|

Surbhi Junior Research Fellow Department of Management, DAV University Jalandhar, Punjab, India |

Sandeep Vij Associate Professor, Department of Management, DAV University, Jalandhar, Punjab |

Holcim and Lafarge merged on 7th April 2014, to form a cement giant which dominated the cement industry worldwide with its presence in 90 countries owning 168 plants and having 386 million tons per annum of cement producing capacity. The deal was struck by swapping 9 Holcim shares for 10 Lafarge shares. The aim of the merged entity was to be on top in the global cement industry which they did achieve by this merger. The merger made it easy for the company to get the finances, reduced their CAPEX, improved their credit rating and got the company synergies worth millions and billions. However, the deal drew the regulatory scrutiny of competition watchdogs in about fifteen different countries; and were asked to divest from many of their plants in different nations so as to convince the regulators that their combined market concentration will not reduce the competition. Their reduced post-merger profits further created challenges for the company to stay in the top position that they gained after the merger. A series of delays and regulatory challenges that LafargeHolcim group had to face during the implementation of the merger deal were strategically used by the merged entity to become a leading cement company in the global market. Will they be able to come out of the chaos they were in after this merger and be able to maintain the top position?

Keywords: Cement Industry, Mergers and Acquisitions, Divestment, Non-Market Strategy, Legal ChallengesOn April 7, 2014, Holcim (a Switzerland based global building materials and aggregates company) and Lafarge (a French industrial company specializing in cement, construction aggregates and concrete) agreed to terms on a “merger of equals” with a swap ratio of 9 Holcim shares for 10 Lafarge shares. The merger of these cement giants was built upon the strengths and identities of the companies, which was likely to help them to deliver better results to their stakeholders. Lafarge and Holcim finally merged to form Lafarge Holcim in July 2015 and created a mammoth multinational cement producing company. With its presence in 90 countries, owning 164 cement plants, controlling around 386 million tons per annum (MTPA) of cement production capacity, Lafarge Holcim became largest cement producer worldwide (see Exhibit 1). But the deal drew the regulatory scrutiny of competition watchdogs in about fifteen different countries (Jolly, 2014). Thereby, forcing the merged entity to shed many of their plants so as to convince the regulators that their combined market concentration will not reduce the competition. The marriage of Lafarge and Holcim posed some interesting questions like, how will the deal benefit both the parties? What synergies will accrue to the joint entity? Why did it take almost a year for the deal to materialize? How did Lafarge Holcim sail the legal challenges emerging out of the deal?

