 2017). For a tax policy to be effective, it should be well planned and efficiently implemented. The policies which are poorly implemented may be deficient in uplifting the economic development (Kransdorff, 2010). Studies also suggest taxing land at higher than the building for developments (Junge& Levinson 2012). Taxes may also be seen as a means of bringing welfare. Kiss (2009) suggested that any tax rate above the Nash equilibrium rate may reduce welfare. The empirical studies may be summarized as under

|

S/N |

Authors |

Data and period |

Method |

Results |

|

1 |

Skinner, (1987). |

31 sub-Saharan African countries during 1965-73 and 1974-82. |

Regression Analysis |

Output growth will be affected when countries are not on a steady growth path. |

|

2 |

Barro, (1991). |

98 countries 1960-1985 |

Regression Analysis |

There is a negative relation of per capita growth and the ratio of private investment to GDP with the ratio of government consumption expenditure to GDP. |

|

3 |

Poulson& Kaplan, (2008) |

United States ,1964 -2004 |

Ordinary least squares regression analysis |

Economic growth is negatively impacted due to higher marginal rates of taxes. |

|

4 |

Padda&Akram (2009) |

Pakistan, India and Sri Lanka, 1973–2008 |

GLS transformed Dickey-Fuller, Impulse response |

The tax rate changes have a negative impact on the economic growth of the selected three countries in the short run. |

|

5 |

Dackehag&Hansson (2012). |

25 OECD member countries, 1970-2010 |

Regression model |

There is a negative impact of taxation of corporate income on economic growth. |

|

6 |

Ferede&Dahlby, (2012). |

Canada, 1977–2006 |

Regression model |

Higher the corporate income tax, lower will be private investment and slower will be economic growth |

|

7 |

McBride,(2012) |

twenty-six such studies going back to 1983 |

Review Article |

Taxes have a negative effect on growth. Corporate income taxes are most harmful followed by personal income taxes. |

|

8 |

Veronika&Lenka, (2012). |

27 EU member countries , 1998 – 2010 |

Regression model |

If the tax burden is reduced, there will be a greater impact on EU15 countries as compared to EU12 new member countries. |

|

9 |

Stoilova&Patonov (2013) |

EU countries, 1995-2010 |

Regression model |

The tax structure based on direct taxes plays a crucial role in the economic growth of EU countries. |

|

10 |

Gale &Samwick, (2014). |

Past 50 years, U.S. |

simulation analyses |

Different taxes have a different impact on economic growth. Reforms should focus on improving incentives, curtailing existing subsidies, removing windfall gains and minimizing deficit financing to have long term growth of the economy

|

|

11 |

Macek, (2014). |

OECD Countries 2000-2011 |

Regression model |

There is a negative impact of corporate taxes and income taxes on economic growth, however, the negative impact of value-added tax was not confirmed. |

|

12 |

Huňady&Orviská (2015). |

EU countries (1999-2011) |

panel data regressions |

There is a maximum tax rate below which the positive impact of taxes on economic growth may be seen, however, once the threshold limit crossed the negative impact of taxes start. |

|

13 |

Sinevicienea&Railieneb, (2015) |

European Union (EU) countries, 2003 – 2012 |

Spearman’s correlations |

The taxation structure is an important driving force for private investment. |

|

14 |

Clausing, (2016). |

U.S. multinational corporations, 1983 – 2012 |

Regression Analysis |

For the countries having without low tax rates, tax base erosion is a large problem. |

|

15 |

Iriqat, &Anabtawi, (2016). |

Palestine, 1999-2014 |

Ordinary Least Square |

There is no Granger Causality flowing from tax revenue to GDP, Government spending, Consumption, Investment and Balance of trade |

|

16 |

McNabb, (2016). |

100 developing and developed countries. the past 30 years |

Error correction model |

A shift in tax structure from trade to domestic consumption taxes are having positive effects for economies classified as lower-middle-income. |

|

17 |

Ojong, Anthony &Arikpo, (2016) |

Nigeria, 1986 to 2010. |

Regressions model |

No significant relationship was found between Company Income Tax and GDP and growth of the Nigeria economy |

|

18 |

Kalaš, Mirović, &Andrašić, (2017). |

United States, 1996-2016 |

Regression model |

There is no significant impact of personal income taxes and corporate income tax over growth of GDP. |

|

19 |

Matallah&Matallah (2017) |

Algeria 1970-2015 |

Johansen Cointegration test and Vector Error Correction Model (VECM) |

While direct taxes have a significant negative effect, the indirect tax has a significant positive effect on real GDP in the long run. |

|

20 |

Stoilova, D. (2017). |

EU-28 member states, 1996–2013

|

regression model

|

Tax structure based on selective consumption taxes, taxes on personal income and property is more conducive to the economic growth |

|

21 |

Tapşın, (2017). |

OECD countries, 2008-2014 |

panel regression method |

The tax burden is more positively affected by direct taxes and economic growth |

|

22 |

Venkataraman, &Urmi, (2017). |

India 1977-2015 |

ARDL Bounds test |

Economic growth is more affected by Customs duty as compared to Excise duty |

|

23 |

Ahmad, Sial& Ahmad, (2018). |

Pakistan, 1974 – 2010 |

Auto Regressive Distributed Lag (ARDL) bounds testing approach |

Indirect taxes bring negative effect in the long run as compared to short-run |

|

24 |

BÂZGAN, (2018). |

Romania, 2009-2017 |

Vector Autoregressive Model |

Indirect taxes have a positive influence on economic growth as compared to direct taxes. |

|

25 |

Kate, F. & Milionis, P (2019). |

77 OECD Member countries (1965-2014) |

Ordinary Least Square |

Where growth is driven by domestic innovation activity, positive rates of capital taxation can increase the long-run growth rate. |

|

26 |

Vatavu, Lobont, Stefea, &Olariu, (2019). |

the Central and Eastern Europe (CEE) countries, 1995–2015 |

Granger non-causality tests, Cointegration techniques with error correction models

|

There is a significant influence of taxation on economic growth and citizen wellbeing.

