|

Prof Mrs P.SHEELA Professor, Dept of Finance Gitam Institute of Management GITAM (Deemed to be university), Visakhapatnam |

M.SUGUNA RESEARCH SCHOLAR Dept of Finance, Gitam Institute of Management GITAM (Deemed to be university), Visakhapatnam |

Varanasi Karthik MBA student in Finance Gitam Institute of Management GITAM (Deemed to be university), Visakhapatnam |

Today, one of the major issue that is haunting the Indian banking sector is Non Performing Assets (NPAs). With the rising NPAs the earning capacity and profitability of the banks are being highly affected. This paper compares the data of five selected Indian public and private sector banks and attempted to analyse and interpret how efficiently NPAs are managed over the period of 2010-2018. The findings were focused on performance and the management of NPAs point of view, through the study it was observed that the public sector banks are better performing, but coming to the management of NPAs the private sector banks are in better position. Finally, this study concludes with the findings and observations made from out of the analyses.

Keywords:NPAs, Gross NPAs, Net NPAs, Advances, Public and Private Sector Banks

The banking industry has undergone a sea of change after the first phase of economic liberalization in 1991, the top priority of the banks during those dayswas more towards performance such as opening wide networks/branches, supporting for the development of rural areas, lending to priority sector, enhancing employment generation, etc. While the primary function of banks stilled remained on extending loans to various sectors such as agriculture, industry, personal loans, housing loans etc.,due to which credit management, asset quality was not in list of priority in Indian banking sector. Over the period of time it was observed that the banks have tightened their lending process and have become more conscious while extending loans and also failed on realizing that lending carries a credit risk which resulted to the credit provided by the bank is not coming back and in turn was piling up as bad debts, referred to as Non-Performing Assets (NPAs). In the past few years the banking sector had been witnessing the rising NPAs. The regulatory bodies through the suggestions and recommendations have been initiating various measure to control this rising NPAs. All these efforts are not yielding the banking sector with relevant solutions. The pilling NPAs is impacting the profitability and it is also threatening the sustainability of the banks. The government has been coming forward with the technique of merging the banks so that it would be able to better monitor and control the growing NPAs. The impact of NPAs is being experienced by good number of banks across the country in the form of decreasing efficiency which in turn is reducing the profitability of such banks. NPAs has become a two edged sword has the banks are not able to receive income but at the same time it has to pay for it. In such a circumstances NPAs is not only reducing the banks earning capacity but is badly affecting their return on investment. Under this situation the researchers intended to carry out this study by comparing the NPAs of selected banks based on their performance to contribute to a dimension of the burning problem.

1. To examine and compare the NPA trends of the selected Public and Private Sector Banks 2. To compare the GNPA and NNPA percentage of advances of the selected Public and Private Sector Banks 3. To analyze the controlling trends of NPAs in the selected Public and Private Sector Banks 4. To suggest few strategies for better managing or controlling NPAs

There was considerable research that has been carried out through white papers, reports by different committees constituted by the Government agencies, adding to few thousands of research articles and expert opinions on NPAs. The researchers had the opportunities to review such research outcome with the objective on drawing this part of the study. Selvarajan & Vadivalagan (2013) in their research paper had analyzed that the growth of Indian Bank’s lending specially to Priority sector has been increasing. Indian Bank has been losing their control on NPAs when compared to the early years prior to economic reforms in India. They have suggested that banks in India should adopt strategies that could not only manage but also has to initiate news ways to recover the borrowed funds. Bhavani Prasad and Veera D (2011) their study on NPAs in Indian Banking sector had observed that PSBs accounted to more than 70% of total NPAs and this was mainly due to fall in the revenues from the traditional sources. Singh (2016), in his research concluded that banks needs adapt adequate and effective measures on fixing pre-sanctioned appraisal and post disbursement supervision system. Banks has to continuously monitor loans in order to identify loans that might become non- performing assets. Banks must be given proper powers to inspect and ensure effective utilization of borrowed funds. According to Sahoo (2013), until the banks are able to effectively manage their NPAs only than it would strengthen the process of financial inclusion and would be able to contribute more towards infrastructure development in the country. Jana and Thakur (2015) through their research had suggested three principles of safety, liquidity and profitability which is the three deciding factors which would control and manage the NPAs. Kumar (2015), through his study had concluded that Non-performing Assets (NPAs) today is becoming a concern and is causing huge problem for the Indian banking sector since several years. Mahajan (2014), in his research had opined that top management of private banks in India and foreign banks is more professional and is more competent in managing NPAs when compared with that of the public sector bank. Shalini, H S (2013)in her study had suggested the importance and need for scrutinizing the project proposal before the bank decides on the sanctioning loan to a prospective borrower. Kumar, P T (2013) through his study highlighted the significance on understanding quality of loan portfolio as it is very essential in evaluating the performance and the ways in which it would help in sustaining the operation of the bank. According to the researcher analysis it was expressed that high rate of NPAs would impact the overall performance and solvency of the bank. Mishra (2013) through his research had observed that in the public sector banks the level of gross NPAs and Net NPAs was quite shocking in India. Thus, suggested that the public sector banks need to manage their NPAs in a more careful manner from their operations, credit appraisal and lending process. According to the research carried out by Prof. Pharate S. R. it was observed that a large proportion of NPAs is by big time account holders and borrowers, than compared to the small borrowers, which is likely leading towards willful default. He also had expressed that since the legal system was very considerate and had a soft corner towards the borrowers and was neglecting the interest of banks, which needs to be reviewed. Chatterjee, Mukherjee and Das (2012)through their research had recommended that banks should analyze and scrutinize the genuineness of the borrowers on why they approach banks in seeking for loans and emphasized that the banks has to investigate the wealth and background of the guarantor who stands as a surety. Dr. Gurumoorty., B. Sudha.,(2012) through their research it was noted the PSBs are more effected by the three letter virus, the reason was that the PSBs were more focused towards fulfilling the social objectives rather than from the economic objectives as directed by their regulatory bodies. Prashanth k Reddy (2002) through his research had opined and suggested on how Indian banks can learn ways in better controlling NPAs from the banks operating across the globe.