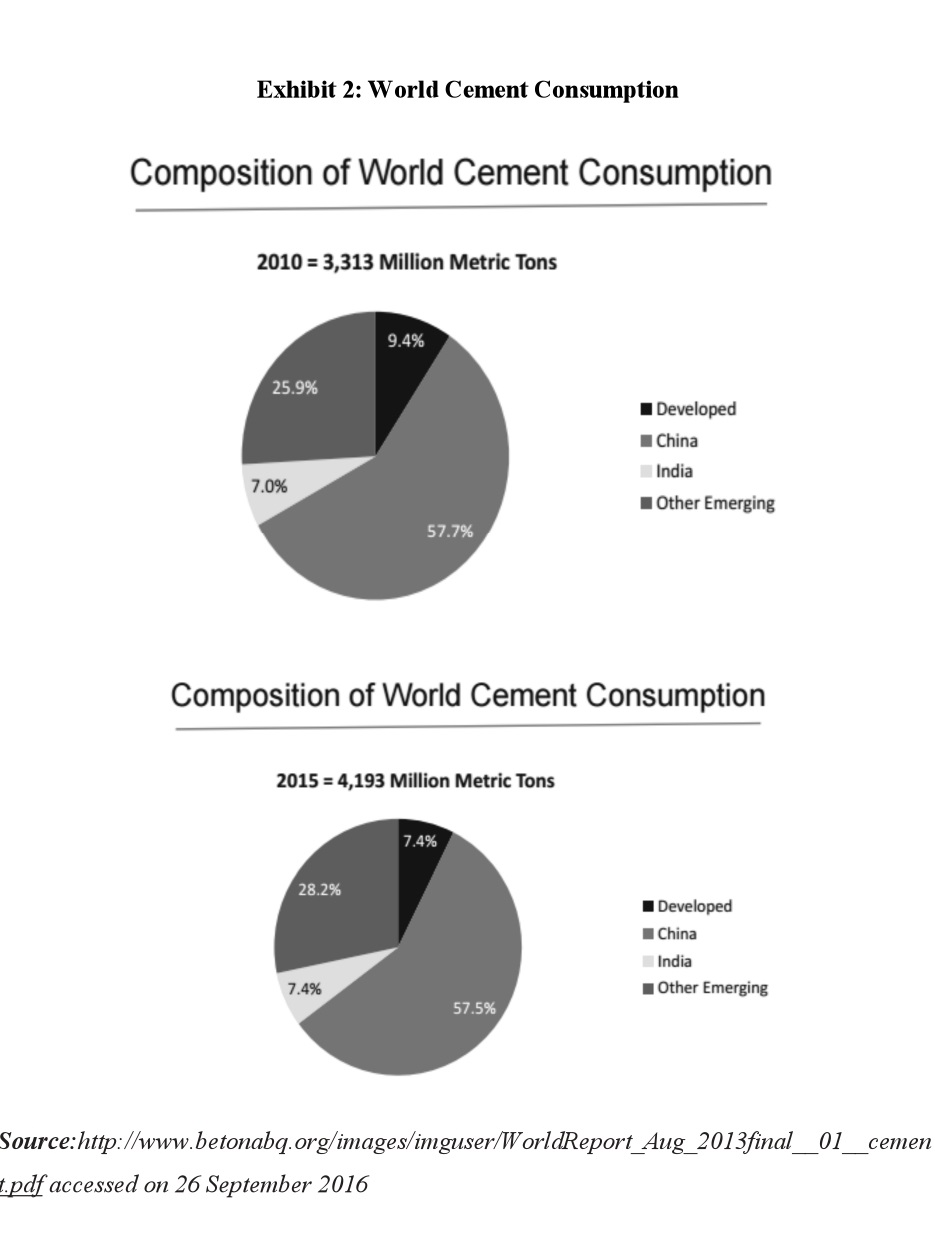

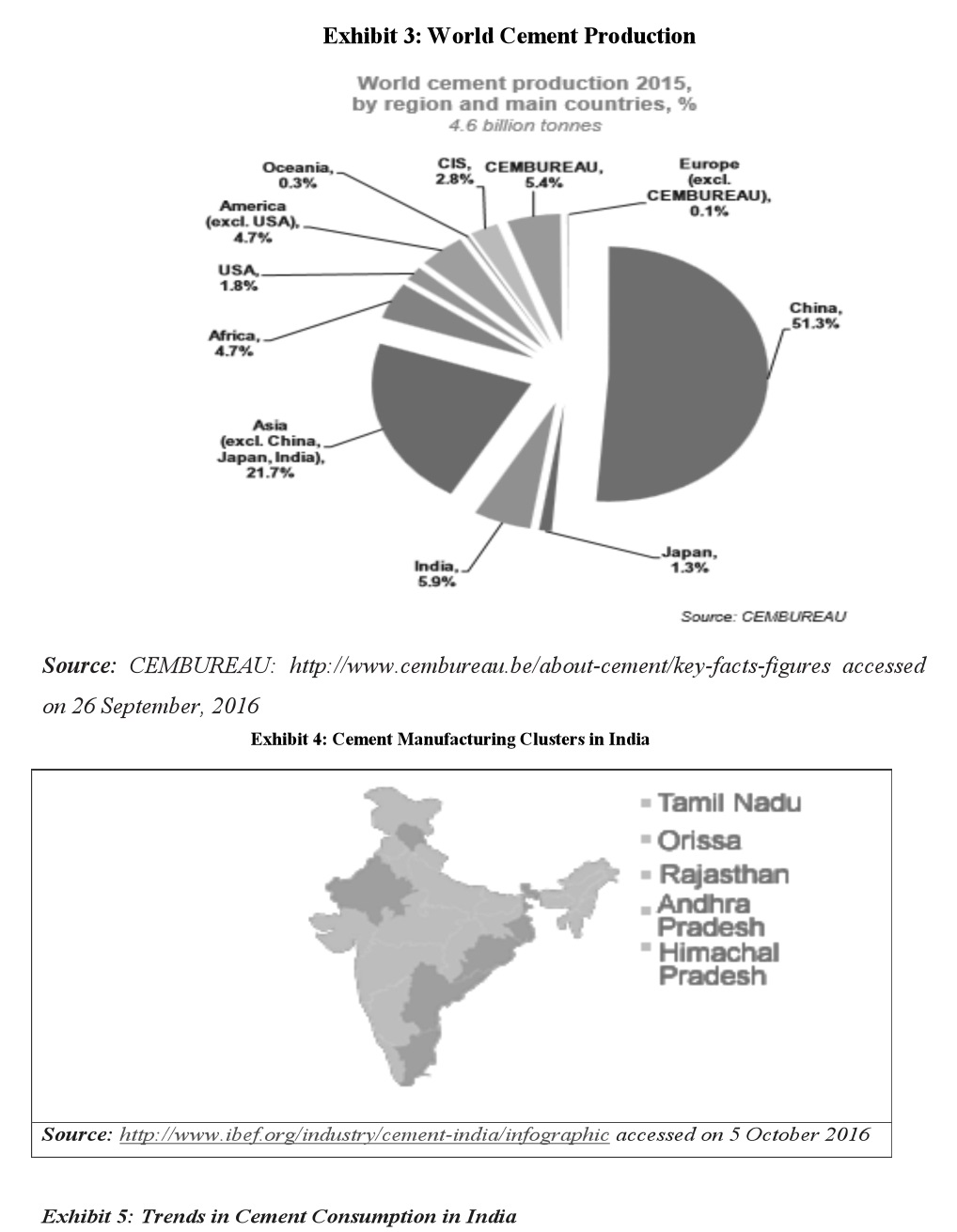

Cement plays a necessary role in economic development of any country. Global cement production had continued to expand at an average rate of 7.07% during 2008 to 2013. World sales of cement were predicted to expand more than 5% per annum during 2017. Globally, many markets witnessed significant consolidation. After the removal of government controls from the cement industry in 1989, in India, the growth rate of capacity addition in the cement industry increased. Due to the increased production but lack of simultaneous demand, companies had to struggle to survive because of the excess capacity. Entry of foreign players resulted in the consolidation of the fragmented industry. Though the industry saw consolidation by domestic players starting in the mid-1990s, it was only in the late 1990s that foreign players entered the market. Holcim entered India by investing in Kalyanpur Cements in 1990 and Lafarge commenced its Indian operations by acquiring Tisco’s cement plants in 1999. The Indian Cement industry had achieved a 2nd position in the world after China (see Exhibit 2 and Exhibit 3). With nearly 390 million tons of cement production capacity in 2015, India was the second largest cement producer in the world. By Financial Year 2025, cement production has been predicted to reach to 550 million tons per annum. Of the total, 98 percent of the capacity lies with the private sector and rest, with the public sector. 70 percent of the total production capacity lies with the top 20 companies. And in terms of plant size, 188 large cement plants account for 97 percent of the total installed capacity, while 365 small plants account for the rest. Cement industry in India was concentrated in the states of Andhra Pradesh, Rajasthan and Tamil Nadu with 77 plants. (see Exhibit 4). A forecast about global cement industry was that it will grow at a steady CAGR of more than 9% by 2020. The purchasing capacity of people in emerging markets, such as India and China, had been increasing considerably. This increase in the purchasing capacity of the populace coupled with a rise in urban population had augmented demand for a number of residential projects worldwide. The increase in the number of residential construction projects will drive the global construction industry, which in turn will spur the demand for cement during the forecast period (see Exhibit 5). It had been observed by the analysts that a number of countries were currently witnessing the large-scale migration of the populace from rural areas to urban areas. To meet the needs of such a large-scale migration, countries across the globe were focusing on infrastructure development. This change in the focus towards infrastructure development will bolster cement sales, which in turn will drive market growth during the estimated period.