|

This study is based on secondary data collected from the website of Reserve Bank of India. This study has collected 45 year’s data from 1973-74 to 2018-19. The data relates to Direct Taxes, Indirect Taxes (IDT) and Gross Domestic Product (GDP). Direct taxes have been segmented into Corporate Taxes (CT) and Personal Income Taxes (PIT) for understanding the individual effects. All the data have been converted into a natural log (LN) to maintain consistency. Data have been analyzed using E Views 7.1. The study applies the model of Matallah and Matallah (2017). However, the study excludes the impact of expenditure on GDP because the paper confines itself to examine the only impact of taxes on the GDP of the Indian economy. Following functional relationship is developed. GDP = f (PIT, CT, IDT) (1) Where GDP refers to Gross Domestic Products, PIT refers to Personal Income Taxes and IDT refers to Indirect Taxes. Above functional relation after converting into a natural log (ln) may be written in equation form as follows: ln GDP = β_0 + β_1 〖ln CT〗_t + β_2 〖ln PIT〗_t +β_3 〖ln IDT〗_t+ ε_t(2) Here,β_0, β_1,β_2 and β_(3 ) are defined parameters to be tested under the study, t shows the time trend and ε reflects error term. For testing unit root, the Augmented Dickey-Fuller (ADF) test is to be applied. The selection of an appropriate model will depend on unit root analysis. If the variables are stationary at level, Ordinary Least Square Method (OLS) may yield good results. However, if variables are found to have stationary at first difference, the application of Ordinary Least Square Method (OLS) may produce spurious regressions and the most appropriate model in such a case would be Johansen Cointegration which studies whether a combination of variables move together or not. If Cointegration is detected between variables, Vector Error Correction Model (VECM) followed by Wald Test shall be applied to establish the long run and short-run relation between the variables. The study seeks to test the hypothesis at 5% (α = 0.05) level.

The descriptive statistics of the variables are listed in table-2. The results show larger deviations in values for the Personal Income Taxes (LNPIT) and Corporate Taxes (LNCT) as compared to Indirect Taxes (LNIDT). Further, the results of the JarqueBera test reflect that all the variables under study are normally distributed

|

|

LNGDP |

LNCT |

LNIDT |

LNPIT |

|

Mean |

13.96587 |

9.712420 |

10.86743 |

8.756885 |

|

Median |

14.09276 |

9.769734 |

11.06416 |

8.278088 |

|

Maximum |

16.76048 |

12.97050 |

13.48912 |

12.71687 |

|

Minimum |

11.13342 |

6.368187 |

8.023552 |

5.361292 |

|

Std. Dev. |

1.720226 |

2.069154 |

1.552884 |

2.400541 |

|

Skewness |

-0.030205 |

0.069775 |

-0.129742 |

0.229521 |

|

Kurtosis |

1.764404 |

1.664383 |

1.951479 |

1.489098 |

|

Jarque-Bera |

2.933167 |

3.456416 |

2.236228 |

4.779294 |

|

Probability |

0.230712 |

0.177602 |

0.326896 |

0.091662 |

|

Sum |

642.4298 |

446.7713 |

499.9016 |

402.8167 |

|

Sum Sq. Dev. |

133.1630 |

192.6630 |

108.5152 |

259.3168 |

|

Observations |

46 |

46 |

46 |

46 |

Unit root is tested using Augmented Dickey-Fuller (ADF) test by applying the following equation ∆ Y_t = α_0 + b_1t + β_(Yt-1)+ ∑_(i=1)^p▒γ_(i∆ Y_(t-i) ) +ε_t(3) In above equation ∆ represents first difference, Y denotes dependent variable, t reflects time trend and ε_t shows the error term. Further, P is the optimal lag length andα,β and γ denote the parameters under considerations to be tested. b_1t is included for the trend which may be eliminated in case variables do not reflect a time trend. However, as precautionary measure, unit root has been tested using both only intercept and intercept with trend. The results of ADF test (table-3) shows that all the variables are stationary at the first difference.

|

Lags: Testing down from 9 lags Criterion: Schwarz Information Criterion (BIC) |

||||

|

Variables |

P-Value at I(0) |

P-Value at I(1) |

||

|

|

With intercept |

With intercept and trend |

With intercept |

With intercept and trend |

|

Gross Domestic Product (LNGDP) |

0.9539 |

0.3259 |

0.0006 |

0.0041 |

|

Corporate Taxes (LNCT) |

0.9052 |

0.3696 |

0.0000 |

0.0001 |

|

Indirect Taxes (LNIDT) |

0.7709 |

0.3235 |

0.0000 |

0.0000 |

|

Personal Income Taxes (LNPIT) |

0.9576 |

0.4762 |

0.0000 |

0.0000 |

When the variables are found to be stationary at first differences, the application of the Ordinary Least Square (OLS) method may yield spurious regressions. In such cases, the Johansen Cointegration test may be applied which assumes that a combination of variables may move together. However, for applying Johansen Cointegration, all the variables should be integrated into the same order. Since in this study all the four variables have been found stationary at first differences, Johansen and Juselius (1990) method is applied to identify the number of cointegrating vectors. As the first step, the VAR lag selection test is applied for selecting the appropriate lag length. The results of the VAR lag selection test (Table-4) show 1 lag as the most appropriate so the Johansen Cointegration test is conducted at lag 1.

