|

Muhammad Kashif Majeed PhD Scholar College of Business Administration, Liaoning Technical University, China |

Ji Cheng Jun Professor College of Business Administration, Liaoning Technical University, China |

Muhammad Mohsin PhD Scholar College of Business Administration, Liaoning Technical University, China (Corresponding Author) |

Muhammad Zeeshan Rafiq PhD Scholar College of Business Administration, Liaoning Technical University, China |

Shazia Salamat PhD Scholar College of Business Administration, Liaoning Technical University, China |

This research paper has two objectives. First, to evaluate the market risk, exchange rate risk, and interest rate risk sensitivities (coefficients) of Pakistan listed banking companies. Second, it estimates the relationship between market measure of risk and corporate decision variables (accounting financial ratios). The data of market, exchange rate and interest rate risks on monthly basis while the date of accounting variables annuals basis. The span period of data is 2008 to 2018. The OLS econometric technique is used to find the result of this research. The result of first step shows that the market risk sensitivities are positively significant at 1% level for all banks in the sample while the exchange rate risk rare significant but the interest rate risk betas complete insignificant in all banks. So in second step only market risk sensitivities are regress with accounting variables. The accosting variables deposit of customer, investment and non-interest income significant at 5% and 10% level while the other variables insignificant. This study is helpful for banks' regularity authority, depositor, policymaker and as well as Government.

Keywords: accounting ratios, risks, and OLS

This empirical study describes market measures of risk and accounting-based financial ratios performance of Pakistani’s banks, in finding and analyzing evidence about firm financial, for fundamental investment decisions are used ratios and market sensitivities. The empirical confirmation found in the previous literature is based on Japan banking system on Secondary data (Elyasiani & Mansur, 1998; Abimbola & Olusegun, 2017). This research paper attempts to find relationship between market measures of Risk and cooperative decision variables i.e. accounting variables by using bank-specific data of Pakistan. It can observe relationship of a bank’s financial sensitivities and market measure of risk, like that if bank changes its financial strategies systematic risk measured, beta changes on market acuity which is effect on the firm/ bank, it is linked by corporate decision and capital market. In this study it’s very important to awareness about financial ratios and market measures of risk sensitivities. The connection between market and accounting variables are very wide research in accounting and finance literature. The difference between the rates of interest and more profitable banker lends to others. Commercial banks operate on commercial basis. The first and foremost goal for banks to earn profit, but a central bank is a goal to protect the interests of country and be aware market sensitivities (ADUBI & OKUNMADEWA , 1999; AKEL, 2014). The Bank is amid way party between debtors and investors. According to Crowther, 'forgive a bank or savings that are out of their income from those who collect money. It lends to those who need it "Banking Sector centuries now one of the pillars of economic success (AKEL, 2014; Patterson, Watts, & Gill, 2002). The history of the imperial colonies newly acquired banks that provide finance for projects about how to give you some information? The time and cost savings with banks to provide an avenue for both have an essential role in relationship among some variables (interest, Exchange, Market risk and accounting variables). The inter-temporal capital asset pricing model (ICAPM) interest rate risk and accounting variables could unify the model (ICAPM) additional market risk. The variation in interest rate stands to move for investment chance (Abimbola & Olusegun, 2017; BEKAERT & HARVEY, 2000)Moreover, the implication of Arbitrage Pricing Theory (APT) can be responsible for data of interest rate (BHATTACHARYA & MUKHERJEE, 2006; Cushman , 2003; Cooper, Robinson, & Patall, 2011)and exchange rate risks and accounting variables are priced factor in the balance charge of bank stock. Market exchange and interest rate risks are in pricing the US commercial bank stock returns(BEKAERT & HARVEY, 2000)(Bartram , Brown, & Minton, 2007). The factor model tests it under conditional and unrestricted frameworks (ADUBI &OKUNMADEWA , 1999). In Asian countries systematic risk less substantial than firm-specific risk (Huy, 2017; KANDIL, 2004). When the foreign exchange risk increases, then interest rate risk decreases(Olugbenga , 2012; Phylaktis & Ravazzolo, 2006) in major cause variations in exchange, interest, and market risk to bank’s operation and bank boost the size dramatically. Many banks face failure in financial crises of 2007 to 2008.Including largest bank of the world and other banks also affected by these crises(Kazerooni & Feshari, 2009; Naseem, Mohsin, & Salamat, 2018). Where banking business avoid the interest and would still operate for profit. Banks are divided in two major forms: central bank and commercial banks. Both forms of bank control the whole circulation of money in a country. We work on commercial banks in Pakistan so now history of Pakistani commercial bank must be explained. Banking system established in Pakistan after partition of 1947. With the strong support of State bank Habib bank established in 1947. 195 branches of bank help out-state bank to keep financial stability. Then National bank, HabibBank and Allied bank were started operation in newly Islamic republic Pakistan (Naseem, Mohsin, & Salamat, 2018; Pan, Wing Fok, & Liu, 2006) Commercial banks work favorably until 1974 in Pakistan. During 1980 to1990 financial sector’s services limited to the large corporation business, the government and politicians of banks privatized almost 23 banks established in which 10 banks were domestically licensed. A sense of hard competition occurred among 21 domestic and27 foreign banks; particularly administrated interest rates, exchange rate and market rate were smooth. He compels government to derive at market resolute rates. Period of 1997 to 2006 the amendment occur in banking companies ordinance(1962) state bank of Pakistan act(1956), improved prudential framework set up in 1989.