Holderbank started its operations by opening a cement plant in 1912. Later in 1920’s the company started expanding in other European countries and in Egypt, Lebanon, and South Africa. In 1942, Holderbank opened a research lab by the name of Technical Centre Holderbank. In 1960’s after its entry into the Canadian market, a large cement production facility was opened in Michigan (USA). Almost simultaneously, it invested in a small plant near Sao Paulo (Brazil). During the period 1962 – 1991 Holderbank also started expanding its operations to Latin America. In 1974, Holderbank for the very first time entered Asia through the Philippines. Later, Holderbank started exploring new markets by entering Spain in 1980 and Eastern Europe, China, India and Southeast Asia in the 1990s. In 2001 Holderbank changed its name to Holcim by a vote at the annual general meeting. In 2005, Holcim entered into a strategic alliance with Gujarat Ambuja Cements by making a public purchase offer to the shareholders of the Associated Cement Companies (ACC) and Ambuja Cement Eastern. In the same year, Holcim acquired Aggregate Industries, thus entering the UK market and strengthening its aggregates and ready-mix concrete businesses in North America. In 2009, Holcim expanded its Australian business through the acquisition of Cemex Australia, now Holcim Australia, a company with countrywide operations in the aggregates, ready-mix concrete and concrete products business. This acquisition enabled Holcim to include Australia in its strategy of expanding its aggregates and ready-mix concrete business in mature markets (see Exhibit 6). Holcim was a global leader in the manufacturing and distribution of cement and aggregates (crushed stone, gravel, and sand), as well as other activities, including ready-mix concrete, asphalt, and associated services. The company had majority and minority shareholdings in some 70 countries and on every continent. In 2014, Holcim recorded net sales of over $21.58 billion.

The Lafarge started its operations in 1833, in Le Teil (Ardèche, France) when Joseph-Auguste Pavin de Lafarge began regular extraction operations in the limestone quarries. Through consistent growth and numerous acquisitions, Lafarge became France’s largest cement producer by the late 30’s. Lafarge’s first step to international expansion took place in 1864 when it got a project for the construction of Suez Canal. Following its success with the cement business, Lafarge opened a research laboratory near Le Teil, France in 1887 which was the world’s first laboratory to specialize in cement. During the period following the 1950s to 1970s, Lafarge established itself in United States, Canada, and Brazil, through plant construction and acquisition of firms. During the 1980s and 1990s, Lafarge expanded itself in Sub-Saharan, East Africa, China, India, and South Korea. In 2008, Lafarge acquired Orascom Cement which was of one its significant acquisitions. Orascom was a leading cement company in many of the key markets including Middle East, Mediterranean Basin, Egypt, Algeria, United Arab Emirates, and Iraq. In 2014, Lafarge employed 63,000 people in 61 countries and recorded sales of $17.66 billion. As a leading player in cement, aggregates and concrete businesses, Lafarge offered innovative solutions for the constructing of compact, durable and beautiful buildings around the world. With its own research facilities, Lafarge contributed to sustainable construction as well as architectural creativity. (see Exhibit 7).