|

Lag |

LogL |

LR |

FPE |

AIC |

SC |

HQ |

|

0 |

-52.29078 |

NA |

0.000171 |

2.680513 |

2.846006 |

2.741173 |

|

1 |

186.2373 |

420.2638* |

4.31e-09* |

-7.916062* |

-7.088600* |

-7.612764* |

|

2 |

202.1181 |

24.95554 |

4.43e-09 |

-7.910385 |

-6.420954 |

-7.364450 |

|

3 |

215.0272 |

17.82690 |

5.43e-09 |

-7.763201 |

-5.611801 |

-6.974628 |

|

4 |

233.9826 |

22.56597 |

5.28e-09 |

-7.903935 |

-5.090566 |

-6.872724 |

|

* indicates lag order selected by the criterion LR: sequential modified LR test statistic (each test at 5% level) FPE: Final prediction error AIC: Akaike information criterion SC: Schwarz information criterion HQ: Hannan-Quinn information criterion |

||||||

For the testing hypothesis, two popular tests under Johansen Cointegration are the "Trace test" and "Max-Eigenvalue test”. The number of cointegrating vectors under Johansen Cointegration should be lesser than the number of variables under study. Thus, for proper long term relation, the number of cointegrating vectors should be n-1. Since, in the present study, the number of variables is four, the number of cointegrating vectors should at most be three. Thus, the following hypothesizes are set for deciding the number of cointegrating vectors among the variables:

variables: Ho: There is no cointegrating vector among the variables H1: There is at most one cointegrating vector among the variables H2: There are at most two cointegrating vectors among the variables H3: There are at most three cointegrating vectors among the variables

Results of both the Trace test and the Maximum Eigenvalue test have identified one cointegrating vector at 0.05 level (Table-5 and Table-6)

|

Hypothesized No. of CE(s) |

Eigenvalue |

Trace Statistic |

0.05 Critical Value |

Prob.** |

|

None * |

0.569959 |

59.86292 |

47.85613 |

0.0025 |

|

At most 1 |

0.323816 |

22.73244 |

29.79707 |

0.2594 |

|

At most 2 |

0.114467 |

5.515657 |

15.49471 |

0.7519 |

|

At most 3 |

0.003783 |

0.166774 |

3.841466 |

0.6830 |

|

Trace test indicates 1 cointegratingeqn(s) at the 0.05 level * denotes rejection of the hypothesis at the 0.05 level **MacKinnon-Haug-Michelis (1999) p-values |

||||

|

Hypothesized No. of CE(s) |

Eigenvalue |

Max-Eigen Statistic |

0.05 Critical Value |

Prob.** |

|

None * |

0.569959 |

37.13047 |

27.58434 |

0.0022 |

|

At most 1 |

0.323816 |

17.21679 |

21.13162 |

0.1620 |

|

At most 2 |

0.114467 |

5.348883 |

14.26460 |

0.6973 |

|

At most 3 |

0.003783 |

0.166774 |

3.841466 |

0.6830 |

|

Max-eigenvalue test indicates 1 cointegrating eqn(s) at the 0.05 level * denotes rejection of the hypothesis at the 0.05 level **MacKinnon-Haug-Michelis (1999) p-values |

||||

Vector Error Correction Model (VECM) may be applied to study the long run and short-run relationship among the variables and also the speed at which equilibrium is restored after a given shock in any of the variables. However, for the applicability of this model Johansen test must identify one or more cointegrating vectors. Firstly the basic equation of VAR model is given as under: Y_t = α_t + β_1 y_(t-1) +〖 β〗_2 y_(t-2) + ……… β_p y_(t-p)+ ε_t (4) After this, the VECM representation of VAR model may be given as under 〖∆Y〗_t= α_t + Π_(Y_(t-1) )+∑_(i=1)^(p-1)▒Γ_(i ∆Y_(t-i) ) + ε_t(5) The equation (5) shows a Vector Error Correction Model (VECM) having order p-1 where Π commonly denoted as αβ’ represents long term relation between the variables. Since, the results of Johansen Cointegration has identified one cointegrating vector, the study proceeds to apply VECM to evaluate relation between the variables. The Results of the VECM are shown in table-6. As per results, following long run equation may be given lnGDP_t = -0.606039lnCT_t + 0.150670 lnPIT_t-0.537524 lnIDT_t-3.552687+ε_1t(6) The above equation (7) shows positive long run relation of GDP with Corporate Taxes and Indirect Taxes and negative long run relationship with Personal Income Taxes. Thus, 1% increase in Corporate Taxes may increase GDP by 0.60% and 1% increase in Indirect Taxes may increase GDP by 0.53%. While 1% increase in Personal Income Taxes may decrease GDP by 0.15%.