In this study, rechecks important and often disputed theoretical and empirical issues. This research is basically focused on issues choice of interest rate in exchange rate and accounting variables determination model correlations, unit roots, familiar cycle and stability using monthly data from 1980 to 1997 for exchange rate between U.S dollar and the following currencies British pound (GBP) Japanese (YEN) Canadian dollar (CAD) (Chamberlain, Howe, & Popper, 1997; Gaul & Palvia, 2013). These studies recheck some unsettled theoretical and empirical issues in respect of relationship between nominal exchange rate and interest rate variations. The model forecast that differential appreciations home currency due to growth in interest rate.And then (Cooper, Robinson, & Patall, 2011; Destek, 2015; Dimitrova, 2005) describes that not only conditional although unconditional framework has an impact on developing and estimating a multifactor model on US banking sector (Mohsin et al., 2018;Naseem et al., 2019) (Naseem et al., 2018; Lan et al., 2019; Rafiq et al., 2019) For the checking of the relationship among these factors three-factor methods are used. According to NLSUR via GMM the interest rate risk is an unconditional element. Results of this study are that interest rate risk premium is found to be the most important one in explaining the forces at work of the US bank portfolio return, among three time-varying risk premia. Some previous articles have examined the impact of different factors on Pakistani banking sectors. For instance, (Enisan, 2017; Hamrita & Trifi , 2011) proof conduct that significantly declining in the US banking sectors in the traditional banking business managing of Accepting deposits and making loans. (Hatemi & Irondust, 2007; Huy, 2017; Jorion, 2013; Priestley & Ødegaard, 2003) This paper is related to the data of four South Asian countries which explained the relationship between stock prices, exchange rates, and accounting variables applied same model test between stock prices and exchange rates long run and short run to check the association. This study goes to test relation among interest rate, exchange rate, market measures of risk and accounting variables through using Pakistani banks data.

Empirical confirmation found in the previous literature is based on Japan banking system on Secondary data. This research paper attempts to find a relationship between market measures of Risk and cooperative decision variables, i.e. accounting variables by using bank-specific data of Pakistan. The operating system of Pakistan listed banks and Japanese banks are not similar in terms of Structure and Management. This study found on the Pakistani listed banking system, provide the necessary evidence of the banking sensitivities to Exchange rate, Interest rate and market risk as well as find the relationship between these variables sensitivity and the accounting variables.

This study would be helpful for Pakistanis as well as foreign investors, bankers, academic communities and Investors & potential investors will get to understand whether changes to forecast the banks stock return prices by using foreign exchange rate, interest rate, market risk, and bank specified ratio. Objectives of the study To estimation the sensitivities of interest, exchange, and market risk of bank stock returns. To check relations of exchange, interest, Market risk sensitivities, and accounting variables. Hypothesis Development H0(i) =There is no relationship between exchange rate, interest rate, market risk, and bank stock returns. H1(i)= There is a relationship between exchange rate, interest rate, market risk, and bank stock returns. H0(ii) =There is no relationship between exchange rate, interest rate, market risk sensitivities,, and accounting variables. H1(ii)= There is a relationship between exchange rate, interest rate, and market risk sensitivities and accounting variables.