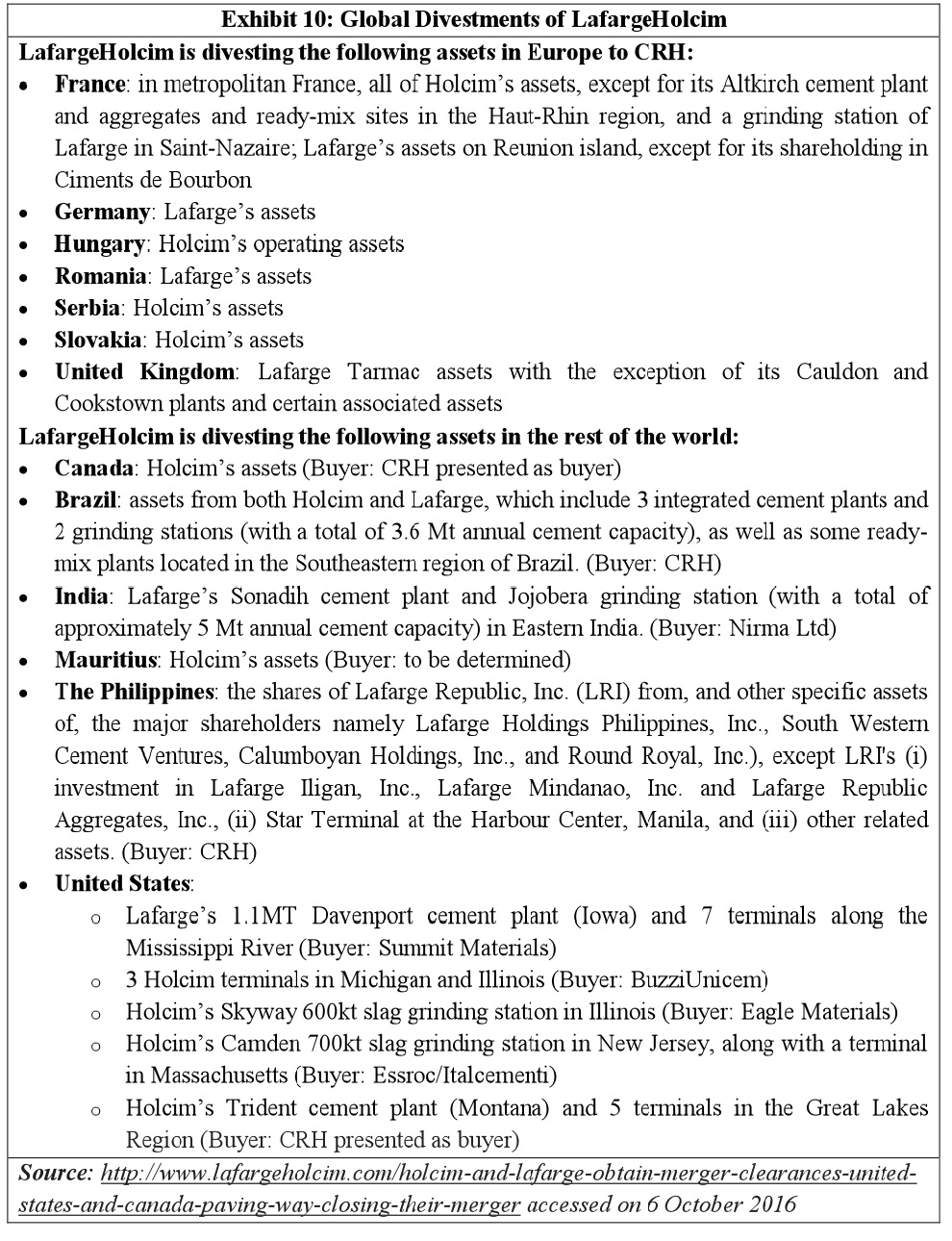

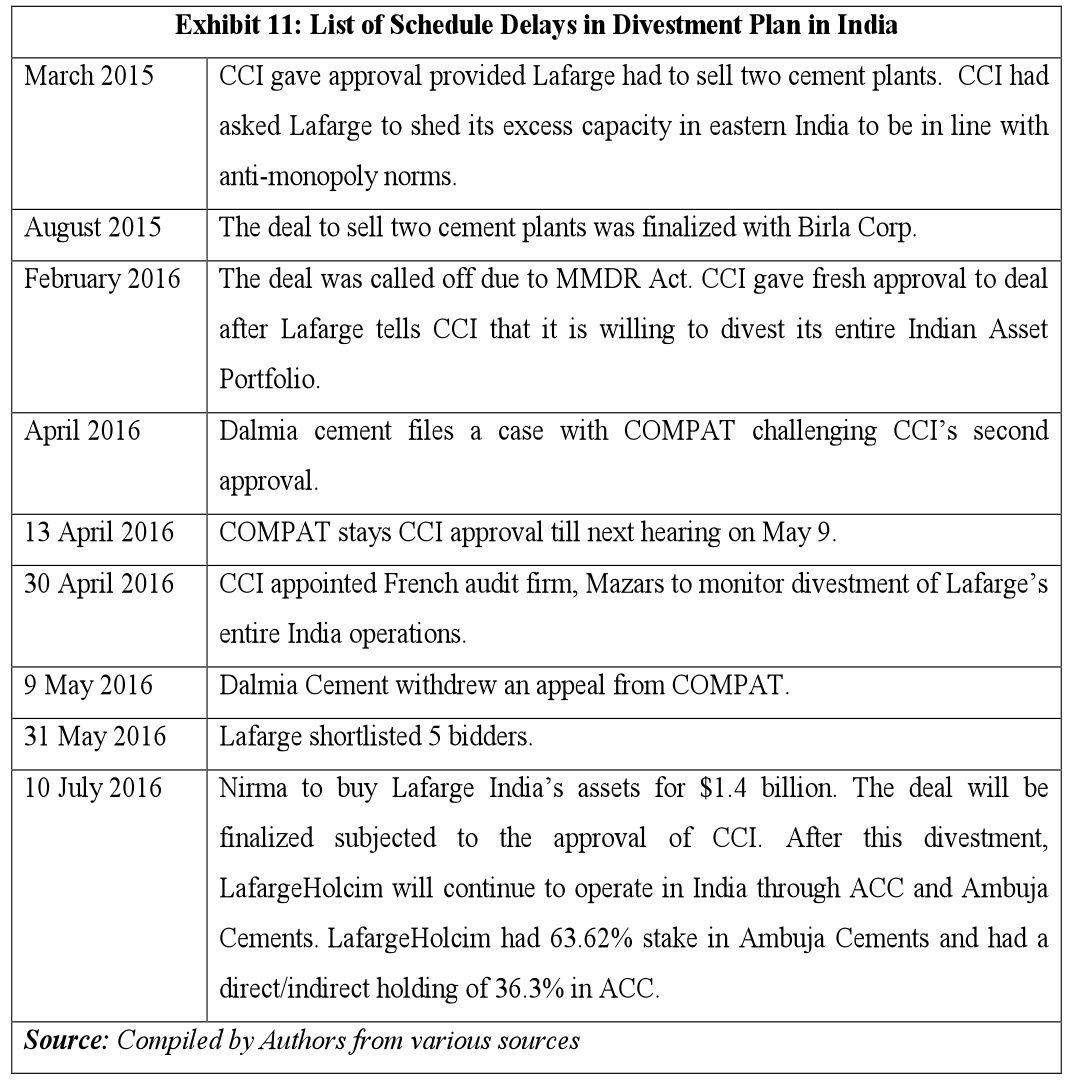

In 2014, Holcim announced its merger project which gave birth to Lafarge Holcim, the new leader of the building materials industry. The proposed deal took almost more than a year and was finalized in 2015. Lafarge and Holcim were merged on the belief that, being counterparts in terms of their product portfolio and their identical cultures would make it easy for them to integrate and benefits of this friendship could be transferred to their customers, employees, and shareholders. Emerging markets like India had witnessed increasing consolidation with big players taking over the small players. With this merger of equals, Lafarge Holcim became largest cement producer in the building materials industry with control of around 386 MTPA of cement production capacity, having a presence in 90 countries and owning 164 cement plants worldwide. The merger was an all-share deal with a swap ratio of 9 Holcim shares for 10 Lafarge shares. Company domiciled in Switzerland had its share listed on SIX Swiss Exchange (Zurich) and Euronext (Paris). As a result of the merger, the company got operational synergies worth $1.38 billion, financial and cash flow synergies worth $552 million and additional working capital savings of $565.8 million (see Exhibit 8). Both Lafarge and Holcim used debt as one of their main pillar of support to expand in emerging markets, where widespread urbanization made the requirement of building materials a necessity. But because of housing bubble burst in the U.S. in 2008, Europe sank into a sovereign debt crisis, and this demand for building materials collapsed. Lafarge further suffered when its investment of $12 billion in Orascom Cement (in 2008) of Egypt faced a setback due to the unrest caused by Arab Spring in the country. Situations worsened when the yearning of power-hungry cement plants could not be fulfilled because of simultaneous hike in the energy prices and cement plants started running at a loss or well below their capacity (Huet and Baghdjian, 2014). The motive of the merger was to help Lafarge in getting finance at a lower cost taking advantage of the better credit rating of Holcim of Baa2 by Moody’s. Because Lafarge’s, debt received a "junk" ratings from Standard & Poor's and Moody. Lafarge’s wanted to reclaim its investment grade rating through this merger. Further, the companies wanted to cut off their cost, debt and to bear up the escalating energy prices and weaker demand that affected the sector since the 2008 economic crisis. Product market of Lafarge Holcim also got the benefit of diversification. Lafarge had a strong presence in Africa and the Middle East, while Holcim was strong in Latin America (see Exhibit 9). Lafarge Holcim got the benefit from the long-term growth potential of emerging countries as well as a cyclical recovery in developed economies. Lafarge Holcim was positioned very strongly in the cement industry, based on a low-cost advantage and high barriers to entry. These competitive advantages stem from the low value/weight ratio of cement and the difficulty in obtaining permits for cement plants. In addition, analysts believed that Lafarge Holcim’s emerging markets footprint will support its competitive position. Cement had low value relative to its weight, which creates local markets rather than global markets, as high shipping costs relative to the value of the materials creates a low-cost advantage for local producers and high barriers to entry for outside competitors. The additional costs make it unlikely that imports will enter the local market, except in periods of excess demand. This advantage was further supported by high barriers to entry. Permits for new quarries and cement plants were difficult to obtain. Local opposition from residents and regulations make it difficult to build new facilities close to populated areas, which were the primary sources of strong demand. Asia-Pacific was a key segment for Lafarge Holcim, with India representing one of its largest footprints in the region. Its presence in India comes from its 61% ownership stake in Ambuja Cement, one of the two largest cement companies in the country. Lafarge Holcim’s Indian assets were particularly moat-worthy. In addition to the competitive advantages, any new entrant to the Indian cement industry faces significant hurdles. This includes government land approvals, limestone reserve linkages, coal supply linkages for captive power, and the costs of building a distribution network.