|

Vector Error Correction Estimates Date: 10/13/19 Time: 08:36 Sample (adjusted): 3 46 Included observations: 44 after adjustments Standard errors in ( ) & t-statistics in [ ] |

||||

|

CointegratingEq: |

CointEq1 |

|||

|

LNGDP(-1) |

1.000000 |

|||

|

LNCT(-1) |

-0.606039 (0.08316) [-7.28805] |

|||

|

LNPIT(-1) |

0.150670 (0.04307) [ 3.49839] |

|||

|

LNIDT(-1) |

-0.537524 (0.06583) [-8.16514] |

|||

|

C |

-3.552687 |

|||

|

|

||||

|

Error Correction: |

D(LNGDP) |

D(LNCT) |

D(LNPIT) |

D(LNIDT) |

|

CointEq1 |

-0.097395 (0.03772) [-2.58210] |

0.514175 (0.18235) [ 2.81976] |

0.053540 (0.47829) [ 0.11194] |

0.244523 (0.12504) [ 1.95555] |

|

D(LNGDP(-1)) |

0.323337 (0.15117) [ 2.13884] |

1.569191 (0.73083) [ 2.14715] |

0.769730 (1.91693) [ 0.40154] |

0.937412 (0.50115) [ 1.87052] |

|

D(LNCT(-1)) |

-0.012390 (0.03337) [-0.37130] |

0.216613 (0.16132) [ 1.34277] |

0.212830 (0.42313) [ 0.50299] |

0.056300 (0.11062) [ 0.50895] |

|

D(LNPIT(-1)) |

-0.006621 (0.01304) [-0.50773] |

-0.116302 (0.06304) [-1.84477] |

-0.252520 (0.16536) [-1.52707] |

-0.080184 (0.04323) [-1.85477] |

|

D(LNIDT(-1)) |

-0.134785 (0.04759) [-2.83227] |

-0.161597 (0.23006) [-0.70240] |

0.083418 (0.60344) [ 0.13824] |

0.009104 (0.15776) [ 0.05771] |

|

C |

0.102772 (0.01812) [ 5.67172] |

-0.044369 (0.08760) [-0.50651] |

0.058255 (0.22977) [ 0.25354] |

0.004359 (0.06007) [ 0.07256] |

|

|

||||

|

R-squared |

0.400915 |

0.233801 |

0.070169 |

0.160171 |

|

Adj. R-squared |

0.322088 |

0.132986 |

-0.052177 |

0.049667 |

|

Sum sq. resids |

0.021366 |

0.499331 |

3.435352 |

0.234798 |

|

S.E. equation |

0.023712 |

0.114631 |

0.300673 |

0.078606 |

|

F-statistic |

5.086009 |

2.319099 |

0.573529 |

1.449464 |

|

Log likelihood |

105.4303 |

36.09757 |

-6.331748 |

52.69752 |

|

Akaike AIC |

-4.519561 |

-1.368072 |

0.560534 |

-2.122615 |

|

Schwarz SC |

-4.276262 |

-1.124773 |

0.803833 |

-1.879316 |

|

Mean dependent |

0.124116 |

0.145606 |

0.155119 |

0.118321 |

|

S.D. dependent |

0.028799 |

0.123109 |

0.293123 |

0.080634 |

|

Determinant resid covariance (dof adj.) 2.30E-09 Determinant resid covariance 1.28E-09 Log likelihood 200.8016 Akaike information criterion -7.854617 Schwarz criterion -6.719224 |

||||

Short run equation may be reproduced as below 〖∆LNGDP〗_t = - 0.097 〖ECT〗_(t-1) + 〖0.323 ∆LNGDP〗_(t-1) - 〖0.012 ∆LNCT〗_(t-1) - 〖0.006 ∆LNPIT〗_(t-1) -0.134 〖∆LNIDT〗_(t-1)+ 0.102 (9) The speed at which equilibrium restored due to a shock in one variable is measured by the Error Correction Coefficient. However, the Error Correction Coefficient needs to be negative as well as significant. Table-8 shows that the value of the error correction coefficient is -0.097395 with a probability of 0.0138. Thus, the error correction coefficient is negative and significant in the present study. Further, the coefficient of Indirect Taxes also negative and significant and hence it can be emphasized that in the short run also Indirect Taxes have a positive influence on the GDP. Further, since coefficients of Personal Income Taxes and Corporate Taxes are negative but not significant, Wald Test is estimated to evaluate short-run relation between Personal Income Taxes and Corporate Taxes to GDP.

|

Dependent Variable: D(LNGDP) Method: Least Squares Date: 10/13/19 Time: 09:34 Sample (adjusted): 3 46 Included observations: 44 after adjustments |

||||

|

D(LNGDP) = C(1)*( LNGDP(-1) - 0.606039159171*LNCT(-1) + 0.150670152967*LNPIT(-1) - 0.537523745633*LNIDT(-1) - 3.55268722392 ) + C(2)*D(LNGDP(-1)) + C(3)*D(LNCT(-1)) + C(4) *D(LNPIT(-1)) + C(5)*D(LNIDT(-1)) + C(6) |

||||

|

|

Coefficient |

Std. Error |

t-Statistic |

Prob. |

|

C(1) |

-0.097395 |

0.037719 |

-2.582103 |

0.0138 |

|

C(2) |

0.323337 |

0.151174 |

2.138841 |

0.0389 |

|

C(3) |

-0.012390 |

0.033369 |

-0.371298 |

0.7125 |

|

C(4) |

-0.006621 |

0.013041 |

-0.507729 |

0.6146 |

|

C(5) |

-0.134785 |

0.047589 |

-2.832267 |

0.0074 |

|

C(6) |

0.102772 |

0.018120 |

5.671721 |

0.0000 |

|

R-squared 0.400915 Adjusted R-squared 0.322088 S.E. of regression 0.023712 Sum squared resid 0.021366 Log likelihood 105.4303 F-statistic 5.086009 Prob (F-statistic) 0.001149 |