In this study, the sample of 11 banks is used which is listed on Pakistan stock exchange. The convenient sampling technique is used to select the sample size of the banks because the lack of availability of the data

The secondary data used to conclude the above objective of this study. This data is collected from a different site like as Pakistan stock exchange, state Bank of Pakistan, Banks annuls reports and from previous literature

The date span period is 10 year from January 2008 to December 2018. The date of the exchange rate, interest rate, market risk, and banks stock return is collected on monthly basis, but the data of accounting variables is annually basis.

The Eviews 10 software is used to find this above objective of this study.

First, in this study the multiply regression is used to find out the link between exchange rate, interest rate, Market risk, and bank stock returns. This model is also used by (Naseem, Mohsin,& Salamat, 2019; BEKAERT & HARVEY, 2000)this step found out the sensitivities of exchange rate, interest rate, and market risk. In second step isfound out the association between market measures of risk and accounting variables. The marketmeasures variables sensitivities which appear on the left-hand side of the model and the accounting variables on right-hand side as explanatory variables (Nieh & Lee, 2001; Qazi, Ahmed, & Mudassar , 2012). The second step cross-sectional, using OLS method.

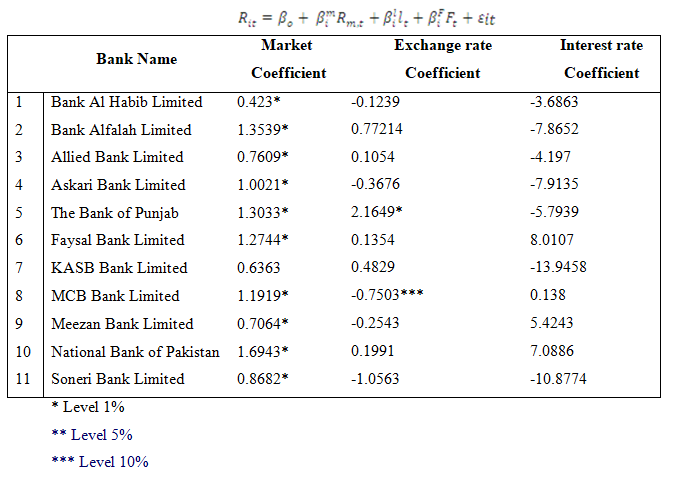

The first step econometric model is following R_it=β_o+ β_i^m R_(m,t)+β_i^l l_t+β_i^F F_t+εit………..(1) R_it= dependent variable;R_(m,t) =independent variable;l_t =interest rate; F_t=Foreign exchange rate;εit= Standard error;β_o = bank stock returns;β_i^m,β_i^l,β_i^F stand for regression coefficient The second step econometric models as follows Market risk beta model βm=β0+β1CASH+β2INS+β3 DEP+β4II+β5NII+β6IE+β7NIE+V…… (1) βm=dependent variable; Cash=independent variables; INS=Investment; DEP =Deposit of customer; II = interest income; IE = interest Expense; NII = Non interest Income; NIE = Non interest Expense;V = Standard error. Whereas “β_o” is the β_m Interceptβ1, β2, β3,β4, β5, β6 and β7 in research model stand for slop or regression coefficient “e” is a random error. Exchange Beta Model βF=β0+β1IE+β3INS+β4NIE+β5NII+V….. (2) βF = Dependent variable (Foreign Exchange); INE= Interest Expense; II=Interest Income; INS=Investment; NII=NonInterestIncome; NIE=NonInterest Expense; V=Standard error.Whereas “β_o” is the βF Intercept β1, β2, β3, β4 and β5 in research model stand for slop or regression coefficient “e” is a random error. Interest Rate Beta Model β_(i= )^1 β0+β1IE+β2II+β3INS+β4NIE+β5NII+V…….(3) β_i^l = Dependent variable (interest rate beta); IE=Interest Expense; II= Interest Income; INS= Investment; NII= Non-Interest Income; NIE=Non Interest Expense; V=Standard error. Whereas “β_o” is theβ_i^lIntercept β1, β2, β3, β4, and β5in research model stand for slop or regression coefficient “e” is random error.