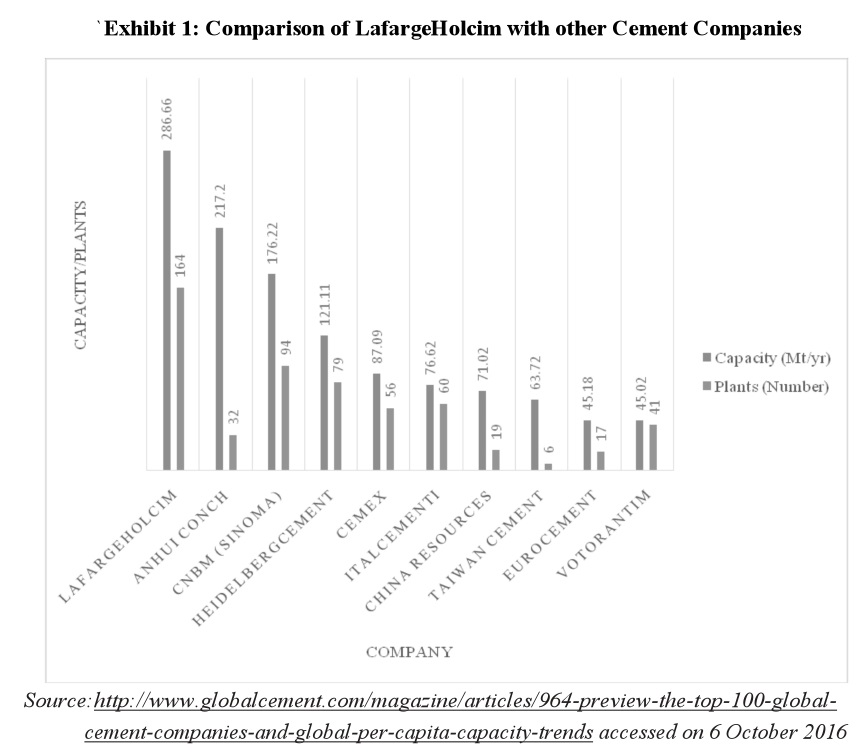

After the merger, Lafarge Holcim had to adjust to the challenging conditions in important markets like China and India. The merged entity missed its third-quarter sales and earnings expectations in 2015, after the merger. Following the same, it decided to review its portfolio. The stronger Swiss franc and lower prices weighed on its first results since its creation. LafargeHolcim reported an 8.7% drop in its sales after three months since its merger, Mr. Olsen CEO of Lafarge Holcim said that they were willing to exit the entire country, where the market conditions were weak. The results were not considered satisfactory by the company and they attributed this to a slowdown in China. Because of the high production capacity for cement in the country, the weaker demand meant, fall in prices. The company expected same conditions in some of its biggest markets, which include Brazil, France, and India, to remain “challenging” (Revill, 2015). To come out of these conditions Lafarge Holcim had a divestment target of $3.6 billion in 2016. Mr. Olsen said, “We have a position of number 1, 2 or 3 in 70% of our markets. Where we don’t have that position we are looking at divesting or swapping assets” (Revill, 2015). Construction activity was the single most important driver of earnings power for the company. Given the high fixed costs of cement production and that over 80% of operating EBITDA came from cement sales, downturns in construction demand posed a significant risk to LafargeHolcim’s earnings. Some key operating costs were largely beyond the company’s control. Rising energy costs were a threat to margins. Kilns required significant energy to reach the extremely high temperatures necessary for cement production. Additionally, cement production was fairly pollutive and new requirements for emissions control technologies at kilns could add additional costs for the company. Given its global footprint, LafargeHolcim also faced material currency risk. The company earned revenue in local currencies, although debt was denominated in a number of currencies, including Swiss francs, U.S. Dollars, Euros, and British pounds. Any depreciation in local currencies relative to the currencies of its debt could have a significant effect on the company’s ability to service its debt. In particular, depreciation of the Indian rupee could have a significant impact. The company also faced execution risk on the integration of assets from the completed merger of Lafarge and Holcim. Given the large scale of the two companies, integration was complicated and costly. Getting the synergies from the deal was not at all a cake walk for the merged entity. To make LafargeHolcim merger a success these two entities had to get anti-trust approvals from 17 jurisdictions including from the European Commission. In this context, operations in Europe, U.S, Brazil, Canada, India, Philippines and Mauritius had to be divested to give confidence to the regulators that their dominant position would not hamper competition (see Exhibit 10). LafargeHolcim reported in its annual report that it had a cement market share of 40 percent in the U.K., 34 percent in France, 33 percent in Canada, 12 percent in the United States and more than 30 percent in several east European and African countries (Huet and Baghdjian, 2014). As a remedy for the merger of the Group’s Legacy companies, it had $3.6 billion divestment target for the year 2016. Divestment decision of Lafarge Holcim in India took almost a year to materialize because of the legal issues in India. Competition Commission of India (CCI) imposed a stay on the merger until and unless Lafarge Holcim would divest some of their plants in the country. The deal, if allowed to materialize without divestment, would have created the dominance of the company in eastern India. Holcim's ACC and Gujarat Ambuja had 10.7 MTPA capacity while Lafarge had 7.8 MTPA. The combined capacity of the merged company would have resulted in 18.5 MTPA which would have been almost 40 percent of the region's 46 million tons capacity (Gangal, 2016). Initially, CCI gave approval to the merger deal of Lafarge Holcim in India on a condition that LafargeHolcim will have to sell off their two cement plants to avoid creation of a monopoly in eastern India. This deal to sell Lafarge India’s Jojobera and Sonadih plants in eastern India, valued at $895.2 million, was finalized with Birla Corporation. But the deal could not be materialized due to the provisions of Mines and Minerals (Development and Regulation) Act (Patel, 2016). According to MMDR Act, Birla’s would get the cement plants but not the mining rights to the limestone mines attached to it. This made the Birla’s to walk away from the deal. LafargeHolcim submitted a revised proposal to CCI that they were willing to divest their entire Indian asset portfolio across Rajasthan, Haryana, Chhattisgarh, Jharkhand and West Bengal, to which CCI willingly gave approval. There came a new turn in the story, when Dalmia cement filed a case with Competition Appellate Tribunal (COMPAT), challenging the CCI’s second approval on the plea that it was out of the powers of CCI to pass a fresh order when its initial order had not been complied with and also that CCI should know and disclose the acquirer for LafargeHolcim assets to avoid a situation where a couple of players could come and dominate the Indian cement market. This appeal was duly heard by COMPAT and CCI’s order of giving approval to the decision of LafargeHolcim to sell