Despite of recommendations made through various committee and experts, the various reforms that had been initiated by RBI this problem of NPA is rising and is further causing ill effects to the economy at large. Hence, the t study was an attempt to explore the issue from the point of GNPA and NNPA percentage of advances of the selected public and private sector banks a comparison.

Research design adopted in carrying out this study is descriptive in form since it deals with statistical data in order to compare banks performance in connection with NPAs. The sample consists of five Public sector banks such as – State Bank of India, Punjab National Bank, Canara bank, and Central Bank of India, Bank of Baroda and five Private sector Banks - ICICI Bank Ltd, Axis Bank Ltd, HDFC Bank, Kotak Mahindra Bank, and Yes bank. The data for the study was collected through the secondary sources from RBI website, websites of the banks for the period spread across 2011-2018. Data is presented with the help of Graphs, charts and tables etc.

It was used to for comparing the degree of variation from one data series to another, even if the means are drastically different from one another. The two data series which were taken into consideration for coefficient of variance was GNPA’s and advances of banks.

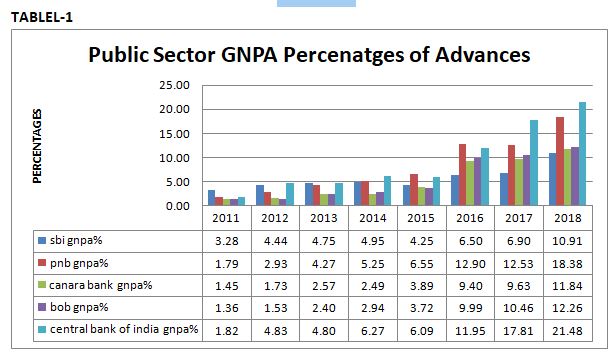

Table 1, it is observed that by the end of 2010-11, Gross NPAs to gross advances ratio of SBI Bank was 3.28 percent, and with gradual increase it stood at 10.91 percent by the end of 2017-18 and which is lowest when compared to other selected Banks in the public sector. In case of PNB, the Gross NPA ratio was 1.79 percent at the end of 2010-11 and it has increased to 18.38 percent by the end of 2017-18 and it being the highest. In the case of Canara Bank GNPA ratio was 1.45 percent by the end of 2010-2011 and it has increased to 11.84 percent in the year 2017-2018. In the case of Bank of Baroda GNPA ratio has increased from 1.36 percent to 12.26 percent during the period 2010-2011 to 2017-2018.It is observed from central bank of India gross NPA’s has raised from 1.82 percent to 21.48 percent 2010 to 2018. Which is highest among the selected banks in public sector. It is also observed that the GNPAs ratio has shown an increasing trend of banks over the period of study.

|

BANKS |

SBI |

PNB |

CANARA BANK |

BOB |

CENTRAL BANK OF INDIA |

|

MEAN |

5.75 |

8.08 |

5.375 |

5.58 |

9.38 |

|

SDV |

2.24214 |

5.478106 |

3.924124 |

4.222519 |

6.551798298 |

|

COV |

38.99 |

67.80 |

73.00 |

75.66 |

69.84 |

Table 1.1 it is well understood that out of selected five banks from the public sector, Canara bank with mean value 5.375 has controlled its NPA ratio, while comparing to other selected banks in the public sector. According to COV performance of SBI stands good among five public sector banks.