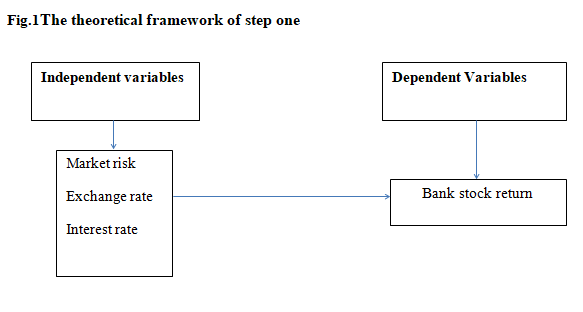

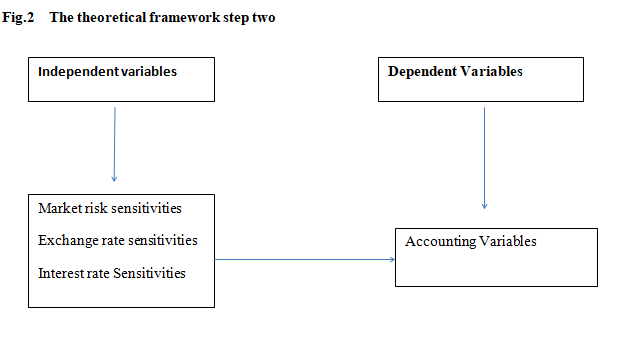

Figure#1 shows the conceptual framework of step one, and figure#2 shows the theoretical framework of second step of this study. Table #1 shows the results of descriptive statistics of all banks which is used in this study and market measure variables such as exchange rate, interest rate, and market risk. The monthly average return of all banks is between -0.119% to 2.147% with stander deviation 10.3762% to 26.8374% and the monthly performance of exchange rate, interest rate, and market risk is 0.228% to 1.9981% with standardization 0.2686% to 7.3852%. The value of the skewness is negative and blew 0 in six banks suchas (Elyasiani & Mansur, 2005; Hamrita & Trifi , 2011; Kallunki, 1997) and remaining four banks result shows the value of skewness positive and also the importance of market risk and interest rate negative but the exchange rate skewness value behave positively. The value of Kurtosis of all banks and market measure variables is more the 3 which shows that the data is not normally distributed expect of Bank Alfallahthis assumption is also clarified by jarque-bera test which is significant at 1% level to reject the null hypothesis for normality hope of one bank(Fizari, et al., 2011; Dimitrova, 2005; Zubair , 2013; Kamal & Haque, 2016). Table # 2 presented the result of step one. The OLS is estimated individually for all banks. The result of OLS shows that the market risk is positively significant at 1% level in all banks and the coefficient value are between 0.423 to 1.6943 which mean this empirical evidence reject the H0 (null hypothesis) at 1% level accept alternative hypothesis. The exchange rate is insignificant in all banks except MCB and Punjab bank the value of coefficient in some banks are positive, and some are negative based on this empirical evidence we cannot reject the H0 null hypothesis except of two banks. The interest rate result shows that the value of coefficient in all banks is insignificant but the value of coefficient in some bank positive and negative on the base of these results impossible to reject the H0 null hypothesis. After evaluation, the result of step one this research moves to step two. The result of step one table clearly shows that the market risk sensitivity is positively significant (Mohsin et al., 2019; Naseem et al., 2019a,b; Naseem et al., 2018a,b), but the two variables exchange rate interest rate beta is insignificant (Lawal & Ijirshar, 2013; Martin & Mauer, 2001). So in step two we just specified the market beta model to find the relationship between market risk-sensitive and accounting variables. The market beta model based on cross-sectional data. This type of model is also specified by (Elyasiani & Iqbal, 2005; Enisan, 2017). The result of table # 3 shows that no other variables are positive significant expect of deposit of customer, investment and non-interest expense at level 5% and 10%. On the basis of these result cannot reject the H0 null hypothesis and accept the alternative hypothesis.