their entire Indian assets was stayed. Later CCI appointed a French audit firm, Mazars, to monitor the divestment process of LafargeHolcim to ensure that the competition in Indian cement market is not affected by the deal and all regulations under the Competition Act, 2002 were duly complied with (Arora, 2016). Meanwhile, Rajya Sabha, through an amendment to MMDR Act, allowed companies to transfer captive mining leases issued prior to January 2016. This amendment came with a condition of bearing the transfer fees by the acquirer thus meaning a higher cost of acquisition. A few days later Dalmia cement withdrew their appeal from COMPAT saying that they have no interest left in acquiring assets of LafargeHolcim as there was no commercial prudence in acquiring their cement plants. Then Lafarge shortlisted 5 bidders including Mexico’s CEMEX, China’s Anhui Conch Cement, JSW Cement, Piramal Enterprises and the Nirma Group. Of these, CEMEX and Anhui were overseas cement players that did not have a presence in India so far while Piramal and Nirma currently didn't have any presence in the cement sector (Chaki, 2016). Finally, on 10th July 2016, a deal to buy Lafarge India’s assets was finalized with Nirma Ltd. for $1.4 billion, which deal was yet to be approved by CCI LafargeHolcim had to tide over similar regulatory challenges in many countries of the world (Pillay, 2016). However, the company took it as an opportunity to sell off its loss-making and less attractive assets across the world and improve its credit rating (see Exhibit 11). Eric Olsen, CEO LafargeHolcim said, “With the recent divestments announced in India, Sri Lanka, China, and Vietnam, we have exceeded our CHF 3.5 billion commitment for the whole of 2016 in a little over seven months. These transactions, all secured at good conditions, also help us to streamline and simplify our operations and allow us to maximize synergies in countries like Morocco, China, and India. Following the successful execution of our divestment program to date, we are extending the program to CHF 5 billion. We expect to complete the remainder of this by the end of 2017.” By achieving their divestment target of $3.6 billion the company contributed towards its target to reduce net debt to around $13.39 billion by the end of 2016 and also extended its divestment program to $5.15 billion, which was expected to be completed by the end of 2017. Divestments helped to generate cash and simultaneously the reducing CAPEX, significantly strengthened the credit ratios of the company and the company was able to return excess cash to shareholders through share buybacks or special dividends and that too with a solid investment grade credit rating. In September 2016, LafargeHolcim decided to lay off 250 jobs as part of its global operations reorganization strategy. This would include laying off 130 jobs in Switzerland, 80 in France, and the remainder in other global sites around the world. This represents around 0.25% of LafargeHolcim’s 100,000 staff. The company wanted to free up the resources which could be further used to strengthen their position in the strategic markets. The merger had presented more challenges to the group than expected. Apart from regulatory challenges, LafargeHolcim had to face cut-throat competition from some of the top players in cement industry including Anhui Conch and CNBM from China, HeidelbergCement from Germany, and CEMEX from Mexico. Though Anhui Conch had only 34 production sites as compared to 164 of LafargeHolcim, yet the difference in their production capacity was not as large as the difference in their number of plants. Though LafargeHolcim was present in 90 countries and Anhui Conch only in 4, Anhui Conch was placed at a better position in terms of its net debt, return on Investment, and average capacity per plant (see Exhibit 12) (Schneider,2016). LafargeHolcim had got the benefit of geographical diversification and its competitor Anhui Conch had got the competitive edge in centralized procurement and economies of scale. China National Building Materials (CNBM) was the third-largest cement producer in 2015, with 94 cement plants and 176.22 MTPA of cement production capacity. CNBN, another competitor of LafargeHolcim had continually pursued low carbon production and management and had created a green industry in order to be a responsible corporate citizen. Whereas, on 18th October 2016, LafargeHolcim was fined Euro 270,000 to pay as compensation to farmers, in Zasavje region, who presented measurements showing that permitted emission had been exceeded 10-fold and in some cases, 100-fold, damaging their lands, orchards, forests and declining their yields. HeidelbergCement bagged the fourth rank in the list of cement companies in 2015, with 121.11 MTPA cement production capacity from 79 cement plants. HeidelbergCement believed in concrete results. The company produced more than 100 million tons of cement, clinker and concrete annually. It was also the largest cement producing company in Germany. Cement, concrete, and aggregates together accounted for nearly 90% of the company's sales. CEMEX, the building materials company had 56 cement plants with an annual production capacity of about 95 MTPA. Most of the company’s sales can be accrued to its cement business. It also produces, markets, and distributes ready-mix concrete, aggregates, and clinker. CEMEX had its operations in North America, Africa, Asia, Europe, the Middle East, and South America. The US, Mexico, and Europe accounted for more than 70% of its revenues.