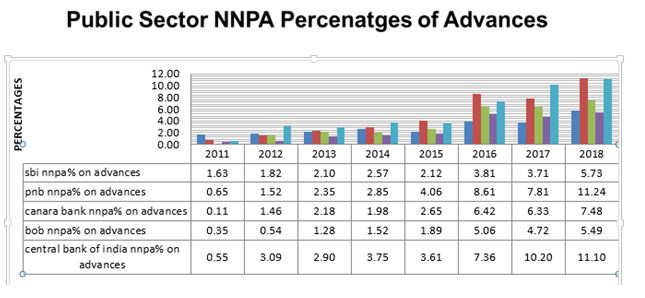

Through the table 2, it is very clear that Net NPA ratio had increased from 1.63 percent to 5.73 percent in case with SBI Bank, while in the case of PNB, it is very clear that this ratio had increased from 0.65 percent to 11.24 percent. Coming to the case of Canara Bank Net NPA’s ratio had risen from 0.11 to 7.48 percent. Whereas in the case of BOB, this ratio increased from 0.35 percent to 5.49 percent, in case of central bank of India, this ratio increased from 0.55 percent to 11.10 percent during 2010-2011 to 2017-2018. It is observed that the NNPAs ratio has shown an increasing trend in selected banks under Public Sector over the period

|

BANKS |

SBI |

PNB |

CANARA BANK |

BOB |

CENTRAL BANK OF INDIA |

|

MEAN |

2.94 |

4.89 |

3.58 |

2.60625 |

5.32 |

|

SDV |

1.30476 |

3.59381 |

2.568029 |

1.987989 |

3.541815 |

|

COV |

44.35 |

73.47 |

71.73 |

76.24 |

66.56 |

The table 2.1 it is very clear Bank of Baroda Mean value 2.60625 is least among selected public sector banks by which we can conclude that this bank has controlled their NNPAS most effectively comparing to that of other banks in the public sector. SBI has less COV 44.35 which shows that risk is less and performance is satisfactory when compared to other selected public sector banks.

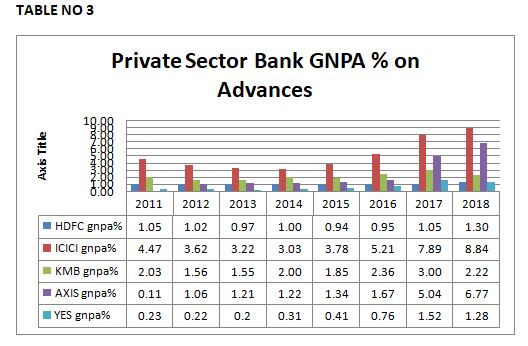

Table 3, it is very clear that by the end of 2010-11, GNPAs to gross advances ratio of ICICI bank was 4.47 percent while at the end of 2013-14, it had reduced to 3.03percent but by the end of 2017-2018 GNPA % had reached to 8.84 percent. Which is highest among all other private sector banks. GNPA ratio of HDFC bank was 1.05percent by the end of 2010-2011 while by the end of 2014-15, it came down 0.90 percent. With its effective strategies it is managing GNPA% at 1.30 percent. In case of AXIS bank, this ratio has increased from 0.11 percent by the end of 2010-11to 6.77 percent by the end of 2017-2018.Gross NPA ratio of kotak Mahindra bank was 2.03 by the end of 2010-2011 and it had very slight inclination of 2.22 percent by the year ending 2018. It is very obvious that the GNPA ratio of yes bank had increased from .23 percent to 1.28 percent by the end of 217-2018.

|

BANKS

|

HDFC BANK |

ICICI BANK |

KOTAK MAHINDRA BANK |

AXIS BANK |

YES BANK |

|

MEAN |

1.04 |

5.01 |

2.07 |

2.3025 |

0.61625 |

|

SDV |

0.107587 |

2.057436 |

0.441147 |

2.164923 |

0.486542329 |

|

COV |

10.34 |

41.07 |

21.31 |

94.02 |

78.9 |

From table 3.1, it is noticed that Yes bank mean value 0.61is the lowest among the selected banks in the private sector. It is clear that yes bank was able to control their gross NPA’s when compared to other banks in the private sector. The coefficient of variance of HDFC bank is 10.34, least among the banks in the private sector, which shows their risk is low and their performance is satisfactory while comparing with the other selected banks in the private sector.