Based on the results of this study following suggestions would be helpful to listed banks in Pakistan. Banks should develop a healthy relationship in interest, exchange; market risk and accounting variables because these variables mostly effect on foreign exchange risk management strategies and Pakistanis banks should be developing their management and structure system. Even though analytics results show market risk sensitivity is positively significant, but the two variables exchange rate interest rate beta are insignificant holding and financial performance of banks it would be suitable method to check the relationship of market sensitivities and also the market sensitive strong relation found with accounting variables.

The main objective of this study is to find the relationship between markets, interest, exchange rate betas, and accounting variables of Pakistan listed banks. Firstly it uses the Ordinary Least Squares (OLS) model for analysis. Secondly, to estimates the relationship between market measure of risk and accounting variables. The result of OLS shows that the market risk is positively significant at 1% level in all banks,but exchange rate risk is insignificant in all banks except MCB and BOP. The results of first stage show that all Pakistanis banks sample is sensitivities to Market and Exchange rate in a positive direction then the interest rate. In the second stage we just specified the market beta model to find the relationship between market risk sensitivities and accounting variables because those two variables are insignificant so could not move on for next analysis. The market beta model is based on cross-sectional OLS model. The result of market beta model shows that some accounting variables deposit of customer, investment and non-interest income significant at 5% and 10% level while the other variables insignificant.

The recently study emphasize only Pakistanis listed banks and also found the relationship between limited variables. In Pakistan, many numbers of banks but this study focuses on listed Banks. The OLS econometric technique to use to found link but also many other models like as GARCH type family model better define the relation.

In this study investigate only Pakistanis banks, but future researcher could be including many countries banks comparison in this case of study. In prospective research I recommend to researcher in sample size include all banks as well as the contrast between some countries to use GARCH type of family model