Mean dependent var 0.124116 S.D. dependent var 0.028799 Akaike info criterion -4.519561 Schwarz criterion -4.276262 Hannan-Quinn criter. -4.429334 Durbin-Watson stat 1.782546 |

|||

For estimating Wald test following hypothesis are set H0: C(3)=C(=4)=0 H1: C(3)=C(4)≠0 Wald test results accepts the null hypothesis that there is no short run causality flowing from Corporate Taxes and Personal Income Taxes to GDP (Table-9)

|

Test Statistic |

Value |

df |

Probability |

|

F-statistic |

0.242539 |

(2, 38) |

0.7858 |

|

Chi-square |

0.485077 |

2 |

0.7846 |

|

Null Hypothesis: C(3)=C(4)=0 |

|||

|

Null Hypothesis Summary: |

|||

|

Normalized Restriction (= 0) |

Value |

Std. Err. |

|

|

C(3) |

-0.006621 |

0.013041 |

|

|

C(4) |

-0.012390 |

0.033369 |

|

|

Restrictions are linear in coefficients. |

|||

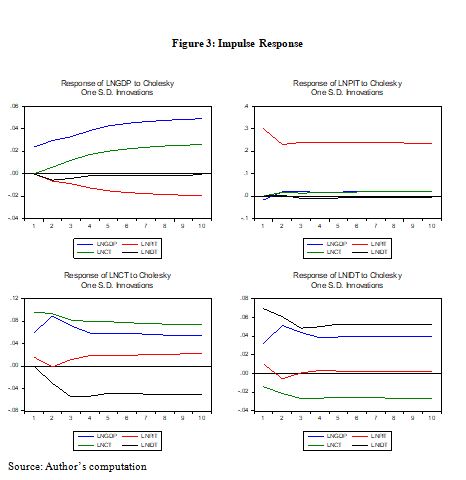

The results of the estimated variance decomposition have been shown in table-10. Variance Decomposition identifies the effect on one variable due to a shock in other variables. It is evident that in the first year due to its own shock, 100% fluctuations have been caused in GDP. In the second year, a shock in GDP will cause 93% fluctuations in GDP while a shock in Corporate Taxes will cause 1.32% fluctuations in GDP, a shock in Personal Income taxes will result in 3.49% fluctuations in GDP and a shock in Indirect taxes will cause 2.13% variability in GDP. In the fifth year, a shock in GDP will cause 80% fluctuations in GDP while a shock in Corporate Taxes will cause 8.86% fluctuations in GDP, a shock in Personal Income taxes will result in 10.24% fluctuations in GDP and a shock in Indirect taxes will cause 0.76% variability in GDP. In the tenth year, a shock in GDP will cause 73% fluctuations in GDP while a shock in Corporate Taxes will cause 12% fluctuations in GDP, a shock in Personal Income taxes will result in 13% fluctuations in GDP and a shock in Indirect taxes will cause 0.27% variability in GDP. In the short run and long run both GDP in India is more affected due to a change in Personal Income Taxes where unfortunately the study has identified higher tax evasions. The same results are also reflected by Impulse Response of the variables as shown in figure-3.