Table 4, it is very clear that NNPA ratio of ICICI Bank is on a rise from 1.11 percent in 2010-11 to 4.77 percent in 2017-18.In case of HDFC Bank, this ratio had rose from 0.19 Percent in 2010-11 to 0.40 percent in 2017-2018, whereas in the case of AXIS Bank it had risen from 0.02 percent in 2010-2011 to 3.40 percent during the same period, while in the case KMB NNPA ratio has increased from 0.72 percent to 0.98 percent 2017-2018. It is observed from the case with YES bank NNPA ratio has shown an increasing trend when compared to the other banks in the selected private sector over the period.

|

BANKS |

HDFC |

ICICI BANK |

KOTAK MAHINDRA BANK |

AXIS BANK |

YES BANK |

|

MEAN |

0.26 |

2.19 |

0.91 |

0.96375 |

0.25 |

|

SDV |

0.071403344 |

1.632329624 |

0.22 |

1.097359758 |

0.28943911 |

|

COV |

27.46 |

78.10 |

24.17 |

113.50 |

115.6 |

Table 4.1, it is clear the mean value of yes bank is 0.25 which is least when compared to other banks in the private sector. It is now clear that among the banks in the selected private sector, Yes bank is able to control NPA’s efficiently than others. The coefficient of variance of HDFC bank is 27.46 which is least while comparing with that of other private banks in private sector. It shows that HDFC bank has low risk and their performance is satisfactory while comparing with the other banks in the private sector.

|

BANKS |

MEAN VALUE |

STANDARD DEVIATION |

COEFFICIENT OF VARIATION |

|

PUBLIC SECTOR BANKS |

3.52 |

1.42 |

0.40 |

|

PRIVATE SECTOR BANKS |

2.17 |

1.24 |

0.57 |

From the table 5 we can interpret the findings as follows: 1).According to mean value private sector banks have performed well in controlling NPAs in comparison to public sector banks. 2).But, According to coefficient of variation the performance of public sector banks is more efficient than private sector banks.

From the table5 it shows that the private sector banks (Mean=2.17) is less than public sector bank (Mean =3.52) which reflects the private sector banks performed well in controlling the NPAs when in comparison to public sector banks. From out of the five public sector banks selected for the study, the Canara bank (Mean = 5.35) has controlled its Gross NPA Ratio by using various policy measures when compared to other public sector banks. Out of the five private sector banks selected for the study, Yes bank (Mean =0.61) has controlled its GNPA Ratio well by adopting various other policy measures when compared to other private sector banks. So, the public sector banks needs to go a long way in adopting measures on reducing the NPAs. By considering the coefficient of variation, it can be said that the performance of public sector banks is more stable than private sector banks.

The NPAs have always been a problem for the banks in India. It is just not only problem for the banks but this impact the economy at large. The money locked up in NPAs do have a direct impact on profitability of the bank, since Indian banks are still highly dependent on income from interest from funds lent. This study shows that extent of NPA in the banks of public sector is still higher while comparing with that of the banks in the private sector. One reason could be the number of branches set up by the banks in the public sector is more, when compared to that of the banks in the private sector. Based on the regulatory norms the Banks in the public sector is compelled to expand into the rural areas, likewise the banks in the private sector have the flexibility is identifying the branches that needs to be setup in the urban or prime business localities. The customers’ base in the banks of private sector is comparatively less than when compared with the banks in the public sector, likewise the private sector bank has the flexibility in accepting or rejecting the loan request. More over the public sector banks has to follow the mandatory requirements has per the policy while lending and is to make sure that they have to cover the principles of social justice, social financing. Likewise the banks in the public sector has to follow the ratio of lending to the priority and non-priority sector. Even though various steps have been initiated taken by government in an attempt to reduce the NPAs but still there is a long way to go and a lot needs to be done to curb this problem. There is a need on reengineering of banking sector by adopting better diagnostics measures to identify wilful default. Changes should be made in the governance so that it clarifies role, purpose and business strategy of public sector banks. The problem of recovery is not from the small time borrowers but it lies with large borrowers and a strict policy should be evolved out of time in solving this problem. So the problem of NPAs needs lots of attention, if not very shortly these rising NPAs will keep killing the profitability of banks which affects the Indian economy’s growth prospects. It is very essential at this time that both the banks from the public as well as private sector has to give the top priority by ensuring that the enterprise, business or individuals who approaches for loans is a sound party with high integrity, credibility and good character and are capable of carrying forward their business with great responsibility. This can be referred to their past performance or referrals made to the banks. Banker must examine the balance sheet that shows the borrowers true colors and also helps on better analyzing their business status. Likewise, bankers must develop a strong monitoring strategy which helps them on understanding their business progress from time to time so that the purpose for which the loans have been granted is well realized. This initiative could be achieved through the use of technology. The banks have to associate with noted independent credit agency and seek their help in developing a customized credit appraisal system for their proposed projects before granting loan to aspiring borrowers. Likewise timely reports about the progress of the funded projects have to be collected in order to decide and suggest necessary advice.