1. Abimbola, A. B., & Olusegun, A. J. (2017). Appraising The Exchange Rate Volatility, Stock Market Performance, And Aggregate Output Nexus In Nigeria. Business And Economics Journal, 12. 2. Adubi, A. A., & Okunmadewa, F. (1999). Price, Exchange Rate Volatility And Nigeria's Agricultural Trade Flows A Dynamic Analysis. African Economic Research Consortium, 50. 3. Akel, G. (2014). Relationship Between Exchange Rates And Stock Prices In Transition Economies Evidence From Linear And Nonlinear Causality Tests. Economics & Finance Conference, Vienna, 13. 4. Bartram, S. M., Brown, G. W., & Minton, B. A. (2007). Resolving The Exposure Puzzle: The Many Facets Of Exchange Rate Exposure. Fdic Center For Financial Research, 62. 5. Bekaert, G., & Harvey, C. R. (2000). Foreign Speculators And Emerging Equity Markets. The Journal Of Finance, 50. 6. Bhattacharya, B., & Mukherjee, J. (2006). Causal Relationship Between Stock Market Exchange Rate, Foreign Exchange Reserves AndValue Of Trade Balance: A Case Study For India. International Journal Of Economics And Financial Issues, 24. 7. Cooper, H., Robinson, J. C., & Patall, E. A. (2011). Does Homework Improve Academic Achievement? A Synthesis Of Research 1987–2003. American Educational Research Association, 63. 8. Cushman, D. O. (2003). A Portfolio Balance Approach To The Canadian-U.S. Exchange Rate. International Review Of Economics And Finance, 39. 9. Destek, M. A. (2015). Nuclear Energy Consumption And Economic Growth In G-6 And Management. International Journal Of Energy Economics And Policy, 6. 10. Dimitrova, D. (2005). The Relationship Between Exchange Rates And Stock Prices: Studied In A Multivariate Model. Issues In Political Economy, Vol. 14, August 2005, 25. 11. Enisan, A. A. (2017). Determinants Of Foreign Direct Investment In Nigeria: A Markov Regime-Switching Approach. Determinants Of Foreign Direct Investment In Nigeria, 28. 12. Hamrita, M. E., & Trifi, A. (2011). The Relationship Between Interest Rate, Exchange Rate And Stock Price: A Wavelet Analysis. International Journal Of Economics And Financial Issues, 9. 13. Hatemi, A. J., & Irondust, M. (2007). On The Causality Between Exchange Rates And Stock Prices:A Note. Bulletin Of Economic Research, 7. 14. Huy, T. Q. (2017). The Linkage Between Exchange Rates And Stock Prices: Evidence From Vietnam. Asian Economic And Financial Review, 11. 15. Jorion, P. (2013). The Pricing Of Exchange Rate Risk In The Stock Market. The Journal Of Financial And Quantitative Analysis, 15. 16. Kamal, J. B., & Haque, A. E. (2016). Dependence Between The Stock Market And Foreign Exchange Market In South Asia: A Copula-Garch Approach. The Journal Of Developing Areas, 22. 17. Kandil, M. (2004). Exchange Rate Fluctuations And Economic Activity In Developing Countries: Theory And Evidence. Journal Of Economic Development, 24. 18. Kazerooni, A. R., & Feshari, M. (2009). The Impacts Of The Unified Exchange Rate System On Domestic Price In Iran. Iranian Economic Review, 26. 19. Lawal, M., & Ijirshar, V. U. (2013). Empirical Analysis Of Exchange Rate Volatility And Nigeria Stock Market Performance. International Journal Of Science And Research, 9. 20. Martin, A. D., & Mauer, L. J. (2001). Exchange Rate Exposures Of Us Banks Exchange Rate Exposures Of Us Banks. Journal Of Banking & Finance, 15. 21. Naseem, S., Mohsin, M., & Salamat, S. (2018). Does Exchange Rate Affect The Karachi Stock Market Prices In Pakistan? Asian Journal Of Research, 8. 22. Naseem, S., Mohsin, M., & Salamat, S. (2018). Impact Of The Inflation Rate, Current Balance On Pakistan Gdp. Asian Journal Of Research, 8. 23. Naseem, S., Mohsin, M., & Salamat, S. (2019). Asymmetric Effect And Exchange Rate Volatility: Evidence From Pakistan. Social Science And Humanities, 6. 24. Nieh, C. C., & Lee, C. F. (2001). The Dynamic Relationship Between Stock Prices And Exchange Rates For G-7 Countries. The Quarterly Review Of Economics And Finance, 14. 25. Olugbenga, A. A. (2012). Exchange Rate Volatility And Stock Market Behaviour: The Nigerian Experience. European Journal Of Business And Management, 10. 26. Pan, M. S., Wing Fok, R., & Liu, Y. A. (2006). Dynamic Linkages Between Exchange Rates And Stock Prices Evidence From East Asian Markets. International Review Of Economics And Finance, 18. 27. Patterson, R., Watts, K., & Gill, T. (2002). Micro-Particles In Recirculating Aquaculture Systems: Determination Of Particle Density By Density Gradient Centrifugation. Aquacultural Engineering, 11. 28. Phylaktis, K., & Ravazzolo, F. (2006). Stock Prices And Exchange Rate Dynamics. Journal Of Monetary Economics, 37. 29. Priestley, R., & Ødegaard, B. A. (2003). Exchange Rate Regimes And The Price Of Exchange Rate Risk. Forthcoming In Economics Letters, 9. 30. Qazi, A. Q., Ahmed, K., & Mudassar , M. (2012). Disaggregate Energy Consumption And Industrial Output In Pakistan: An Empirical Analysis . Economics Letter, 16. 31. Zubair, A. (2013). Causal Relationship Between Stock Market Index And Exchange Rate: Evidence From Nigeria. Cbn Journal Of Applied Statistics, 24. 32. Mohsin, M., Naiwen, L., Majeed, M. K., & Naseem, S. (2018, July). Impact Of Macroeconomic Variables On Exchange Rate: An Evidence From Pakistan. In International Conference On Applied Economics (Pp. 325-333). Springer, Cham. 33. Naseem, S., Rizwan, F., Abbas, Z., & Zia-Ur-Rehman, M. (2019). Impact Of Macroeconomic Variables On Pakistan Stock Market. Dialogue (1819-6462), 14(2). 34. Naseem, S., Mohsin, M., Zia-Ur-Rehman, M., & Baig, S. A. (2018). Volatility Of Pakistan Stock Market: A Comparison Of Garch Type Models With Five Distribution. Amazonia Investiga, 7(17), 486-504. 35. Rafiq, M. Z., Jun, J. C., Naseem, S., & Mohsin, M. (2019). Impact Of Market Risk, Interest Rate, Exchange Rate On Banks Stock Return: Evidence From Listed Banks Of Pakistan. Amazonia Investiga, 8(21), 667-673. 36. Lan, V. T., Fu, G. L., Naseem, S., & Mohsin, M. (2019). An Empirical Analysis Between Macroeconomic Variables And Gold Prices. International Journal Of Recent Technology And Engineering (Ijrte), 5-9. 37. Mohsin, M., Naseem, S., Muneer, D., & Salamat, S. (June 2019). The Volatility Of Exchange Rate Using Garch Type Models With Normal Distribution: Evidence From Pakistan. Pacific Business Review International, 124- 129 Volume 11 Issue 12. 38. Naseem, S., Fu, G. L., Lan, V. T., Mohsin, M., & -Ur-Rehman, M. Z. (January 2019b). Macroeconomic Variables And The Pakistan Stock Market: Exploring Long And Short-Run Relationships. Pacific Business Review International, 62-72 Volume 11 Issue 7, . 39. Naseem, S., Mohsin, M., & Salamat, S. (2018b). Does Exchange Rate Affect The Karachi Stock Market Prices In Pakistan? Asian Journal Of Research , 8. 40. Naseem, S., Mohsin, M., & Salamat, S. (2018a). Impact Of The Inflation Rate, Current Balance On Pakistan Gdp . Asian Journal Of Research. 41. Naseem, S., Mohsin, M., & Salamat, S. (2019a). Asymmetric Effect And Exchange Rate Volatility: Evidence From Pakistan. Social Science And Humanities, 6.