The merger of the two cement giants Lafarge and Holcim was expected to bring laurels to both the companies but faced quite a tough time of legal interventions and their profits plunging down. Will they be able to cope up with the tough times and be able to maintain the position of being at the top in the cement industry?

1. What were the strategic reasons behind Lafarge and Holcim merger?

2. What were the reasons for post-merger integration delay in execution/implementation of the merger deal between Lafarge and Holcim?

3. Do you see a strategic move in divestment decision by LafargeHolcim or it was merely a legal compulsion?

4. What concerns or risks do you foresee that any post-merger integration program should aim to mitigate?

5. What is non-market Strategy? Identify how was non-market strategy pursued in this case?

Arora, R. (2016, April 30). CCI appoints French audit firm Mazars to monitor asset sale process of Lafarge India. The Economic Times, Retrieved 14 September 2016, from www.economictimes.indiatimes.com/industry/indl-goods/svs/cement/cci-appoints-french-audit-firm-mazars-to-monitor-asset-sale-process-of-lafarge-india/articleshow/52047838.cms Chaki, D. (2016, June 1). Lafarge cuts India buyers’ list to five. Financial Express, Retrieved 14 September 2016, from www.financialexpress.com/industry/companies/lafarge-cuts-india-buyers-list-to-five/270601/ Gangal, N. (2016, July 11). LafargeHolcim to sell Lafarge India assets to Nirma for $1.4 bn. Forbes India, Retrieved 18 September 2016, from www.forbesindia.com/article/special/lafargeholcim-to-sell-lafarge-india-assets-to-nirma-for-$1.4-bn/43743/1#ixzz4KlkprFNM Huet, N & Baghdjian, A. (2014, April, 4). Cement groups Lafarge, Holcim in $50 billion-plus merger talks. Reuters, Retrieved 19 September, 2016, from www.reuters.com/article/us-lafarge-holcim-idUSBREA3314L20140404 Jolly, D. (2014, April). Antitrust hurdles loom large for giant cement merger. The New York Times, Retrieved 25 September 2016, from www.dealbook.nytimes.com/2014/04/07/cement-makers-holcim-and-lafarge-agree-to-merge/?_r=0 Patel, D. (2016, April 14). Holcim-Lafarge merger hits competition tribunal wall. Business Standard, Retrieved 14 September 2016, from www.business-standard.com/article/companies/holcim-lafarge-merger-hits-competition-tribunal-wall-116041300459_1.html Pillay, A. (2016, June 15). Nirma to buy Lafarge India assets from LafargeHolcim for $1.4 billion. LiveMint, Retrieved 14 September 2016, from www.livemint.com/Companies/hGXG78x0Jqvbo8iS1eokPP/Nirma-to-buy-Lafarge-India-assets-from-LafargeHolcim-at-14.html Revill, J. (2015, November, 26). LafargeHolcim plans $3.5 billion in cement asset sales. The Wall Street Journal, Retrieved 20 September 2016, from www.wsj.com/articles/lafargeholcim-sales-miss-forecasts-1448433793 Schneider, D. (2016, September 4). LafargeHolcim vs Anhui Conch. Swissquote, Retrieved 6 October 2016, from www.static.swissquote.info/magazine/40/en/#/19