|

Variance Decomposition of LNGDP: |

|||||

|

Period |

S.E. |

LNGDP |

LNCT |

LNPIT |

LNIDT |

|

1 |

0.023712 |

100.0000 |

0.000000 |

0.000000 |

0.000000 |

|

2 |

0.039249 |

93.05101 |

1.324825 |

3.493422 |

2.130748 |

|

3 |

0.053573 |

87.86793 |

4.466828 |

5.911391 |

1.753849 |

|

4 |

0.069279 |

83.29133 |

7.178602 |

8.414558 |

1.115513 |

|

5 |

0.085179 |

80.12465 |

8.862130 |

10.24774 |

0.765479 |

|

6 |

0.100242 |

77.95092 |

9.989304 |

11.48169 |

0.578085 |

|

7 |

0.114363 |

76.36132 |

10.82617 |

12.35160 |

0.460910 |

|

8 |

0.127667 |

75.16214 |

11.45801 |

13.00010 |

0.379755 |

|

9 |

0.140218 |

74.24408 |

11.93756 |

13.49665 |

0.321712 |

|

10 |

0.152057 |

73.52763 |

12.31004 |

13.88330 |

0.279025 |

|

Variance Decomposition of LNCT: |

|||||

|

Period |

S.E. |

LNGDP |

LNCT |

LNPIT |

LNIDT |

|

1 |

0.114631 |

26.59935 |

73.40065 |

0.000000 |

0.000000 |

|

2 |

0.175677 |

37.22351 |

58.83994 |

0.934151 |

3.002392 |

|

3 |

0.214514 |

36.32709 |

54.42123 |

0.636167 |

8.615519 |

|

4 |

0.243136 |

34.17571 |

53.69798 |

0.542721 |

11.58358 |

|

5 |

0.267417 |

32.95596 |

53.66769 |

0.496495 |

12.87986 |

|

6 |

0.289320 |

32.24218 |

53.45725 |

0.468816 |

13.83176 |

|

7 |

0.309293 |

31.61799 |

53.19823 |

0.467449 |

14.71633 |

|

8 |

0.327695 |

31.04672 |

53.00826 |

0.482785 |

15.46224 |

|

9 |

0.344900 |

30.56318 |

52.86837 |

0.503014 |

16.06543 |

|

10 |

0.361167 |

30.15744 |

52.74741 |

0.524074 |

16.57108 |

|

Variance Decomposition of LNPIT: |

|||||

|

Period |

S.E. |

LNGDP |

LNCT |

LNPIT |

LNIDT |

|

1 |

0.300673 |

0.302194 |

2.779583 |

96.91822 |

0.000000 |

|

2 |

0.379654 |

0.452320 |

3.836228 |

95.70145 |

0.010005 |

|

3 |

0.449722 |

0.525131 |

4.145885 |

95.27434 |

0.054647 |

|

4 |

0.510290 |

0.515824 |

4.383488 |

95.00859 |

0.092096 |

|

5 |

0.564162 |

0.520532 |

4.610541 |

94.77034 |

0.098584 |

|

6 |

0.612858 |

0.547125 |

4.802009 |

94.55122 |

0.099647 |

|

7 |

0.657815 |

0.575692 |

4.954074 |

94.36807 |

0.102165 |

|

8 |

0.699853 |

0.599621 |

5.079213 |

94.21648 |

0.104690 |

|

9 |

0.739458 |

0.620655 |

5.185536 |

94.08751 |

0.106302 |

|

10 |

0.777003 |

0.639864 |

5.276378 |

93.97637 |

0.107390 |

|

Variance Decomposition of LNIDT: |

|||||

|

Period |

S.E. |

LNGDP |

LNCT |

LNPIT |

LNIDT |

|

1 |

0.078606 |

16.87707 |

2.406459 |

2.538523 |

78.17795 |

|

2 |

0.114240 |

28.43313 |

4.814103 |

1.227740 |

65.52503 |

|

3 |

0.134438 |

31.23590 |

7.256592 |

1.034706 |

60.47280 |

|

4 |

0.150921 |

31.28080 |

8.598673 |

1.081985 |

59.03854 |

|

5 |

0.166737 |

31.16515 |

9.244270 |

1.061576 |

58.52901 |

|

6 |

0.181442 |

31.26687 |

9.704525 |

1.022530 |

58.00608 |

|

7 |

0.194859 |

31.35523 |

10.10137 |

1.004282 |

57.53912 |

|

8 |

0.207328 |

31.37526 |

10.42038 |

0.998561 |

57.20580 |

|

9 |

0.219110 |

31.37312 |

10.67020 |

0.994796 |

56.96188 |

|

10 |

0.230304 |

31.37147 |

10.87406 |

0.991453 |

56.76302 |

Granger Causality tests the directional relationship between the variables. The test emphasizes which variable causes the other variable. The directional relationship between the variables either may be one-sided or both sided. The results of Granger Causality are reflected in table-11. The results show that GDP and Personal Income Taxes Granger cause each other. Corporate Taxes Granger causes Personal Income Taxes however, the reverse is not true.

|

|

|

|

|

|

|

|

|

|

|

Null Hypothesis: |

Obs |

F-Statistic |

Prob. |

|

|

|

|

|

|

|

|

|

|

|

LNPIT does not Granger Cause LNGDP |

45 |

4.12882 |

0.0485 |

|

LNGDP does not Granger Cause LNPIT |

5.77121 |

0.0208 |

|

|

|

|

|

|

|

|

|

|

|

|

LNCT does not Granger Cause LNGDP |

45 |

0.40677 |

0.5271 |

|

LNGDP does not Granger Cause LNCT |

2.38837 |

0.1297 |

|

|

|

|

|

|

|

|

|

|

|

|

LNIDT does not Granger Cause LNGDP |

45 |

1.15073 |

0.2895 |

|

LNGDP does not Granger Cause LNIDT |

3.92745 |

0.0541 |

|

|

|

|

|

|

|

|

|

|

|

|

LNCT does not Granger Cause LNPIT |

45 |

5.31901 |

0.0261 |

|

LNPIT does not Granger Cause LNCT |

0.31198 |

0.5794 |

|

|

|

|

|

|

|

|

|

|

|

|

LNIDT does not Granger Cause LNPIT |

45 |

2.87974 |

0.0971 |

|

LNPIT does not Granger Cause LNIDT |

0.14262 |

0.7076 |

|

|

|

|

|

|

|

|

|

|

|

|

LNIDT does not Granger Cause LNCT |

45 |

0.93729 |

0.3385 |

|

LNCT does not Granger Cause LNIDT |

1.07678 |

0.3054 |

|

|

|

|

|

|

The study has identified a significant long-run positive relation between Indirect Taxes and Corporate Taxes to GDP in India while Personal Income Tax has a negative impact on GDP in the long run. In the short run, only Indirect Taxes has a positive impact on the GDP. Out of the three independent variables selected in the study, Personal Income Tax has a more negative impact on GDP as compared to Corporate Taxes and Indirect Taxes and this impact is bidirectional too. The findings of this paper are in line with the findings of Venkataraman and Urmi (2017) who showed Personal Income Taxes as having no impact, Corporate Taxes and customs duty as having a significant positive impact on the economic growth of India. Matallah & Matallah (2017) also asserted the negative impact of Direct Taxes and the positive impact of Indirect Taxes in the long run in Algeria. The same findings were also arrived at by Vazquez et al (2009), Dackehag & Hansson (2012) and Geetanjali & Venugopal (2017) regarding the negative impact of Direct Taxes on economic growth in the long run. Unnecessary complicacy into direct tax systems, higher marginal rates of personal taxes and weak enforcement were some of the issues that were resulting in a large number of taxpayers to either escape the tax laws or paying lesser taxes Chelliah, R. (2006). However contrary to Johansson et al (2008), the impact of Corporate Taxes has been found positive in the long run in India