|

Banks |

Mean |

Median |

Std. Dev. |

Skewness |

Kurtosis |

Jarque-Bera |

Probability |

|

Bank Al Habib |

0.006364 |

0.01805 |

0.103762 |

-0.678241 |

3.992692 |

14.12739 |

0.000856 |

|

Bank Alfallah |

0.003239 |

0.010431 |

0.127653 |

-0.244588 |

3.676989 |

3.488037 |

0.174816 |

|

Allied Bank Limited |

0.015621 |

0.011376 |

0.121729 |

-0.078432 |

5.502596 |

31.43796 |

0 |

|

AskariBank Limited |

-0.00224 |

0.005019 |

0.12711 |

-0.86353 |

4.455147 |

25.50093 |

0.000003 |

|

The Bank of Punjab |

0.002947 |

-0.00563 |

0.16771 |

0.653859 |

5.503334 |

39.88403 |

0 |

|

FaysalBank Limited |

-0.00119 |

0 |

0.126236 |

-0.298243 |

6.050107 |

48.29476 |

0 |

|

KASB Bank Limited |

0.016713 |

-0.003 |

0.268374 |

2.335703 |

16.46253 |

1015.308 |

0 |

|

MCB Bank Limited |

0.02147 |

0.012511 |

0.121268 |

-0.402215 |

4.790228 |

19.26012 |

0.000066 |

|

MeezanBank Limited |

0.012814 |

-0.00133 |

0.109317 |

1.215605 |

8.919236 |

204.7407 |

0 |

|

National Bank of Pakistan |

0.009825 |

0.00085 |

0.139624 |

0.025628 |

4.351807 |

9.15005 |

0.010306 |

|

Soneri Bank Limited |

0.000701 |

-0.00485 |

0.173836 |

1.017904 |

9.269223 |

217.2383 |

0 |

|

Market Risk |

0.017423 |

0.019981 |

0.073852 |

-1.240894 |

8.462769 |

180.0056 |

0 |

|

Exchange Rate |

0.005225 |

0.00228 |

0.012181 |

1.674807 |

9.794667 |

286.9371 |

0 |

|

Interest Rate |

0.007964 |

0.007841 |

0.002686 |

-0.987565 |

3.424048 |

20.40478 |

0.000037 |

|

Independent Variables |

beta values |

|

Cash |

0.015456 |

|

Deposit of customer |

0.422052** |

|

Investment |

-0.37275** |

|

Interest expense |

0.092733 |

|

Interest income |

-0.31688 |

|

Non-interest expense |

0.178544*** |

|

Non-interest income |

0.089985 |