Annual report. (2015, March 23). Lafarge, Retrieved 6 October 2016, from www.lafarge.com/sites/default/files/atoms/files/03232015-press_publication-2014_annual_report-uk.pdf Cement industry in India. (n.d.). India Brand Equity Foundation, Retrieved 15 September 2016, from www.ibef.org/industry/cement-india.aspx Cement Segment. (n.d.). China National Building Materials, Retrieved 19 October 2016, from www.cnbmltd.com/en/ywbk/index.jsp Cemex, S.A.B. de C.V. Company Information. (n.d.). Hoovers, Retrieved 20 October 2016, from www.hoovers.com/company-information/cs/company-profile.cemex_sab_de_cv.241c59c314c8de50.html Consolidating the cement industry – brick by brick. (2012, September 8). Consult Club IIM Ahmedabad, Retrieved 24 October 2016, from http://consultclub-iima.com/?p=303 Creating the most advanced group in the building materials industry. (2015, May). LafargeHolcim, Retrieved 29 September 2016, from www.lafargeholcim.com/sites/lafargeholcim.com/files/atoms/files/05292015-finance_publication-investor_presentation_project_merger_lafargeholcim.pdf ENS Economic Bureau. (2016, May 10). Last hurdle over in sale of Lafarge cement biz, Dalmia cement withdraws appeal from Compat, The Indian Express, Retrieved 14 September 2016, from www.indianexpress.com/article/business/companies/dalmia-cement-lafarge-cement-sale-2792505/ Global overview. (n.d.). Cement Manufacturers’ Association, Retrieved 5 October 2016, from www.cmaindia.org/cms/global-overview.php HeidelbergCement AG company information. (n.d.). Hoovers, Retrieved 20 October 2016, from www.hoovers.com/company-information/cs/company-profile.heidelbergcement_ag.74260739e50b220d.html Holcim and Lafarge obtain merger clearances in the United States and Canada paving the way to closing their merger. (2015, April 5). LafargeHolcim, Retrieved 5 October 2016, www.lafargeholcim.com/holcim-and-lafarge-obtain-merger-clearances-united-states-and-canada-paving-way-closing-their-merger#ixzz4OGZoseon Lafarge confirms that Lafarge and Holcim are in advanced discussions regarding a possible combination. (2014, April 4). LafargeHolcim, Retrieved 23 September 2016, from www.lafargeholcim.com/lafarge-confirms-lafarge-and-holcim-are-advanced-discussions-regarding-a-possible-combination#ixzz4KDg4KW74 LafargeHolcim cuts 250 jobs as it completes merger. (2016, September 16). Global Cement, Retrieved 27 September 2016, from www.globalcement.com/news/item/5300-lafargeholcim-cuts-250-jobs-as-it-completes-merger LafargeHolcim reports Q2 2016 results. (2016, May 8). LafargeHolcim, Retrieved 18 September 2016, from www.lafargeholcim.com/lafargeholcim-reports-q2-2016-results#ixzz4KDb5sBfE LafargeHolcim to pay farmers Euro270,000 for pollution in Slovenia. (2016, October 18). Global Cement, Retrieved 19 October 2016, from www.globalcement.com/news/item/5402-lafargeholcim-to-pay-farmers-euro270-000-for-pollution-in-slovenia LafargeHolcim ups stake in ACC, Ambuja cements for $320 mn. (2016, November 15). VC Circle, Retrieved 15 November 2016, from www.vccircle.com/news/commodities/2016/11/15/holcim-ups-stake-acc-ambuja-cements-320-mn Market outlook of the global cement industry. (2016, January). Technavio, Retrieved 1 October 2016, from www.technavio.com/report/global-metals-and-minerals-cement-industry-outlook-market Media releases - Merger project. (n.d.). LafargeHolcim. Retrieved 18 September 2016, from www.lafargeholcim.com/media-releases Number of plants of selected top cement producers in 2016. (n.d.). Statista, Retrieved 5 October 2016, from www.statista.com/statistics/298776/cement-producers-number-of-plants/ Our history. (n.d.). LafargeHolcim, Retrieved 18 September 2016, from www.lafargeholcim.com/our-history World demand for cement to reach 4.7 billion metric tons in 2017. (2013, November 30). The Free Library, Retrieved 5 October 2016, from www.thefreelibrary.com/World+demand+for+cement+to+reach+4.7+billion+metric+tons+in+2017.-a0356141298

This case was developed from published sources, solely as the basis for class discussion. It is not intended to serve as endorsements, sources of primary data, or illustrations of effective or ineffective management. The detailed Teaching Note for this case is available with the authors. The instructors wanting to use this case in their class can write to the authors for teaching note.