To analyze the impact of tax structures in India on its economic growth, the study has examined the impacts of Personal Income Taxes, Corporate Taxes and Indirect Taxes in India from 1973-74 to 2018-19. The results highlight that Corporate Taxes and Indirect Taxes have positive impact while Personal Income Tax negative impact on economic growth of India in the long run. The results are in line with other studies conducted in different countries across the globe. The important structural changes in taxes domain include Goods and Services Tax which has been implemented since first July, 2017 and Direct Taxes code which is yet to be implemented. The real effects of these structural changes may be evaluated after some years when adequate data will be available for research. As conclusion, it is suggested to reduce slowly Personal Income Taxes by chronologically increasing Corporate Taxes and Indirect Taxes for overall economic growth of India

Acharya, S. (2005). Thirty Years of Tax Reform in India. Economic and Political Weekly, 40(20), 2061-2070. Ahmad, S., Sial, M. & Ahmad, N. (2018). Indirect Taxes and Economic Growth: An Empirical Analysis of Pakistan. Pakistan Journal of Applied Economics, 28(1) (65-81) Ashraf, N., Camerer, C. &Loewenstein, G. (2005). Adam Smith, Behavioral Economist. Journal of Economic Perspectives, 19(3), 1-15 Barro, R. J. (1991). Economic Growth in a Cross Section of Countries. The Quarterly Journal of Economics, 106(2), 407-443. Bazgan, R. (2018). The impact of direct and indirect taxes on economic growth: An empirical analysis related to Romania. Proceedings of the 12th International Conference on Business Excellence, 114-127, DOI: 10.2478/picbe-2018-0012. Caulkins, J., Kilmer, B., Kleiman, M., MacCoun, R., Midgette, G., Oglesby, P., Reuter, P. (2015). Taxation and Other Sources of Revenue. In Considering Marijuana Legalization: Insights for Vermont and Other Jurisdictions (pp. 75-100). Santa Monica, Calif.: RAND Corporation. Chang, W. (2006). Relative Wealth, Consumption Taxation, and Economic Growth. Journal of Economics, 88(2), 103-129. Chelliah, R. (2006). Reforming India’s Tax Base for Economic Development. In JHA R. (Ed.), The First Ten K R Narayanan Orations: Essays by Eminent Persons on the Rapidly Transforming Indian Economy (pp. 5-16). ANU Press. Retrieved from http://www.jstor.org/stable/j.ctt2jbknm.6 Clausing, K. A. (2016). The effect of profit shifting on the corporate tax base in the United States and beyond. National Tax Journal, 69 (4), 905–934 D. Stoilova& N. Patonov (2012). An Empirical Evidence for the Impact of Taxation on Economy Growth in the European Union, Book of Proceedings – Tourism and Management Studies International Conference Algarve. 3, 1031-1039 Dackehag, M. & Hansson, A. (2012). Taxation of Income and Economic Growth: An Empirical Analysis of 25 Rich OECD Countries. Working Paper 2012(6 Department of Economics, Lund University Engen, E., & Skinner, J. (1996). Taxation and Economic Growth. National Tax Journal, 49(4), 617-642. Ferede, E. &Dahlby, B. (2012). The impact of tax cuts on economic growth: evidence from the Canadian Provinces. National Tax Journal, 65 (3), 563–594 Fisher, S. (2010). The True Benjamin Franklin. [EBook #34193]. Accessed from https://www.varsitytutors.com/ebooks/earlyamerica/TrueBenjaminFranklin/TrueBenjaminFranklin.pdf Gale, G. W. &Samwick, A. A. (2014). Effects of Income Tax Changes on Economic Growth. Economic Studies at Brookings, The Brookings Institution. Geetanjali, J. &Venugopal, P. (2017). Impact of Direct Taxes on GDP: A Study. IOSR Journal of Business and Management, 21-27 Minister of Finance, Government of India (July, 5, 2019) Speech of NirmalaSitharaman, Budget 2019-2020. Retrieved from https://www.indiabudget.gov.in/doc/Budget_Speech.pdf Harrod, R. F. (1939). An Essay in Dynamic Theory. The Economic Journal, 49 (193), 14–33. Hodgson, H., &Sadiq, K. (2017). Gender equality and a rights-based approach to tax reform. In STEWART M. (Ed.), Tax, Social Policy and Gender: Rethinking equality and efficiency (pp. 99-130) Huňady, J. &Orviská, M. (2015). The non-linear effect of corporate taxes on economic growth. Timisoara Journal of Economics and Business, 8(1), 14-31 Iriqat, R. &Anabtawi, A. (2016). GDP and Tax Revenues-Causality Relationship in Developing Countries: Evidence from Palestine. International Journal of Economics and Finance, 8(4), 54-62 Johansen, Soren, and Katarina Juselius. 1990. Maximum likelihood estimation and inference on Cointegration with applications to the demand for money. Oxford Bulletin of Economics and Statistics 52: 169–210 Johansson, Åsa& Heady, Christopher & Arnold, Jens &Brys, Bert &Vartia, Laura. (2008). Taxation and Economic Growth. OECD, Economics Department, OECD Economics Department Working Papers. 