B.Selvarajan & Dr. G. Vadivalagan. (2013). “A Study on Management of Non-Performing Assets in Priority Sector reference to Indian Bank and Public Sector Banks (PSBs)”,. Global Journal of Management and Business Research., Volume 13 Issue 1 Version 1.0 Banker’s hand book of NPA management,Hyderabad – Banambar Sahoo – Asia Law House. Prasad, G.V.B. & Veena, D. (2011).“NPAs Reduction Strategies for Commercial Banks in India”,. IJMBS Vol. 1, Issue 3 Vivek Rajbahadur Singh.(2016).“A Study of Non-Performing Assets of Commercial Banks and it’s recovery in India”,. Annual Research Journal of SCMS, Pune, Vol. 4, March 2016 Sahoo, Banambar (2015).“Non- Performing Assets in Indian Banks: its causes, consequence and cures”,. The Management Accountant.Vol.50. no.1.Jan.2015. Kumar, P T (2013). “A comparative study of NPA of old private sector banks and foreign banks”,. Research journal of Management Sciences, ISSN 2319-1171 vol.2 (7),38-40. Mahajan, Dr Poonam (2014).“Non-Performing Assets: A study of public, private & foreign banks in India”,. Pacific Business Review International. Vol 7 issue 1, 2014. Shalini, H S (2013).“A Study on causes and remedies for non-performing assets in Indian public sector banks with special reference to agricultural development branch, State bank of Mysore”,. International Journal of Business and Management Invention, Vol. 2 Issue 1, pp 26-38. Chatterjee,C. and Mukherjee J. and Das, R.(2012).“Management of Non-performing Assets – A current scenario”,. International Journal of Social Science & Interdisciplinary Research. Vol. 1 Issue 11. Chaudhary, K. & Sharma, M. (2011).“Performance of Indian Public Sector Banks and Private Sector Banks: A Comparative Study”,. International Journal of Innovation, Management and Technology, Vol. 2, No. 3 Kaur, K. & Singh, B. (2011). “Non-performing assets of public and private sector banks (a comparative study)”,. South Asian Journal of Marketing and Management Research, Vol. 1, Issue 3 Rai, K. (2012).“Study on performance of NPAs of Indian commercial banks”,. Asian Journal of Research in Banking and finance, Vol. 2, Issue 12 Khanna, P. (2012).“Managing nonperforming assets in commercial banks”,. Gian Jyoti E-Journal, Volume 1, Issue 3 (Apr – Jun 2012) ISSN 2250-348X Mohamed M. Sheik, Adul Kader M. Mohiadeen and Anisa H. (2012). “Relationship among organizational Commitment, Trust and job satisfaction: An Empirical Study in Banking Industry”,. Res, J. Management Sci., 1(2), 1-7 Dr. D. Ganesan R.Santhanakrishnan (2013). “Non-Performing Assets: A Study of State Bank of India”,. Asia Pacific Journal of Research, Volume: I, Issue: X,. Mishra, A.K. (2013).“Trends of non-performing assets (NPA) in public sector banks in India during 1993–2012”,.International Journal of Research in Commerce & Management, Vol. 4, No. 11,pp.111–114. D.Jayakoddi and Dr.P.Rengarajan,(2016).“A Study on Non- performing Assets of selected public and private sector banks in India”,.Intercontinental Journal of Finance Research Review ISSN: 2321-0354 - Online ISSN: 2347-1654 - Print – Impact of Factor: 1.552 VOLUME 4, ISSUE 9,. Vaibhavi Shah and Sunil Sharma, (2016). “A Comparative Study of NPA in ICICI Bank and HDFC Bank”,. Avinava national Monthly Referred Journal of Research in Commerce and Management. Vol.5, Issue 2.. Dr. Biswanath Sukul, (2017). “Non-Performing Assets (NPAs): A Comparative Analysis of Selected Private Sector Banks”,. International Journal of Humanities and Social Science Invention ISSN (Online): 2319 – 7722, ISSN (Print): 2319 – 7714 www.ijhssi.org ||Volume 6 Issue 1. *****