10.1787/241216205486. Junge, J., & Levinson, D. (2012). Financing transportation with land value taxes: Effects on development intensity. Journal of Transport and Land Use, 5(1), 49-63. Kalaš, B., Mirović, V. &Andrašić, j. (2017). Estimating the impact of taxes on the economic growth in the United States. Economic themes. 55(4), 481-499 Kate, F. & Milionis, P (2019). Is capital taxation always harmful for economic growth? International Tax and Public Finance, 26, (4) 758–805 Kiss, Á. (2009). Minimum taxes and repeated tax competition. In Essays in Political Economy and International Public Finance (pp. 79-88). Frankfurt am Main: Peter Lang AG Kransdorff, M. (2010). Tax Incentives and Foreign Direct Investment in South Africa. Consilience, (3), 68-84 Lau, A., & Pearce, J. (2016). Salaries Tax. In Hong Kong Taxation: Law and Practice, 2016–17 Edition (pp. 55-198). Sha Tin, N.T., Hong Kong: Chinese University Press. Macek, R. (2014). The Impact of Taxation on Economic Growth: Case Study of OECD Countries. Review of Economic Perspectives. 14(4), 309-328 Martinez-Vazquez, Jorge &Vulovic, Violeta& Liu, Yongzheng. (2009). Direct versus Indirect Taxation: Trends, Theory and Economic Significance. International Studies Program, Andrew Young School of Policy Studies, Georgia State University, International Studies Program Working Paper Series, at AYSPS, GSU. Matallah, A., &Matallah, S. (2017). Does fiscal policy spur economic growth? Empirical evidence from Algeria. Theoretical and Applied Economics, 3(612), 125-146. McBride, W. (2012). What Is the Evidence on Taxes and Growth? Growth?., Tax Foundation Special Report No. 207, Washington, DC McNabb, K. (2016). Tax structures and economic growth: New evidence from the Government Revenue Dataset. WIDER Working Paper 2016/148: The United Nations University World Institute for Development Economics Research Myles, G. (2000). Taxation and Economic Growth. Fiscal Studies, 21(1), 141-168. Ogbonna, George &Odoemelam, Ndubuisi. (2015). Impact of Taxation on Economic Development of Nigeria: 2000-2013. Journal of Social and Policy Research Development. 9. 251-267. Ojong, C.M., Anthony, O. &Arikpo, O. F. (2016). The Impact of Tax Revenue on Economic Growth: Evidence from Nigeria. IOSR Journal of Economics and Finance, 7(1), 32-38 Padda, I. &Akram, N. (2009). The Impact of Tax Policies on Economic Growth: Evidence from South-Asian Economies. The Pakistan Development Review, 48 (4), 961–971 Passant, J. (2017). Tax, Inequality and Challenges for the Future. In LEVY R., O’BRIEN M., RICE S., RIDGE P., & THORNTON M. (Eds.), New Directions for Law in Australia: Essays in Contemporary Law Reform (pp. 49-58) Peters, George &Kiabel, Bariyima. (2015). Tax Incentives and Foreign Direct Investment in Nigeria. IOSR Journal of Economics and Finance (IOSR-JEF). 6. 2321-5933. 10.9790/5933-06511020. Poulson, B.W. & Kaplan, J. G. (2008). State Income Taxes and Economic Growth. Cato Journal, 28 (1), 53-71 Rao, M., & Rao, R. (2010). Tax System Reform in India. In Gordon R. (Ed.), Taxation in Developing Countries: Six Case Studies and Policy Implications (pp. 109-152). NEW YORK: Columbia University Press Scully, G. (2003). Optimal Taxation, Economic Growth and Income Inequality. Public Choice, 115(3/4), 299-312. Skinner, J. (1987). Taxation and output growth: Evidence from African countries. Working paper no. 2335, National Bureau of Economic Research, Cambridge Slemrod, J. (1990). Optimal Taxation and Optimal Tax Systems. The Journal of Economic Perspectives, 4(1), 157-178. Slemrod, J. (2018). Is This Tax Reform, or Just Confusion? The Journal of Economic Perspectives, 32(4), 73-96 Solow, R. (1956). A Contribution to the Theory of Economic Growth. The Quarterly Journal of Economics, 70(1), 65-94. Stoilova, D. (2017). Tax structure and economic growth: Evidence from the European Union. ContaduríayAdministración 62, 1041 1057 Tapşın, G. (2017).The effect of economic growth and direct taxes on tax burden in OECD Countries. European Journal of Business, Economics and A ccountancy,5(4), 44-52, Ullmann, Robert &Watrin, Christoph. (2008). Comparing Direct and Indirect Taxation: The Influence of Framing on Tax Compliance. European Journal of Comparative Economics. 5. 23-56. Venkataraman, S. &Urmi, A. (2017). The impact of taxation on economic growth in India: A disaggregated approach using the ARDL bounds test to co-integration. International Journal of Accounting and Economics Studies. 5(1). 19-21 Veronika, B. &Lenka, J. (2012). Taxation of Corporations and Their Impact on Economic Growth: The Case of EU Countries. Journal of Competitiveness, 4(4) 96-108